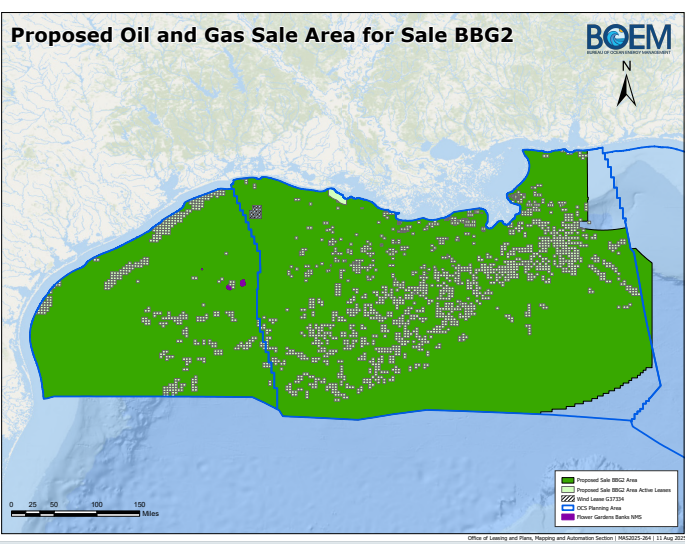

Although no one was expecting a barnburner only 3 months after the previous sale, BBG2 was historically weak for a Gulf-wide sale. The table below compares BBG2 with the previous 4 Gulf sales, none of which were particularly impressive.

However, the sale was not without highlights. There was some spirited bidding for tracts in the Green Canyon area. BP’s bid was the highest of 5 for GC Block 404. BP bid $21 million for the block, 45% of the high bids sum for the entire sale. The BP bid was also $20 million higher than the next highest bid for that tract (ouch!).

Also interesting was Chevron edging Shell $5,887,188.00 to $5,501,240.00 to acquire GC Block 492.

Sale No.

257

259

261

BBG1

BBG2

date

11/17/2021

3/29/2023

12/20/2023

12/10/2025

3/11/2026

companies participating

33

32

26

30

13

total bids

2233

2842

3161

219

38

tracts receiving bids

2143

2442

2751

181

25

sum of all bids $millions

198.5

309.8

441.9

371.9

69.9

sum of high bids ($millions)

101.7

263.8

382.2

279.4

47.0

highest bid company block

$10,001,252 Anadarko AC 259

$15,911,947 Chevron KC 96

$25,500,085 Anadarko MC 389

$18,592,086 Chevron KC 25

$21,009,990 bp GC 404

most high bids company sum ($millions)

46 bp 29.0

75 Chevron 108.0

65 Shell 69.0

50 bp 61.0

6 Anadarko (Oxy) 4.0

sum of high bids ($millions) company

47.1 Chevron

108 Chevron

88.3 Hess

61.0 bp

22.6 bp

most high bids by independent

14-DG Expl.

13-Beacon 13-Red Willow

22-Red Willow

14-Murphy

5-LLOG

1excludes 36 leases improperly acquired for carbon disposal purposes; 2excludes 69 leases improperly acquired for carbon disposal purposes; 3excludes 94 leases improperly acquired for carbon disposal purposes

For historical comparison purposes, Gulf Sale 206 drew $3.7 billion ($5.6 billion in today’s dollars) in 2008. Twenty-siz sales between 1972 and 2013 garnered more than $1 billion in high bids.

Sen. Mike Lee has introduced legislation to repeal the Jones Act, which is drawing additional scrutiny for the increased cost of transporting US oil production and LNG to US ports.

Because facilities on the Outer Continental Shelf are US ports under the Jones Act, the Act has been problematic for both the offshore oil and wind industries. The attached Customs and Border Patrol document delves into the nuances of Jones Act compliance for lifting operations (p.14-15) and “points” on the OCS (p.17).

EXAMPLE: CBP interprets the OCSLA to extend the Jones Act to artificial islands and similar structures, as well as to mobile oil drilling rigs, drilling platforms, and other devices attached to the seabed of the OCS for the purpose of resource extraction and/or exploration operations. Such objects located on the OCS are considered points or places in the United States for purposes of the Jones Act. Similarly, floating warehouse vessels, when anchored on the OCS to supply drilling rigs on the OCS, are also coastwise points.

Check out this complex CBP ruling on the transportation of well fluids from one location in a subsea well cluster to another. See if you understand and agree with their conclusion (below).

The transportation of fluids as described in the FACTS section above, by a dynamically-positioned, foreign-flagged drill ship between wells located within an IF (integrated facility), which subsequently, transships the fluids to a coastwise qualified barge for transportation to a coastwise point, violates 46 U.S.C. § 55102.

On a related matter, it’s still unclear to me whether the attachment of the lower marine riser package to a subsea wellhead makes a floating, dynamically positioned drillship a US port under the Jones Act.

Gulf of America oil and gas lease sale BBG2 will be held tomorrow. The Notice of Sale is attached.

Although Big Beautiful Gulf 1 (BBG1) was rather lackluster, BBG 2 is unlikely to match it in terms of the number of bids and their sum. Prior to BBG1, there had been no lease sale for two years. BBG 2 is being held only 3 months later.

Given the short duration between sales, the bid evaluations for BBG1 are not yet completed. However, the sale notice advises that any block which received a bid in BBG1 is excluded from BBG2.

Will the recent increase in oil prices influence bidding? Probably not given the longer term nature of offshore development and expectations that the current price spike will be of short duration. Onshore shale oil production is more responsive to price fluctuations.

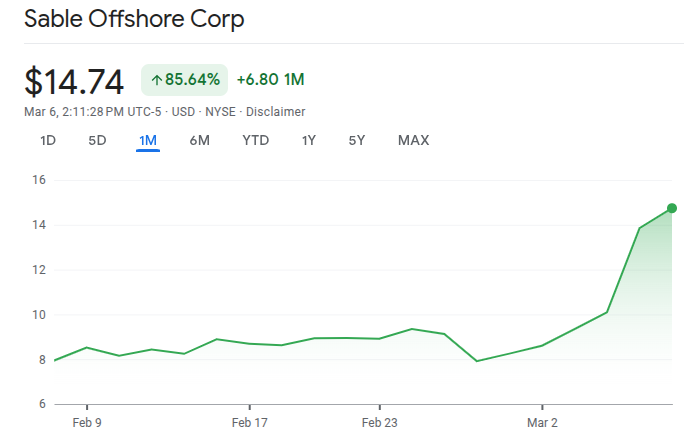

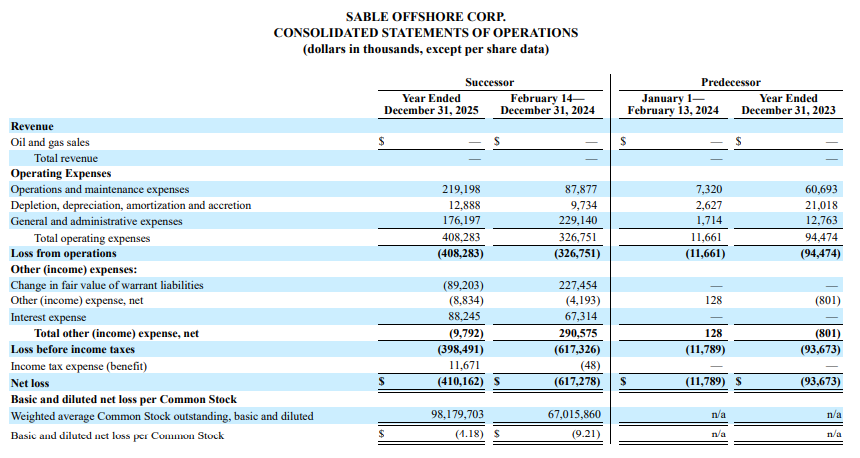

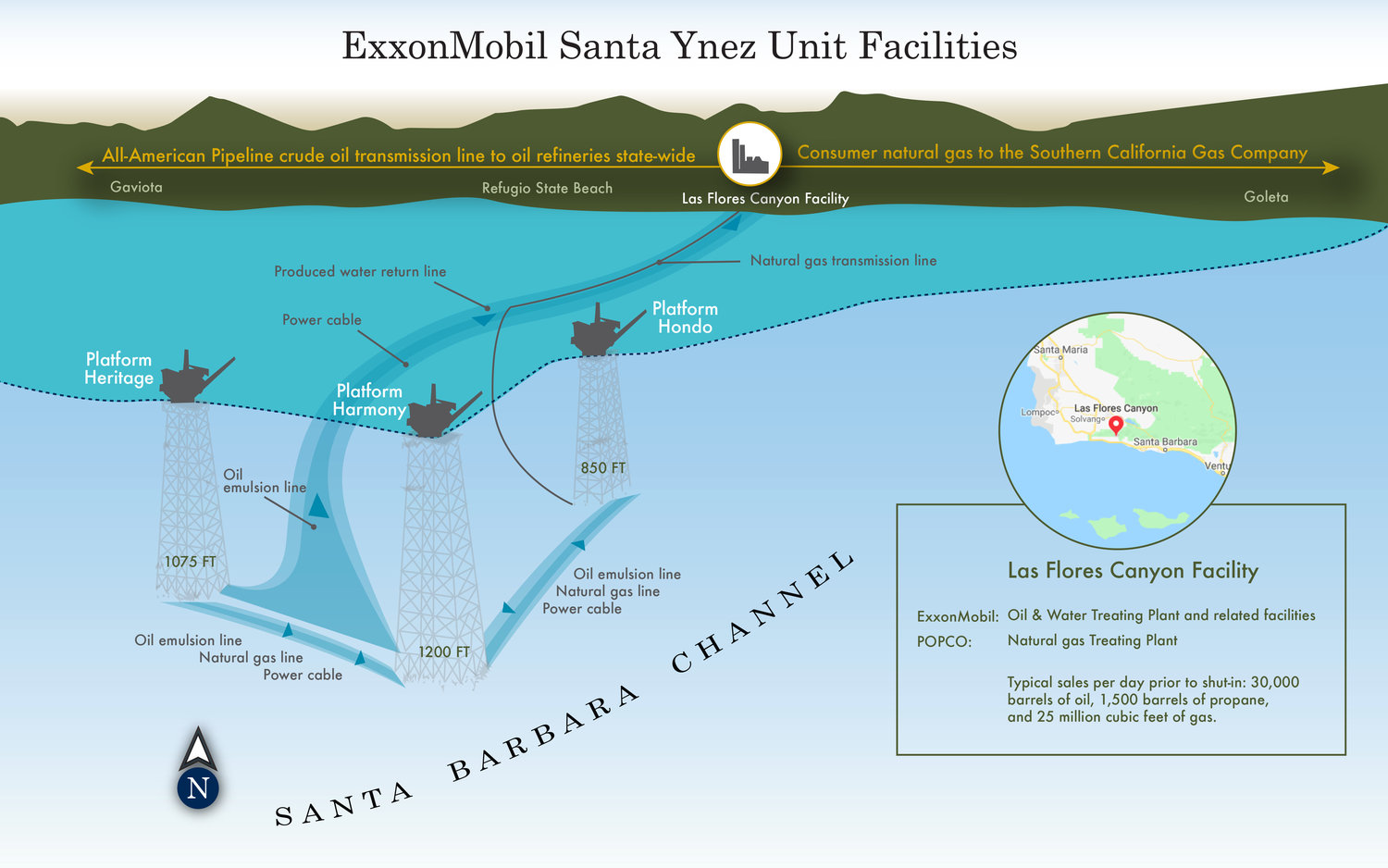

Attached is an opinion prepared by the Assistant Attorney General, Office of Legal Counsel, for the General Counsel, Dept. of Energy. This opinion may boost prospects for Santa Ynez Unit (SYU) production, either by Sable Offshore or a successor.

A few key excerpts from the DOJ opinion (emphasis added):

p. 1: You have asked whether an order issued under the Defense Production Act of 1950 (“DPA” or “Act”), Pub. L. No. 81-774, 64 Stat. 798 (codified as amended at 50 U.S.C. § 4501 et seq.), to Sable by the President or his delegee would preempt the California laws currently impeding Sable from resuming production and operating the associated pipeline infrastructure. We conclude that it would.

p. 6: As the Supreme Court has explained, executive orders “may create rights protected against inconsistent state laws through the Supremacy Clause,” especially when such orders are issued pursuant to “congressional authorization.”

p. 20: State law, we have been advised, is not currently the only impediment to Sable’s ability to resume production and transportation of oil. A consent decree entered in United States v. Plains All American Pipeline L.P., No. 20-cv-02415 (C.D. Cal. Oct. 14, 2020), Dkt. 33 (“Consent Decree”), “currently vests authority over resumption of transportation through the onshore portions of the Santa Ynez Pipeline System with the California Office of the State Fire Marshal.” Sable Letter at 9. We have been advised that, in addition to the United States and various State of California entities, Sable is a party to the Consent decree as a result of an acquisition. You have asked whether an executive order under the DPA would displace these provisions of the Consent Decree, even though there are both federal- and state-law claims at issue in that case. For three reasons, we think it would.

The potential rewards are great – 500+ million barrels of oil, 3 major production platforms, associated pipelines, onshore processing facilities – but can Sable survive the costly legal and administrative challenges? What is Exxon’s plan for the Santa Ynez Unit if Sable should fail?

BOEM: At this time, no bids have been received. In accordance with OBBBA, we will continue to hold leasing opportunities for Cook Inlet so that industry has a regular, predictable federal leasing schedule that ensures we achieve President Trump’s American Energy Dominance Agenda.

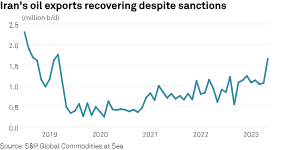

S&P Global reports on the surge in Iranian oil production and exports. In the quote below, note the concern about the higher oil prices that might result from tightening the sanctions. If oil price concerns are driving critical foreign policy decisions, this would be a rather stunning indictment of US energy policy, which is sometimes perceived as being more hostile toward domestic producers than international adversaries.

“Before the war, US-Iranian tensions had eased, which facilitated higher Iranian oil exports. Iranian crude oil production increased 500,000 b/d from March to September 2023 — to 3.1 million b/d from 2.6 million,” the analysts said. “Biden will be under pressure to enforce sanctions and curtail Iranian export revenue. This is a challenging situation for the Biden administration, which wants more oil on the market, not less. The attacks on Israel could override the oil issue.“

Q. I wanted to ask you about oil, if I could, and the money that it’s bringing in. So, is the amount of oil that’s being brought in by Iran — specifically, records amount, 85 percent to China, more oil being sold above the price cap from Russia — giving the President any pause on changing these energy policies for fossil fuels here in the U.S.?

MR. KIRBY: I would — just let me back up a little bit. I mean, it’s important to remember that Iran gets most of its oil revenue off the black market and evad- — evading sanctions, which they do. It’s costly to them. In fact, our evidence is that they really only receive a fraction of the market value of the oil that they sell, because they have to sell it on the black market.

We will always, as we do in any case, typically, revisit sanctions regimes to see if they need to be changed or adjusted, specifically with respect to Iranian oil.

The President, since the beginning of the administration, has been concerned about making sure we have a viable global market for oil, working hard to keep the prices of gasoline down here in the United States. Part of that is making sure you remove some of the volatility in that global supply and demand.

I don’t have any announcements or decisions to make today with respect to any changes to the domestic oil production.

Q But isn’t it a national security issue when you have countries that are profiting off of oil and the increased price of oil that don’t like Israel, that don’t like America?

MR. KIRBY: We don’t want, for instance, Russia to be able to — to get a windfall in profits from the oil market so that they can then turn that around and — and apply that to weapons in Ukraine. We certainly don’t want to see Iran do — be able to do much of the same, which is why we’re — we’re putting as much pressure on them as we are.

Q So, why not increase oil production here?

MR. KIRBY: I — again, I don’t have any announcements to make today.

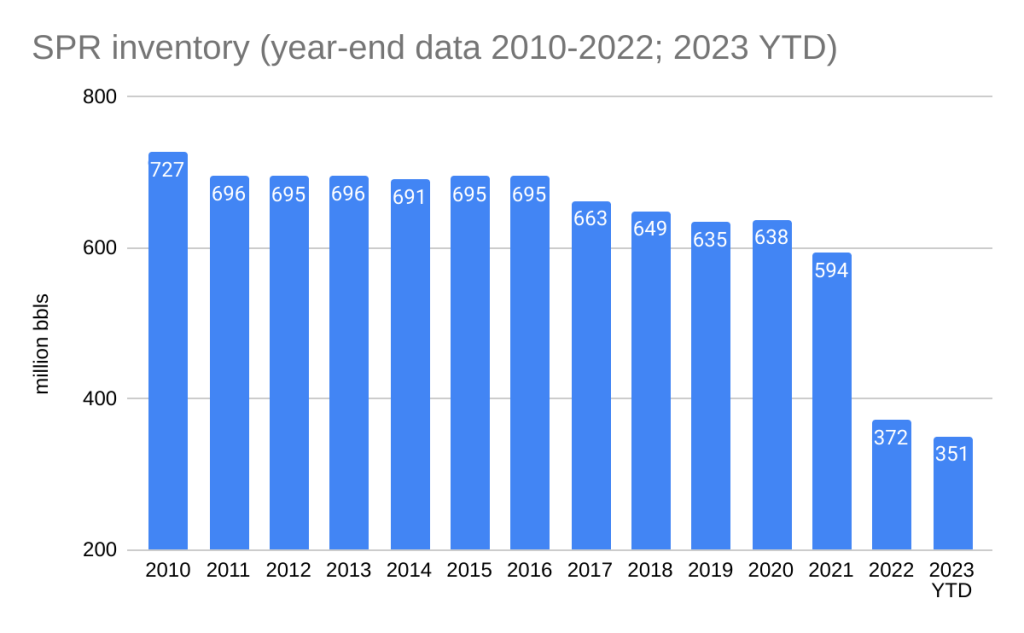

On a related note, the Strategic Petroleum Reserve has remained at historic low levels. The current volume is 351.3 million barrels, a slight rise from the low of 346.8 million barrels in July, the lowest volume since 8/19/1983 when the SPR was still being filled. Have the oil embargoes following the Yom Kippur War, the reason for the SPR’s existence, been forgotten?

Judge Donna Geckupholds restraining orderlarge investment in Sable

On Friday, California Superior Court Judge Donna Geck upheld the restraining order that blocks Sable Offshore from restarting Santa Ynez Unit production. She scheduled a followup court hearing for June 27. Meanwhile, the Ninth Circuit Court of Appeal’s hearing on PHMSA’s assertion of Federal jurisdiction over the onshore pipeline segments is scheduled for July.

Can Sable survive financially until those hearings are concluded?

Contradictorily, we learn that FourWorld Capital Management just purchased 8 million shares of Sable. Is that the financial equivalent of Pickett’s Charge or does FourWorld have good reasons for their optimism?

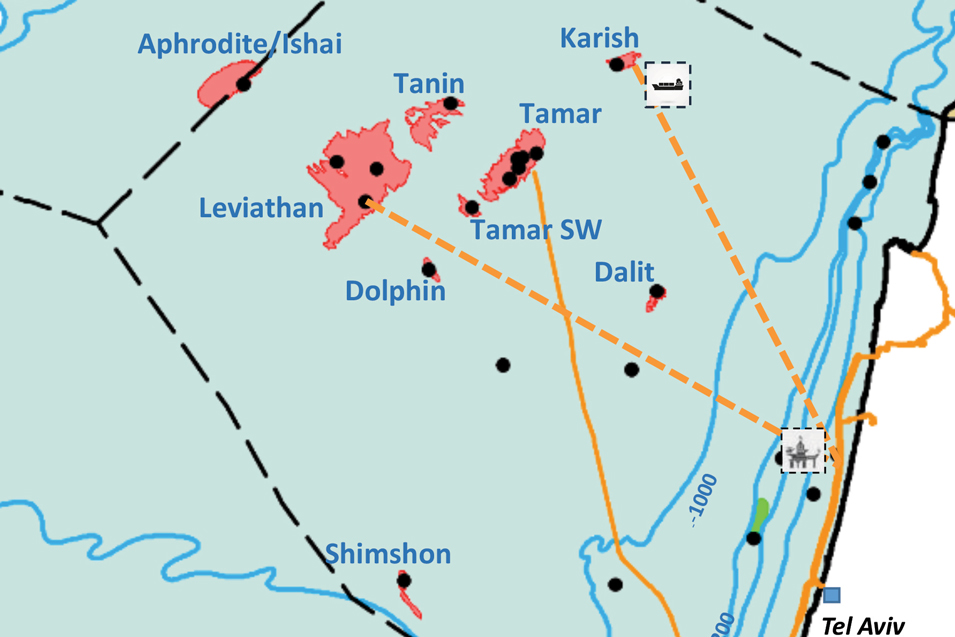

Argus reports that Israel’s energy ministry has instructed Chevron and Energean to suspend production at their offshore Leviathan and Karish gas fields.

Although, the Israeli facility shut-ins will result in the curtailment of exports, Egypt has implemented a backup plan to ensure adequate supply.

There is no indication that Chevron’s Tamar field has been shut-in.

Summary table:

field (operator)

2024 production (billion cubic meters) (% of Israel’s total)