This Court should grant Plaintiffs—the State of Louisiana, the American Petroleum Institute (“API”), and Chevron U.S.A. Inc. (“Chevron”)—a preliminary injunction and prevent those unlawful provisions from permanently disrupting the result of the fast-approaching lease sale (which Congress has directed must occur by September 30, and which cannot be delayed without causing Plaintiffs even more serious injury).

From a regulatory policy standpoint, this appears to be a strong filing. Operationally, the most important points pertain to the costly and premature Rice’s whale restrictions first discussed on this blog.

Most notably, the plaintiffs seek (p.39):

A preliminary and permanent injunction striking, setting aside, and enjoining BOEM from implementing the specific challenged provisions of the Final Notice of Sale and Record of Decision for Lease Sale 261;

An order vacating the specific challenged provisions of the Final Notice of Sale and Record of Decision for Lease Sale 261;

An order compelling Defendants to proceed with Lease Sale 261 on September 27, 2023, without the challenged provisions;

Keathley Canyon (KC) Block 96, the tract receiving the highest bid in the entire sale ($15,911,947 by Chevron), had a BOEM MROV of only $576,000. Clearly, Chevron and the government have a very different view of the value of this tract. BP was the second bidder for KC 96, and their bid ($4,003,103) was also considerably higher than BOEM’s MROV. This one will very interesting to follow.

The only bid that was rejected in Sale 257 was the BP/Talos bid of $1.8 million for Green Canyon Block 777. BOEM’s MROV in the Sale 257 evaluations was $4.4 million. BP again bid on GC 777 in Sale 259, but their bid was only $583,000 (even though BOEM’s Sale 257 evaluation was public information). BOEM’s MROV was reduced only slightly to $4.2 million, and they again rejected BP’s bid. We’ll see what happens in the next sale.

51 of the 230 accepted bids were >$1 million, all for deepwater tracts. All of the rejected bids were for deepwater tracts, and a higher percentage (4/14) were >$1 million. This makes sense given that the higher potential prospects are in deepwater.

These results demonstrate again that resource evaluation is far from an exact science. BOEM is not selling barrels of oil and cubic feet of gas. BOEM is evaluating prospects, and companies are bidding on the opportunity to explore these prospects.

Bidding strategies differ; the more companies participating, the better the long-term prospects for the OCS program.

Per the BSEE borehole file, there were 2 deepwater exploratory well starts since 4/1/2023. The Shell well is another GoM milestone in that it is the 150th well spudded in >8000′ of water. The first was in the year 2000.

Operator

spud date

location

water depth

Chevron

5/5/2023

Mississippi Canyon 608

6678′

Shell

4/13/2023

Alaminos Canyon 728

8660′

Arena and Cantium continue to drive shelf drilling. Below are the shelf development wells since 4/1/2023:

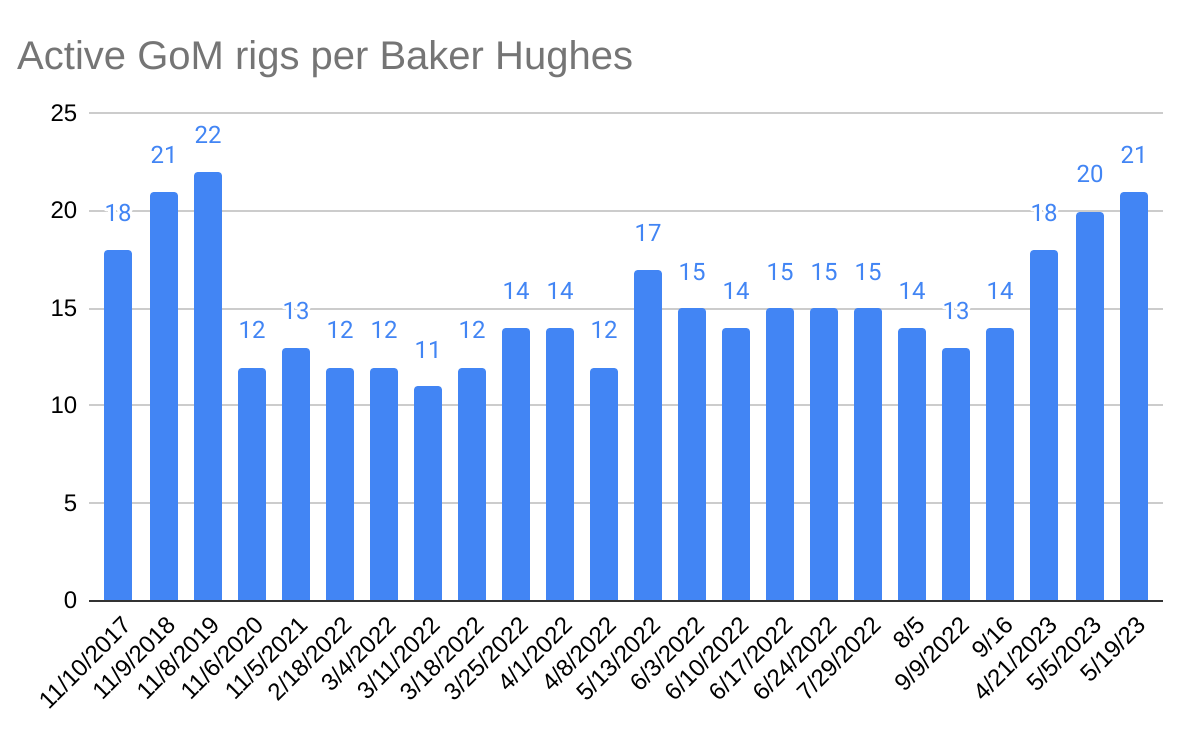

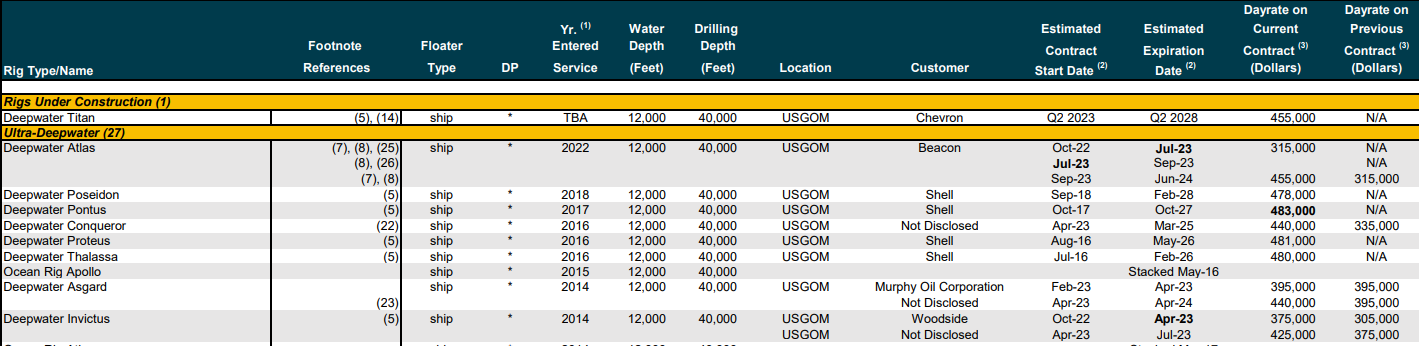

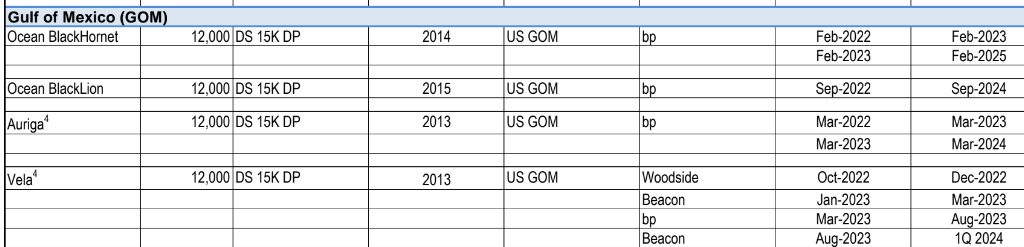

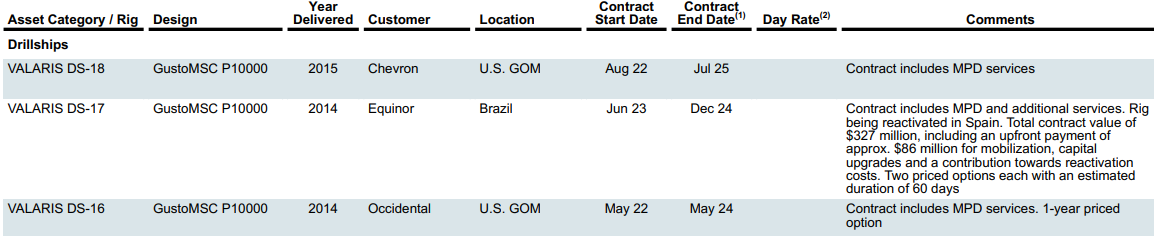

Based on drilling contractor rig activity reports, the table below lists 19 deepwater MODUs under or soon to begin contracts in the GoM. (Further details are pasted at the end of this post.) Per the Valeris report, platform rigs are operating on bp’s Thunder Horse and Mad Dog platforms. Per the BSEE borehole file, Arena and Cantium continue to drill development wells on the GoM shelf.

Prior to the installation of these platforms, the last deepwater platform addition was Shell’s Appomattox in 2018. That gap in deepwater platform installations was the longest since Bullwinkle was installed in 1988.

The 5 new structures will increase the deepwater platform count by 9% from 56 to 61, and in the next few years should account for approximately 1/4 of GoM oil production.

Exxon doubled down on their strategic CCS bidding; their only bids (69 in total) again appeared to be solely for carbon sequestration purposes. As previously noted, acquiring tracts for CCS purposes is not authorized in an oil and gas sale. Arguably, these bids should be rejected.

The other super-majors, BP, Chevron, and Shell, were active participants as were many independents.

It was good to see BOEM Director Liz Klein announcing bids. This shows respect for the OCS oil and gas program.

BOEM published their Sale 257 Decision Matrix on Friday (2/24/2023), and my previous speculation regarding the rejected Sale 257 high bid has proven to be partially incorrect. The rejected high bid was submitted by BP and Talos and was for Green Canyon Block 777. BOEM’s analytics assigned a Mean of the Range-of-Value (MROV) of $4.4 million to that tract, which tied for the highest MROV for any tract receiving a bid. The BP/Talos bid was $1.8 million or just 40% of BOEM’s MROV. BOEM’s tract evaluation is interesting given that the other bid on this wildcat tract (by Chevron, $1.185 million) was considerably lower than the rejected BP/Talos bid.

The Sale 257 bid that I thought might have been rejected was for lease G37261. This lease was never issued per the lease inquiry data base and the final bid recap. BHP’s bid of $3.6 million for that tract (Green Canyon Block 79) was more than 5 times BOEM’s MROV of $576,000, and was accepted per the decision matrix. Why was the lease never issued?

Both Green Canyon 79 and 777 should again be for sale in legislatively mandated Sale 259, which will be held in just a few weeks on March 29, 2023, just 2 days prior to the deadline. It will be interesting to see what the bidding on those tracts looks like.

Meanwhile, Exxon and BOEM are still mum about the 94 Sale 257 oil and gas leases that Exxon acquired for carbon sequestration purposes.Note the large patches of blue just offshore Texas on the map above. These leases were all valued by BOEM at only $144,000 each, which is equivalent to the minimum bid of $25/acre. This valuation reflects the absence of perceived value for oil and gas production purposes. Exxon bid $158,400 for each tract, $27.50/acre or 10% higher than the minimum bid. Given that (1) the Notice of Sale only provided for lease acquisition for oil and gas exploration and production purposes, and (2) it was common knowledge that these tracts were acquired for carbon sequestration, should these bids have been rejected?