Those of us who were involved with OCS oil and gas operations in the 1970s remember the heated battles between Exxon and Santa Barbara County that led to the installation of the infamous Offshore Storage & Treatment (OS&T) facility in Federal waters. This was the first floating production, storage, and offloading facility (FPSO) in US waters by 3 decades!

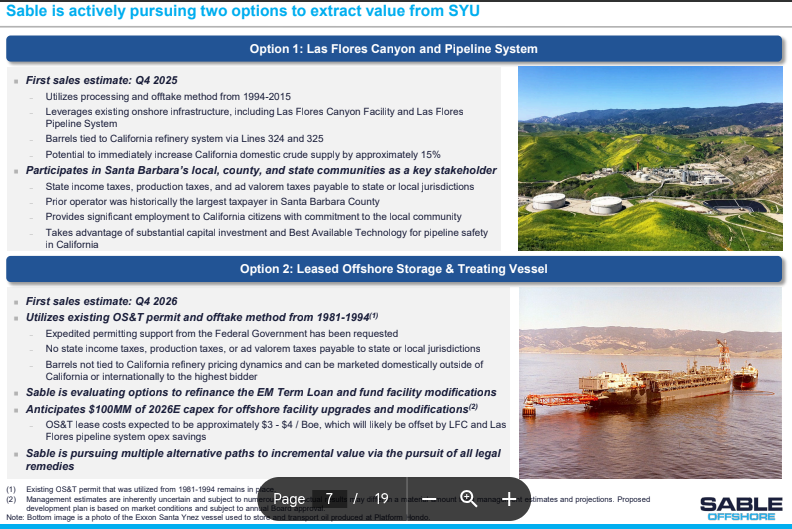

In light of Sable’s difficult (bordering on impossible) onshore permitting challenges, the company resurrected the OS&T option in a recent presentation to investors (pertinent slide pasted above). The extent to which this is purely a tactical maneuver remains to be seen, but this option would be very difficult to execute, even with a supportive Federal regulatory environment.

Updatedincident tables for OCS oil and gas operations. The most recent data are nearly 2 years old. The public has a right to timely information on the type of incidents that are occurring, the operating companies, and the resulting casualties, pollution, and property damage.

A summary of incidents associated with the OCS wind program. From press reports, we know about the fatality during Empire Wind construction. What other incidents have occurred to date?

Attached is the Dept. of the Interior’s Semiannual Regulatory Agenda (9/22/2025). BSEE and BOEM decommissioning rules are excerpted below.

Of particular concern is the revised BOEM regulation (107) that “would reduce the amount of supplemental financial assurance required from oil gas, and sulfur lessees operating on the OCS.” See our previous post on this regulatory action. Note that a proposed rule is expected to be published by year end.

REVISIONS TO DECOMMISSIONING REQUIREMENTS ON THE OCS [1014–AA53] Legal Authority: Outer Continental Shelf Lands Act, 43 U.S.C. 1331 to 1356a Abstract: This proposed rule would address issues relating to (1) idle iron by adding a definition of this term to clarify that it applies to idle wells and structures on active leases; (2) abandonment in place of subsea infrastructure by adding regulations addressing when BSEE may approve decommissioning-in-place instead of removal of certain subsea equipment; and (3) other operational considerations. Timetable: NPRM ……………… 07/00/26 NPRM Comment Period End: 10/00/26

RISK MANAGEMENT AND FINANCIAL ASSURANCE FOR OUTER CONTINENTAL SHELF LEASE AND GRANT OBLIGATIONS [1010–AE26] Legal Authority: 43 U.S.C. 1331, OCS Lands Act; E.O. 14154, Unleashing American Energy Abstract: This proposed rule would rescind BOEM’s final rule ‘‘Risk Management and Financial Assurance for OCS Lease and Grant Obligations.’’ The proposed rule would revise the criteria for determining whether oil, gas, and sulfur lessees, right-of-use and easement grant holders, and pipeline right-of-way grant holders are required to provide financial assurance above the current minimum bonding levels to ensure compliance with their Outer Continental Shelf (OCS) Lands Act obligations. This rule, if finalized, would reduce the amount of supplemental financial assurance required from oil gas, and sulfur lessees operating on the OCS and would support the goals of E.O. 14154; Timetable: NPRM ……………… 01/00/26

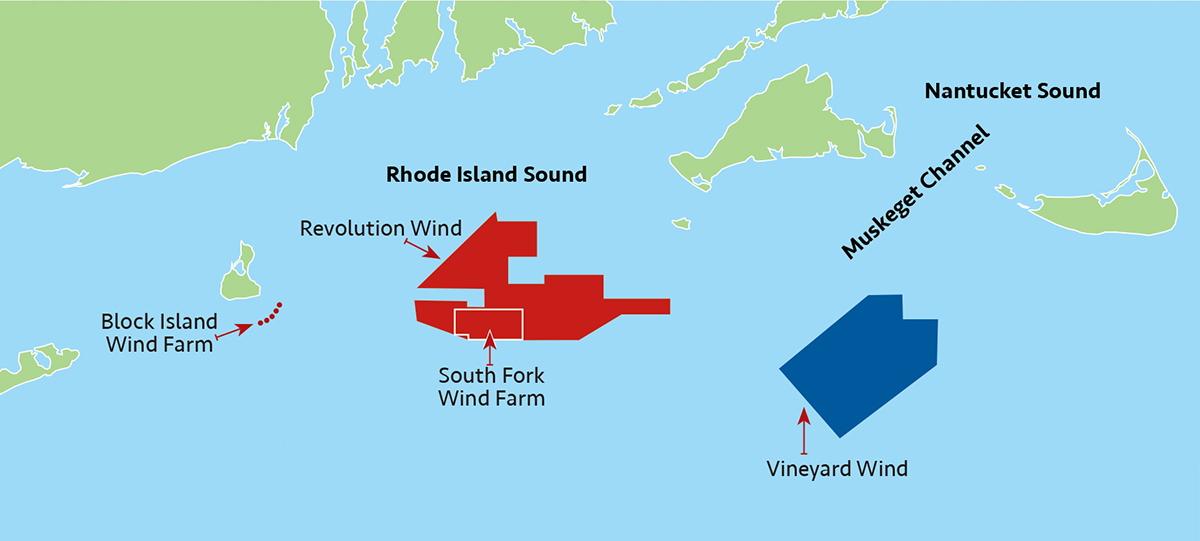

Judge Royce Lamberth granted an injunction allowing Orsted to resume work on the Revolution Wind project. BOEM halted work on the project one month ago.

The table below captures the shorter public comments and provides links to the longer ones. They are listed in the order they were posted on Regulations.gov.

commenter

summary/link

anonymous

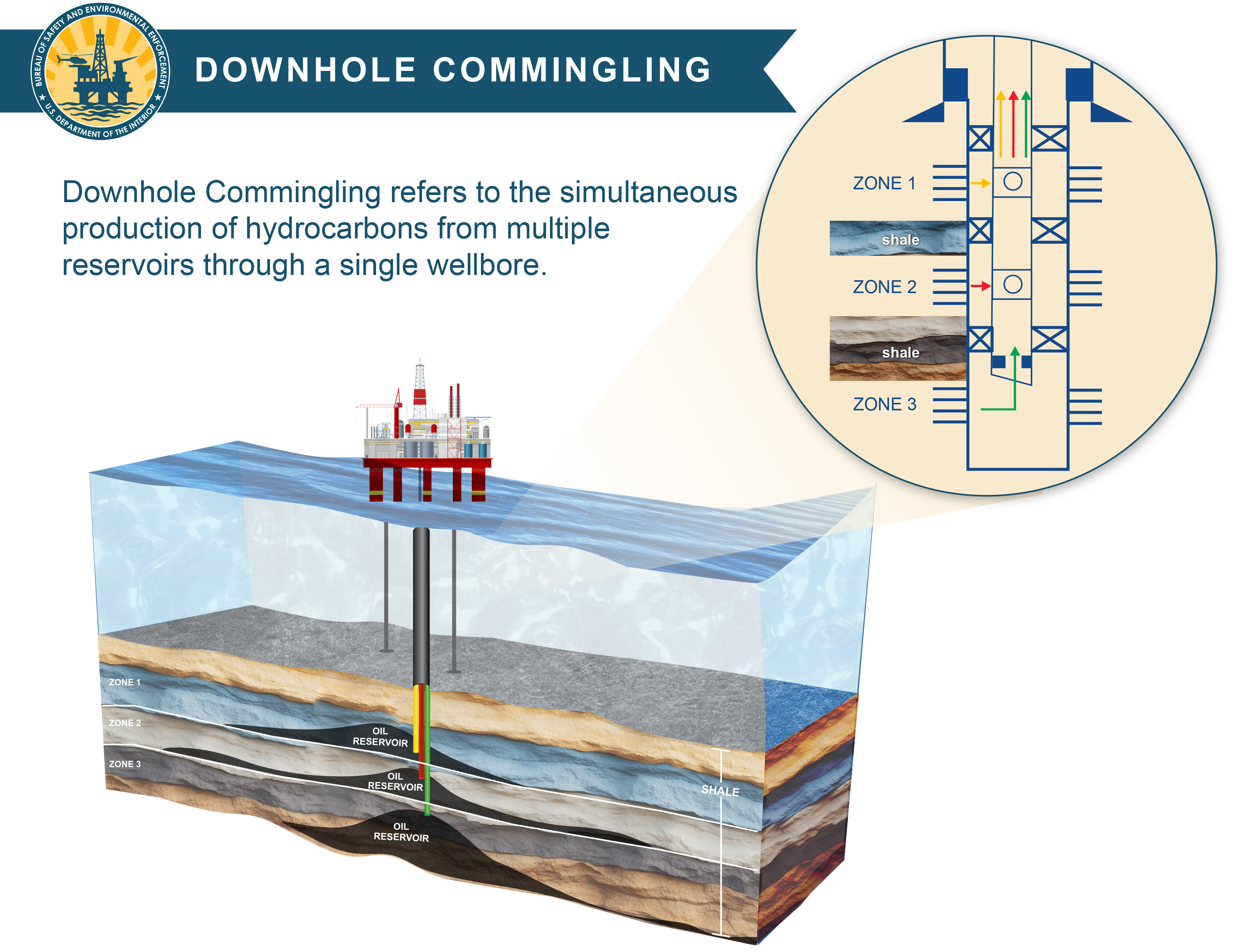

I recommend under no circumstance that we allow the onsite worker to approve the commingling of bore holes because there is extreme significant safety and environmental hazards that exist. The best alternative is to have an environmental engineer and environmental scientist approve any commingling

…your regulatory proposal is inconsistent with the federal law, the best available science on protecting the health and lives of children, and the legal mandate that agency decision-making does not deprive children of their fundamental constitutional rights…

I support updating the regulations to align with the One Big Beautiful Bill Act, but I encourage BSEE to ensure that safety standards and environmental protections remain the highest priority in all commingling approvals. Clear guidance for industry compliance and transparent public reporting would also strengthen confidence in this rule.

Ananda Foster

Regulations need to catch up with technology and we have not had a chance to do that yet. If you allow them on throttle access, they will destroy it. We all rely on the ocean, how can you do this to your own constituents?

Legislatively dictating well construction, completion, or operational approvals is a redline for me, and I continue to strongly believe the downhole commingling rule should be published as a draft for public review and comment.

The only industry comments are from API and bp America. Both support the direct final rule, and I respect their position. My main quarrel is with the legislative action that put us in this position.

I have had many disagreements with API members over the years, but the dialogue has always been professional. Technical and policy disagreements are healthy for the OCS program, and I will continue to raise potential issues and concerns on this blog.

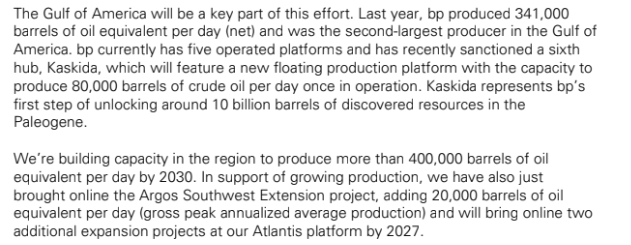

With regard to bp, I have been impressed by their commitment to the Gulf of America, as summarized in this excerpt from their comments:

John Smith shared the attached letter from Senators Adam Schiff and Alex Padilla, and members of the California congressional delegation. The letter questions BSEE’s inexplicable announcement about the resumption of Santa Ynez Unit (SYU) production. That announcement boasted:

“This is a significant achievement for the Interior Department and aligns with the Administration’s Energy Dominance initiative, as it successfully resumed production in just five months.“

BSEE’s announcement, which has not been explained and is still featured on their homepage, served only to further complicate the resumption of production from the SYU, which has reserves in excess of 500 million barrels.

…and should be an integral part of Job Safety Analyses!

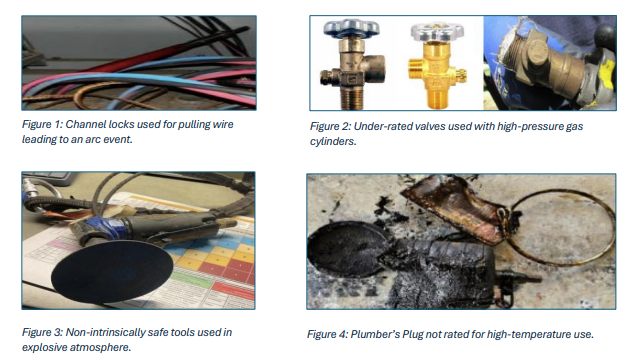

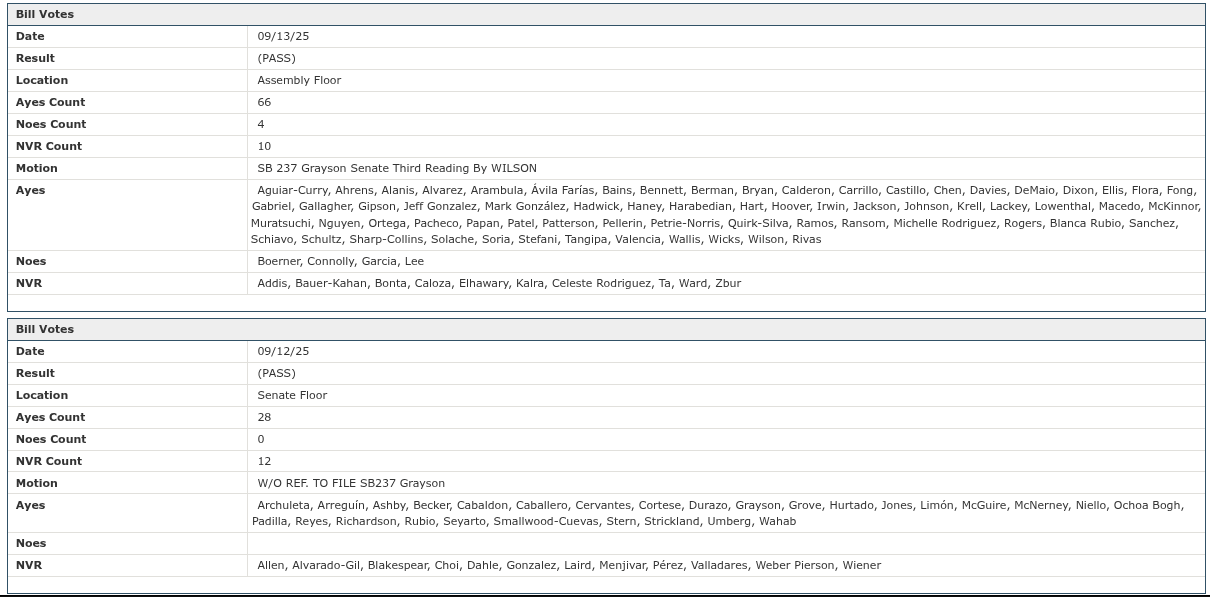

According to BSEE, there is a recurring trend of equipment misuse contributing to fire and explosion hazards during offshore oil and gas operations in the Gulf of America.

Workers have used tools not rated for electrical work on live circuits (Figure 1) and mismatched hydraulic or pneumatic tools for high-pressure systems (Figure 2). In several cases, non-intrinsically safe hand tools were used in explosive atmospheres, including mudrooms and drilling floors.

John Smith has highlighted the attached bill that could, if passed, further derail Sable’s plans to restart Santa Ynez Unit (SYU) production.

This provision appears to target Sable:

Section 3(b)(2): Repair, reactivation, and maintenance of an oil and gas facility facility, including an oil pipeline, that has been idled, inactive, or out of service for five years or more shall be considered a new or expanded development requiring a new coastal development permit consistent with this section.

The legislation would be effective on 1/1/2026 so perhaps Sable will already be producing. Sable may also explore the jurisdictional and interstate commerce issues touched on in this post.

This LA Times update adds to the confusion as to the implications for Sable.

Sables’ share price sank on Tuesday following reports from Bloomberg and others that Governor Newsom is proposing new restrictions on California’s offshore oil industry. With Sable Offshore as a primary target, stricter requirements for restarting inactive intrastate oil pipelines would be imposed. •

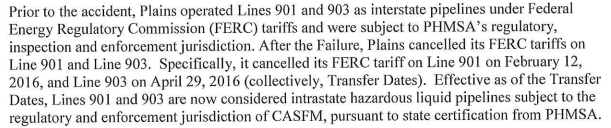

This could trigger yet another legal battle or increase the complexity of those that are ongoing. The onshore pipeline, now owned by Sable Offshore, was originally classified as an interstate pipeline under Federal jurisdiction. However, following the 2015 Refugio oil spill, it was reclassified as an intrastate pipeline via a 2016 letter of understanding signed by representatives of the Federal Office of Pipeline Safety (DOT-PHMSA) and the Office of the State Fire Marshal (pertinent text pasted below).

Given that the Sable pipeline will carry OCS production, it would seem to fundamentally be an interstate line (Federal jurisdiction), as it was when owned by Plains. Could DOT reverse the 2016 letter agreement? That is conjecture for the attorneys and courts to consider.

Meanwhile, below is an upbeat Sable video on the pipeline!