Followers of the US OCS oil and gas program have observed some impressive chutzpah over the years, but a new law suit challenging the extension of Santa Ynez Unit leases raises the bar.

Groups that helped block every attempt to resume production in the Santa Ynez Unit are now suing to terminate the leases for non-production.Brilliant!🥇

“Without these extensions, each of the leases would have expired and ExxonMobil would have been required to permanently cease its oil and gas operations, plug its wells, and decommission its other infrastructure.”See the full text of the law suit.

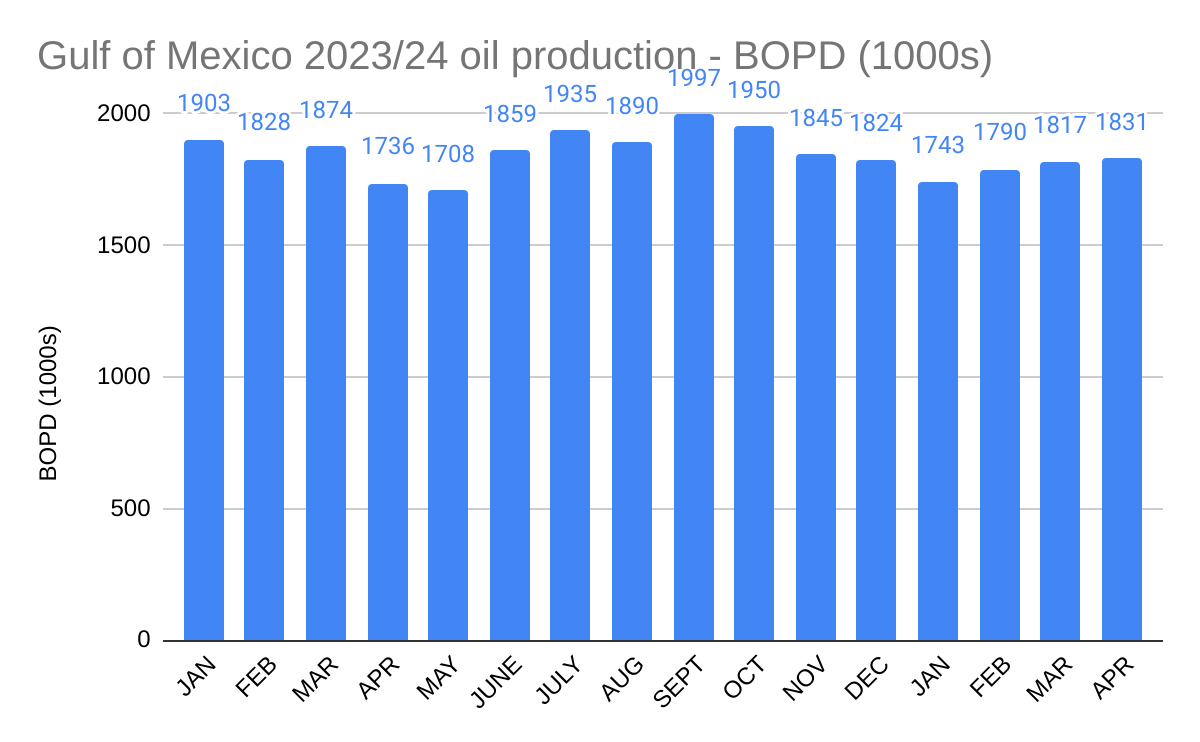

EIA has released the April oil production data. The Federal waters of the Gulf of Mexico produced 1.831 million BOPD in April, which is essentially level with corrected March production (1.817 million).

GoM production fell more than 12% from nearly 2 million BOPD in September 2023 to 1.743 million BOPD in January 2024 before climbing back to 1.8 million BOPD over the past 3 months (see chart below). What’s up?

The mysterious Main Pass Oil Gathering (MPOG) system shutdown in November 2023 no doubt contributed to the decline, but that system was reported to be fully online in April. Based on the GoM data, the MPOG shutdown may have reduced production by 50-80,000 BOPD. That would account for less than half of the GoM decline since Sept 2023.

We may learn more about the MPOG shut-in volumes when the NTSB investigation report is published. (Don’t expect a report soon. The NTSB report on the Huntington Beach pipeline spill took nearly 2 years to complete. The final NTSB report on the deadly December 2022 GoM helicopter crash has still not been issued.)

In 2022, EIA projected that additional GoM capacity would offset production declines, but would not sustain crude oil production at levels of 2.0 million BOPD. That forecast has proven to be accurate.

Bottom line: 1.8 million BOPD does in fact appear to be the current GoM production baseline. The GoM is thus significantly under-performing BOEM forecasts. This should be a concern to those who support responsible OCS production.

In a major decision, the Supreme Court overturned the Chevron doctrine, which for four decades led judges to defer to how federal agencies interpreted a law when its language wasn’t clear. In a later post, we will speculate on how this ruling could affect the offshore regulatory program.

One of the most important principles in administrative law, the “Chevron deference” was coined after a landmark case,Chevron U.S.A., Inc. v. Natural Resources Defense Council, Inc., 468 U.S. 837 (1984). The Chevron deference is referring to the doctrine of judicial deference given to administrative actions. In Chevron, the Supreme Court set forth a legal test as to when the court should defer to the agency’s answer or interpretation, holding that such judicial deference is appropriate where the agency’s answer was not unreasonable, so long as Congress had not spoken directly to the precise issue at question.

Carbon sequestration (i.e. subsurface disposal) is a controversial and divisive topic, and important questions regarding the costs and benefits remain. Nonetheless, the Infrastructure Bill of 2021 authorized the disposal of CO2 on the OCS, and stipulated that the Secretary of the Interior promulgate regulations for that purpose. However, that major task cannot be completed without a better understanding of the potential environmental impacts.

BOEM has announced a study (see attached pages from their new Environmental Studies Plan) to consider the potential for CO2 leakage and related environmental concerns. A few excerpts from BOEM’s summary follow:

Problem: Potential CO2 leakage from carbon sequestration (CS) project activities could occur via a number of pathways. Few studies model and/or measure CO2 leakage, transport, dispersion, attenuation, and environmental impacts in the offshore environment, and those that do exist are preliminary.

Intervention: BOEM needs more information about the dynamics, fate, transport, and potential environmental impacts of CO2 leakage under various scenarios, including worst-case, on the OCS to inform the new nationwide CS Program and to protect the environment from CO2 leakage.

Comparison: The study will model CO2 leakage under various scenarios, including worst-case scenarios, using the GOM OCS Region as a case-study and can be applied to all OCS regions. Outcome The leakage and worst-case scenario modeling will aid BOEM’s ongoing rulemaking efforts, program development and implementation, and future operational needs including NEPA analyses, lease planning, lease stipulations, consultations, plan and permit approvals, mitigation measures, risk assessment and monitoring requirements, etc. Study results will also provide direction for future studies to include field and/or laboratory analyses.

The performance period for this important study extends through 2027, so it’s hard to envision final CS regulations prior to that date. You can’t issue regulations without first assessing the potential harm that could result from their promulgation (as required by NEPA).

BOEM’s summary mentions “the anticipation of a CS lease sale in the GOM after final regulations are published.” Hopefully, this also means that BOEM will not permit improperly acquired oil and gas leases (Sales 257, 259, and 261) to be converted to CS leases.

“We will do everything we can to make sure that the market is supplied well enough to ensure as low price as possible for American consumers,” Hochstein told the newspaper. “I think that we have enough in the SPR if it’s necessary.” ~Amos Hochstein, Special Presidential Coordinator for Global Infrastructure and Energy Security.

Maybe they should remove “Energy Security” from his impressive title since that seems to be a low priority.

Apparently it’s fine (and environmentally friendly) to deplete strategic oil reserves to reduce prices prior to an election, but not to hold regular oil and gas lease sales in the adjacent Gulf of Mexico. 2024 will be the first year without an OCS lease sale since 1958, and the Administration bragged about the new 5 year leasing plan having the fewest proposed sales in history!

“Consistent with the requirements of the Inflation Reduction Act (IRA) concerning offshore conventional and renewable energy leasing, the Department of the Interior today published the final 2024–2029 National Outer Continental Shelf Oil and Gas Leasing Program (Program) with the fewest oil and gas lease sales in history.

These three lease sales are the minimum number that will enable the Interior Department’s offshore wind energy program to continue issuing leases in a way that will ensure continued progress towards the Administration’s goal of 30 gigawatts of offshore wind by 2030.”

The limited media coverage of the lawsuit originated from a single Reuters article. Apparently Reuters learned about the suit and reached out to the litigants. Their article quoted Louisiana Attorney General Liz Murrill as follows:

“This is a really egregious direct assault on intermediate level producers of oil and gas, and that affects a lot of business in our state,” Murrill told Reuters in an interview.

That quote is all we have from the AGs. Why the absence of announcements:

Interest in working with industry and the Federal govt to seek policy solutions that best address OCS decommissioning issues? (This would be encouraging.)

State of Louisiana, Louisiana Oil & Gas Association, State of Mississippi, State of Texas, Gulf Energy Alliance, Independent Petroleum Association of America and U S Oil & Gas Association

Defendant:

Deb Haaland, U S Dept of Interior, Bureau of Ocean Energy Management, Elizabeth Klein, Steve Feldgus and James Kendall

Case Number:

2:2024cv00820

Filed:

June 17, 2024

Court:

US District Court for the Western District of Louisiana

Presiding Judge:

James D Cain

Referring Judge:

Thomas P LeBlanc

Nature of Suit:

Other Statutes: Administrative Procedures Act/Review or Appeal of Agency Decision

Cause of Action:

28 U.S.C. § 2201 Constitutionality of State Statute(s)

California State Lands Commission decision on the pipeline right of ways (ROWs) in state waters. (Those ROWs had expired.)

Transfer of leases to Sable – Environmental groups, the California Coastal Commission and/or other parties could file suit challenging the transfer of the leases to Sable.

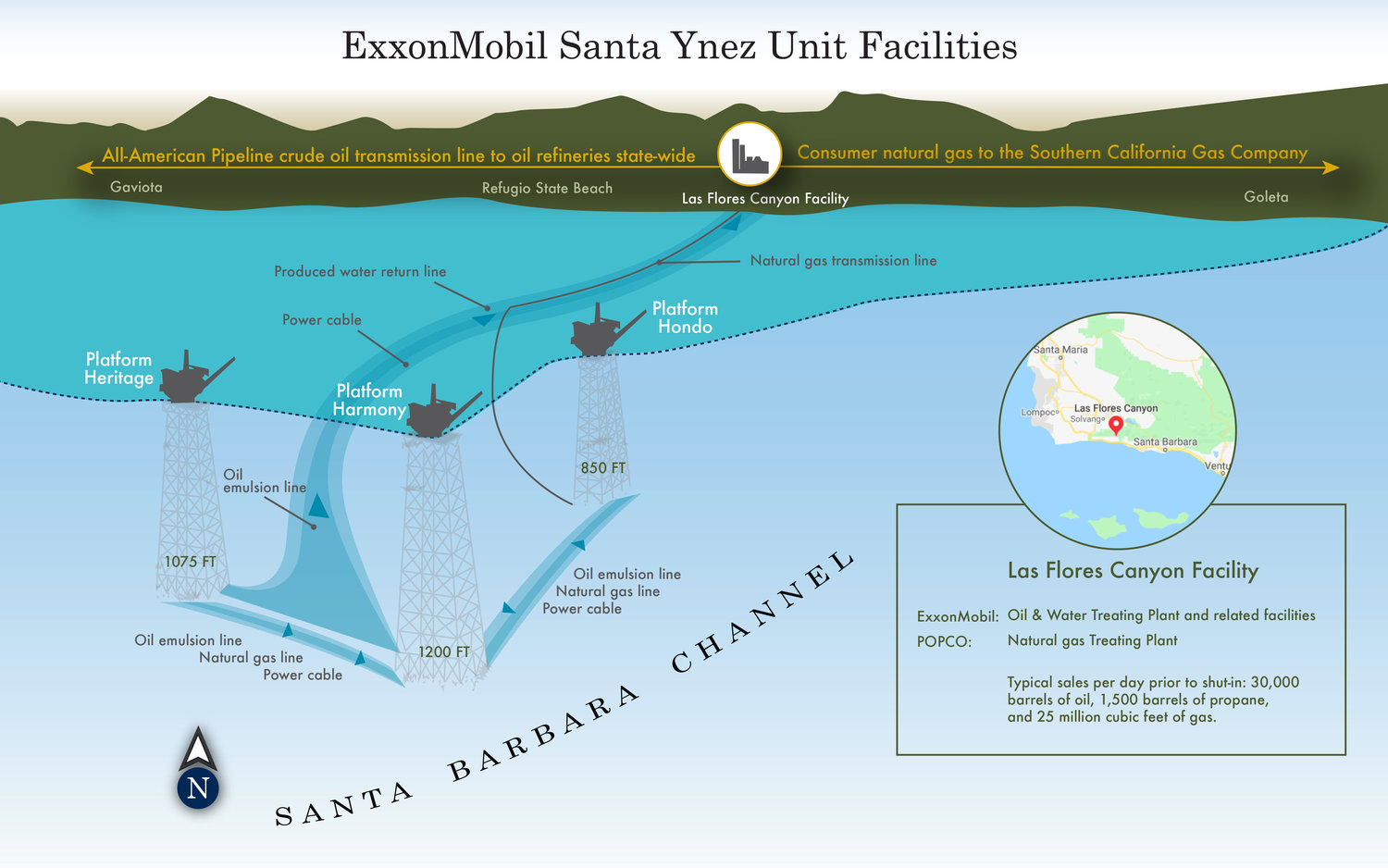

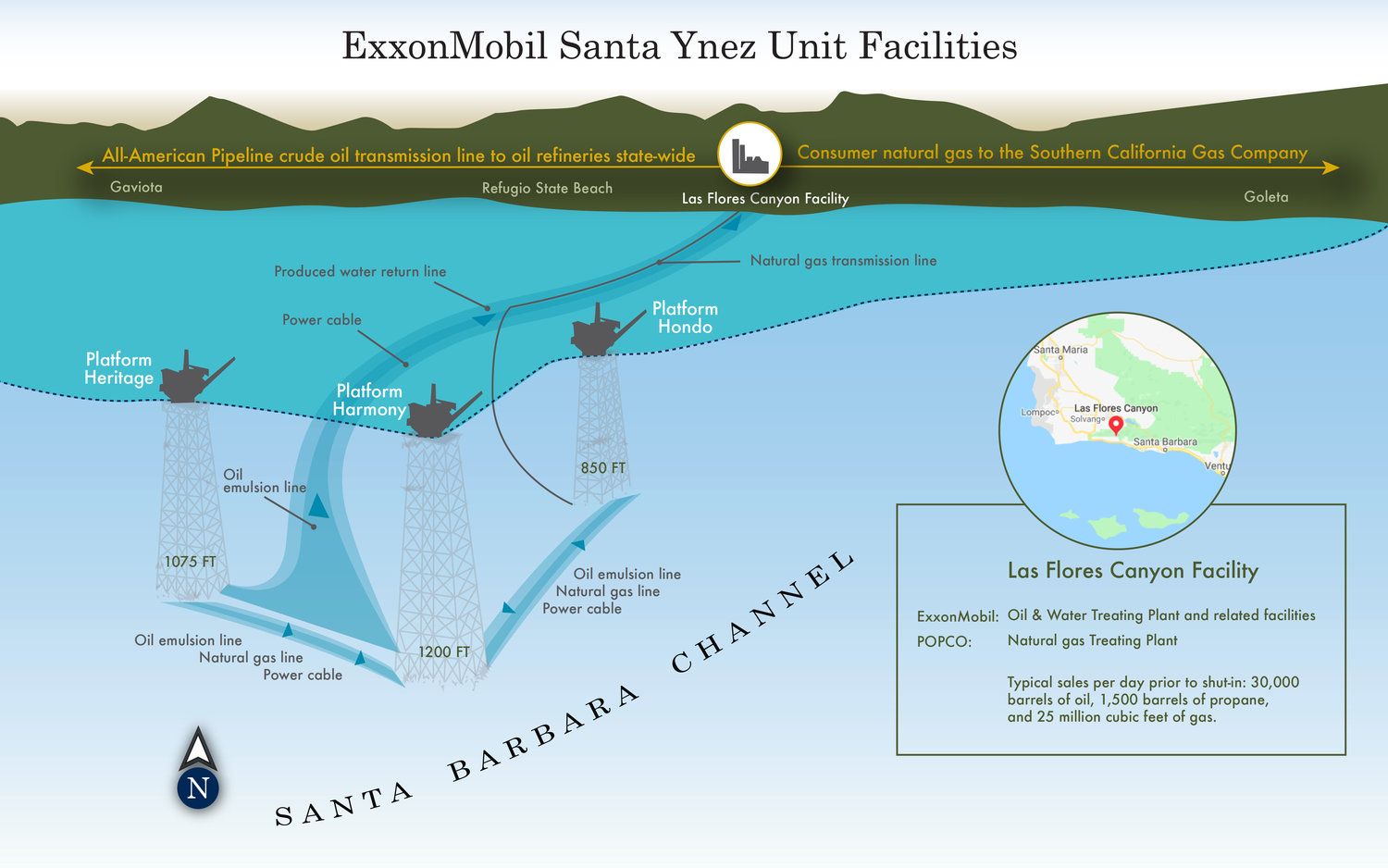

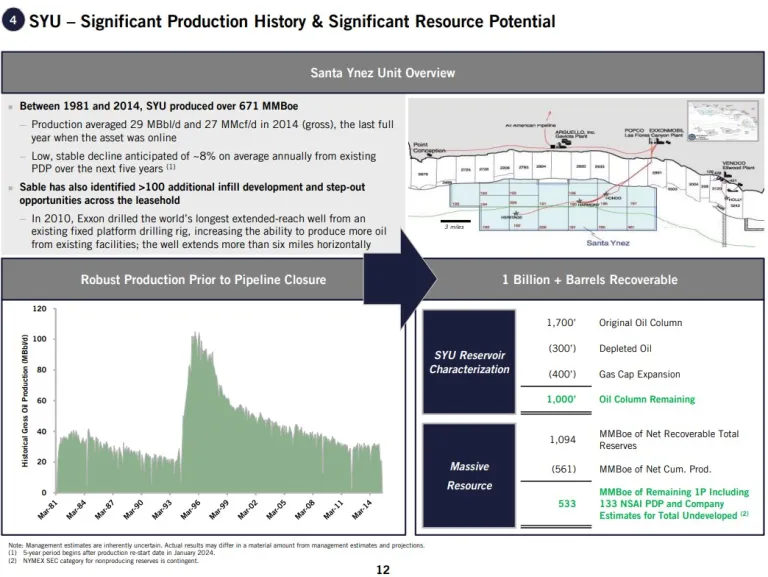

According to John, the question is not whether production will resume in 2024, but whether it will ever resume. And John reminds us that as of 1/1/2026, the SYU and all of the headaches revert to Exxon. See the SYU overview below:

This action figure of Willie Mays making his signature basket catch has been a prized possession since 1957. Baseball was, by far, the most important American sport back then and Willie was a megastar. I was a Phillies fan, but loved Willie, as did baseball fans everywhere. Below is a 7 minute video that nicely captures the man and his game.

From an offshore energy perspective, the US offshore program also had “rookie” status when Willie joined the Giants in 1951. BSEE’s borehole file lists 93 wells spudded prior to July 1, 1951 in what became the Federal waters of the Gulf. Per BOEM’s structures file, 27 platforms had been installed by that date. The Submerged Lands Act and OCS Lands Act were enacted 2 years later to provide a framework for the leasing and development that followed.