In 2016, this old Transocean semisubmersible was being towed from Norway to Malta prior to being scrapped in Turkey. The rig broke free and grounded at Dalmore, Scotland. This picture, with a Scottish cemetery in the foreground, is a fitting tribute to old rigs, the wells they drilled, the storms they endured, and the people they served.

The picture and title will be added to our world-famous Rigs-to-Reefs+++ page. Many thanks to those who have contributed to this important resource over the years.

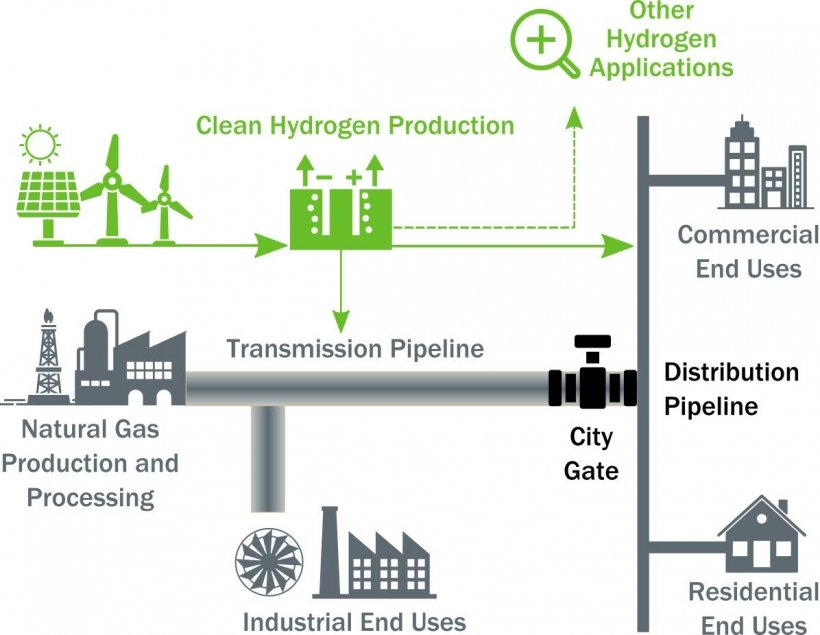

The study will help to determine the extent to which hydrogen can be transported in natural gas pipelines without introducing embrittlement and other pipeline safety risks.

The video below is from 6 months ago but is even more relevant today. Those who produce nothing but insults shouldn’t be dictating corporate strategy.

Rep. @ByronDonalds: "How do we ever expect to beat [China] on the world stage when we're cutting our neck when it comes to energy production while they are burning more coal, burning more oil, they're increasing their emissions and they're not showing up in Scotland." pic.twitter.com/WnIyUbKKPG

After 8 outstanding years with Australia’s offshore safety and environmental regulator, Stuart Smith has announced that he will be departing NOPSEMA in September. Stuart was a highly effective CEO and an important contributor to international offshore safety initiatives. Best wishes to Stuart!

Department of the Interior spokesperson: “there are 10.9 million acres of offshore federal waters already under lease to industry,” and “of those, the industry is not producing on more than three-quarters (75.7% or 8.26 million acres).”

As if the preventable expiration of the 5 year leasing program wasn’t bad enough, we get to hear the non-producing leases bit yet again. This pitch was popularized during the oil embargoes in the 1970’s and resurfaces whenever it is deemed to be politically helpful.

The decline in the number of producing leases since 2011(62%) has been less than the decline in the number of active leases (71%).

DOI’s primary concern should be the preventable decline in active leases.

Old comments:

539 days since the last US offshore oil and gas lease sale

182 lease sales since 1954, but none since 2020

Only 0.5% of US offshore land is leased for oil and gas exploration and production (assuming commercial quantities of oil and gas are discovered).

When you acquire a lease, you are not purchasing oil and gas. You are acquiring the right to explore for, and hopefully produce, those resources. Most leases will never produce.

Drilling strategies are linked to geophysical data and geologic information obtained in drilling other wells in the area and region.

Leases expire if they are not producing by the end of the lease term, which is 5 to 10 years depending on location.

You pay bonuses for all leases and annual rental fees for non-producing leases. None of these payments are returned if no discoveries are made.

These provisions were added to the bill without debate and their inclusion was a surprise to most observers. Presumably, DOI had the opportunity to review the text, because that is standard practice.

Sale 257 was vacated by the DC Federal Court for reasons unrelated to the sequestration bids.

Questions:

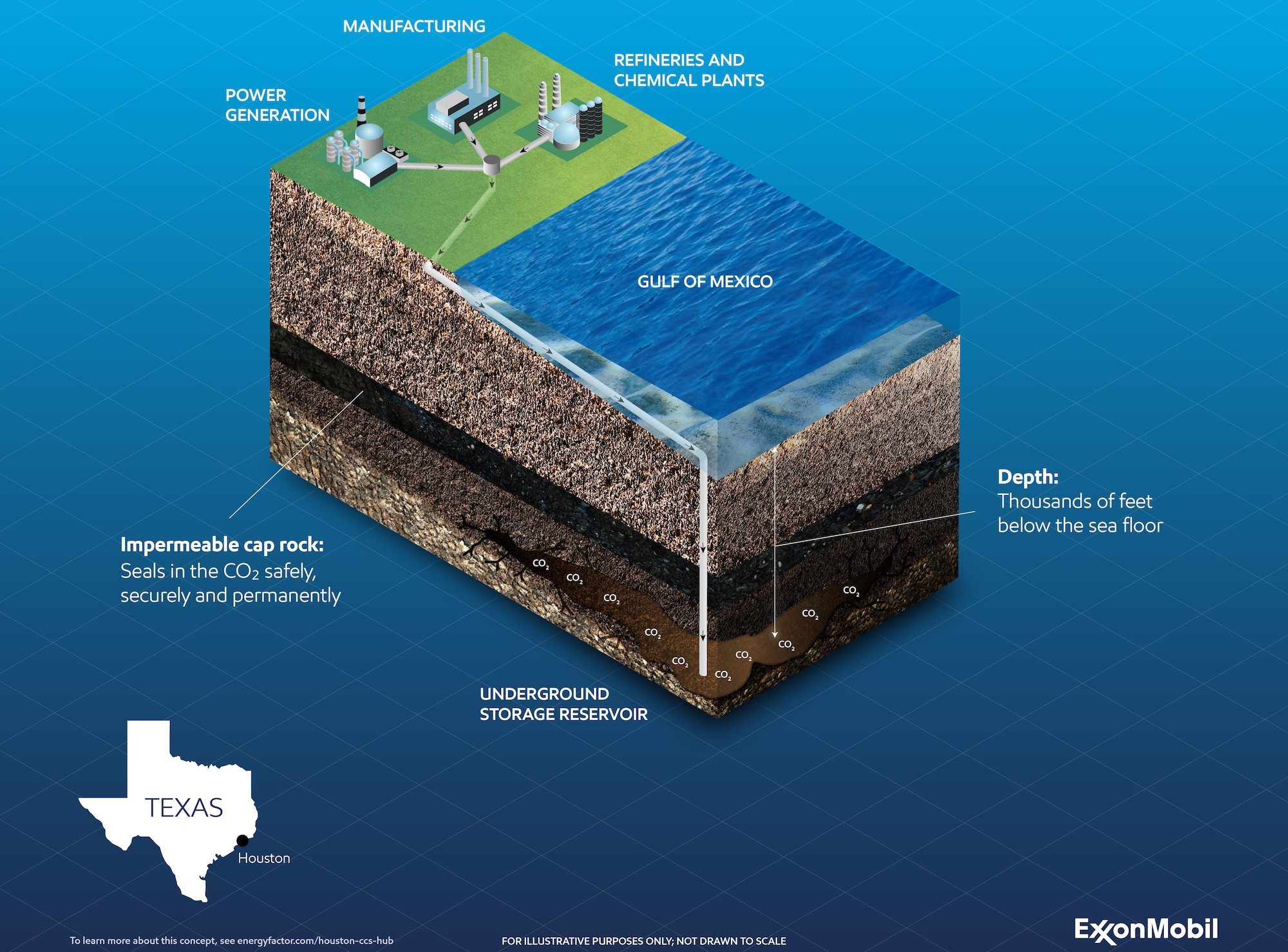

What are the costs per ton of offshore carbon sequestration including emissions collection, offshore wells and platforms, the associated pipeline infrastructure, ongoing operational and maintenance costs, and decommissioning?

What is the timeframe given that the starting point is likely years away?

How long would CO2 sequestration continue.

Who pays? Polluters? Federal subsidies? Tax credits?

Who is liable for:

safety and environmental incidents associated with these projects?

CO2 that escapes from reservoirs, wells, and pipelines (now and centuries from now)?

decommissioning?

hurricane preparedness and damage?

For Gulf of Mexico sequestration, how much energy would be consumed per ton of CO2 injected? Power source? Emissions?

To what extent will these operations interfere with other offshore activities?

Relatively speaking, how important is US sequestration given:

the steady progress that is being made via natural gas and renewables?

What are the benefits of offshore sequestration relative to investments in other carbon reduction alternatives?

Will BOEM conduct a proper carbon sequestration lease sale with public notice (as required by BOEM regulations) such that all interested parties can bid?

What will be the lease terms?

Environmental assessment?

How will bids be evaluated?

What happens to the Exxon bids if the Judge’s Sale 257 decision is reversed?

What is the status of the DOI regulations mandated in the legislation with an 11/15/2022 deadline?

When will we see an Advanced Notice or Notice of Proposed Rulemaking?

Given that DOI has no jurisdiction over the State waters and onshore aspects of these projects, what is the status of parallel regulatory initiatives?

Finally and most importantly, how does drilling offshore sequestration wells instead of exploration and development wells increase oil and gas production?

….for continuing to recognize the Conservation Division of the Geological Survey (USGS) as the US offshore safety regulator, even though 40 years have passed since that was the case and there have been 3 successor bureaus. 😀

(a) Design and equipment requirements of this subchapter for OCS facilities, including mobile offshore drilling units in contact with the seabed of the OCS for exploration or exploitation of subsea resources, are in addition to the regulations and orders of theU.S. Geological Survey applicable to those facilities.

USGS North Atlantic District, Hyannis, MA, Halloween 1980

Most of us old-timers think the best regulatory framework for the offshore program was in the USGS days (pre-1982). Some of this may be nostalgia, but there are some good reasons for this thinking:

USGS was/is an internationally acclaimed scientific organization that was always headed by a renowned geologist. The regulatory program was thus somewhat insulated from political pressures. Vince McKelvey, Bill Menard, and Dallas Peck were the Directors when I worked for USGS. Their credentials are linked. Bill and Dallas visited our Hyannis office (not at Halloween 😀) and were very supportive.

The Conservation Division was responsible for onshore operations on Federal lands as well as offshore activity. This facilitated information sharing and offered diverse career opportunities. My first bosses in New Orleans had worked previously in the Farmington and Roswell, NM offices.

We had excellent synergy with the other USGS divisions. The Marine Science Center in Woods Hole was an incredible resource for our Hyannis office. The Woods Hole office, particularly Mike Bothner and Brad Butman, had a critical role in the Georges Bank Monitoring Program, the best ever (in my biased opinion) environmental study of exploratory drilling operations in a frontier area.

The USGS Conservation Division had a very small and supportive headquarter’s staff, which minimized the potential for conflict with field offices.

Prior to the formation of the Minerals Management Service (MMS) in 1982, the Bureau of Land Management was responsible for leasing, but all regulatory functions were under USGS. This included resource evaluation/conservation, plan review and approval, permitting, inspections and enforcement, and investigations. The division of MMS responsibilities, most notably the assignment of plan approval to the leasing bureau (BOEM) rather than the regulatory bureau (BSEE), complicates the work of both bureaus and is a prescription for inefficiency, confusion, overlap, and conflict.

Operating companies that produced >1 million bbls of oil or >1 BCF of gas in 2021 are listed in descending order based on oil production.

Both the total number of well starts and the number of exploratory wells are indicated

An INC is an Incident of Noncompliance (i.e. a violation). W=warning, CSI=component shut-in, and FSI=facility shut-in are the enforcement actions.

All of the below data are publicly available on the BSEE-BOEM websites.

2021 oil (MMbbls)

2021 gas (BCF)

2021/22 well starts total-expl

2021/22 INCs W-CSI-FSI

Shell

149.8

190.8

28-12

11-14-4

bp

114.0

82.7

5-2

6-3-4

Chevron

83.7

42.2

8-8

1-1-3

Anadarko (Oxy)

67.7

57.8

8-6

8-5-1

Hess

27.5

61.7

2-2

7-4-0

Murphy

25.1

50.0

7-7

4-8-1

LLOG

20.4

29.0

3-0

1-1-1

Talos

17.7

23.0

5-0

25-26-14

BHP

14.5

5.9

3-2

2-3-0

Exxon

13.2

2.3

–

1-1-1

Beacon

10.5

15.7

1-0

0-0-0

Fieldwood

10.4

24.7

–

685-235-91

EnVen

9.6

12.6

6-0

2-6-3

Kosmos

9.4

8.4

1-1

1-0-0

Arena

8.6

27.9

32-0

68-45-19

Walter

8.1

36.2

2-2

3-1-2

Cox

6.2

30.3

–

237-169-3

Eni

4.7

13.6

2-0

8-0-2

W&T

5.0

27.2

1-0

65-40-7

Cantium

4.5

5.5

18-0

23-15-2

QuarterNorth

4.2

8.3

–

no data

GoM Shelf

2.3

4.8

–

52-5-2

ANKOR

1.4

2.5

–

0-0-1

Byron

1.0

4.4

–

5-8-2

Renaissance

0.7

1.6

–

20-9-3

Sanare

0.3

4.5

–

38-20-3

Helis

0.2

1.2

–

1-0-2

Contango

0.03

5.0

–

4-0-0

Samchully

0.02

1.2

–

no data

Comments:

“Energy transition” companies Shell and bp still love the Gulf of Mexico, which is a good thing for them and us. Together they accounted for 42.4% of the 2021 oil production.

The top 4 producers, Shell, bp, Chevron (includes Unocal), and Anadarko accounted for 2/3 of GoM oil production, nearly all of which was from deepwater leases.

Those are impressive production numbers for Anadarko (Oxy). No wonder Warren Buffett likes Oxy stock.

The relative number of deepwater exploratory wells is mildly encouraging given our concerns about sustaining production.

Exploratory well determinations are rather subjective and may not be entirely consistent.

Understandably, no exploratory wells were drilled by Arena or Cantium, the companies responsible for most well operations on shelf (shallow water) leases.

Overall, the INC numbers are impressively low for the deepwater operators, with Chevron and LLOG standing out. BSEE does not post the specific violation information (more on this in an upcoming post), so it’s difficult to properly assess a company’s compliance record.

Unfortunately, incident data could not be included on the scoreboard. BSEE’s incident tables are badly out of date, and no 2021/2022 summaries have been posted.

Exxon production is limited to the Hoover Diana spar, which was installed 22 years ago. The largest US oil company has only drilled one GoM exploratory well (2018) in the past 5 years. Currently, their main GoM interest seems to be the sequestration (disposal) of onshore emissions. (More on this topic in an upcoming post.)