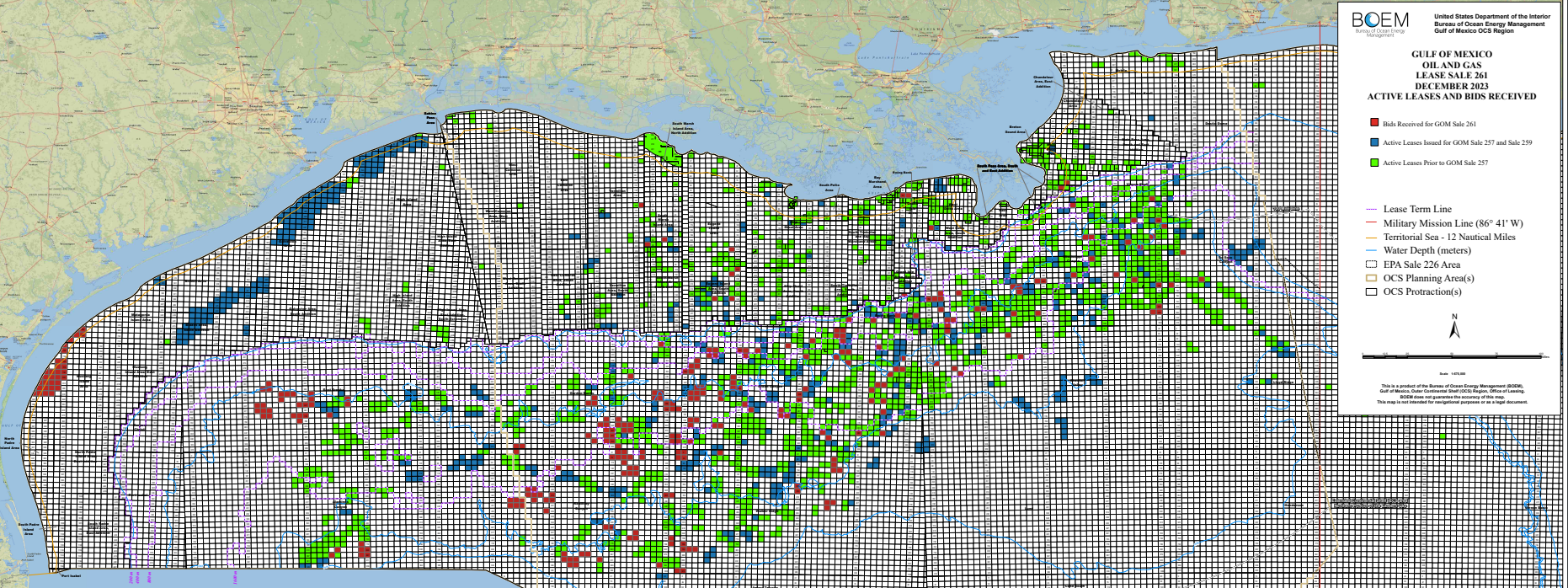

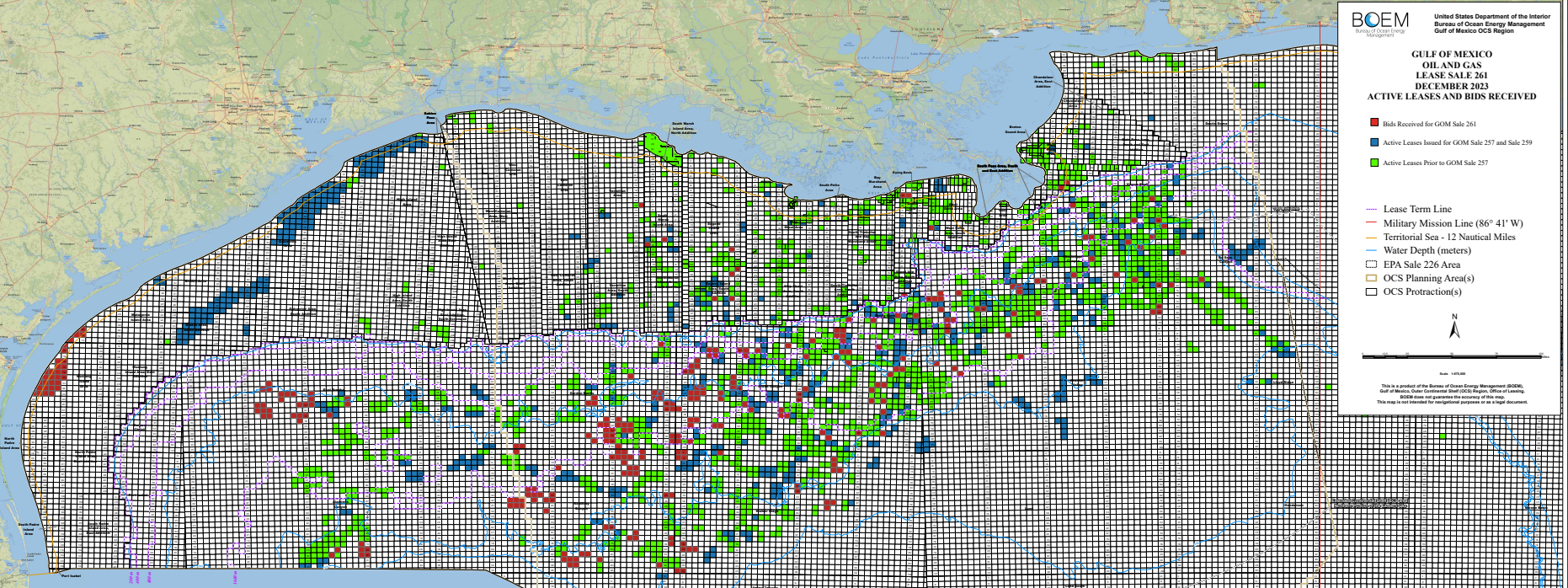

199 oil and gas leases were wrongfully acquired at Sales 257, 259, and 261 with the intent of developing these leases for carbon disposal purposes. Repsol was the sole bidder at Sale 261 for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

Despite false starts by Exxon and Repsol (see above summary), no carbon sequestration (disposal) leases may be issued or developed until implementing regulations have been promulgated. In that regard, no news is good news for those who are less than enamored with CO2 disposal in the Gulf of Mexico.

The implementing regulations will be controversial. Most operating companies prioritize GoM production over GoM disposal. Most environmental organizations are strongly opposed to CO2 disposal schemes that sustain fossil fuel production and benefit fossil fuel producers. Taxpayers are leery of subsidizing these projects and absorbing increased costs for energy and consumer goods.

The Administration is, of course, well aware of this opposition and will not be publishing implementing regulations prior to the election. The next Administration, regardless of the election outcome, will no doubt take a hard look at these issues before proposing regulations.

The few oil and gas producers that are rather cynically hoping to cash in on CO2 disposal in the GoM will therefore have to wait, perhaps for a long time.

Carbon sequestration (i.e. subsurface disposal) is a controversial and divisive topic, and important questions regarding the costs and benefits remain. Nonetheless, the Infrastructure Bill of 2021 authorized the disposal of CO2 on the OCS, and stipulated that the Secretary of the Interior promulgate regulations for that purpose. However, that major task cannot be completed without a better understanding of the potential environmental impacts.

BOEM has announced a study (see attached pages from their new Environmental Studies Plan) to consider the potential for CO2 leakage and related environmental concerns. A few excerpts from BOEM’s summary follow:

Problem: Potential CO2 leakage from carbon sequestration (CS) project activities could occur via a number of pathways. Few studies model and/or measure CO2 leakage, transport, dispersion, attenuation, and environmental impacts in the offshore environment, and those that do exist are preliminary.

Intervention: BOEM needs more information about the dynamics, fate, transport, and potential environmental impacts of CO2 leakage under various scenarios, including worst-case, on the OCS to inform the new nationwide CS Program and to protect the environment from CO2 leakage.

Comparison: The study will model CO2 leakage under various scenarios, including worst-case scenarios, using the GOM OCS Region as a case-study and can be applied to all OCS regions. Outcome The leakage and worst-case scenario modeling will aid BOEM’s ongoing rulemaking efforts, program development and implementation, and future operational needs including NEPA analyses, lease planning, lease stipulations, consultations, plan and permit approvals, mitigation measures, risk assessment and monitoring requirements, etc. Study results will also provide direction for future studies to include field and/or laboratory analyses.

The performance period for this important study extends through 2027, so it’s hard to envision final CS regulations prior to that date. You can’t issue regulations without first assessing the potential harm that could result from their promulgation (as required by NEPA).

BOEM’s summary mentions “the anticipation of a CS lease sale in the GOM after final regulations are published.” Hopefully, this also means that BOEM will not permit improperly acquired oil and gas leases (Sales 257, 259, and 261) to be converted to CS leases.

At Sale 261, Repsol was the sole bidder for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

The 199 oil and gas leases that were wrongfully acquired for carbon disposal purposes remain idle with the government collecting rental payments at the rate of $10/acre/yr ($7 for Sale 257 leases). Collectively, this amounts to approximately $10 million/yr.

Presumably, the lessees cannot claim CCS tax credits for their bonus and rental payments.

The primary term for these leases is only 5 years, and the clock is ticking. The 94 oil and gas leases acquired by Exxon at Sale 257 for carbon disposal purposes are approaching the end of their second year. They would be almost a year older if litigation hadn’t delayed the issuance of Sale 257 leases (break for Exxon?).

No exploration plans have been filed for any of these leases. Presumably Exxon and Repsol do not intend to drill any wells unless the leases are converted to authorize carbon disposal.

The “Infrastructure Bill,” signed 2 days before Sale 257, required the Secretary of the Interior to promulgate regulations not later than one year after the date of enactment (11/15/2021). That deadline has long passed.

The delay in the regulations is understandable given the complex lease management, operational, and environmental issues.

Like the practices and operations they are intended to enable, the regulations are certain to be divisive. Neither the offshore industry nor the environmental community are of one mind on these issues, particularly with regard to the acquisition of oil and gas leases for carbon disposal purposes.

Energy Intelligence suggests that final carbon disposal regulations will be promulgated this year. This is highly unlikely, given that a proposed rule must first be published for public comment.

Publication of a proposed rule prior to the election is unlikely – too controversial.

Presumably, the regulations will establish a competitive process for the conversion of any oil and gas leases.

The leases that were wrongfully acquired at Sales 257, 259, and 261 should not be extended for any period of time, even if their expiration date approaches before a competitive process is established.

“Exxon Mobil has led a persistent and apparently successful lobbying campaign behind the scenes to push the US federal government to adopt rules that would allow the conversion of existing oil and gas leases in the Gulf of Mexico into offshore carbon capture and storage (CCS) acreage, according to documents seen by Energy Intelligence and numerous interviews with industry players.”Energy Intelligence

The Energy Intelligence article documents the ongoing carbon disposal lobbying by Exxon and others. Those meetings are okay prior to publishing a Notice of Proposed Rulemaking (NPRM) for public comment. However, the article implies that the next step is a final rule: “Whether or not Exxon succeeds will become fully clear when the US issues final rules guiding CCS leasing, expected sometime this year.”

A final rule this year is unlikely, because an NPRM has to be published first for public comment. The only exception would be if BOEM was able to establish “good cause” criteria for a direct final or interim final rule in accordance with the Administrative Procedures Act. Such an attempt at corner cutting seems unlikely, especially in an election year when all regulatory actions are subject to additional scrutiny.

Exxon must have thought they had a clear path forward after 11th hour additions to the “Infrastructure Bill” authorized carbon disposal on the OCS, exempted such disposal from the Ocean Dumping Act, and provided $billions for CCS projects. Keep in mind that the Infrastructure Bill was signed just two days before OCS Oil and Gas Lease Sale 257, at which Exxon acquired 94 leases for carbon disposal purposes.

What the Infrastructure Bill did not provide is authority to acquire carbon disposal leases at an oil and gas lease sale. Now the lobbyists are apparently scrambling to overcome that obstacle administratively.

A single company or small group of companies should not be dictating the path forward for the Gulf of Mexico. Super-major Exxon is a relative minnow in the Gulf of Mexico OCS. They have not drilled an exploratory well since 2018, not drilled a development well since 2019, operate only one platform (Hoover, installed in 2000), ranked 11th in 2023 oil production, and ranked 29th in 2023 gas production.

Lastly, and most importantly, public comment on the myriad of technical, financial, and policy issues associated with GoM carbon disposal is imperative. That input is essential before final regulations are promulgated.

At Sale 261, Repsol was the sole bidder for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 and 259.

14 of the high bids at Gulf of Mexico Lease Sale 259 were rejected. Did those tracts receive bids at sale 261? What was the net gain or loss of revenue? See the summary bullets and table below

6 of the 14 tracts received no bids whatsoever

5 of the 14 tracts received higher bids that were accepted.

2 tracts received substantially higher bids that were again rejected

1 tract received a lower bid that was accepted

net bonus revenue gain to the govt from the bid rejections (pending re-offering at future sales): $1,032,877

net bonus revenue gain = 0.27% of the total high bids at sale 261

net loss in future rental and royalty payments: ????

For a net bonus revenue gain to date of only 1/4 of one per cent, 8 of the 14 sale 259 tracts with rejected high bids remain closed to exploration. The timing of any future sales is very much in doubt given the minimalist 5 year leasing plan and the associated legal challenges.

Current bid evaluation practices only make sense if regular lease sales are held on a predictable schedule, as has historically been the case.

A post from last March discussed the high and seemingly unfair royalty and rental rates for new leases in the shallow waters of the Gulf of Mexico shelf. A 50% increase in the shelf royalty rate for lease sales 259 and 261 combined with rather punitive rental rates have likely contributed to the sharp decline in bidding for shelf lease blocks (see table below).

This decline in shelf bidding is unfortunate because the smaller companies that operate in the shallow waters of the Gulf are critical to sustaining the production infrastructure. These companies are also significant producers of environmentally favorable nonassociated (gas-well) natural gas.

lease sale

shelf blocks with bids (excluding CCS bids)

sum of high shelf bids ($million, excluding CCS bids)

BOEM has completed their evaluation of the Sale 261 shelf bids (see below). Each of these blocks received only a single bid, and every bid was accepted. Ironically, the invalid CCS bids for blocks that have no oil and gas value, were the first to be accepted. This was also the case for Sales 257 and 259.

Company

Block

high bid ($) per acre ($)

date accepted

Byron

SM 60

128,750 25.75

2/2

Byron

SM 70

182,235 33.32

2/20

Cantium

GI 35

125,000 25.00

2/20

Cantium

GI 36

125,000 25.00

2/20

Cantium

MP 314

125,000 25.00

3/12

Cantium

SP 63

125,000 25.00

3/12

Arena

EI 231

135,000 27.18

2/20

Arena

EI 277

135,000 27.18

2/20

Arena

EI 281

135,000 27.18

2/20

Arena

EI 340

135,000 27.18

2/20

Arena

EI 343

135,000 27.18

2/20

Arena

WD 119

135,000 26.75

3/12

Focus

V 152

121,152 25.16

2/20

Repsol

36 CCS bids

187,200 (1) 32.50

1/23

(1) All of the Repsol bids were $32.50/ac. Total bids varied by block size, but were $187,200 for the 5760 acre blocks.

Suggestions:

Seek a legislative fix to the Inflation Reduction Act😉 provision that established a 1/6 royalty rate floor for all OCS leases (formerly the royalty rate was 1/8 for leases on the shelf).

In the interim, administratively lower the royalty for shelf leases to 1/6 (from 18 3/4%).

For future oil and gas lease sales, accept all high bids that exceed the specified minimum bid (currently $25/ac for the shelf). The Gulf of Mexico shelf has been extensively explored and developed for 70 years. While prospects remain, they are generally marginal as evidenced by the recent lease sale results. Fair market value is what any company is willing to bid (above the specified minimum).

Focus on assuring that lease purchasers are technically qualified to minimize safety risks, and that financial assurance for decommissioning (for new and existing leases owned by the high bidder) has been fully addressed.

Bayou Bend CCS LLC commenced drilling an offshore (Texas State waters) and an onshore stratigraphic well for carbon sequestration in the first quarter 2024.

Is offshore carbon disposal ocean dumping?One of the provisions that was slipped into the “2021 Infrastructure Bill” exempted carbon sequestration from the Marine Protection, Research, and Sanctuaries Act of 1972 (Ocean Dumping Act). This exemption revises the OCS Lands Act and thus does not apply to State offshore lands. The Texas offshore wells must therefore be permitted by EPA as “Class VI wells,” as is the case for onshore disposal wells. However, Texas and Louisiana have asked the EPA for “primacy,” which would allow state agencies to approve and oversee these operations.

Meanwhile, the regulations for carbon disposal on the OCS, which the Infrastructure Bill mandated by November 2022, have yet to be published for comment. The latest Federal regulatory agenda indicates a publication date of 12/00/2023 for these regulations. Presumably the staff work has been completed and the rule is stalled in the review process.

Despite the absence of a regulatory framework, BOEM has accepted sequestration bids at the last three oil and gas lease sales. These bids were evaluated as if the leases were being acquired for oil and gas exploration and production, even though the bidders’ intentions were widely known. Why was BOEM a willing participant in this charade, not just at one sale, but at three sales in succession?

Given that the perceived carbon disposal bonanza is dependent on mandates and subsidies, one has to wonder about the massive revenue projections for this industry and raise concerns about the associated public and private financial risks. What is the long term business plan for this industry? Who will be monitoring the offshore wells (in perpetuity)? How will the public be protected from financial assurance and leakage risks? We will see how the myriad of carbon sequestration issues are addressed in the proposed regulations.

Are Exxon and Chinese partner (CNOOC) attempting to use Chevron’s acquisition of Hess to improve their already lucrative position in Guyana’s prolific Stabroek block?

The Stabroek operating agreement outlines terms for Hess, Exxon, and CNOOC to explore and develop the block.

This Stabroek agreement includes a right of first refusal (ROFR) provision which allows the parties to buy out the stake of one of them in the event of a ‘change of control’ transaction.

Chevron and Hess argue that the merger’s structure does not trigger the ROFR clause.

Exxon and CNOOC argue that the clause applies. This could force Hess to offer its stake in the Stabroek block to its partners first.

The Exxon/CNOOC position seems to be a stretch. Chevron did not buy the Stabroek share; they bought the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership.

As an offshore operator, Exxon has been highly responsible from a safety standpoint. However, the company has a shown tendency to stretch the envelope when it comes to contract rights. The most recent example was their acquisition of 163 GoM oil and gas leases for carbon disposal purposes, contrary to the terms of the sale notice and lease contracts.

Updated BSEE incident data tables. The last data are for 2021. The public should have timely access to information about safety and pollution events on Federal lands and the performance records of companies conducting these operations. During the MMS era, these tables were updated quarterly and the Directors (all administrations) did not tolerate delay.

The final NTSB report on the 12/29/2022 GoM helicopter crashthat killed 4. The preliminary report was timely, but the final report has yet to be published. Is the NTSB considering the muddled regulatory regime for helidecks. (Regulatory fragmentation is a safety risk factor).

Corrected IRF performance data. This is arguably the IRF’s most important work stream and the data should be accurate. Some commentary about safety performance would also be helpful. What do the incident trends tell us? How does safety performance compare internationally?

Data on safety incidents associated with the OCS wind program during the site assessment, construction, and operational phases.

Information on the mysterious sinking of the Aban Pearl semi-submersiblein May 2010. We know an investigation was conducted. 14 years have now elapsed and the report has still not been shared.

At Oil and Gas Lease Sale 261, Repsol was the sole bidder for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 and 259. All 36 of the Repsol bids have now been accepted.

As previously posted here and here, carbon disposal bidding at the last 3 oil and gas lease sales has made a mockery of the leasing process and the regulations that guide it.

Hopefully, the carbon sequestration regulations that are under development will preclude conversion of leases acquired at Sales 257, 259, and 261. At a minimum, these regulations should require a competitive process for converting any oil and gas leases.