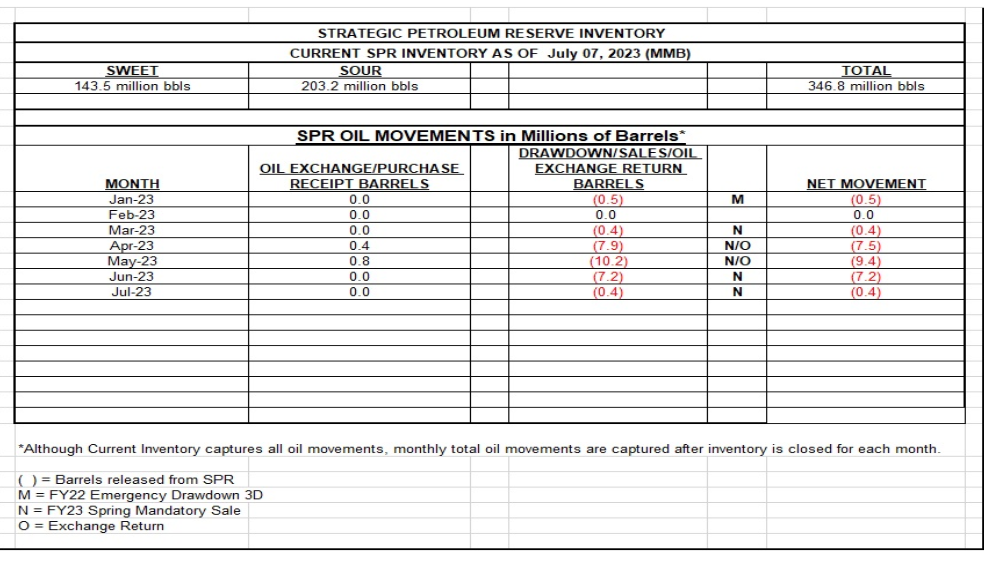

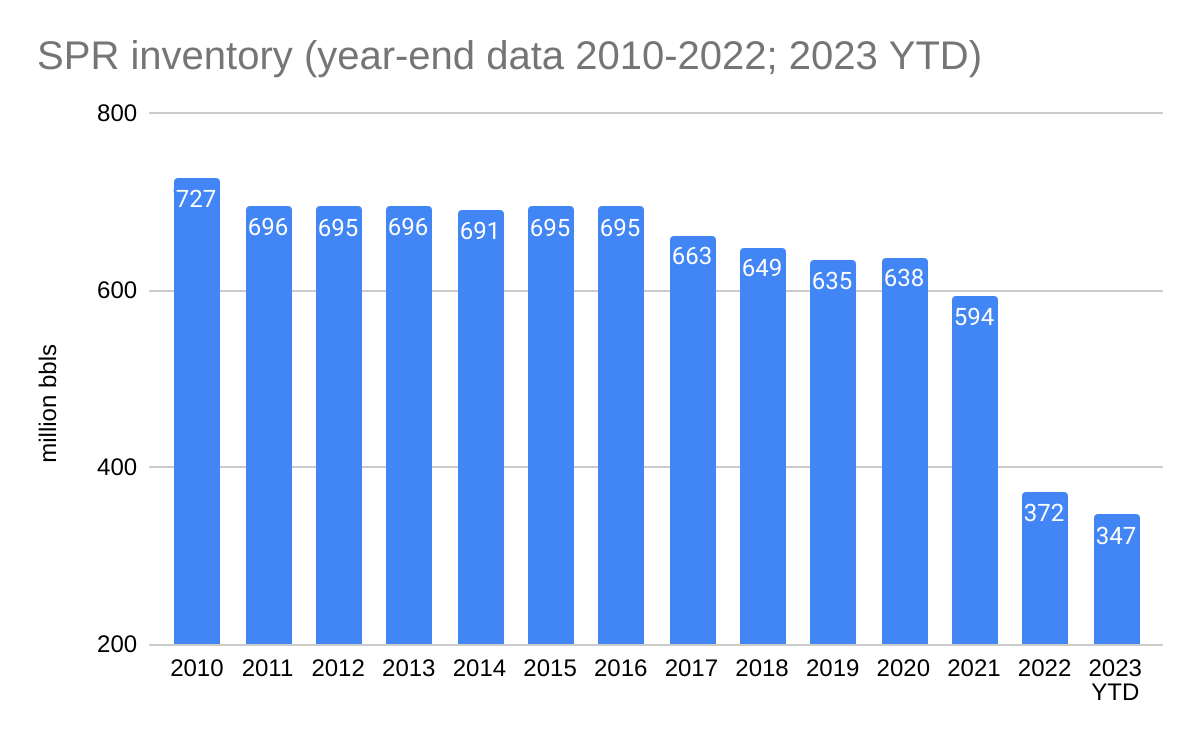

Keep in mind that DOE only intends to buy when prices are <$72/bbl, that the maximum refill rate is 685,000 bopd, and that acquisition, operational, and maintenance delays are to be expected .Filling the reserve to its 727 million barrel capacity was a 28 year process.

Pioneering subsea engineer, JL Daeschler, brought to my attention the little known sinking of the Sedco 135 B semisubmersible drilling rig (pictured above) while in transit from Hiroshima to Borneo in 1965. 13 workers died in this tragedy. Miraculously, a single survivor, dehydrated and floating on a wooden pallet, was found days later by a passing Japanese trawler.

The bottle shape of the columns with the tapered top section was intended to reduce the influence of sea conditions when the rig was on the bottom. These early semisubmersibles sometimes operated in shallow water and sat on the seafloor. However, when buoyant, this type of column reduced the rig’s dynamic stability.

The 135 B tragedy resulted in stricter stability requirements by the American Bureau of Shipping (1968 ABS Rules for Building and Classing Offshore Mobile Drilling Units.)

JL informs me that the Alexander Kielland was a symmetrical pentagon design. Unfortunately, with this design, the failure of a major diagonal brace results in the complete loss of structural integrity.

Per BSEE’s recent announcement, Federal funds will be used to plug wells in the Matagorda Island (MI) area of the Gulf of Mexico (see map below). Based on a BSEE presentation and BSEE borehole data, these wells were drilled by Matagorda Island Gas Operations LLC, a company that filed for bankruptcy in 2014.

Prior to the bankruptcy filing, Matagorda Island Gas was cited for 112 violations on 108 inspections. This INC/inspection rate is approximately double the Gulf of Mexico (all operators) rate in a typical year (0.52 in 2022), and is 4 to 25 times higher than the rate for the 2022 Honor Roll companies.

In a draft rule published on June 29, 2023, BOEM proposes to discontinue using a company’s record of compliance in determining the need for supplemental financial assurance for decommissioning. BOEM’s full explanation for this surprising change is pasted at the end of this post.

Opposing view:

BOEM should be more attentive, not less, to safety performance and compliance data. If they were, taxpayers would have been better protected from the risks associated with the lease acquisitions by Fieldwood, Cox, Black Elk, Signal Hill, and others, and their subsequent bankruptcies.

Safe operations, as reflected in compliance and performance data, are critical to a company’s financial success.

BOEM wrongly infers that Incidents of Noncompliance (INCs) are solely dependent on the number and complexity of facilities. Decades of normalized compliance data have told us that there are marked differences among operators in terms of compliance and safety performance. Companies at the bottom of the performance table don’t usually survive.

Accidents are not mere matters of chance; management and culture matter.

Honor Roll companies, large and small, have superior compliance records, and in 2022 these companies had 50-90% fewer INCs/facility-inspection than the Gulf of Mexico average.

Does BOEM expect noncompliance leaders to be concerned about decommissioning obligations? The record shows that they are not.

Cox’s 2023 bankruptcy was predictable given their past safety performance. In 2022, Cox was a violations leader by any measure, and was responsible for 9 of the 30 safety incidents that were significant enough to require investigation by BSEE.

Fieldwood’s terrible 2021 safety performance has been discussed, and there was ample evidence of performance problems prior to their bankruptcy declaration in 2018. In 2016 and 2017 Fieldwood was, by far, the GoM violations leader with 818 INCs, 401 of which required a facility or component shut-in.

Ironically (or maybe not), the only other company that was even in the same noncompliance ballpark as Fieldwood in 2016 and 2017 was future Cox affiliate Energy XXI GOM. Energy XXI earned 465 INCs (240 shut-ins) during that 2 year period. Did BOEM object to or otherwise comment on the 2018 Cox-Energy XXI merger?

Black Elk Energy was new in 2007 and quickly became a violations leader. Between 2010 and 2012, BSEE cited Black Elk 415 times. 218 of these violations were serious enough to require facility or component shut-ins. On November 16, 2012, explosions at Black Elk’s West Delta 32 platform killed 3 workers, and 2 others suffered severe burns. Criminal charges and a complex bankruptcy followed. BSEE records show 1107 INCs during the company’s short history, 464 of which required facility or component shut-ins.

The rapid growth of Fieldwood, Cox, and Black Elk was in part facilitated by lax lease assignment and financial assurance policies. Operating companies should have to demonstrate that they can operate safety and comply with the regulations before they are approved to acquire more properties.

The Signal Hill sagawas documented nearly 2 years ago, and none of the questions raised in that post have been answered. Violations data and inspector feedback predicted the Signal Hill/POOI failure. Nonetheless, and despite the objections of regional staff, Signal Hill was allowed to tap into its decommissioning account to cover operating expenses. Responsibility for decommissioning Platforms Hogan and Houchin is still uncertain.

Given that BSEE, not BOEM, is responsible for safety and compliance, I sincerely hope that regulatory fragmentationwas not a factor contributing to BOEM’s decision to discontinue the use of compliance data in determining financial assurance needs.

BOEM’s explanation for the proposal to eliminate the record of compliance criterion:

BOEM also proposes to eliminate the existing “record of compliance” criterion found in the current version of § 556.901(d)(1)(v). BOEM has determined that the number of INCs a company receives correlates with the number of OCS properties it owns, not its financial stability, and therefore, BOEM has concluded that it is not an accurate predictor of its financial health. BOEM reviewed BSEE’s Incidents of Non-Compliance (INCs) records and its Increased Oversight List, which represent BSEE’s cumulative records of violations of performance standards on the part of OCS operators and lessees and determined that the number of incidents of non-compliance typically increases with the size and complexity of the operator’s or lessee’s operations, including the ratio of incidents to number of components. Because larger companies (regardless of credit score) tend to have more properties and components and therefore more INCs, BOEM determined that record of compliance criterion does not accurately predict financial default. BOEM’s review of this information confirmed the feedback BOEM received in response to the 2016 NTL, namely that companies with a large number of properties and facilities tended to receive a large number of INCs and had more individual properties on the Increased Oversight List. BOEM specifically requests comments regarding the use of fines and violations as a criterion in the determination of a company’s ability to fulfill decommissioning obligations, and any data or analysis addressing any correlation between the number of violations and the risk of financial default. BOEM also requests comments on whether the elimination of the INC’s criteria would create a disincentive to comply with regulations. BOEM also requests comment on whether or not the cost of decommissioning is likely to increase based on the type, quantity, and magnitude of previous violations.

On a related note, BOEM/BSEE should consider a followup to the John Shultz thesis which found that INCs are a very good predictor of accidents and spills.

Desde el campo Quesqui en #Huimanguillo, Tabasco, el Director General de #PEMEX, Ing. @OctavioRomero_O, reporta al día de hoy sobre el incendio de ayer en Cantarell.

Los compañeros lesionados se encuentran estables y continúa la búsqueda de la persona desaparecida.

BOEM has rather surprisingly proposed to eliminate consideration of a company’s compliance record in determining the need for supplemental financial assurance.An opposing view will be posted tomorrow.

If a lease has proved reserves with a value of at least three times that of the estimated decommissioning cost, no supplemental financial assurance would be required. Comparing two imprecise and variable estimates is neither a simple nor reliable method for determining the need for supplemental financial assurance. BOEM should look at the history of the Carpenteria field (Santa Barbara Channel) and the reserve estimates that were provided to discount decommissioning risks. More on this at a later date.

Transferor liability applies only to those obligations existing at the time of transfer; new facilities, or additions to existing facilities, that were not in existence at the time of any lease transfer are not obligations of a predecessor company and are considered obligations of the party that built such new facilities and its co- and successor lessees. This is a good policy, but is difficult to implement. Some of the complexities may need to be addressed.More later.

The “reverse chronological order” provision was withdrawn in April, so there is no defined process for issuing decommissioning orders to predecessor lessees. Is it good policy to first issue such orders to companies who may have owned leases decades ago, in some cases prior to the establishment of transferor liability in the 1997 MMS “bonding rule?”

The proposed rule would clarify that BOEM will not approve the transfer of a lease interest until the transferee complies with all applicable regulations and orders, including the financial assurance requirements. BOEM needs to be firmly enforce this policy. See tomorrow’s post.

The proposed rule would not allow BOEM to rely upon the financial strength of predecessor lessees when determining whether, or how much, supplemental financial assurance should be provided. This is a good provision.

BOEM proposes to use the P70 probabilistic value to set the amount of any required supplemental financial assurance. These estimates do not seem sufficiently conservative to protect other parties and the public in the event of default. This is particularly true after storm damage which can increase plugging costs more than tenfold.

The probabilistic cost estimates were updated in 2020 and are based on data submitted subsequent to 2016 and 2017 NTLs. How often will these estimates be updated?

The final rule should specify that funds may not be withdrawn from decommissioning accounts for operational purposes, and that BOEM approval is required for such withdrawals.

The Piper Alpha fire was the worst disaster in the history of offshore oil and gas operations and sent shock waves around the world. Eight months later another interactive pipeline-platform fire killed 7 workers at the South Pass 60 “B” facility in the Gulf of Mexico. A US Minerals Management Service task group reviewed the investigation reports for both fires and recommended regulatory changes with regard to:

the identification and notification procedures for out-of-service safety devices and systems,

location and protection of pipeline risers,

diesel and helicopter fuel storage areas and tanks,

Lord Cullen’s comprehensive inquiry into the Piper Alpha tragedy challenged traditional thinking about regulation and how safety objectives could best be achieved, and was perhaps the most important report in the history of offshore oil and gas operations. Per Cullen:

“Many current safety regulations are unduly restrictive because they impose solutions rather than objectives. They also are out of date in relation to technological advances. Guidance notes lend themselves to interpretations that discourage alternatives.There is a danger that compliance takes precedence over wider safety considerations and that sound innovations are discouraged.“

Cullen advocated management systems that describe the safety objectives, the system by which those objectives were to be achieved, the performance standards to be met, and the means by which adherence to those standards was to be monitored. He called for safety cases that describe major hazards on an installation and provide appropriate safety measures. Per Cullen, each operator should be required in the safety case to demonstrate that the safety management systems of the company and the installation are adequate to assure that design and operation of the platform and its equipment are safe.

Because space requirements and intermittency limit the ultimate potential of other renewable energy super-sources, ultradeep geothermal may be the most exciting energy alternative on the horizon. However, ultradeep geothermal’s enormous potential can only be achieved if we can reliably drill deep beneath the surface and tap into superheated rock. As Quaise Energy’s Carlos Araque, formerly a Schlumberger engineer, has noted: “A lot of the challenges are the same as for oil and gas.”

This short video provides a good summary of the drilling technology that is under development.

In 1979 Gulf of Mexico oil production had declined to 263 million barrels and many believed that further declines were inevitable. 40 years later, a record 693 million barrels were produced.

Onshore, lateral drilling and hydraulic fracturing capabilities are continuing. As a result, Exxon and others are predicting projecting higher recovery factors in the Permian Basin. Per Exxon CEO Darren Woods: “We are beginning to see the signs of some very promising new technologies that will significantly improve recovery.”

Opportunity + Ingenuity ➡ Energy Independence + Prosperity