Per the Dept. of the Interior:

- TotalEnergies commits to invest approximately $1 billion—the value of its renounced offshore wind leases—in oil and natural gas and LNG production in the United States.

- Following their new investment, the United States will reimburse the company dollar-for-dollar, up to the amount they paid in lease purchases for offshore wind.

- Specifically, TotalEnergies will invest $928MM, in the following projects in 2026:

- The development of Train 1 to 4 of Rio Grande LNG plant in Texas;

- The development of upstream conventional oil in Gulf of America and of shale gas production.

- Following theseTotal investments, the U.S. will terminate the following leases and reimburse the company:

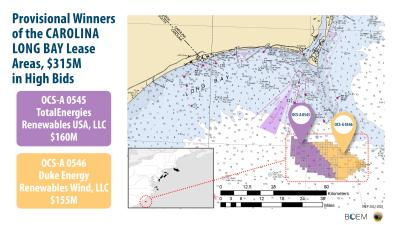

- Lease No. OCS-A 0535 (now 0545). The lease is located in Carolina Long Bay area. This lease was fully executed by TotalEnergies Renewables USA, LLC on June 1, 2022, after payment of $133,333,333.

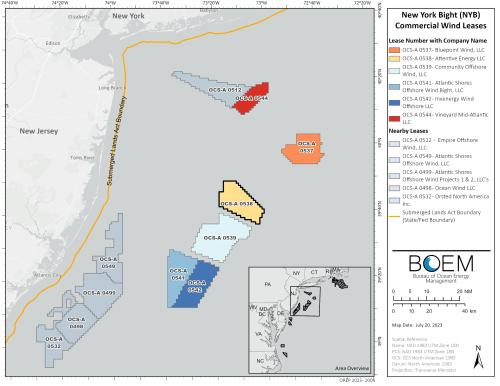

- Lease No. OCS-A 0538. The lease is located in the New York Bight area. The lease was fully executed by Attentive Energy, LLC on May 1, 2022, after payment of $795,000,000.

- Total pledges not to develop any new offshore wind projects in the United States.

Comments:

- This is a good deal for Total.

- They grossly overpaid for these leases during an offshore wind bidding frenzy.

- In particular, the bid of $795 million for the New York Bight lease seemed irrational even at the time of the sale (more so now).

- Construction had not begun on either wind project.

- The LNG project looks like a good investment, and there are good opportunities to buy into deepwater and onshore shale projects.