Tariffs and their uncertainty “will certainly decrease expected investment activity in the energy sector,” says the new report. More than $50 billion of offshore investment this year has been deferred “with operators looking to wait out current market uncertainty before making significant final investment decisions,” Rystad notes.

Rystad estimates that tariffs will increase costs for offshore oil and gas projects by 8% year-over-year and 12% for onshore. “Most steel and raw material exposed cost categories are feeling the majority of the impact from tariffs and thus will take the biggest hit.”

Comment: At a glance, the number of 2025 well starts in the GOA appears to be down (more on this at a later date). While there are many factors affecting drilling decisions, lower oil prices and higher costs associated with tariffs are not compatible with a “drill baby drill” philosophy.

Rystad Energy projects a 10% annual compound growth rate for the subsea market from 2024 to 2027, with total spending anticipated to exceed $42 billion by the end of this period.

Brazil dominates the subsea umbilical risers and flowlines (SURF) market. Unsurprisingly, the US is lagging given the absence of a robust offshore leasing program and the dearth of deepwater discoveries in recent years.

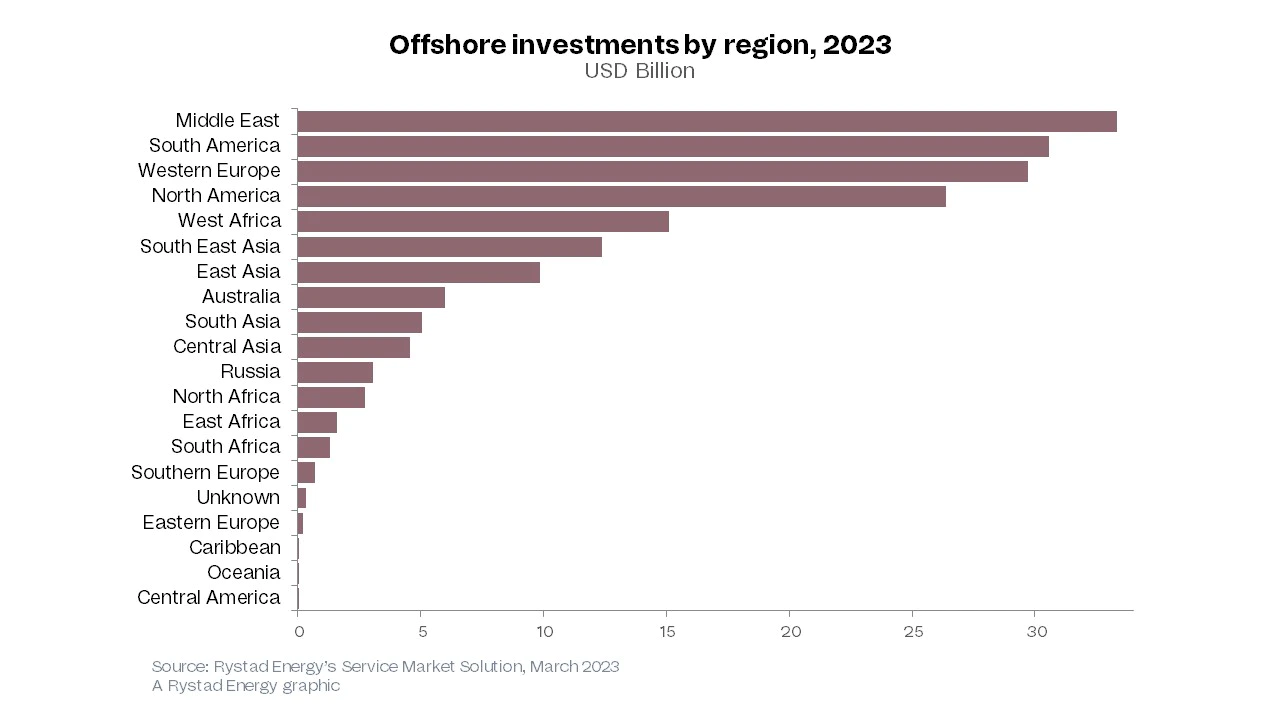

The offshore oil and gas (O&G) sector is set for the highest growth in a decade in the next two years, with $214 billion of new project investments lined up. Rystad Energy research shows that annual greenfield capital expenditure (capex) broke the $100 billion threshold in 2022 and will break it again in 2023 – the first breach for two straight years since 2012 and 2013.

Offshore activity is expected to account for 68% of all sanctioned conventional hydrocarbons in 2023 and 2024, up from 40% between 2015-2018.

Per Offshore-Energy.biz, comments by Aramco President and CEO, Amin H. Nasser, at the Schlumberger Digital Forum:

“When you shame oil and gas investors, dismantle oil- and coal-fired power plants, fail to diversify energy supplies (especially gas), oppose LNG receiving terminals, and reject nuclear power, your transition plan had better be right. Instead, as this crisis has shown, the plan was just a chain of sandcastles that waves of reality have washed away.”

“the warning signs in global energy policies were flashing red for almost a decade,” adding that investments in oil and gas decreased from $700 billion to a little over $300 billion, which is more than 50 per cent between 2014 and 2021.

“this is the moment to increase oil and gas investments, especially capacity development.”

Aramco is working to increase its oil production capacity to 13 million barrels per day by 2027 and grow its gas production by more than half through 2030.

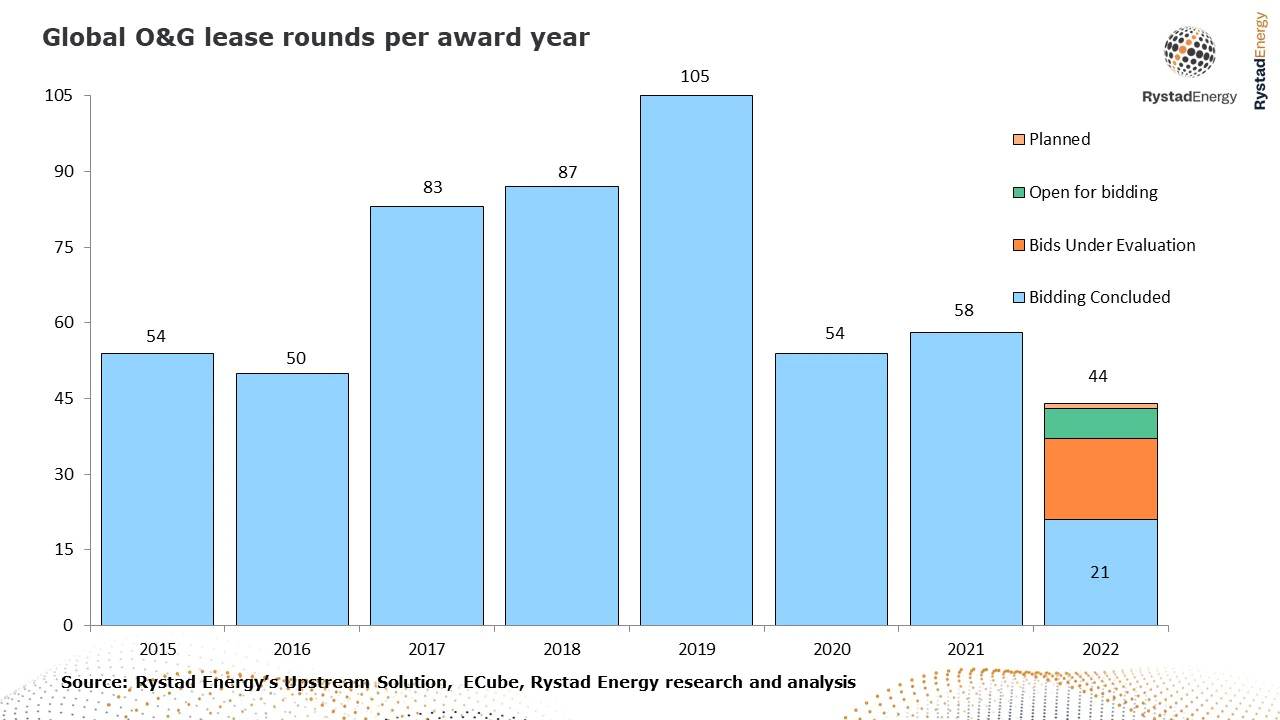

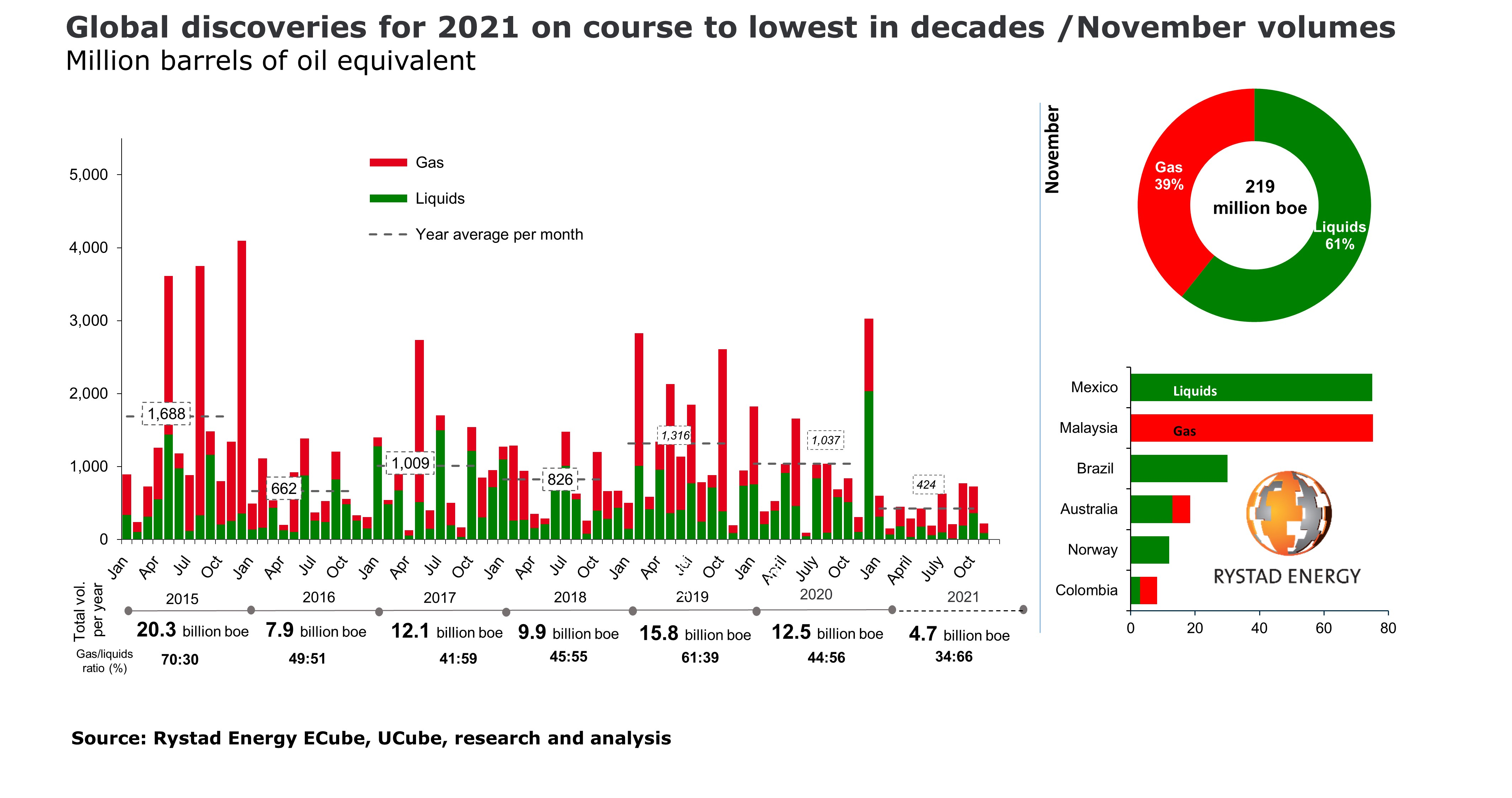

Meanwhile, Rystad reports a further reduction in global oil and gas licensing, with help from the US govt:

“The (worldwide) drop in reserves is driven by the 30 billion barrels of oil produced last year, plus a significant reduction in undiscovered resources, to the tune of 120 billion barrels. The US offshore sector has contributed the largest total to that drop, where 20 billion barrels of oil will remain in the ground, largely thanks to leasing bans on federal land.“

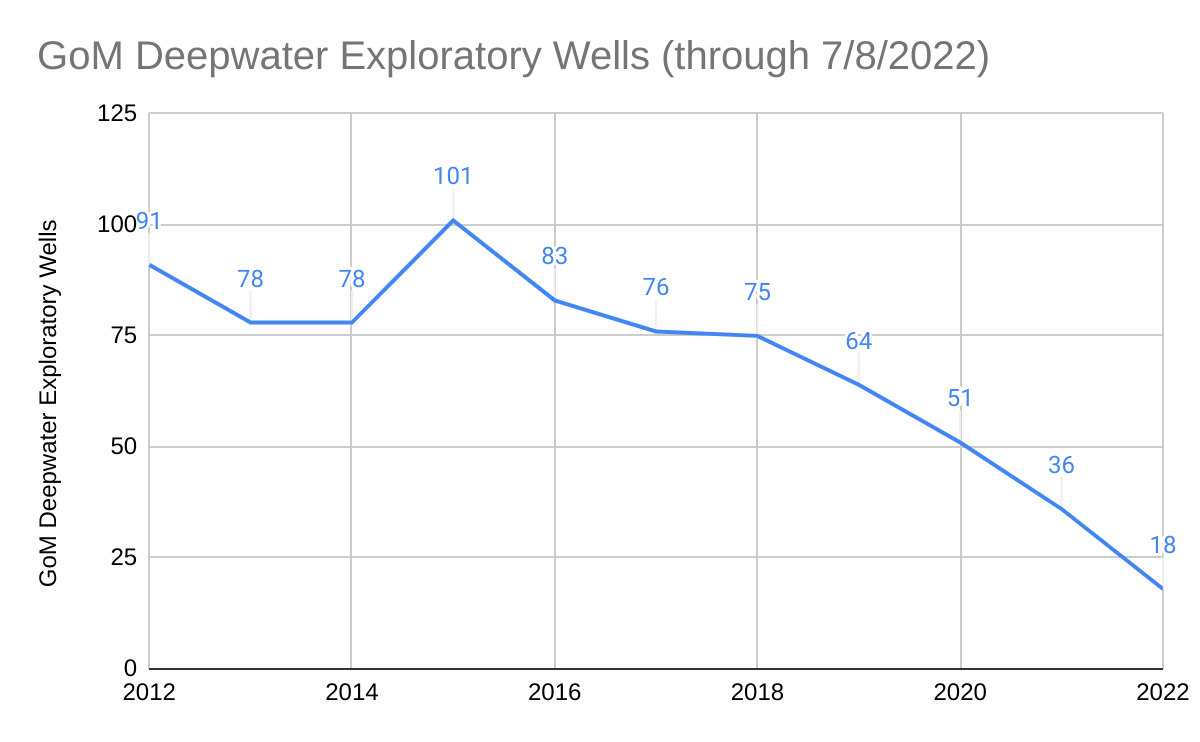

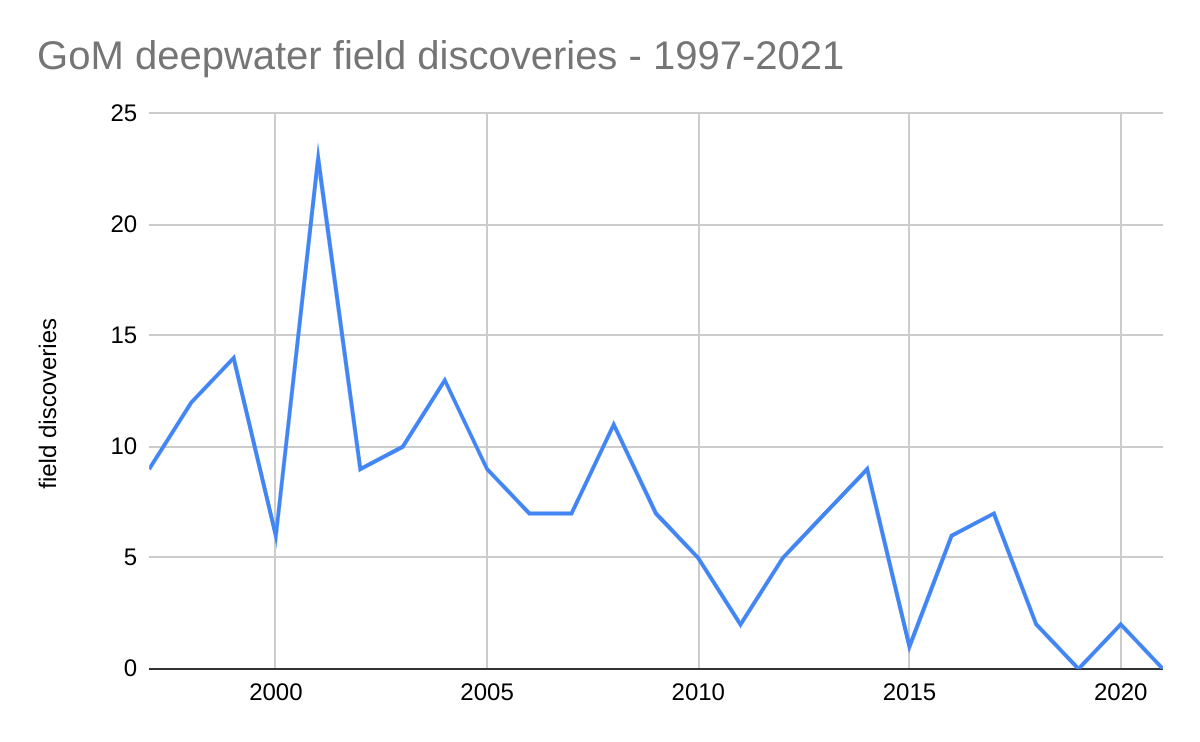

The decline in reserves should come as no surprise to those who follow the US offshore sector. Note the sharp decline in exploratory drilling in the (updated chart below) and the calls for action on this blog a year ago and more recently.

The OCS oil and gas program requires a sustained, consistent commitment by government and industry. Such a consistent commitment, even though required by legislation, is difficult to achieve in our political system, .

The commitment by the oil and gas industry has also been uneven and in some cases disappointing. BOE continues to be troubled by the reduction in exploration by some companies and the decision by others, including leading US companies with a long history of Gulf of Mexico operations, to exit the US offshore sector completely (see the chart below). The exploration decline began before the leasing shutdown (now 600 days in duration). Inconsistent signals from the Federal government and corporate directors, market considerations, and competing investment opportunities are major factors, but there are no doubt other considerations. Constructive dialogue to address these issues is badly needed.

Declines in drilling activity and discoveries suggest that higher real oil prices are on the horizon. We may be fortunate enough to escape significant price hikes and supply disruptions over the next couple of years, but they are coming.

US offshore trends are even more troubling. Per BOEM’s database, no deepwater fields were discovered in 2021 and there were only 2 discoveries in the past 3 years (see chart below). HartEnergy reports 5 announced discoveries in 2021, none of which has been determined by BOEM to be commercially producible. Regardless of the status of those 2021 determinations, recent discoveries have not been sufficient to reach and sustain GoM production volumes at the 2019 peak (August) of 2.044 million BOPD. 2019 was the first year since 1982 without a confirmed deepwater discovery and the trend (below) is not encouraging. Schlumberger data through 2016 indicated GoM depletion rates greater than 20%, and the subsequent low discovery rates do not bode well for future production trends.

from BOEM data

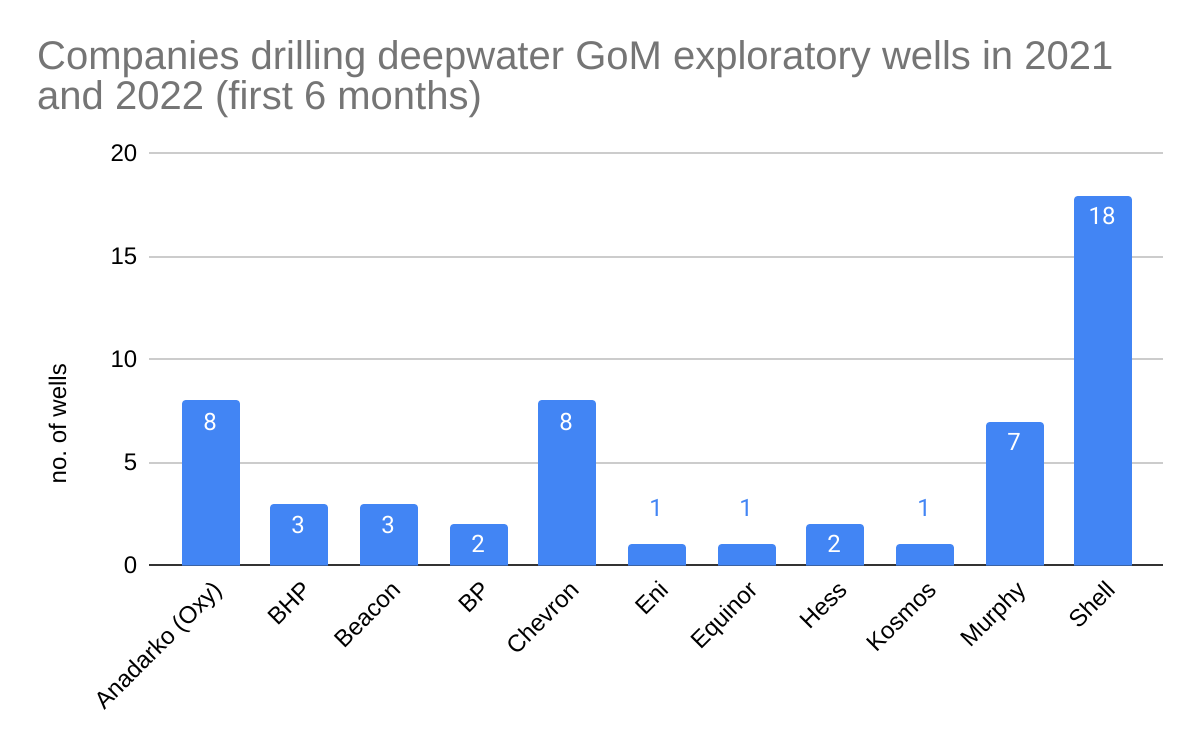

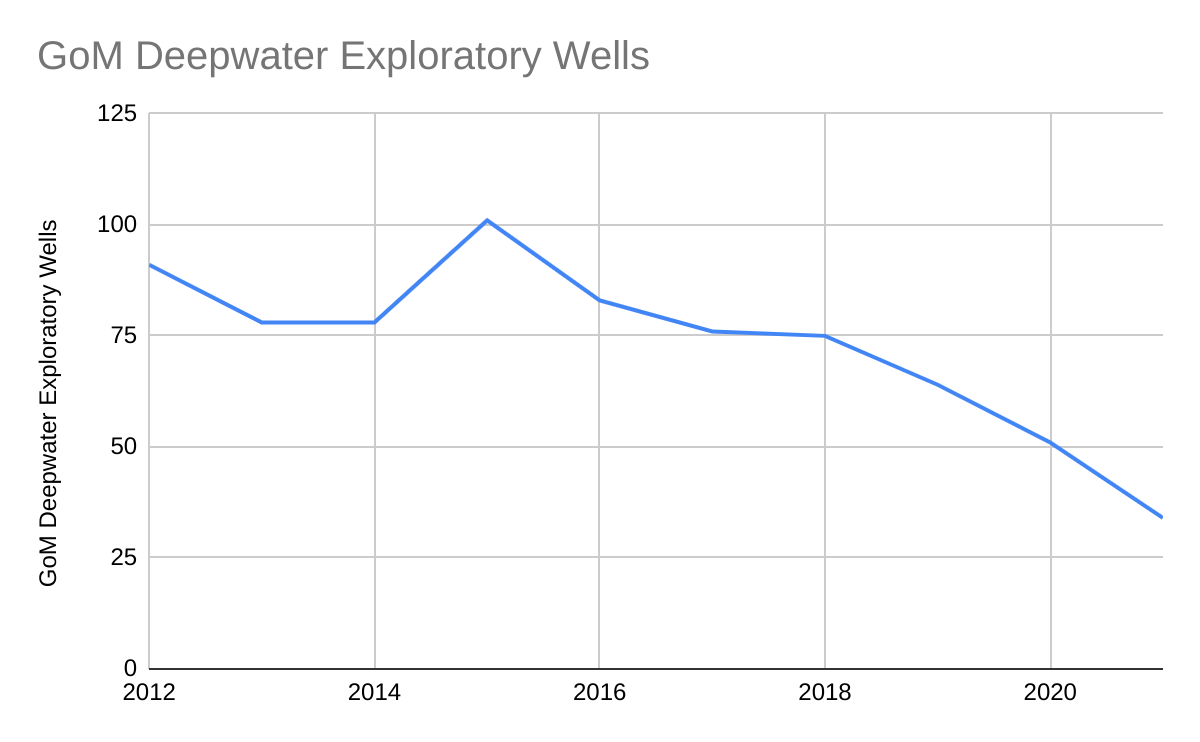

You can’t make discoveries without drilling and only 9 companies drilled deepwater GoM exploratory wells in 2021 (34 wells total). With the Pacific in decommissioning mode, the Atlantic and Eastern GoM off-limits, limited options offshore Alaska, and the decline of the GoM shelf, the deepwater GoM is the only important US offshore production option. The exploration numbers below are therefore concerning.

The shale revolution made the US a net oil exporter, but skepticism about shale production forecasts suggests the need for other supply sources. Given the shale uncertainty and the unrealistic expectations regarding the energy transition, greater US dependence on imported oil is on the horizon. This bodes well for OPEC, but not so well for US and international consumers.

Meanwhile, the US Dept. of Energy shows no evidence of concern about oil and gas production. Although oil and gas account for about 70% of our energy consumption, there has been no mention of either on the DOE homepage for months. DOE does express a strong interest in “energy justice.” Perhaps they can explain how increased imports and higher energy prices benefit the poor. They should also explain how oil imports are environmentally and economically superior to domestic oil and gas production, when the reality is exactly the opposite.