CP’s acquisition of Marathon is an endorsement of shale production, most of which is from private lands. Sadly, these historically important OCS operators no longer have an interest in the Federal offshore sector.

Florida HB 1645 (attached) was signed by Gov. DeSantis on 5/15/2024. The bill boosts natural gas, prohibits offshore wind turbines, and deletes references to climate change and greenhouse gases in state law. Given the State’s support for traditional energy sources, is it time to renew the dialogue about exploration and production in the Eastern Gulf of Mexico (EGOM)?

HB 1645 prohibits offshore and coastal wind development (p. 30), acknowledges that natural gas is critical for power resiliency, prohibits zoning regulations that restrict gas storage facilities and gas appliances (p.8), and relaxes permitting requirements for pipelines <100 miles long.

Given Florida’s energy preferences as expressed in this legislation, the State could assist regional energy planners by better defining its position on oil and gas leasing in the EGOM. What limits, in terms of lease numbers and minimum distances from shore, would best improve Florida’s energy supply options while further minimizing environmental risks?

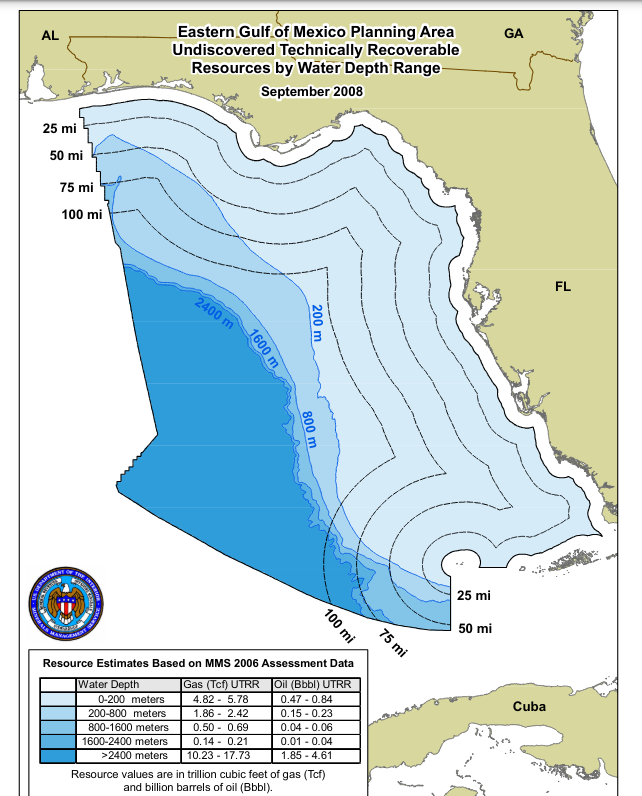

As illustrated on the map below, the petroleum geology of the EGOM and Florida’s preferences are likely aligned in that the best prospects for oil and gas production are in deep water and more than 100 miles from the State’s coast.Does Florida support a 100 mile buffer?

The 4/20/2010 Macondo blowout was a tragic failure that has been, and will continue to be, discussed at length on this blog. We should also acknowledge that prior to Macondo 25,000 wells were drilled on the US OCS over a 25 year period without a single well control fatality, an offshore safety record that was unprecedented in the U.S. and internationally. We should also applaud recent advances in well integrity and control, including the addition of capping stack capabilities that further reduce the risk of a sustained well blowout.

Florida’s independent thinking on energy policy is commendable. That independence is contingent on importing petroleum products and natural gas from elsewhere in the Gulf region. Securing that supply over the intermediate and longer term should be a priority for Florida. In that regard, EGOM production is an important consideration.

“Exxon Mobil has led a persistent and apparently successful lobbying campaign behind the scenes to push the US federal government to adopt rules that would allow the conversion of existing oil and gas leases in the Gulf of Mexico into offshore carbon capture and storage (CCS) acreage, according to documents seen by Energy Intelligence and numerous interviews with industry players.”Energy Intelligence

The Energy Intelligence article documents the ongoing carbon disposal lobbying by Exxon and others. Those meetings are okay prior to publishing a Notice of Proposed Rulemaking (NPRM) for public comment. However, the article implies that the next step is a final rule: “Whether or not Exxon succeeds will become fully clear when the US issues final rules guiding CCS leasing, expected sometime this year.”

A final rule this year is unlikely, because an NPRM has to be published first for public comment. The only exception would be if BOEM was able to establish “good cause” criteria for a direct final or interim final rule in accordance with the Administrative Procedures Act. Such an attempt at corner cutting seems unlikely, especially in an election year when all regulatory actions are subject to additional scrutiny.

Exxon must have thought they had a clear path forward after 11th hour additions to the “Infrastructure Bill” authorized carbon disposal on the OCS, exempted such disposal from the Ocean Dumping Act, and provided $billions for CCS projects. Keep in mind that the Infrastructure Bill was signed just two days before OCS Oil and Gas Lease Sale 257, at which Exxon acquired 94 leases for carbon disposal purposes.

What the Infrastructure Bill did not provide is authority to acquire carbon disposal leases at an oil and gas lease sale. Now the lobbyists are apparently scrambling to overcome that obstacle administratively.

A single company or small group of companies should not be dictating the path forward for the Gulf of Mexico. Super-major Exxon is a relative minnow in the Gulf of Mexico OCS. They have not drilled an exploratory well since 2018, not drilled a development well since 2019, operate only one platform (Hoover, installed in 2000), ranked 11th in 2023 oil production, and ranked 29th in 2023 gas production.

Lastly, and most importantly, public comment on the myriad of technical, financial, and policy issues associated with GoM carbon disposal is imperative. That input is essential before final regulations are promulgated.

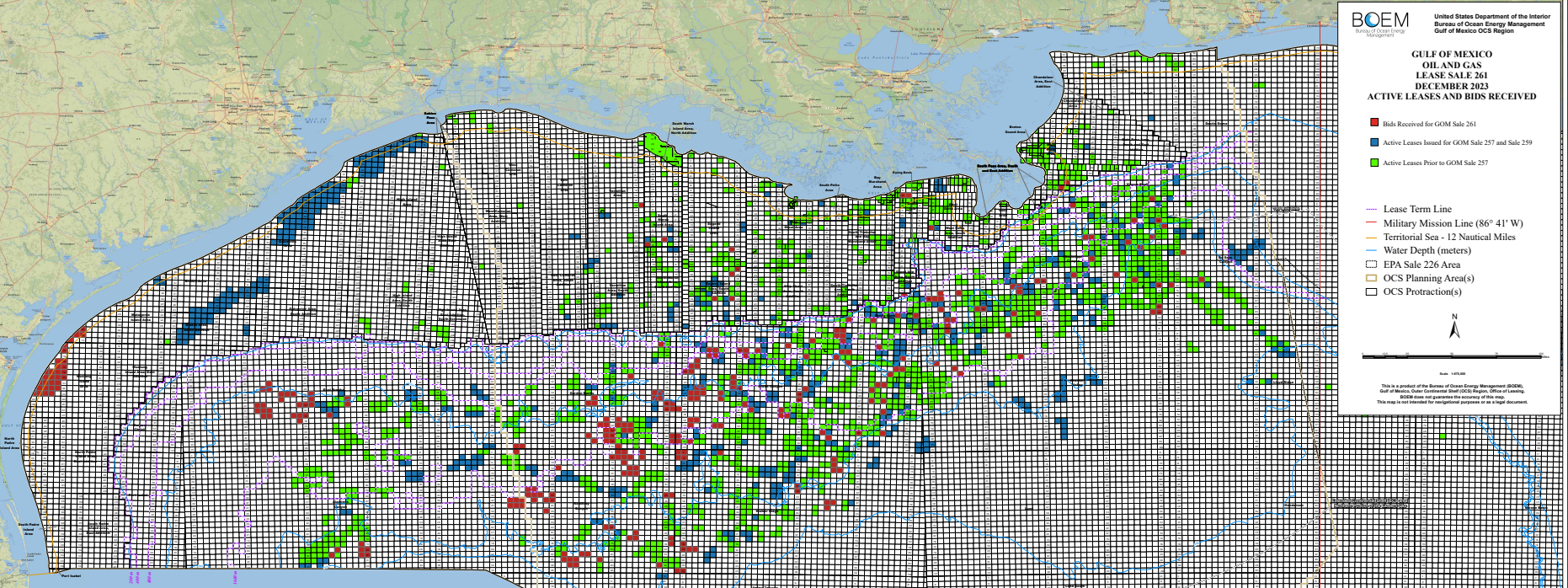

At Sale 261, Repsol was the sole bidder for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 and 259.

“Deepwater is back in vogue.” (Pablo Medina, Welligence)

“Newer deepwater projects have the attributes oil and gas companies are looking for: longer-term production, lower breakeven costs, big resource potentials and lower carbon emissions.” (Medina)

Capital spending on all-new deepwater drilling is poised to hit a 12-year high next year (Rystad)

Investment in all-new and existing deepwater fields could hit $130.7 billion in 2027, a 30% jump over 2023 (Rystad)

Deepwater resources offer lower carbon emissions intensity than shale and other tight oils, averaging 2kg of carbon dioxide per barrel less than shale. (Rystad)

“The return of offshore and deepwater operations is going to be a big topic at OTC, and Namibia is going to be talk of the show.” (James West, Evercore)

Enthusiasm for offshore has climbed with discoveries and technology breakthroughs. Namibia’s Mopane is forecast to hold as much as 10 billion barrels of oil. (Portuguese oil company Galp Energia)

Rates for some rigs have surpassed $500,000 a day and contract durations are lengthening as supply dwindles.

The government’s decision to require that a capping stack be located in Guyanais prudent. Although the need for a capping stack is dependent on multiple barrier failures and is thus extremely low, the environmental and economic consequences of a prolonged well blowout warrant timely access to this tertiary well control option.

A capping stack must be properly maintained and deployable without delay. In that regard, BSEE has a good program for testing Gulf of Mexico capping stack readiness. Capping stack drills are an important post-Macondo addition to the unannounced oil spill response program that dates back to 1981.

“Troy Naquin, BSEE New Orleans District, observes as a capping stack is carefully lowered onto the deck of ship to be transported more than 100 miles offshore for a drill designed to test industry’s ability to successfully deploy it in case of an emergency, May 8, 2023.” BSEE photo/Bobby Nash

The Adjusted Delayed Value (ADV), which takes into account the effects of delaying bonuses and future royalty payments, ranged from 1.3 to 9.2 times the high bids.

Perhaps the closest calls were Chevron’s two Walker Ridge bids which had ADV to bid ratios of only 1.3 to 1.4.

The main concern going forward is the absence of a consistent, predictable leasing schedule for the 3.7% of the OCSthat may be considered for leasing. BOEM’s new methodology, which will be applied at the next lease sale (whenever that might be), does not require the bureau to estimate the delay period between the sale being evaluated and the projected next lease sale. Given that the new 5 year plan calls for a maximum of 3 lease sales, the gap between sales has become a much more significant factor just as the new guidance is being implemented.

The new 5 year “leasing plan” is intended to restrain OCS production in deference to “net zero” pathways. This strategy discourages interest from exploration and production companies. US offshore leases, which are by far the world’s smallest, are even less attractive when you don’t know if and when you will be able to acquire the nearby tracts that may be needed for economical deepwater development. This is not the way to obtain fair market value for public resources.

Block

No. of bids

High Bid ($)

MROV($) ADV($)

High Bidder

MROV/bid ADV/bid

MC 711

1

584,700

6,600,000 2,400,000

bp

11.3 4.1

MC 896

1

641,628

6,100,000 1,600,000

Shell

9.5 2.5

GC 182

1

800,085

3,900,000 2,600,000

Anadarko

4.9 3.2

GC 183

1

800,085

9,100,000 6,000,000

Anadarko

11.4 7.5

GC 226

1

800,085

2,100,000 1,600,000

Anadarko

2.6 2.0

GC 227

2

974,628

13,000,000 9,000,000

Shell

13.3 9.2

GC 345

1

1,095,615

13,000,000 5,300,000

Murphy

11.9 4.8

GC 346

1

845,815

5,100,000 2,000,000

Murphy

6.4 2.4

GC 549

1

800,085

15,000,000 6,900,000

Anadarko

18.7 8.6

AT 237

1

909,899

8,300,000 3,000,000

Equinor

9.1 3.3

WR 285

1

859,837

6,200,000 1,200,000

Chevron

7.2 1.4

WR 329

1

595,837

4,400,000 770,000

Chevron

5.7 1.3

MROV=Mean of the Range-of-Value ADV=Adjusted Delayed Value, which takes into account delaying bonuses and royalties

I had the pleasure of working with Jason Mathews when he was a young MMS engineer. He truly cared about our safety mission and has taken that commitment to the next level at BSEE. Jason shared this important, heartfelt message on the anniversary of the Macondo blowout.

One of the greatest gifts I ever received in life is having a little girl and having the opportunity to go home every evening and spending time with her at cheer, softball, doing homework, etc. I have a great deal of respect for the men and women who work offshore and put their lives on hold for 14-28 days to deliver much needed OCS production to meet US demand. Undoubtedly, they are better / tougher people than me.

Over the last year, my team has seen multiple incidents that had a high potential severity that could have led to a fatal / serious injury or major incident in the GOM. Although we can sit and debate the causal factors for hours, one that jumps to the top of the discussion is the Human Factor – Complacency. Of all the things a leader should fear, complacency heads the list. There is no doubt success breeds complacency, and complacency breeds failure.

To this day, I am still shook by the mindset and complacency of many onboard the Deepwater Horizon prior to the incident. During testimony in the public hearings, John Guide, the BP well team leader for the Horizon, believed that the rig crew had become “too comfortable” because of its good track record for drilling difficult wells. Ross Skidmore, a BP contractor on the rig on April 20, testified that the crew became complacent after completing drilling because “when you get to that point, everybody goes to the mindset that weʹre through, this job is done.” To me, the complacency on the Deepwater Horizon could be attributable to the crew not having access to all of the well data (OptiCem reports – cement job risk) available to BP personnel onshore and the well site leaders on the rig. Our investigation concluded, the overall complacency of the Deepwater Horizon crew was a possible contributing cause of the kick detection failure.

As regulators, we have special roles in the GOM as it relates to safety:

Driving the avoidance of complacency and risk-free mindsets of the offshore employees

Understanding we can’t be selfish – Our success is not our individual personal growth / gains, but it is being unwavering in your promotion of offshore safety to ensure all offshore employees return home to their families safely

Holding each other (internally) and industry (externally) accountable when necessary

In order to achieve greatness offshore, we ,as a regulator, have to believe we can, and never sit still until we achieve it.

Everyone on this email has a very critical function and role. Never underestimate the value of what you do, have the proper mindset, and avoid complacency.

Do whatever it takes to ensure the people offshore are gifted the same gift we receive every day – going home to our families.

All In –

Jason P. Mathews, Petroleum Engineer, Field Operations – OSM

Friday Night LIghts: Coach Mathews and his daughter

Proved reserves should not be a basis for reducing supplemental assurance. The uncertainty associated with reserve estimates and decommissioning costs can easily negate the assumed buffer in BOEM’s 3 to 1 reserves to decommissioning costs ratio. That approach failed completely at the Carpinteria Field in the Santa Barbara Channel (Platforms Hogan and Houchin). See other points on this issue.

Given that the reverse chronological order process for determining predecessor liability was dropped from consideration last April, there is no defined procedure for issuing decommissioning orders to prior owners. The absence of such a procedure increases the likelihood of confusion, inequity, and challenges, particularly when orders are first issued to companies that owned the leases decades ago, in some cases prior to the establishment of transferor liability in the 1997 MMS “bonding rule.”

BOEM’s concern (below) about investment in US offshore exploration and production is interesting given that their 5 year leasing plan strongly implies otherwise.

BOEM’s goal for its financial assurance program continues to be the protection of the American taxpayers from exposure to financial loss associated with OCS development, while ensuring that the financial assurance program does not detrimentally affect offshore investment or position American offshore exploration and production at a competitive disadvantage

I’m just guessing here, but my sense is that BOEM was pressured to finalize this rule in a timely manner (<10 months is timely for such a complex rule) and was thus reluctant to make any significant changes to the proposal published last summer. A public workshop during the comment period would have been a good idea to facilitate informed discussion on the important issues addressed in this rule. Such workshops were once commonplace for major rules.