HOUSTON, Nov 6 (Reuters) – Exxon Mobil Corp will take up to a $2 billion loss on the highly leveraged sale of a troubled California offshore oil and gas field that have been idled since a 2015 pipeline spill.

Sable Offshore, a blank check company founded by industry veteran James Flores, will borrow 97% of the $643 million purchase price from Exxon under a five-year loan. Blank check companies raise money to acquire operating businesses. If Flores fails to restart production at the Santa Ynez field by the start of 2026, Exxon could take back the entire operation, Sable disclosed in a filing.Flores will seek permits to restart Santa Ynez and expects to pump about 28,100 barrels of oil and gas per day beginning in 2024, according to a Sable investor presentation. The field has 112 wells and the potential for at least another 100 wells, its presentation showed.

Jim Flores is well known in the offshore industry dating back to his days as CEO of Flores & Rucks, a Gulf of Mexico exploration and production company, in the 1990’s.

And Exxon is no doubt still on the hook for decommissioning these massive platforms.

These oil and gas leases may not be repurposed for sequestration or other purposes unless an alternate use RUE is issued competitively in accordance with 30 CFR § 585.1007.

So what’s next for these 94 leases, 31% of the entire sale?

When can we expect a statement from Exxon on their intentions for the 94 blocks they acquired? Those 94 blocks (31% of the entire sale) are the elephant in the room, yet we have heard nothing from the company. Given Exxon’s apparent interest in using these leases for CCS purposes, and the tax credits and Federal funding associated with CCS projects (as per the Infrastructure Bill and Inflation Reduction Act), clarification regarding Exxon’s intentions would seem to be appropriate.

From 1997 to 2007, Aera operated the Beta Unit offshore Huntington Beach. Since selling those facilities, all Aera operations have been conducted onshore, primarily in Kern County, a historically important California oil production area. Aera will continue to operate these onshore properties for IKAV, which looks like an interesting company.

The subject legislation requires the Secretary of the Interior to accept the highest valid bid that was received for each tract offered in OCS Lease Sale 257. Exxon was the sole bidder on 94 tracts on the nearshore Texas shelf. The leases were to be acquired for carbon sequestration purposes.

The CCS bids should not be considered valid given that:

Sale 257 was an oil and gas lease sale. The Notice of Sale said nothing about carbon sequestration and did not offer the opportunity to acquire leases for that purpose. Therefore, the public notice requirements for CCS leasing (30 CFR § 556.308) were not fulfilled.

Because there was no draft or final Notice of Sale, interested parties and the public did not have the opportunity to consider and comment on CCS leasing, tract exclusions, bidding parameters, and other factors.

30 CFR § 556.308 requires publication of a lease form. No CCS lease form was posted or published for comment.

CCS operations were not considered in the environmental assessments conducted prior to the sale.

No evaluation criteria for CCS bids have been published.

Unexpectedly, the Infrastructure Bill, signed on 11/15/2021 (just 2 days before Sale 257) included a provision for OCS carbon sequestration. However, that legislation did not require CCS leasing or authorize DOI to sell CCS leases as part of an oil and gas lease sale; nor did it exempt DOI from complying with its leasing regulations. Instead, It gave the Secretary a year (until 11/15/2022) to promulgate necessary implementing regulations. If carbon sequestration in the Gulf of Mexico is deemed to be desirable, a separate CCS sale should be held when the regulatory framework has been established.

Foremost energy experts like Daniel Yergin understand that oil and gas will be critical to our economy and security for decades, and that offshore production is an important component of our energy supply chain. Unfortunately, our massive outer continental shelf has, from an oil and gas standpoint, been effectively reduced to the central and western GoM.

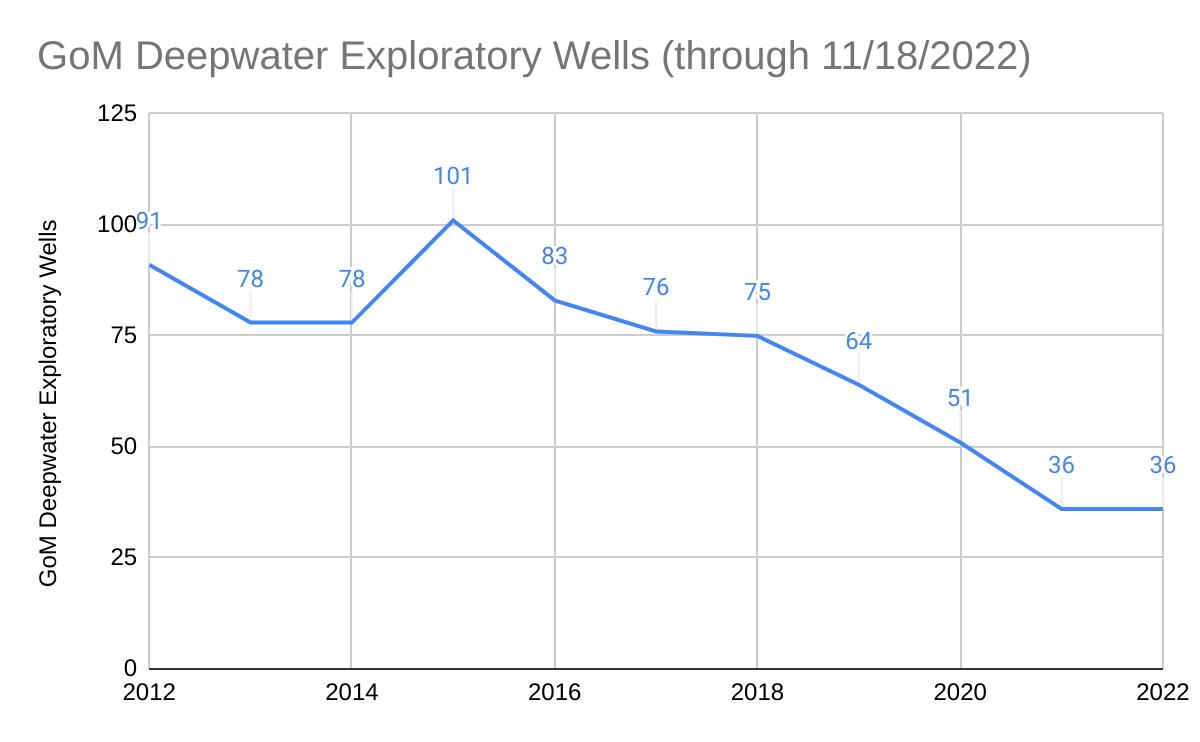

Opportunities in the GoM are being seriously constrained by the extended pause in leasing. A lease sale has not been held for 615 days, the longest US offshore leasing gap since the 1950’s.

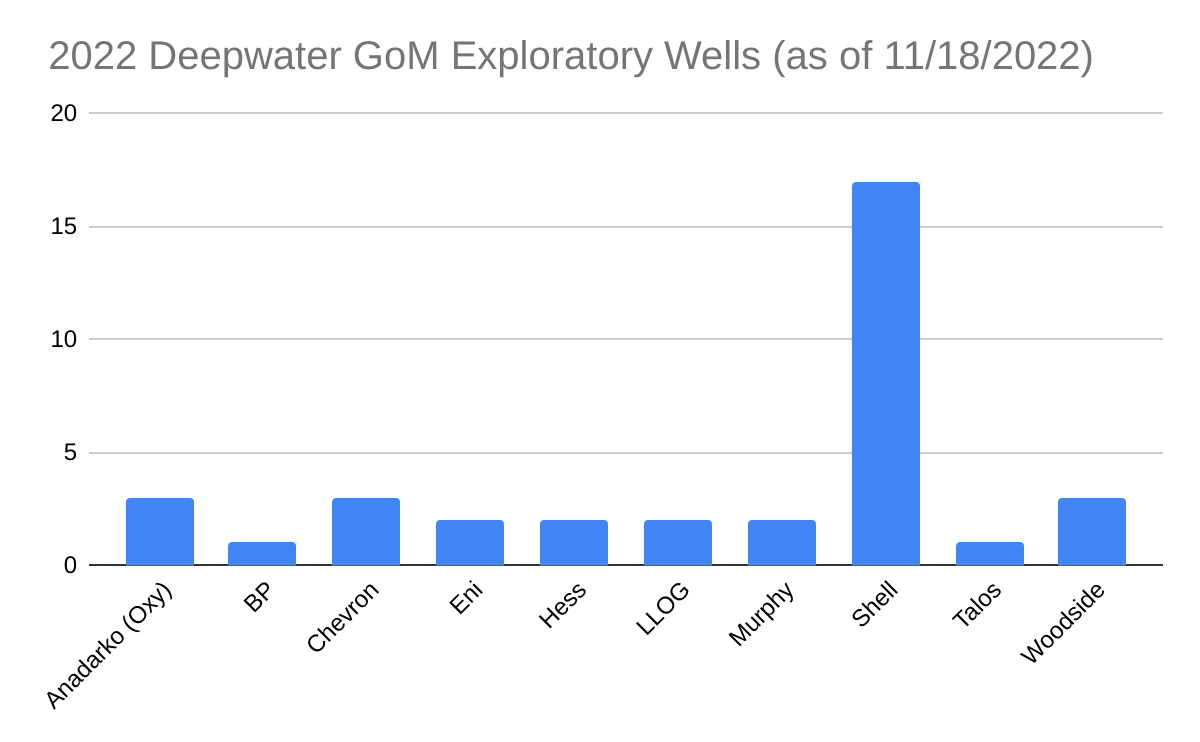

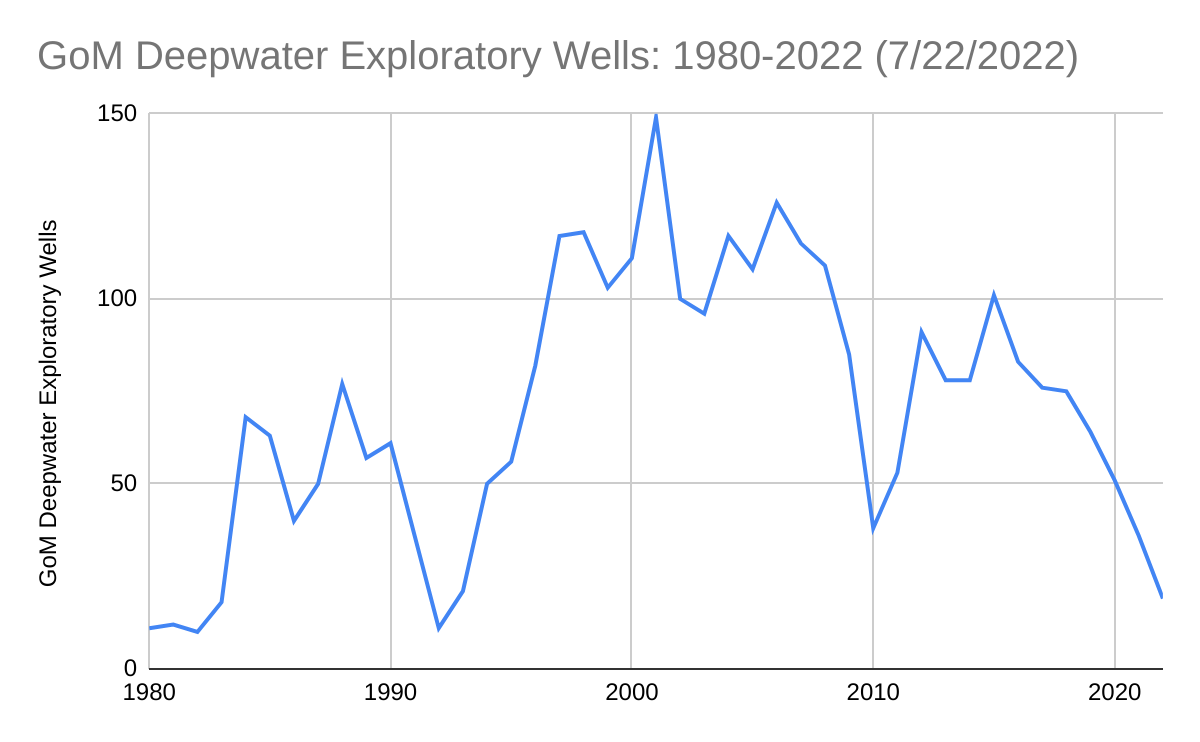

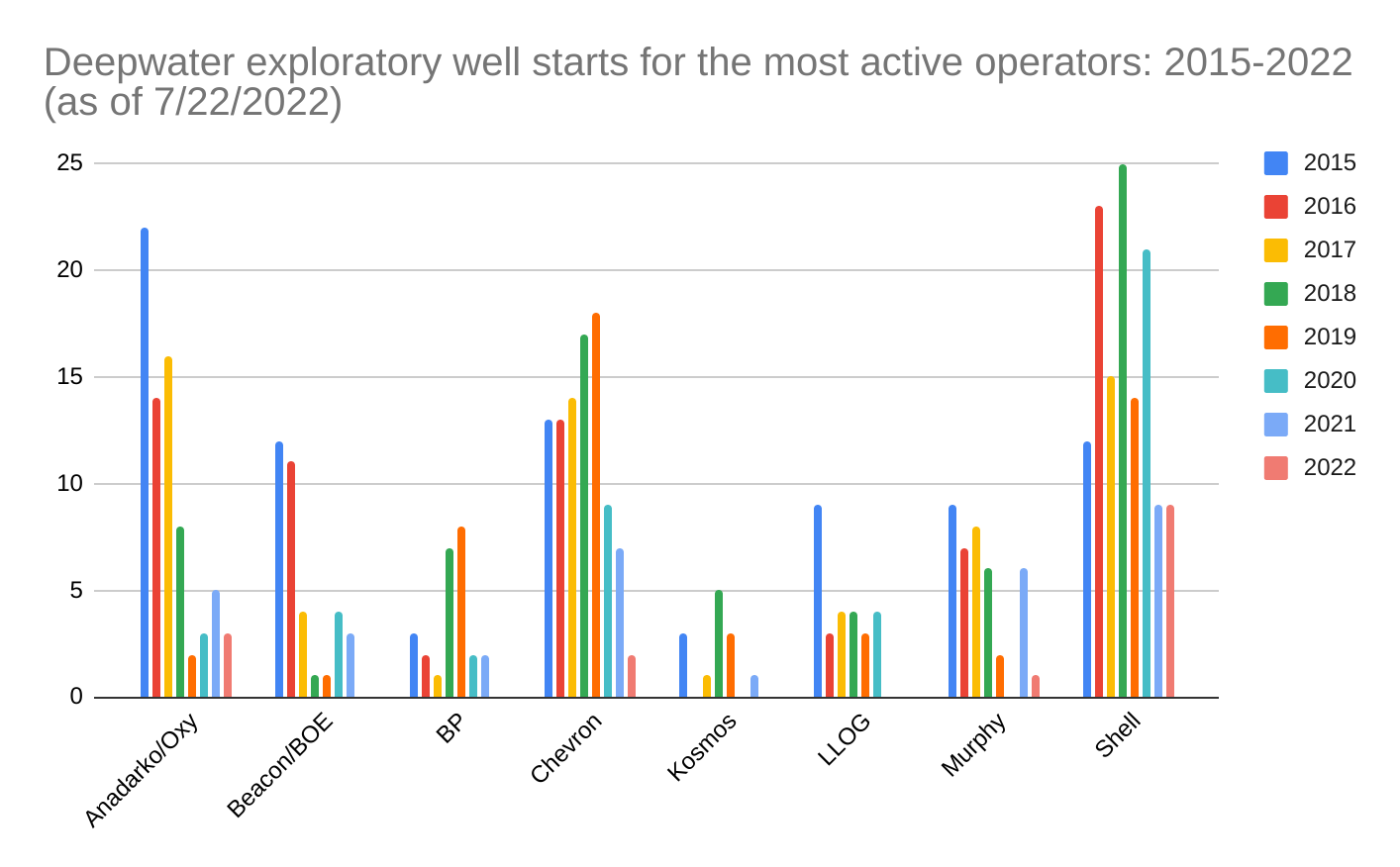

Reserve replacement and sustained production are dependent on exploration. The charts below illustrate the decline in GoM exploratory drilling and the reduced activity by some of the more important operating companies.

Per BSEE data, the number of exploratory well starts averaged only 3/month for the last 18 months (chart 2). This level of activity is the lowest since the early days of deepwater operations (chart 1). There was even more drilling during the post-Macondo moratorium (2010-2011).

ConocoPhillips and Exxon have not drilled a GoM exploratory well since 2016 and 2018 respectively. Activity by other operators has also declined significantly (chart 3). BP has not spudded an exploratory well since Sept. 2021.

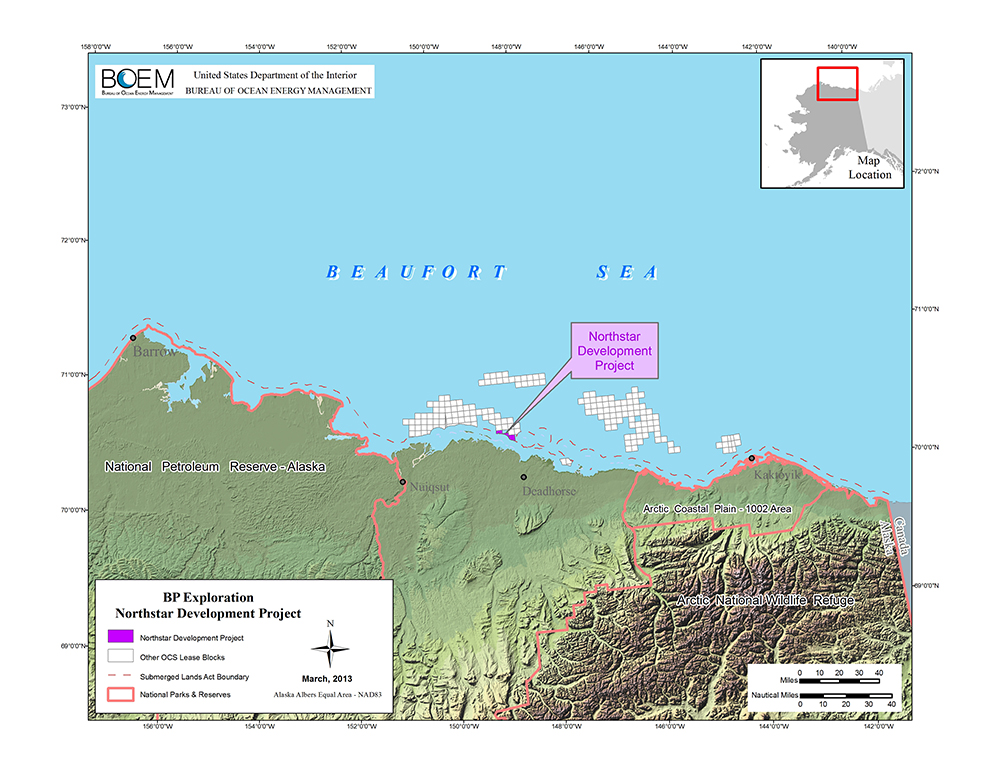

The only current Alaskan OCS production is from Northstar, a joint State-Federal Unit in the Beaufort Sea. The production island is in State waters, but 7 of the wells produce from the Federal sector. The field was originally developed by bp, but Hilcorp is the current operator. To date, BSEE has conducted 5 inspections of the facility in 2022, and no incidents of noncompliance (INCs) were identified.

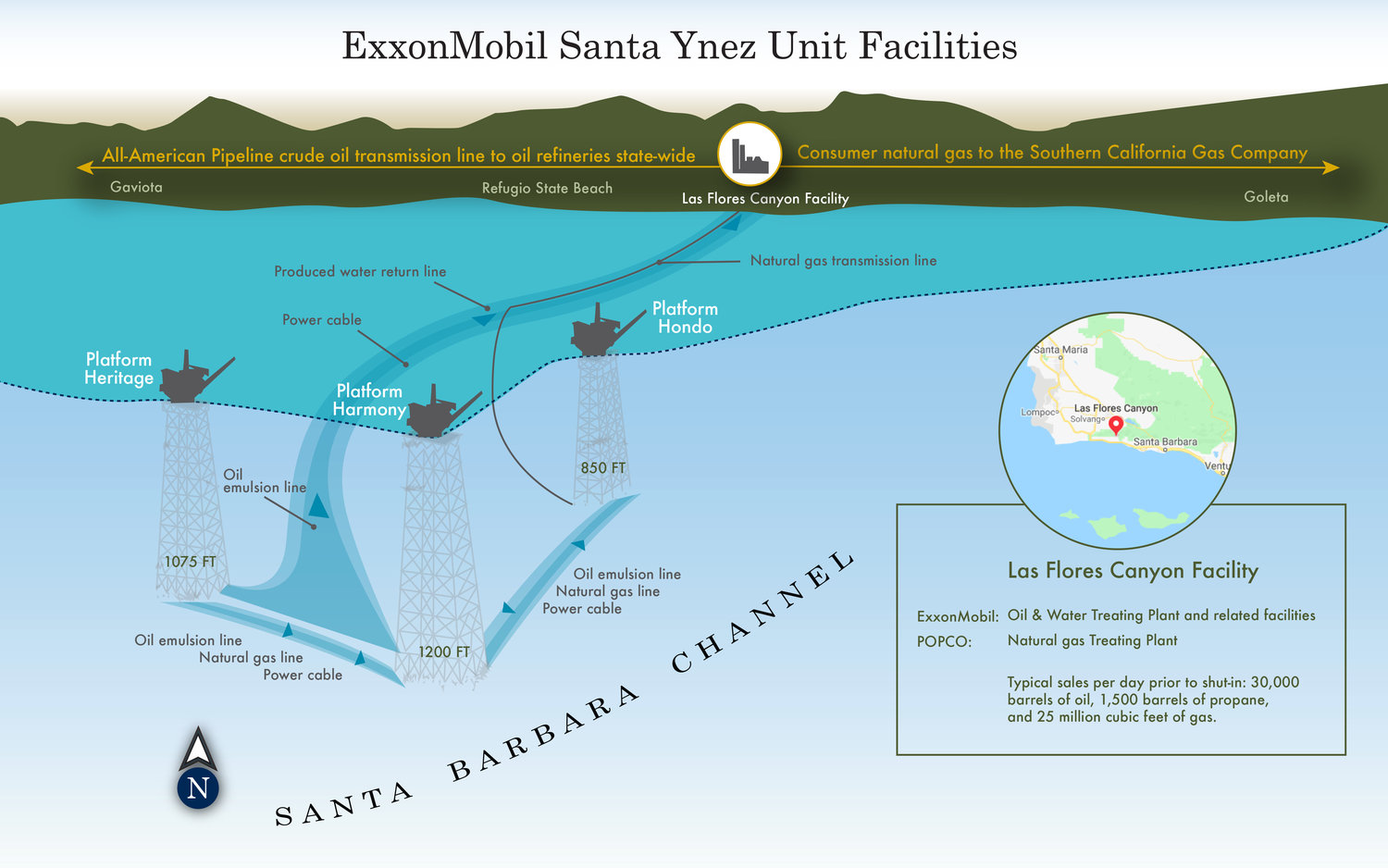

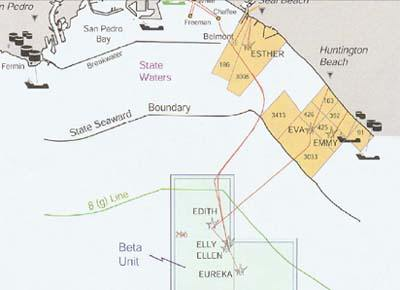

Per BOEM records, 4 companies operate Pacific (California) OCS facilities that are currently producing. Three of those operators have superior 2022 inspection records. No INCs were issued to either Exxon (11 Santa Ynez Unit inspections) or Freeport-McMoRan (24 Platform Irene inspections). Only 2 warning INCs were issued during 12 inspections of Beta Operating Co. platforms Ellen, Elly, and Eureka in the Beta Unit offshore Long Beach.

Apple has full control over the price of its products and trounces ExxonMobil’s earnings in every quarter. Apple could slash the price of its products and still make a huge profit. But ExxonMobil can’t slash the price of its products because it doesn’t set the price.

In the short term, the U.S. government could enact measures often used in emergencies following hurricanes or other supply disruptions — such as waivers of Jones Act provisions and some fuel specifications to increase supplies. Longer term, government can promote investment through clear and consistent policy that supports U.S. resource development, such as regular and predictable lease sales, as well as streamlined regulatory approval and support for infrastructure such as pipelines.

Perhaps Exxon will return to the Gulf of Mexico if the Administration commits to regular and predictable oil and gas lease sales. The company hasn’t drilled a well in the Gulf since 2019.

The longer API letter comments on the fundamentals of refining markets and operations while also addressing the Administration’s “end fossil fuel rhetoric” and negative regulatory signals. Who would want to make major refinery investments under these circumstances?