Reuters has published an interesting article on the Exxon/CNOOC vs. Chevron/Hess dispute scheduled for arbitration next year in Paris. According to Reuters (emphasis added):

“Getting the panel to consider the appraised value is central to Exxon’s claim that the deal is an asset acquisition disguised as a merger. Exxon believes the Guyana asset is so valuable that the merger would trigger a change of control and give Exxon and CNOOC a right of first refusal to the asset sale, the people said.“

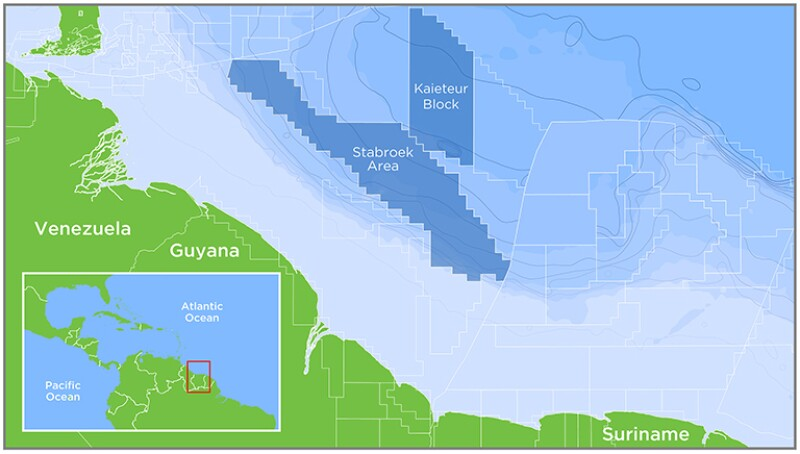

The Exxon argument implies that Hess’s only major asset is its share of Stabroek, which is hardly the case. Hess’s 30% Stabroek share is without question an important asset with great long-term potential, but Hess is also a major player elsewhere, most notably in the Bakken formation in North Dakota and the Gulf of Mexico. Implying that Hess was a single asset acquisition is thus misleading:

- In Q4 of 2023, Hess produced 194,000 boepd in the Bakken formation vs. a Stabroek share of 128,000 bopd.

- In 2023, Hess produced 20 million barrels of oil in the GoM and 40 bcf of gas making them the 8th highest oil producer and 7th highest gas producer.

- Hess acquired 20 GoM leases in Sale 261, ranking first in total high bids ($88 million) among all participants.

- Chevron and Hess GoM assets have significant potential for synergy. The combined company would be the 3rd largest GoM oil producer (behind Shell and bp) and the second largest gas producer (behind only Shell).

Exxon’s ally in this dispute is state owned China National Offshore Oil Corporation. CNOOC acquired their 25% Stabroek share when they purchased Nexen, a Canadian company (sound familiar?). Both the Canadian and US governments had reservations about this acquisition and nearly nixed the deal.

This dispute will continue to smolder given the delay in the arbitration hearings until May 2025. As previously mentioned, I believe the Government of Guyana should have intervened. I’m all for companies settling their disputes privately, but this dispute is over Guyanese resources, and the protracted delay could have implications for Guyana.