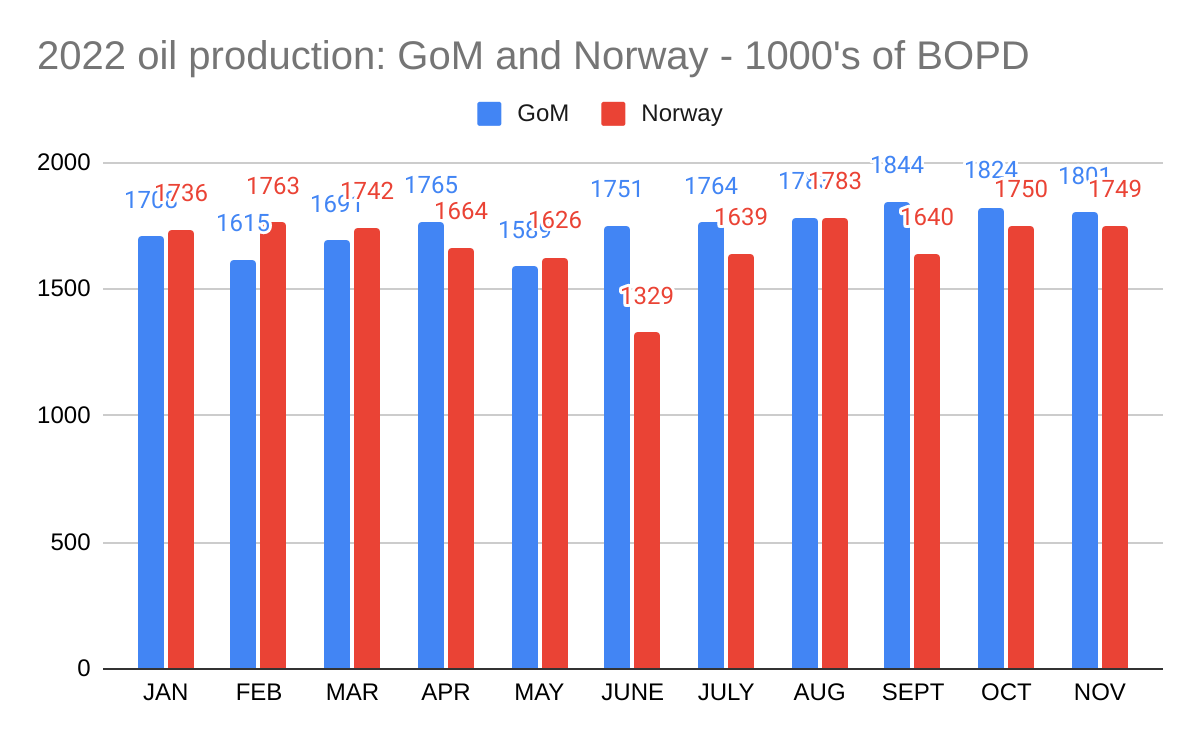

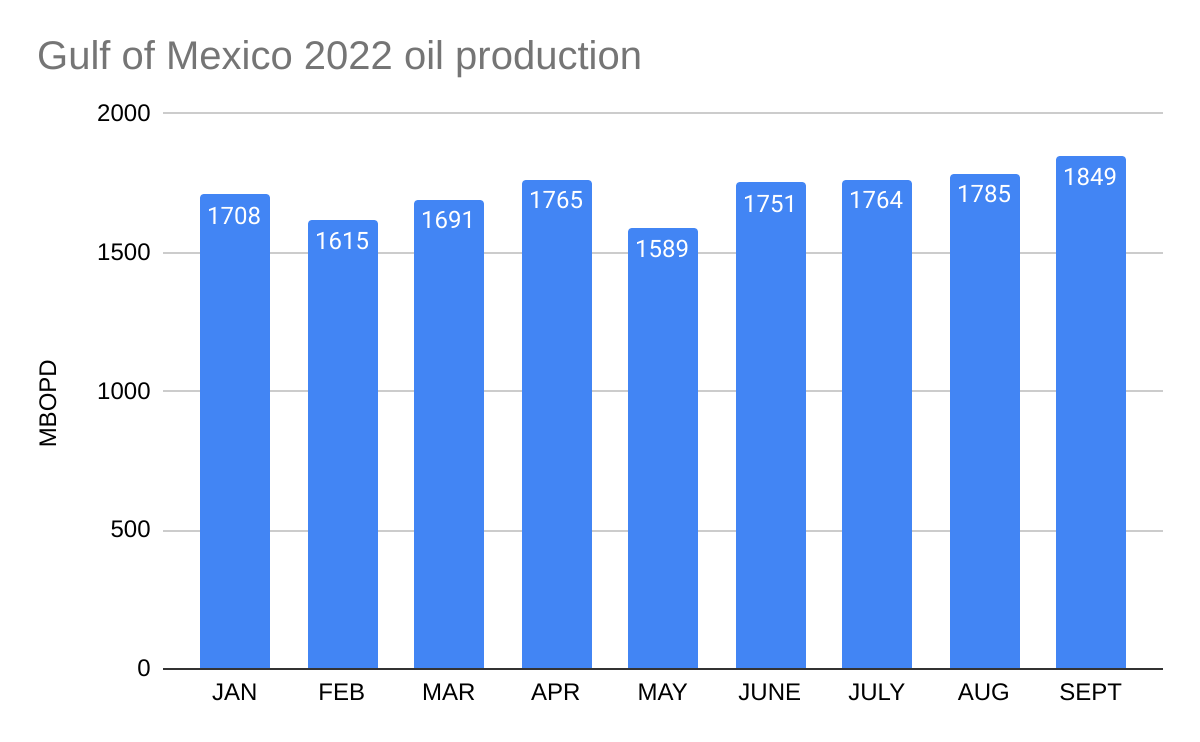

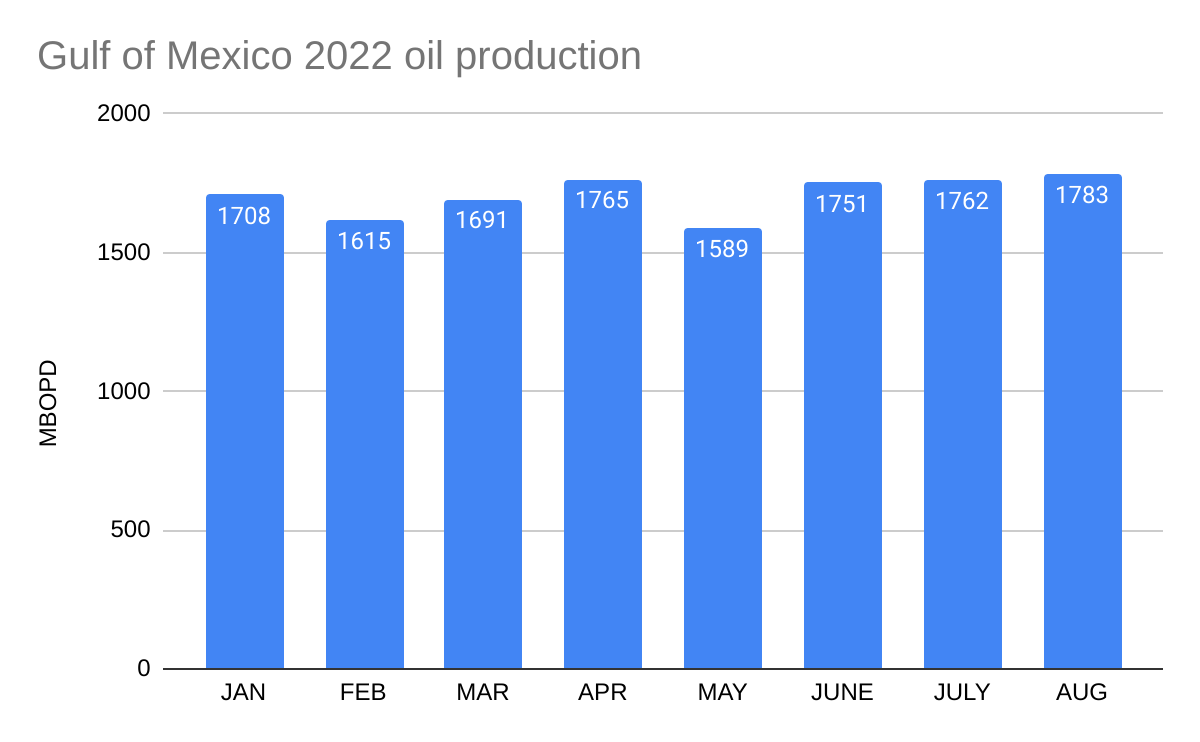

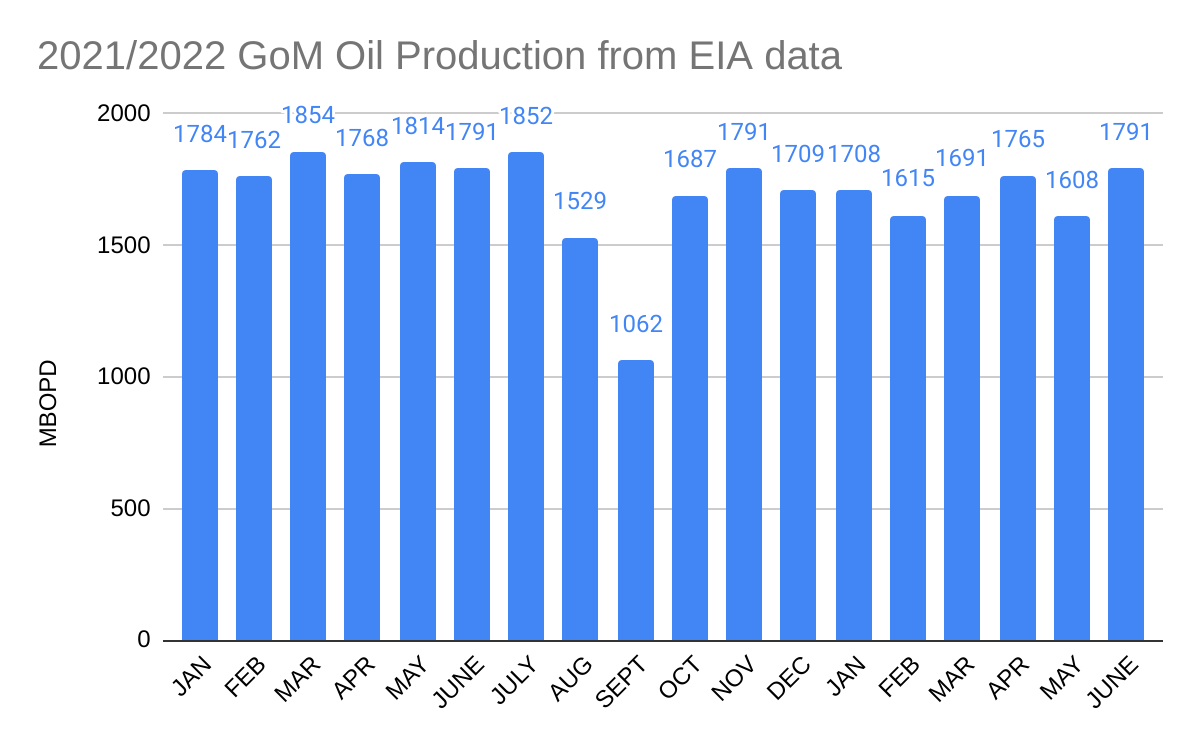

Comments on 2022 oil production:

- Solid year given governmental ambivilence and corporate uncertainties

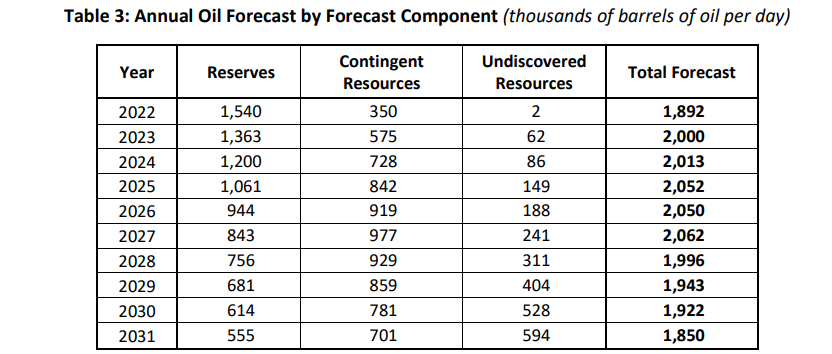

- Below BOEM production forecast.

- The 2019 annual production record remains intact at 1.897 million bopd, but could be exceeded in 2023 if (1) projected deepwater startups are on schedule, (2) prices remain above $70/bbl, (3) depletion is effectively managed, and (4) the hurricane season is again favorable

- The 2 million bopd average seems elusive, but could be surpassed in one of the next few years. After that, a greater commitment on the part of government and industry will be needed.

- The “energy transition” will not affect oil and gas demand for the foreseeable future, more nuclear power plants are not being built, and shale has its limitations. We better not neglect what is left of the OCS oil and gas program.