14 of the high bids at Gulf of Mexico Lease Sale 259 were rejected. Did those tracts receive bids at sale 261? What was the net gain or loss of revenue? See the summary bullets and table below

6 of the 14 tracts received no bids whatsoever

5 of the 14 tracts received higher bids that were accepted.

2 tracts received substantially higher bids that were again rejected

1 tract received a lower bid that was accepted

net bonus revenue gain to the govt from the bid rejections (pending re-offering at future sales): $1,032,877

net bonus revenue gain = 0.27% of the total high bids at sale 261

net loss in future rental and royalty payments: ????

For a net bonus revenue gain to date of only 1/4 of one per cent, 8 of the 14 sale 259 tracts with rejected high bids remain closed to exploration. The timing of any future sales is very much in doubt given the minimalist 5 year leasing plan and the associated legal challenges.

Current bid evaluation practices only make sense if regular lease sales are held on a predictable schedule, as has historically been the case.

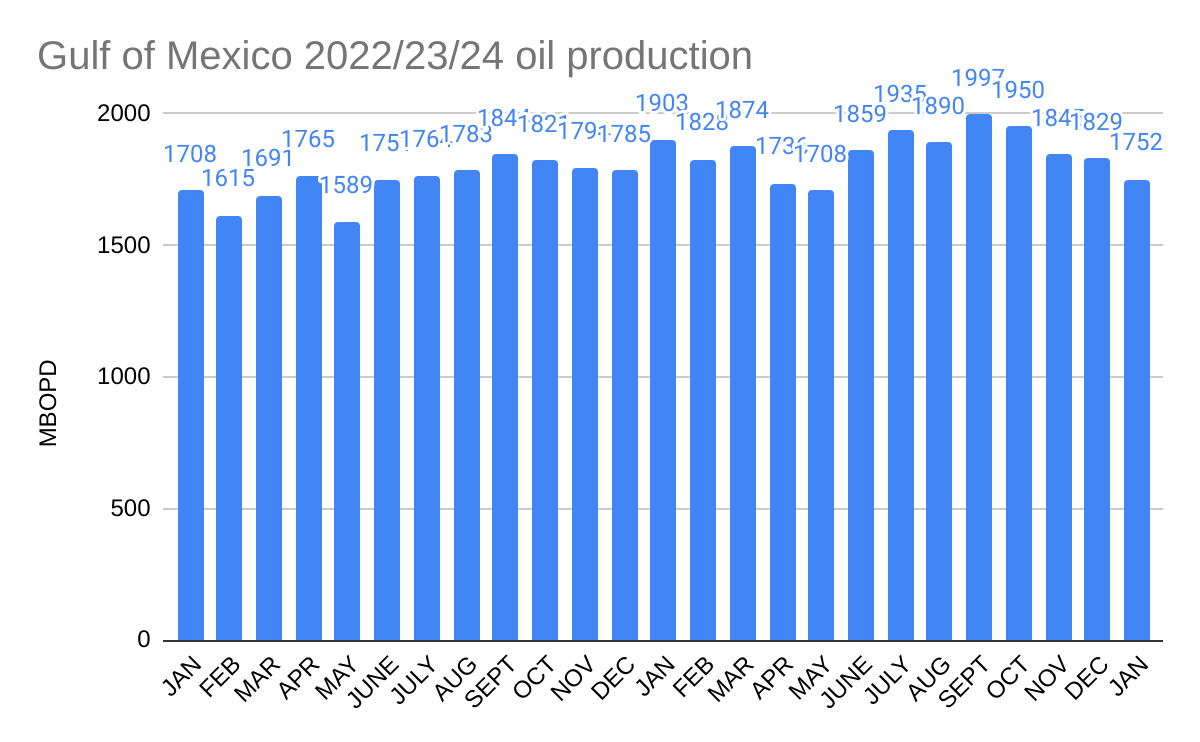

Average GoM oil production from Nov. to Jan. was more than 130,000 BOPD below the July to Oct. average. Production in Jan. 2024 was 245,000 BOPD lower than Sept. 2023 production. (See the table and chart below.)

The production shut-ins associated with the mysterious November sheen in the Main Pass area were no doubt a contributing factor to the decline, but the magnitude and duration of those shut-ins has not been disclosed. The source of the sheen has apparently still not been determined, nor has any information been provided on the status of the Federal investigation. The absence of transparency is disappointing.

… to be able to speak openly and candidly about issues that have been an important part of my professional life for more than a half century.

Whether you represent Big Oil, Big Gas, Big Wind, Big Green, Big Stick (regulators 😀), Big Swamp (Washington DC friends 😉), or none of the above, thank you for visiting this modest, independent blog.

Regardless of your faith, nationality, political views, or thoughts about world events and offshore energy, I hope you have the opportunity to spend time with friends and family this weekend.

I’m posting Sunday’s 60 Minutes segment that focused on deep sea mining and the failure of the US to ratify the UN Convention on the Law of the Sea (UNCLOS). Supplementary comments:

Most Federal employees involved with ocean energy policy, past and present, have supported US government ratification of UNCLOS.

The offshore industry has long supported UNCLOS. Industry trade associations, including API, IADC, and NOIA, are on the record as favoring ratification.

While concerns about UN management of deep sea mining access are understandable, some coordinated administrative structure is needed.

The Metals Company and other companies pursuing deep sea mining opportunities clearly disagree with the assertion that ocean floor mineral harvesting is not economically viable.

Remembering the 123 offshore workers who lost their lives on this dayin 1980 in one of the offshore industry’s great tragedies 🙏

See the excellent interview with Magne Ognedal that describes the evolution of Norway’s highly regarded offshore regulatory regime following the Alexander Kielland tragedy.

A new report ranks eight key energy industry sectors based on their ability to meet the growing demand for affordable, reliable, and clean electric power generation.

As governments around the nation attempt to impose a transition from traditional energy resources to energy sources open referred to as renewables, natural gas is the energy source that is best suited to integrate with the intermittency inherent in the use of wind and solar. Gas provides a reliable, affordable, and increasingly clean source of energy in both traditional and “carbon-constrained” applications.

Gas faces headwinds in the form of increasingly extreme net zero energy policies that will constrict supplies if implemented as proposed. Gas could also improve overall reliability if onsite storage was prioritized to help avoid supply disruptions that can occur in just-in-time pipeline deliveries during periods of extreme weather and demand.

Canadian and US approvals were granted and CNOOC acquired Nexen (Canada) in 2013.

Nexen’s Guyana interest was not mentioned in the press announcement, and appears to have been a rather minor consideration in the acquisition.

So, an apparent afterthought in CNOOC’s takeover of Nexen has (1) proven to be extremely profitable, (2) given the company and the Chinese government leverage in the Exxon-Chevron supermajor dispute, and (3) opened the door for CNOOC to increase their interest in the massive Stabroek field.

Swimming upstream against the Federal policy current, Gulf of Mexico drilling is demonstrating impressive forward progress. Baker Hughes reports 22 active GoM rigs on 3/15/2024, an increase of 3 from the previous week.

Glancing at the charts, this appears to be the highest GoM rig count since Nov. 2019, and is double the recent low of 11 in 2022.

It’s unclear whether Baker Hughes is including the CCS drilling operation offshore Texas. If so, the actual oil and gas rig count is 21 rather than 22.

Baker Hughes also reports 1 active rig offshore California (decommissioning?) and 1 active rig offshore Alaska (Endicott or Northstar?)

Per Baker Hughes, no rigs are currently active offshore Canada.

In 2023, LLOG was the 6th biggest oil producer in the Gulf of Mexico trailing only Shell, bp, Anadarko, Chevron, and Murphy. As a natural gas producer, LLOG ranked fifth ahead of major GoM operators like Chevron and Hess.

Boelte built LLOG into a company with a strong commitment to safety and environmental protection. In that regard, the company achieved BOE Honor Roll status in 2023 and 2022.