It’s prudent, if not imperative, to tow floating wind turbines to sheltered coastal locations for major maintenance. For that reason, Hywind, the world’s first floating wind farm will be offline for up to 4 months this summer.

Hywind Scotland‘s operator, Norwegian power giant Equinor, says that operational data has indicated that its wind turbines need work. The pilot project has been in operation since 2017.

The five Siemens Gamesa turbines will be towed to Norway this summer. An Equinor spokesperson said, “This is the first such operation for a floating farm, and the safest method to do this is to tow the turbines to shore and execute the operations in sheltered conditions.”

electrek

Published data indicate that Hywind has been the UK’s best performing offshore wind farm. Performance data for Hywind, and a chart illustrating the capacity factors since commissioning, are posted below. The 2024 capacity factor will, of course, be substantially reduced as a result of the essential offsite maintenance.

| rolling 12 month capacity factor ending 5/2022 | life capacity factor | age (years) | installed capacity (MWp) | total elec generated (GWh) | power/ unit area spanned (W/m2) | |

| Hywind Scotland | 49.5% | 52.6% | 4.6 | 30 | 642 | 1.0 |

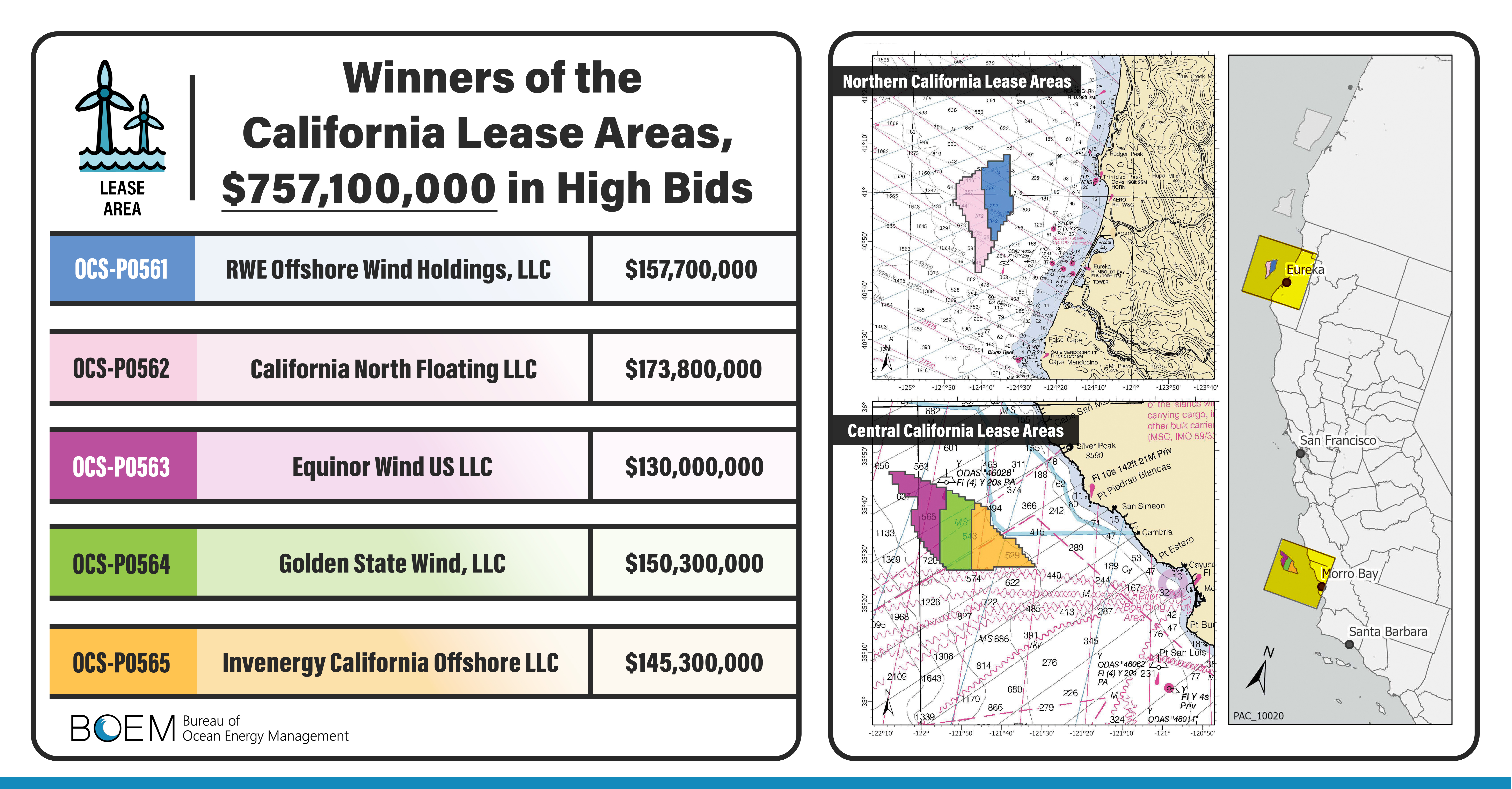

The first US floating turbines are expected to be at these California offshore leases, and Hywind operator Equinor is one of the lessees:

Given the financial challenges facing the offshore wind industry, the still emerging technology, and the risks inherent in California offshore development, the amounts bid on these leases only 13 months ago are stunning.

Some Central Coast residents are not enamoured with “another attempt to industrialize the coast.” Although the turbines will be >20 miles offshore, they will have to be towed to shore for major maintenance. For the Central California leases, nearby harbor areas like Morro Bay (pictured below) would be overwhelmed by the large structures and the maintenance and repair operations. Towing the towers to LA/Long Beach, albeit rather distant from the leases, would seem to be the preferred option for such work.

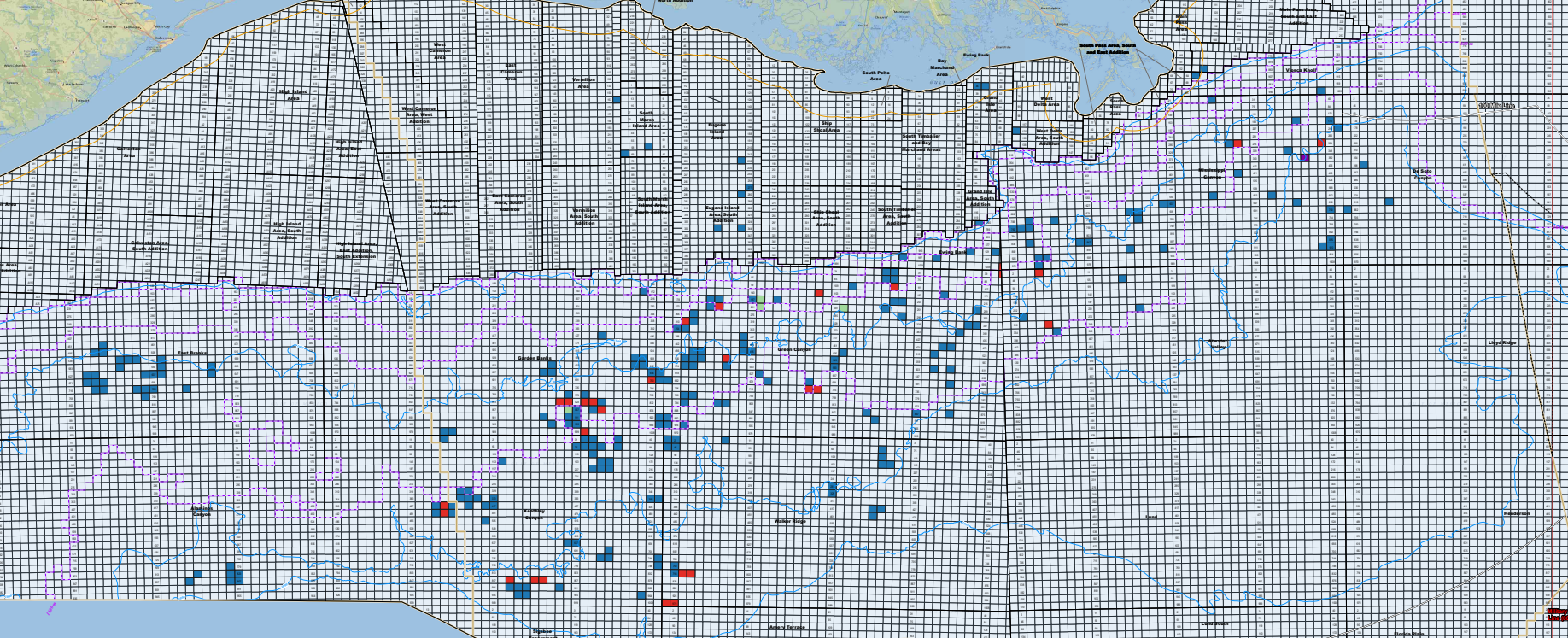

Ironically, a report for BOEM, points to synergies between the offshore wind industry and oil and gas decommissioning industry. Such synergies will only be possible if longstanding oil and gas decommissioning obstacles are satisfactorily addressed and the offshore wind projects proceed as planned.

Which will come first – platform decommissioning or wind turbine commissioning? For those young enough to find out, what is the over-under for the years until (1) half of those platforms are decommissioned, and (2) half of the wind turbines commissioned? Any number <10 is unrealistic for either.