Diamond Ocean Blackhawk is drilling MC 40 well for Anadarko

Following up on last year’s deepwater diligence post, 4 recent deepwater exploratory wells (table below) were spudded within 4.5 years of the effective date of their leases.

Particularly noteworthy is Anadarko’s well on newly acquired Mississippi Canyon Block 40, which was spudded only 18 months after the lease was acquired. Everything has to be in place for such an outcome: corporate priority, data gathering and analysis, well plan, permitting, and rig contract/availability.

The well was apparently a high priority not just for Anadarko, but also for Chevron and Murphy. MC 40 was acquired by Chevron (bidding alone) at Sale 257 for $4,409,990, the third highest bid at the sale. Murphy had submitted a losing bid of $3 million, but was assigned a 33% share of the lease by Chevron on 12/15/2023. One month earlier, Anadarko had been assigned a 33% interest and became lease operator.

Interestingly, BOEM’s Mean Range of Value (MROV) estimate for the block was only $576,000, so the three companies are seeing something that BOEM doesn’t. We’ll see how this plays out.

According to rig tracker data the Ocean Blackhawk is still on location at MC 40. Per BSEE permitting data, the well was approved to be bypassed in mid-May.

Decommissioning financial assurance issues are complex!

This blog has raised significant concerns about BOEM’s decommissioning financial assurance rule, and will continue to comment on decommissioning policy. That said, decommissioning issues are complex and have challenged industry and government in the US and internationally for decades. Add well plugging practices, corrosion, storm risks, reefing vs. total removal, alternative uses for old platforms, and pipeline and seafloor equipment abandonment to the myriad of financial issues and you get a sense of the breadth and complexity of decommissioning issues.

Decommissioning is unique in that the issues divide sectors of the offshore industry that are typically aligned (majors vs. smaller producers). The environmental community is also divided with the reefing and fishing advocates opposing those who insist on complete removal.

Given these divisions, and decommissioning’s operational, environmental, and political complexities, highly partisan assertions are common. A recent article about the financial assurance rule includes a number of such assertions, and provides a framework for discussing some of the more prominent issues. Excerpts from the article and my comments follow.

“This costly rule became final on April 15, 2024, but in the 10 months since its initial proposal, BOEM did nothing to alleviate concerns for smaller companies that comprise of 76 percent of oil and gas operators in the Gulf.“

Comments:

While I concur that shelf operations and the independent companies that conduct them are important, 94% of OCS oil production and 80% of the gas (2023 data) were from deepwater facilities (>1000′ WD) which are largely the domain of the majors (although the participation of independents in the deepwater sector is increasing).

In 2023, four majors – Shell, bp, Oxy (Anadarko) and Chevron – accounted for 2/3 of the Gulf’s total oil production.

1467 of the remaining 1527 GoM platforms are in <1000 feet of water and are almost exclusively operated by small producers. So 96% of the platforms are producing only 6% of the oil and 20% of the gas.

This dichotomy presents a major challenge for BOEM which must protect the public from decommissioning liabilities without unfairly penalizing small producers.

Having worked for respected political appointees from both parties, my experience has been that the smaller producers (somewhat surprisingly) have more political influence than the majors. For this reason, along with the general lack of attention to financial assurance issues in the early years of the offshore program, the standard bond requirement was ridiculously low for much of the program’s history, and supplemental financial assurance assessments were typically inadequate (and still are which is why the new rule was promulgated).

Attention to decommissioning issues grew exponentially in the early 1990s. Prior to that time, platform removal, like well plugging, was classified as “abandonment,” a term that was considered too harsh when bankruptcy issues and the Brent Spar controversy in the North Sea attracted worldwide attention.

“Records obtained via the Freedom of Information Act show private meetings between Interior officials and representatives of the major oil companies as they cooperated on this rule.“

Comments:

The linked FOIA records are not at all problematic. They pertain to meetings prior to the publication of the draft rule, which are appropriate and desirable.

Some of these meetings were in response to BOEM’s request for input regarding their review of the OCS oil and gas program. Such meetings are particularly helpful when a new administration is trying to assess the direction of the program.

Indeed 42 of the 71 pages in the FOIA were official industry comments in response to the BOEM request.

Per the Regulations.gov docket on the financial assurance rule, BOEM also met with stakeholders after the proposed rule was published. Those meetings are allowed as long as the regulator simply receives input and does not signal decisions regarding the content of the final rule.

The docket shows that BOEM had 8 listening sessions with advocates for independent producers. These included 2 sessions with the Gulf Energy Alliance and 6 sessions with individual independent producers.

BOEM also had 2 listening sessions with Oceana, a prominent environmental organization, and multiple sessions with tribal organizations.

The only sessions with representatives from major producers were a single session with API and a single session with Shell, the Gulf’s largest producer.

These meetings (after the proposed rule was published) are noted in the docket as required.

I am concerned that many listening session documents (from all sides of the decommissioning financial assurance issue) were removed from the docket at the direction of OIRA/OMB, purportedly because they included privileged information. This is rather troubling given the number of deletions and the complete absence of information about those meetings. What types of privileged information were these organizations providing and why is there no information whatsoever on these meetings? At a minimum, a list of attendees and general summary for each meeting should have been posted, as was our practice in the past.

“Big Oil must think it won’t miss the small competitors the rule will drive from the market.“

Comments:

There is important synergy between the major producers and independents, and no reason for driving smaller companies from the market.

The independents are critical to sustaining the shelf infrastructure and the associated service companies, which helps to facilitate deepwater development. Majors also benefit from partnering with independents on lease acquisitions, development projects, and lease assignments.

Financial assurance for decommissioning of transferred assets is the one area of significant conflict, particularly when there have been multiple ownership changes since the facilities were initially transferred.

“Historically, joint and several liability protected these small businesses from the financial demands of surety bonds.”

Comments:

Surety bonds, or other forms of financial assurance, have always been required. As previously noted, the amounts were often inadequate.

Joint and several liability was not established in the regulations until May 22,1997. Whether companies are liable for facilities transferred prior to that date has yet to be considered in court.

1130 of the 1527 remaining GoM platforms were installed prior to May 22,1997. Many of these platforms were no doubt transferred prior to that date, which means the liability of the initial owner is uncertain.

Predecessor liability does not apply to new wells and platforms constructed by the current lessees.

Joint and several liability was never intended to relieve current lessees from their financial assurance responsibility, which is why assignors were required to provide such assurance. BOEM is correct in strengthening their enforcement of this requirement.

“The new rule is largely silent on joint and several liability, causing some uncertainty.”

Comment: The joint and several liability provision remains in place at 30 CFR 250.1701(a) BOEM has added language to part 556.704, to clarify, correctly in my opinion, that they may withhold approval of any transfer or assignment of any lease interest if the financial assurance requirements have not been satisfied.

Companies may not be able to acquire the needed financial assurances because the market likely will not even exist.

Comment: The history of small producer failures is no doubt a concern to financial institutions. BOEM offers multiple financial assurance options, some of which have been questioned on this blog. If a company can’t qualify, it’s not the responsibility of the public to assume their decommissioning risks.

What makes matters worse is that all this cost covers a risk that is effectively a rounding error historically and in the context of the royalties flowing from the offshore oil and gas industry. According to BOEM, taxpayers have borne decommissioning liability totaling $58 million – from a single company that lacked predecessor owners of the platform to call on to cover unfunded cleanup costs.

Those who seek to minimize the Federal government’s risk exposure should consider the findings in the 2024 GAO report. Per that report, “BOEM held about $3.5 billion in supplemental bonds to cover between $40 billion and $70 billion in total estimated decommissioning costs as of June 2023.”

When will we find out who will be paying the hundreds of millions needed to decommission long-idled Platforms Hogan and Houchin in the Santa Barbara Channel?

Decommissioning financial assurance is a responsibility of lessees, not the taxpayer.

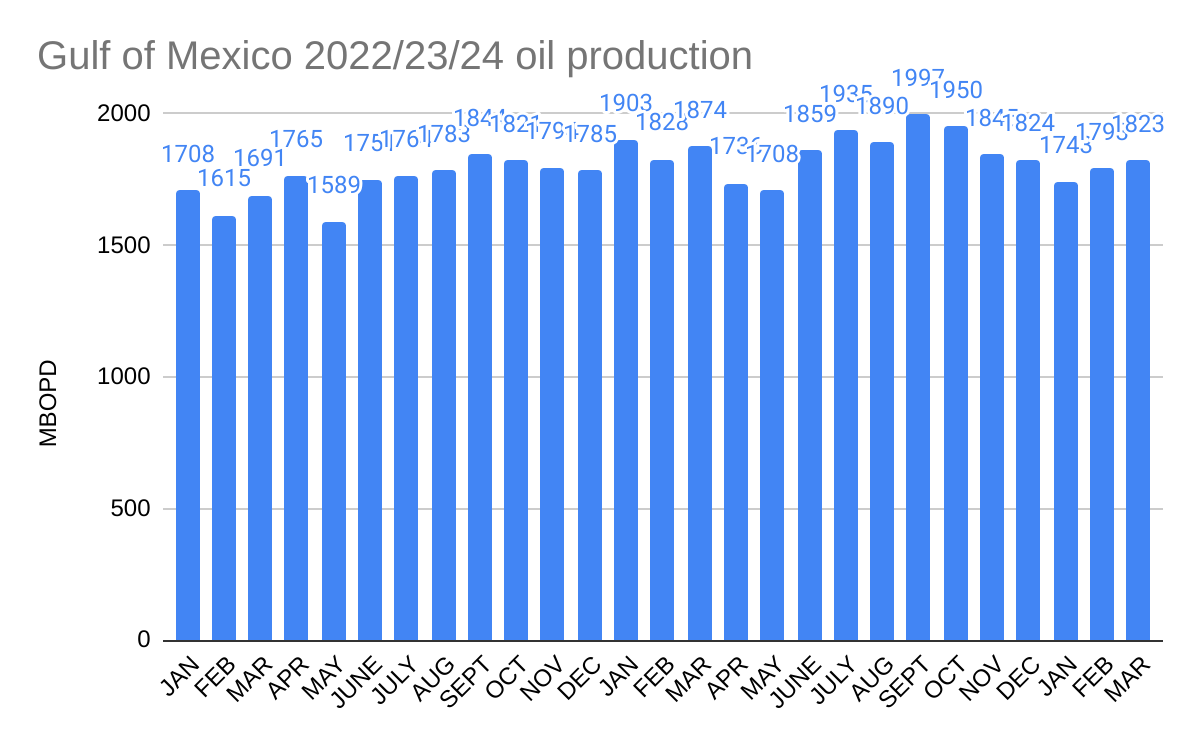

March production (1823 MBOPD) has been added to the GoM summary chart (below).

The Main Pass Oil Gathering (MPOG) system reportedly remained shut-in until early April. We should learn more about the impact of that shut-in when the EIA releases the April production figure at the end of June. Meanwhile, we are still waiting for information from the NTSB on the MPOG incident. To date, the NTSB has only posted a short summary

Note that BOEM’s 2024 forecast called for production to average 2,013 MBOPD, which is above the 2023 peak of 1,997 MBOPD in September.

Most forecasts call for an active 2024 hurricane season, so interruptions in production are likely. There were no production shut-ins from tropical storms in 2023.

CP’s acquisition of Marathon is an endorsement of shale production, most of which is from private lands. Sadly, these historically important OCS operators no longer have an interest in the Federal offshore sector.

Florida HB 1645 (attached) was signed by Gov. DeSantis on 5/15/2024. The bill boosts natural gas, prohibits offshore wind turbines, and deletes references to climate change and greenhouse gases in state law. Given the State’s support for traditional energy sources, is it time to renew the dialogue about exploration and production in the Eastern Gulf of Mexico (EGOM)?

HB 1645 prohibits offshore and coastal wind development (p. 30), acknowledges that natural gas is critical for power resiliency, prohibits zoning regulations that restrict gas storage facilities and gas appliances (p.8), and relaxes permitting requirements for pipelines <100 miles long.

Given Florida’s energy preferences as expressed in this legislation, the State could assist regional energy planners by better defining its position on oil and gas leasing in the EGOM. What limits, in terms of lease numbers and minimum distances from shore, would best improve Florida’s energy supply options while further minimizing environmental risks?

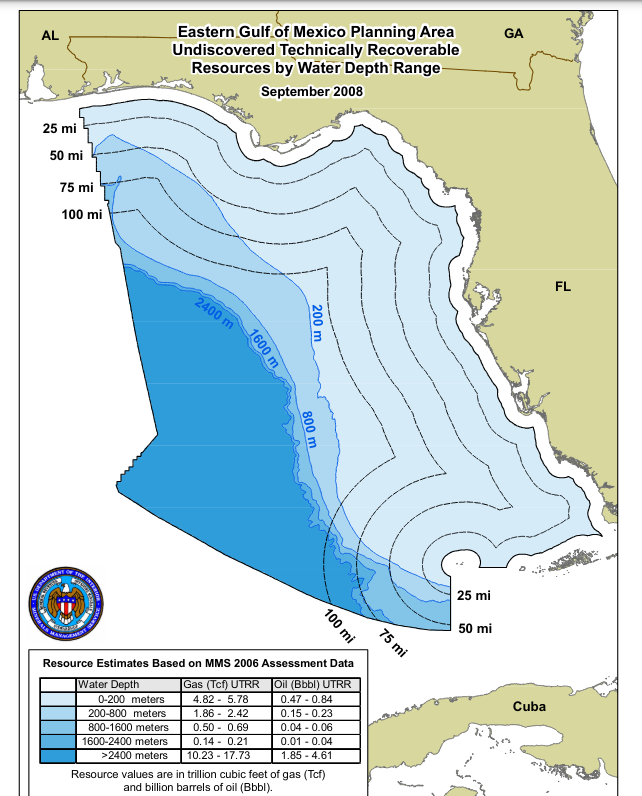

As illustrated on the map below, the petroleum geology of the EGOM and Florida’s preferences are likely aligned in that the best prospects for oil and gas production are in deep water and more than 100 miles from the State’s coast.Does Florida support a 100 mile buffer?

The 4/20/2010 Macondo blowout was a tragic failure that has been, and will continue to be, discussed at length on this blog. We should also acknowledge that prior to Macondo 25,000 wells were drilled on the US OCS over a 25 year period without a single well control fatality, an offshore safety record that was unprecedented in the U.S. and internationally. We should also applaud recent advances in well integrity and control, including the addition of capping stack capabilities that further reduce the risk of a sustained well blowout.

Florida’s independent thinking on energy policy is commendable. That independence is contingent on importing petroleum products and natural gas from elsewhere in the Gulf region. Securing that supply over the intermediate and longer term should be a priority for Florida. In that regard, EGOM production is an important consideration.

“Exxon Mobil has led a persistent and apparently successful lobbying campaign behind the scenes to push the US federal government to adopt rules that would allow the conversion of existing oil and gas leases in the Gulf of Mexico into offshore carbon capture and storage (CCS) acreage, according to documents seen by Energy Intelligence and numerous interviews with industry players.”Energy Intelligence

The Energy Intelligence article documents the ongoing carbon disposal lobbying by Exxon and others. Those meetings are okay prior to publishing a Notice of Proposed Rulemaking (NPRM) for public comment. However, the article implies that the next step is a final rule: “Whether or not Exxon succeeds will become fully clear when the US issues final rules guiding CCS leasing, expected sometime this year.”

A final rule this year is unlikely, because an NPRM has to be published first for public comment. The only exception would be if BOEM was able to establish “good cause” criteria for a direct final or interim final rule in accordance with the Administrative Procedures Act. Such an attempt at corner cutting seems unlikely, especially in an election year when all regulatory actions are subject to additional scrutiny.

Exxon must have thought they had a clear path forward after 11th hour additions to the “Infrastructure Bill” authorized carbon disposal on the OCS, exempted such disposal from the Ocean Dumping Act, and provided $billions for CCS projects. Keep in mind that the Infrastructure Bill was signed just two days before OCS Oil and Gas Lease Sale 257, at which Exxon acquired 94 leases for carbon disposal purposes.

What the Infrastructure Bill did not provide is authority to acquire carbon disposal leases at an oil and gas lease sale. Now the lobbyists are apparently scrambling to overcome that obstacle administratively.

A single company or small group of companies should not be dictating the path forward for the Gulf of Mexico. Super-major Exxon is a relative minnow in the Gulf of Mexico OCS. They have not drilled an exploratory well since 2018, not drilled a development well since 2019, operate only one platform (Hoover, installed in 2000), ranked 11th in 2023 oil production, and ranked 29th in 2023 gas production.

Lastly, and most importantly, public comment on the myriad of technical, financial, and policy issues associated with GoM carbon disposal is imperative. That input is essential before final regulations are promulgated.

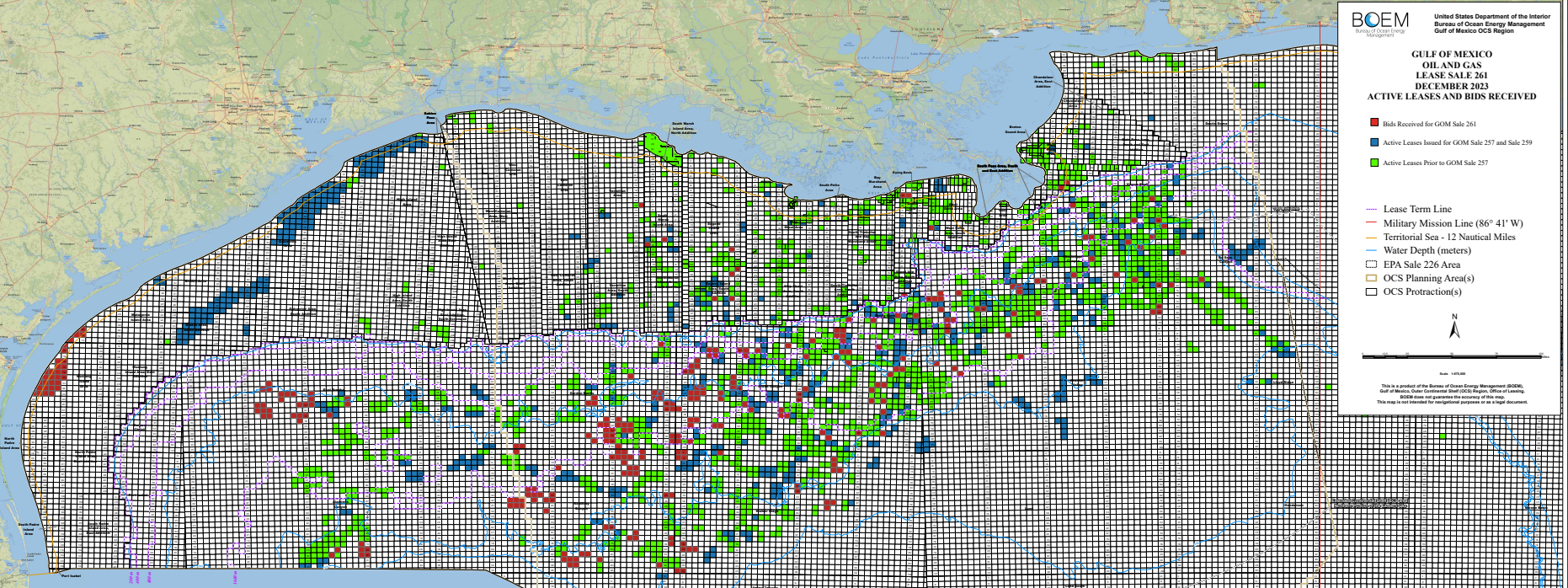

At Sale 261, Repsol was the sole bidder for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 and 259.

“Deepwater is back in vogue.” (Pablo Medina, Welligence)

“Newer deepwater projects have the attributes oil and gas companies are looking for: longer-term production, lower breakeven costs, big resource potentials and lower carbon emissions.” (Medina)

Capital spending on all-new deepwater drilling is poised to hit a 12-year high next year (Rystad)

Investment in all-new and existing deepwater fields could hit $130.7 billion in 2027, a 30% jump over 2023 (Rystad)

Deepwater resources offer lower carbon emissions intensity than shale and other tight oils, averaging 2kg of carbon dioxide per barrel less than shale. (Rystad)

“The return of offshore and deepwater operations is going to be a big topic at OTC, and Namibia is going to be talk of the show.” (James West, Evercore)

Enthusiasm for offshore has climbed with discoveries and technology breakthroughs. Namibia’s Mopane is forecast to hold as much as 10 billion barrels of oil. (Portuguese oil company Galp Energia)

Rates for some rigs have surpassed $500,000 a day and contract durations are lengthening as supply dwindles.

The government’s decision to require that a capping stack be located in Guyanais prudent. Although the need for a capping stack is dependent on multiple barrier failures and is thus extremely low, the environmental and economic consequences of a prolonged well blowout warrant timely access to this tertiary well control option.

A capping stack must be properly maintained and deployable without delay. In that regard, BSEE has a good program for testing Gulf of Mexico capping stack readiness. Capping stack drills are an important post-Macondo addition to the unannounced oil spill response program that dates back to 1981.

“Troy Naquin, BSEE New Orleans District, observes as a capping stack is carefully lowered onto the deck of ship to be transported more than 100 miles offshore for a drill designed to test industry’s ability to successfully deploy it in case of an emergency, May 8, 2023.” BSEE photo/Bobby Nash