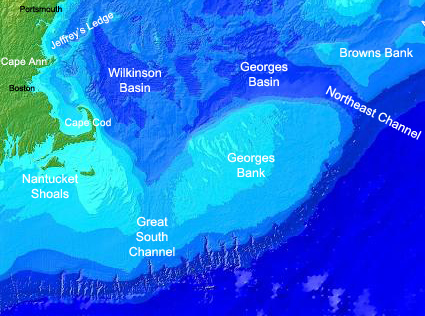

44 years ago today, drilling began on the first two exploratory wells on Georges Bank, the large seafloor feature that separates the Gulf of Maine from the Atlantic Ocean. The above Cape Cod Times headline attests to the drama that was unfolding 155 miles southeast of Nantucket.

After years of debate, oil embargoes, gas lines, and the threat of future supply disruptions tipped the political balance in favor of offshore leasing, and OCS Sale No. 42 (North Atlantic) was held one week before Christmas in 1979. Remarkably, only 19 months elapsed between the lease sale and the initiation of drilling.

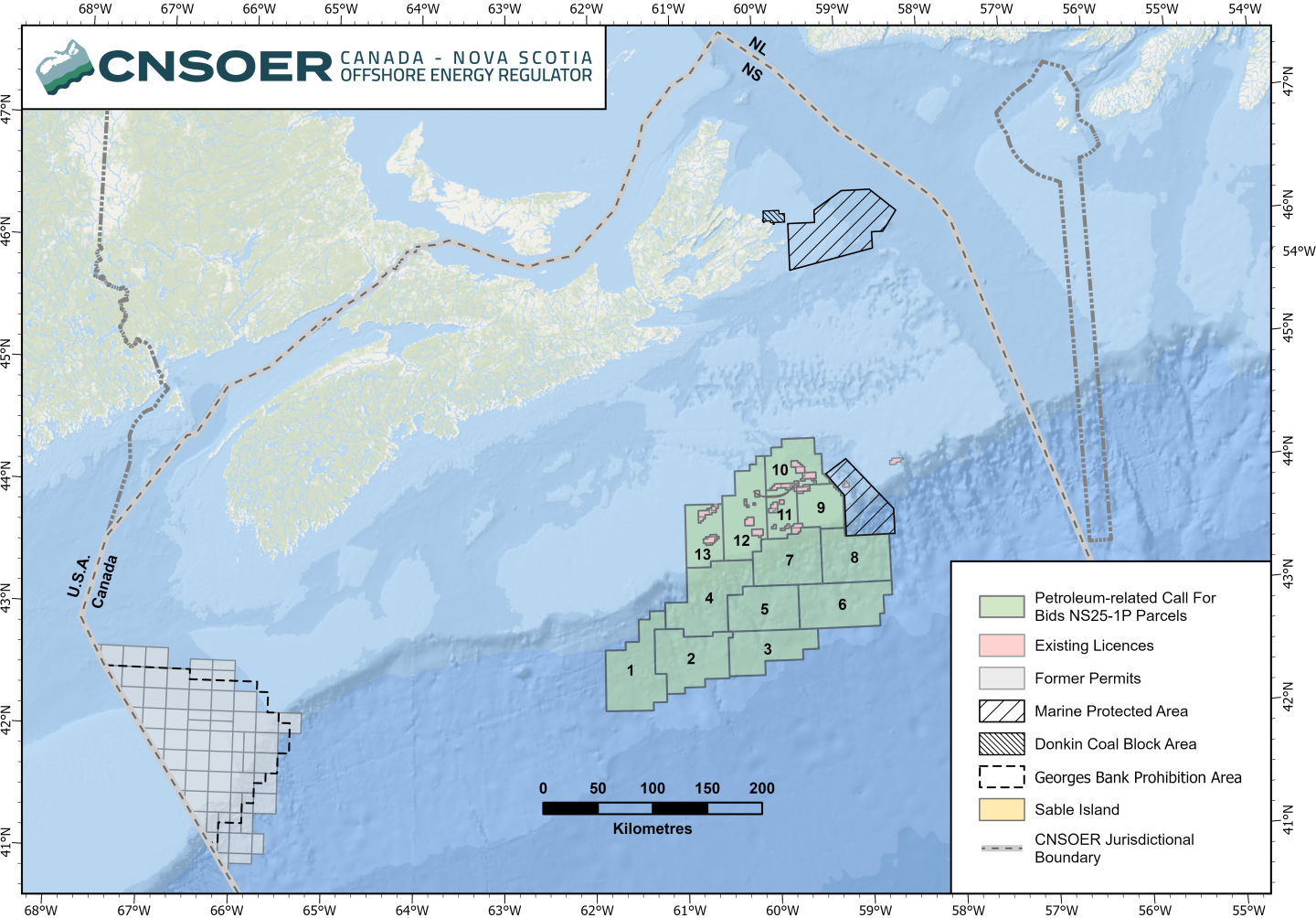

Scotian Shelf gas production ended in 2018, but Nova Scotia Energy Minister Trevor Boudreau (Acadian with many relatives in Louisiana?😉) says he is encouraged by preliminary expressions of industry interest in new licenses. The Provincial/Federal authority has issued a call for bids:

“The Canada-Nova Scotia Offshore Energy Regulator (CNSOER) has issued a petroleum-related Call for Bids NS25-1P, which includes 13 nominated parcels. Bids must be received by April 28, 2026, before 4:00 p.m. Atlantic Time. Successful bidder(s) may be awarded Exploration Licences (ELs), subject to the federal and provincial Ministerial review and approval process set out in legislation.”

“The petroleum-related Call for Bids NS25-1P nominated parcels are located on the central Scotian Shelf and Slope. Parcels 1 to 8 are located in deepwater on the Scotian Slope, in water depths from 200 to 4,300 metres. Parcels 9 to 13 are located on the Scotian Shelf, in water depths less than 200 metres, in the region where all historic gas, and to a lesser extent, oil production, has taken place. The shelf parcels are located near the Sable Island National Park Reserve and west of the Gully Marine Protected Area. No petroleum-related activity can take place within one nautical mile (or 1.85 kilometres) of the Sable Island National Park Reserve.“

As posted in January, most analysts predicted that Chevron and Hess would prevail. Now that the arbitration panel has ruled, Chevron’s acquisition of Hess can be completed.

The position of Exxon and its partner, Chinese govt owned CNOOC, never made much sense given that Chevron was not buying the Stabroek share, they were buying the company that holds that share.

Not much attention has been paid to the importance of Chevron’s acquisition of Hess’s Gulf of America assets. The combined company will be the 3rd largest GoM oil producer (behind Shell and bp) and the second largest gas producer (behind only Shell). Hess acquired 20 GoA leases in Sale 261, ranking first in total high bids ($88 million) among all participants.

Drilling Safety Leaders Pilot Programto be proposed.

Comments on the Dept. of the Interior’s regulatory reform initiative are due by July 21.

DOI’s “Deregulation Suggestions” form implies that their review may be limited in scope. The form focuses solely on rescinding regulations. True regulatory reform requires a broader assessment of regulatory methods and strategies.

Offshore safety regulations address known or perceived operational risks. Deleting individual provisions without considering the effect on the regulatory objective could introduce new risks without reducing the burden on operators and regulators.

More meaningful regulatory reform, and the associated improvements in operator and regulator efficiency, can be achieved by addressing regulatory fragmentation and providing regulatory incentives for companies with outstanding safety and environmental performance records.

My comments to DOI will address fragmentation and the challenges associated with updating regulations and standards. A Drilling Safety Leaders Pilot Program will be proposed. This pilot program would offer a more flexible regulatory regime for operators with outstanding safety records.

The regulatory system can constrain leading operators and delay innovation. The top performers should be encouraged to stay ahead of the technology and management curves. Most of the requirements that were added after Macondo had been adopted by leading operators well before the blowout.

Per the Independent, the alleged conflict of interest that prevented County Supervisor Joan Hartmann from voting on Sable oil matters has been reevaluated. She is now legally permitted full voting rights.

With Hartmann recusing herself, the supervisors had been deadlocked in a perpetual 2-2 tie when voting on issues concerning Sable. Supervisor Hartmann’s participation is not good for Sable given her public comments in opposition to the Santa Ynez Unit restart.

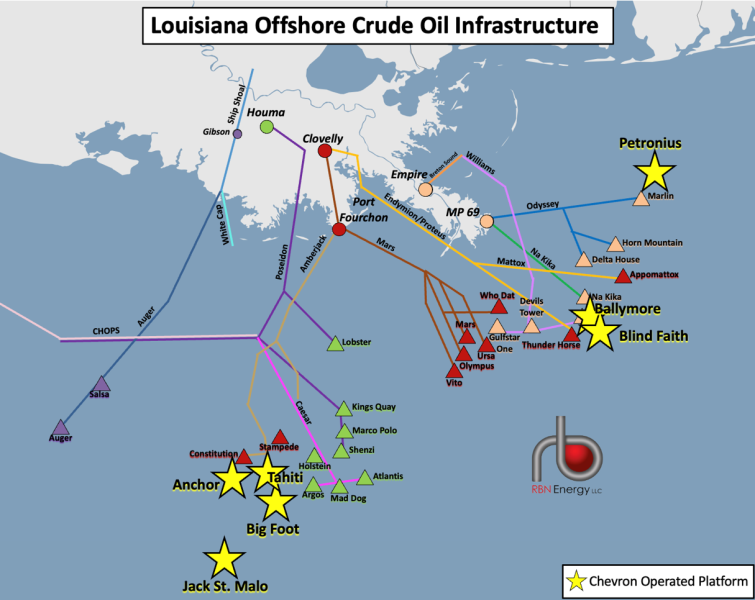

Reuters and others report that zinc from a new Chevron well has contaminated oil production destined for an Exxon refinery via Shell’s Mars Pipeline System. Because contaminated crude may cause maintenance issues and reduces the quality of refined products, Exxon will not accept crude from the Mars system until the zinc issue has been resolved.

The Mars system delivers about 575,000 bopd raising concerns about supplies to Gulf Coast refineries. But fear not, DOE authorized the delivery of up to 1 million barrels of oil from the Strategic Petroleum Reserve to the Exxon’s Baton Rouge refinery.

(Ironically, yesterday’s post pointed to the importance of the SPR and questioned the decision to drastically reduce crude oil purchases. This zinc incident is likely to be minor, and Exxon will repay the SPR in kind. However, more serious regional, domestic, and international events could call for much greater SPR withdrawals.)

The above map shows Chevron platforms that connect with the Mars system at Port Fourchon.

Speculation/commentary:

The well/platform responsible for the zinc contamination has not been identified. Given that production is ramping up at Chevron’s Anchor facility, a new well on that platform may be the source of the zinc. Other Chevron platforms that connect to the Mars system are indicated in the diagram above.

Given that zinc in crude oil is rare, a well completion fluid containing zinc bromide may be the culprit.

Note the integration of offshore production streams, and the involvement of 3 industry super-majors. These companies are highly competitive, as evidenced by the Chevron-Exxon Stabroek dispute, but are also cooperative in producing, transporting, and refining oil and gas. However, they and other majors are restricted (rather illogically) from bidding jointly for leases.

Tariffs and their uncertainty “will certainly decrease expected investment activity in the energy sector,” says the new report. More than $50 billion of offshore investment this year has been deferred “with operators looking to wait out current market uncertainty before making significant final investment decisions,” Rystad notes.

Rystad estimates that tariffs will increase costs for offshore oil and gas projects by 8% year-over-year and 12% for onshore. “Most steel and raw material exposed cost categories are feeling the majority of the impact from tariffs and thus will take the biggest hit.”

Comment: At a glance, the number of 2025 well starts in the GOA appears to be down (more on this at a later date). While there are many factors affecting drilling decisions, lower oil prices and higher costs associated with tariffs are not compatible with a “drill baby drill” philosophy.

We preferred the House version, but the Senate Parliamentarian killed the provisions that reduced the risk of litigation and processing delays.

Whether justified or not, the royalty rate is now capped at 1/6 and a 10-year deepwater lease term is locked in.

The favorable terms and assurance of regular GOA lease sales put the ball squarely in industry’s court. We are looking for a good showing at Sale 262, including some new bidders and the return of some prominent companies.

“Leases awarded through Lease Sale 262 will be for oil and gas exploration and development only.” (News Release)

“Leases issued as a result of GOA Lease Sale 262 are expressly limited to oil and gas exploration and development.” (p. 16 of the Sale Notice)

Comment: Why would BOEM stipulate, for the first time ever, that an Oil and Gas Lease Sale is only for oil and gas exploration and development? Perhaps because, at the last 3 sales, 2 companies wrongfully acquired oil and leases for carbon disposal purposes. Those leases will likely expire at the end of their primary term, and the lessees will have nothing to show for their investment.

Other items of interest:

“Congress may enact legislation through reconciliation efforts sometime after publication of this Proposed NOS“

Comment: The Offshore Oil and Gas Leasing provisions in the “Big Beautiful Bill” make OCS leases more attractive in that they minimize sale uncertainty and return royalty rates to pre-IRA levels.

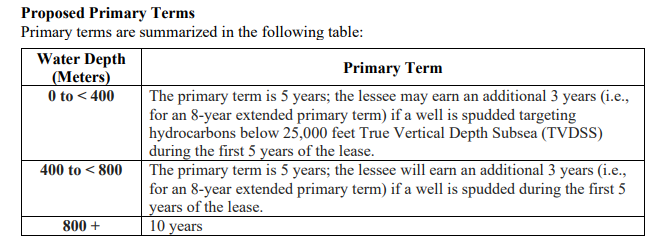

Proposed Primary Terms

Comment: Time for an update. The drilling requirements for a primary term extension should be the same for leases in 0-400 m as for those in 400-800 m. The requirement for an ultra-deep subsurface well is selectively punitive to shelf operations. These operations, although typically less lucrative, are important to the Gulf’s infrastructure.

Restricted Joint Bidders On April 29, 2025, BOEM published the most recent List of Restricted Joint Bidders in the Federal Register (90 FR 17832). Potential bidders are advised to refer to the Federal Register prior to bidding for the most current list at the time of the lease sale. Please refer to the joint bidding provisions at 30 CFR 556.511-556.515

The differences between the House and Senate versions of the Big Beautiful Bill are summarized in the table below. (See the previous post on the House version.)

The Senate bill includes royalty and lease terms that favor deepwater lessees, but excludes the provisions in the House bill that streamline the leasing process and minimize litigation risks. At least some of those House provisions were rejected by the Senate Parliamentarian.

The House will vote on the version that passes the Senate. So the Senate version is more likely to be enacted.

House

Senate

Comment

royalty: 12.5% to 18.75%

royalty: 12.5% to 16 2/3%

Lowering the royalty cap to 1/6 (16 2/3%) unduly limits the Secretary’s discretion and may reduce revenues without significantly increasing production.

2 GOA sales/yr over next 15 yrs.

same as House

Would have liked the opportunity for consideration of very limited Atlantic leasing or stratigraphic test drilling, but that is not politically feasible at this time.

use Sale 254 form and stips 4-10, may update stips 1-3

sale 254 lease form and stips 4-9, may update stips 1-3 and 10

The minor difference favors the Senate version. Stip 10 pertains to restrictions due to Rights-of-Use and Easement for Floating Production Facilities, and needs to be updated with each sale

mandates 10 year lease term for water depths >800 m

Although a 10 year term for deepwater leases is generally prudent, the Secretary should be able to choose a shorter term if concerns about timely exploration and diligent development arise (more likely given the increase in leases that could be issued as a result of the 2 sales/yr mandate).

requires approval of subsurface commingling unless there is “conclusive evidence” of safety or ultimate recovery issues

Although BSEE’s policy change on downhole commingling was warranted, the legislative change removes essentially all discretion by mandating approval unless there is “conclusive evidence” to the contrary. Conclusive evidence is dependent on production history, at which point it may be too late.

Adherence with the Biological Opinion shall satisfy the Secretary’s obligations under the Endangered Species Act of 1973 and the Marine Mammal Protection Act of 1972

This provision reduces govt/lessee litigation risks

Previous EIS’s for the Gulf of Mexico shall satisfy the Secretary’s NEPA obligation.

Rejected by the Senate Parliamentarian.

Consistency determinations prepared by BOEM for Lease Sale 261 for the States of Texas, Louisiana, Mississippi, Alabama, and Florida will satisfy the Secretary’s CZMA obligations.

The States or Parliamentarian may not have been comfortable with this provision which simplifies plan approval processes.

The Secretary may waive any requirement under the Outer Continental Shelf Lands Act that the Secretary determines would delay issuance of a lease.

Rejected by the Senate Parliamentarian?

A lease must be issued to the highest responsible qualified bidder not later than 90 days after the sale date.

Rejected by the Senate Parliamentarian.

A Governor may nominate for leasing under a lease sale held under this section an area of the OCS that is adjacent to the waters of the State

Never understood the need for this provision.

G&G surveys must be approved within 30 days after a complete application is received.

Not feasible in some cases given endangered species concerns.

A lease awarded under Lease Sale 259 or Lease Sale 261 shall not be set aside, vacated, enjoined, suspended, or cancelled except in accordance with section 5 the Outer Continental Shelf Lands Act (43 U.S.C. 1334). Also, new terms or conditions may not be added to these leases.

Reduces litigation risks.

Any action to approve, require modification of, or disapprove any exploration plan, development and production plan, bidding procedure, lease sale, lease issuance, or permit or authorization related to oil and gas exploration, development, or production, or any inaction resulting in the failure to hold a lease sale shall be subject to judicial review only in a United States court of appeals for a circuit in which an affected State is located.

This provision significantly reduces litigation risks. Rejected by Parliamentarian?

6+ Cook Inlet sales over next 10 yrs.

6+ Cook Inlet sales over the next 7 years

90% of Cook Inlet revenues to the State of Alaska.

70% of Cook Inlet revenues to the State of Alaska.

The percentages are high, but the revenues are likely to be low.