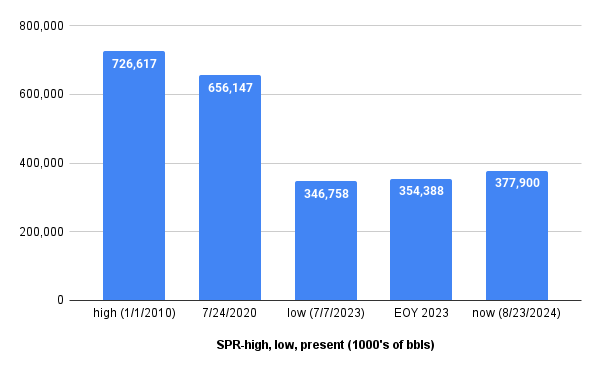

Given the relatively moderate oil prices during much of 2024, DOE has made some progress in adding to the Strategic Petroleum Reserve. However, the 31 million bbls added since July 2023 only amount to about 10% of the reserves withdrawn during the 3 years prior (July 2020 to July 2023) and about 4% of the SPR’s capacity.

10/31/2023: Citing economic factors, Orsted announces they “will cease development of the Ocean Wind 1 and Ocean Wind 2 projects.” (This should have resulted in termination of the leases.)

1/19/2024: Orsted requests a 2 year “suspension of operations” to extend the leases they had ceased developing. (Presumably, this was a hedge with hopes of marketing the leases or getting better terms.)

2/29/2024: True to form, BOEM approves the questionable 2 year suspension request. The approval letter was dated one day before the leases’ 8th anniversary when they would have presumably expired. (This is unconfirmed because the lease document and BOEM’s wind regulations lack clarity regarding lease expiration.)

BOEM’s approval letter (attached) curiously asserts that “suspension of the operations term is necessary for the Lessee’s full enjoyment of the lease in this circumstance to ensure sufficient time for project operations in support of the Project’s economic viability.” (Interesting wording that expresses the accommodative and promotional philosophy of the Federal wind program.)

8/14/2024: Cape May County comments that they are likely to amend their Federal Court filings “since the actions of the NJBPU would appear to have nullified Orsted’s federal permits.”

8/27/2024: Despite the fact that Orsted has ceased development and New Jersey has vacated its approvals, the Federal leases are still active.

Good luck keeping an oil and gas lease if you cease development and request a suspension of operations. BSEE will rightfully deny your request.

This real-life Spider-Man, seen on a Vineyard Wind turbine blade, is Tyler Paton. Tyler is an independent composite specialist who inspects and repairs blades on site. The Nantucket Current shared these images on X.

We sent our drone up to get a better look at what remains of the damaged blade on one of GE Vernova’s Haliade-X turbines at the Vineyard Wind lease area 15 miles southwest of Nantucket: pic.twitter.com/yynXpsunCv

The offshore safety regulator (BSEE) has a very capable technical staff and should produce an informed report on the Vineyard Wind blade failure. The concern is with the internal review process that has seriously delayed the publication of accident investigation reports and safety alerts.

Presumably, DNV, the Vineyard Wind CVA, will provide input into the BSEE investigation. Perhaps the effectiveness of the CVA process and quality control procedures should be separately considered.

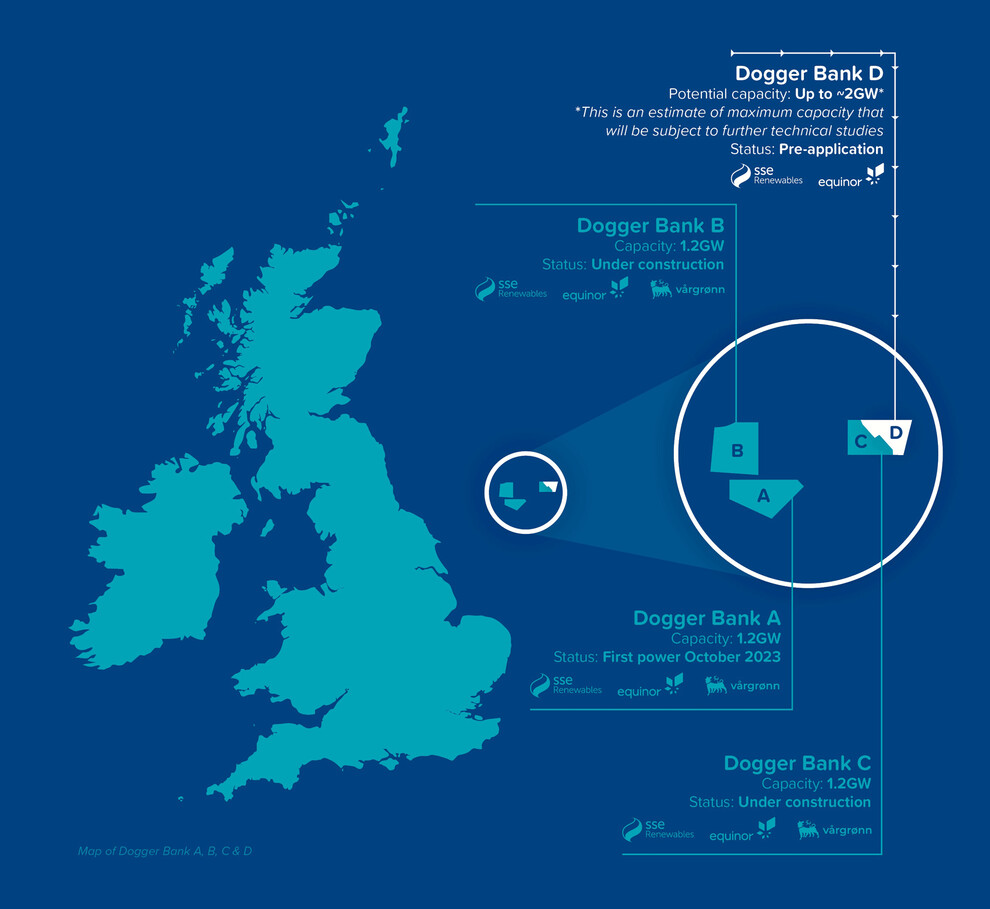

Will Equinor, a major oil and gas producer, Dogger Bank partner, and offshore wind advocate, be investigating the Dogger Bank failures?

A comprehensive International data base on turbine incidents and performance is needed.

As previously noted, offshore substations are large structures. A closeup of the Vineyard Wind 1 substation is pasted below.

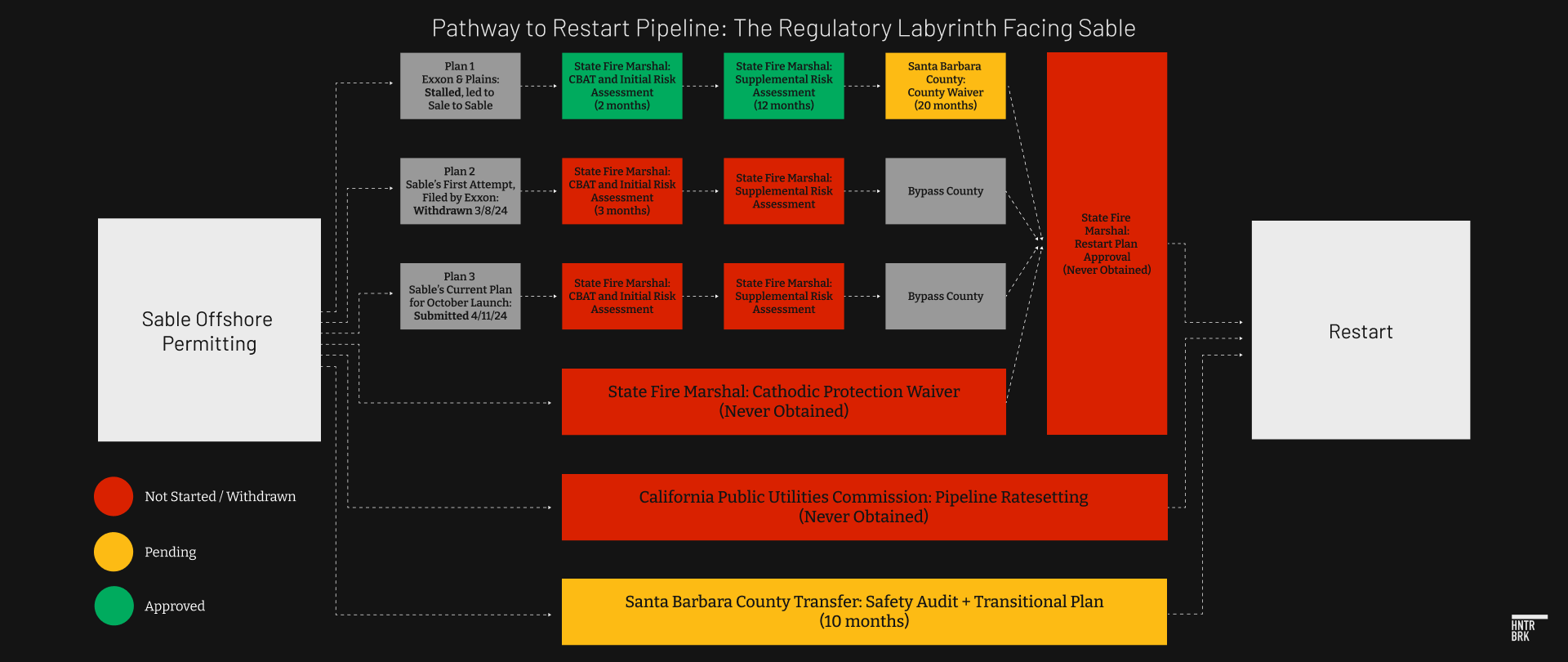

An assessment prepared for Hunterbrook Capital draws the same conclusions regarding the prospects for production, calling the restart “a pipe dream” (presumably the pun was intended given the pipeline permitting quagmire). Hunterbrook’s chart (pasted below) illustrates the regulatory labyrinth facing Sable.

Hunterbrook has also flagged Sable’s ability to continue as a “going concern.” That may be a valid concern, but Sable’s success is very much in Exxon’s best interest. Exxon must have evaluated Sable and been comfortable with their management. Otherwise, they wouldn’t have made the deal.

Does Exxon want the massive SYU headache to revert back to their portfolio, as provided for in their agreement with Sable, if production doesn’t restart by January 1, 2026? Unless Exxon thinks they have a better option than Sable, they will presumably be flexible about the deadline.

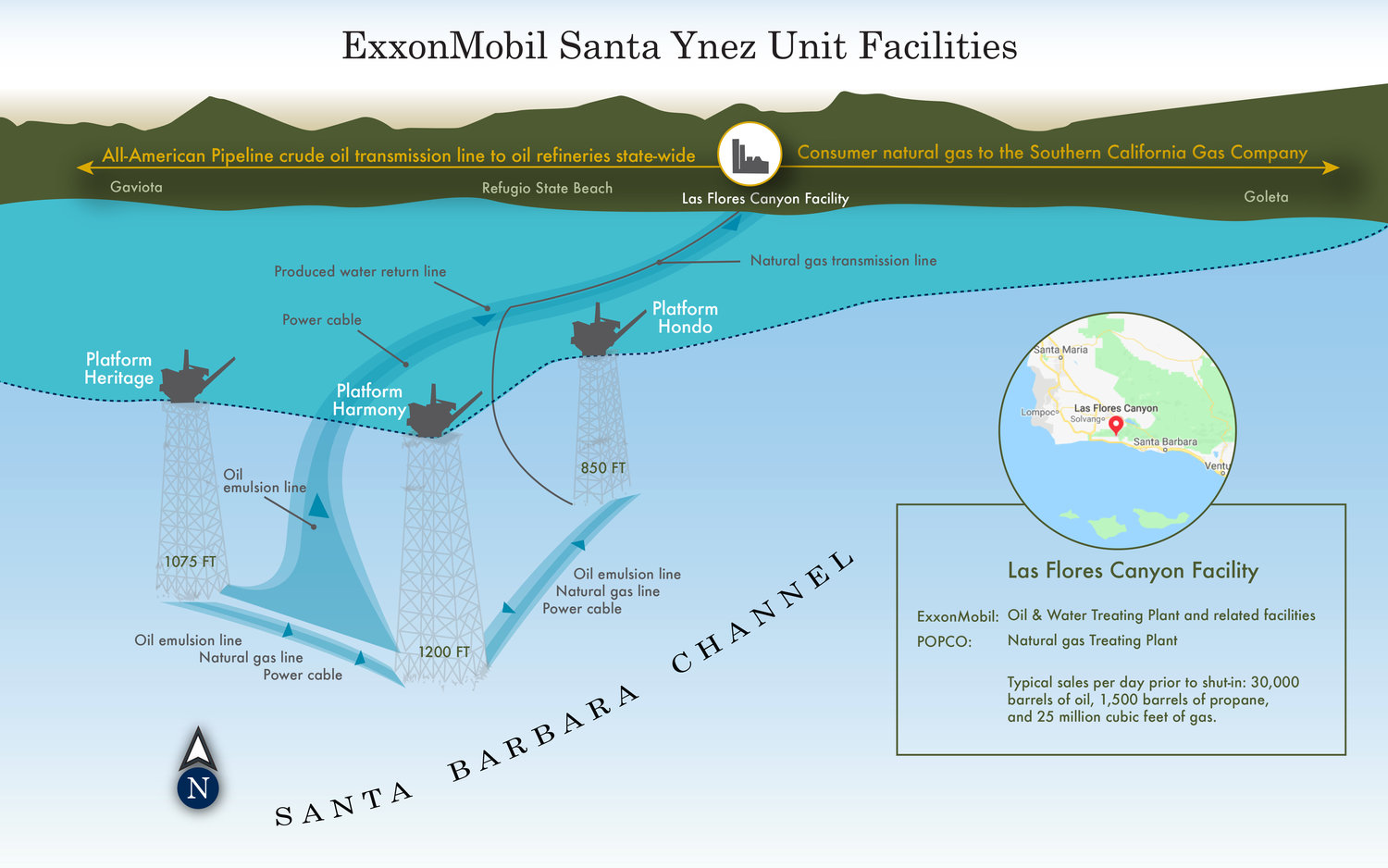

Meanwhile, a judge denied the temporary restraining order requested by Sable to prohibit release of redacted portions of their oil spill contingency plan. Sable had argued that revealing “trade secrets” and specific locations and vulnerabilities of the pipelines could pose a “threat to national security.”

The operator of the wind farm released this short statement yesterday (8/22/2024):

We are aware of a blade failure which occurred this morning on an installed turbine at Dogger Bank A offshore wind farm, which is currently under construction. In line with safety procedures, the surrounding marine area has been restricted and relevant authorities notified. No one was injured or in the vicinity at the time the damage was sustained.

We are working closely with the turbine manufacturer, GE Vernova, which has initiated an investigation into the cause of the incident.

Further updates will be issued in due course as more information becomes available.

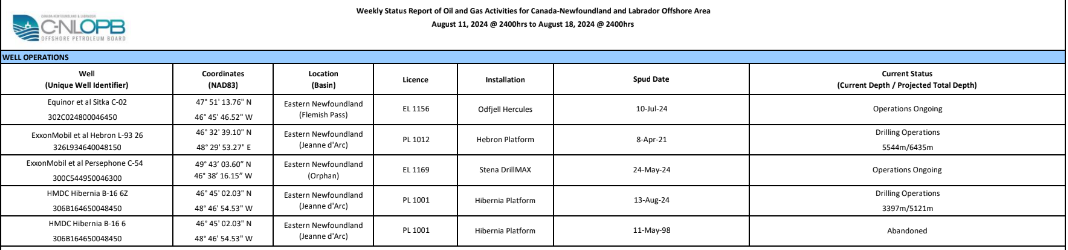

To find the sole exploratory well being drilled in the vast North American Atlantic, you have to exit “wind-only” US waters, head NE to St. John’s, NL (advancing your watch by 1.5 hours 😉), and transit another 317 miles NE to the Stena DrillMAX working for Exxon in the Orphan Basin.

The latest (8/20/2024) CNLOPB report (below) is that operations are ongoing. The well was spudded 3 months ago. That is about all they can disclose without compromising confidentiality. Even seemingly innocuous information like the current and projected well depth provides the opportunity to speculate about geologic conditions and current well activities.

“In the evolving landscape of Guyana’s oil and gas industry, few have managed to carve out a niche quite like Koaito Grant. A name synonymous with corporate photography, Grant’s journey from discovering his passion for capturing moments to becoming a sought-after photographer within the oil and gas sector is as inspiring as it is instructive.“

So true:“It’s the best feeling when a client reaches out and says you were very highly recommended by this or that person.” His professionalism and work ethic have been key differentiators. “I have a client that always asked if I was Guyanese because I’m always early for all projects and activities.”👍 💯

Reuters has published an interesting article on the Exxon/CNOOC vs. Chevron/Hess dispute scheduled for arbitration next year in Paris. According to Reuters (emphasis added):

“Getting the panel to consider the appraised value is central to Exxon’s claim that the deal is an asset acquisition disguised as a merger. Exxon believes the Guyana asset is so valuable that the merger would trigger a change of control and give Exxon and CNOOC a right of first refusal to the asset sale, the people said.“

The Exxon argument implies that Hess’s only major asset is its share of Stabroek, which is hardly the case. Hess’s 30% Stabroek share is without question an important asset with great long-term potential, but Hess is also a major player elsewhere, most notably in the Bakken formation in North Dakota and the Gulf of Mexico. Implying that Hess was a single asset acquisition is thus misleading:

In Q4 of 2023, Hess produced 194,000 boepd in the Bakken formation vs. a Stabroek share of 128,000 bopd.

In 2023, Hess produced 20 million barrels of oil in the GoM and 40 bcf of gas making them the 8th highest oil producer and 7th highest gas producer.

Hess acquired 20 GoM leases in Sale 261, ranking first in total high bids ($88 million) among all participants.

Chevron and Hess GoM assets have significant potential for synergy. The combined company would be the 3rd largest GoM oil producer (behind Shell and bp) and the second largest gas producer (behind only Shell).

This dispute will continue to smolder given the delay in the arbitration hearings until May 2025. As previously mentioned, I believe the Government of Guyana should have intervened. I’m all for companies settling their disputes privately, but this dispute is over Guyanese resources, and the protracted delay could have implications for Guyana.

Four of the five simpler, safer, greener deepwater platforms featured on this blog are now producing. The 5th platform (Whale) is on location and scheduled to begin production later this year.

platform

operator

first production

King’s Quay

Murphy

April 2022

Vito

Shell

Feb 2023

Argos

bp

April 2023

Anchor

Chevron

Aug 2024

Whale

Shell

late 2024

These platforms are in 4000 to 8600′ of water, are expected to reach peak production rates of 100-150,000 boe/day, and have favorable emissions characteristics on a per barrel basis.

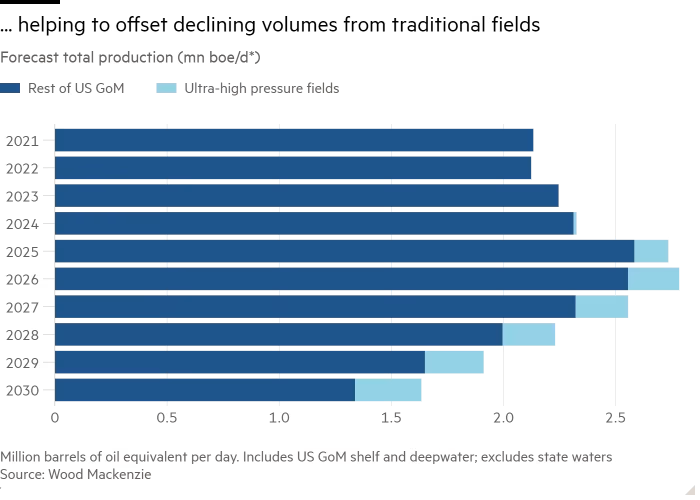

This is all good, but what is next? Will technological advances once again sustain GoM production? The short answer appears to be yes!

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades will facilitate production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded below.)

Chevron’s Anchor is the first deepwater, high-pressure development. Three similar deepwater hub platforms (table below) will begin production over the next 5 years. These host platforms will also facilitate additional production from nearby fields. Each will have production capacities of approximately 100,000 boe/day. Note the long lead times in achieving first production given the technological issues that had to be evaluated and addressed.

platform

operator

discovery date

first production

Kaskida

bp

2006

2029

Sparta

Shell

2012

2028

Shenandoah

Beacon

2009

2025

Wood Mackenzie sees these high pressure projects as the key to sustaining GoM production rates. Their projections for 2024 and 2025 seem optimistic based on 2024 YTD data, which adds to the importance of the projected new production.