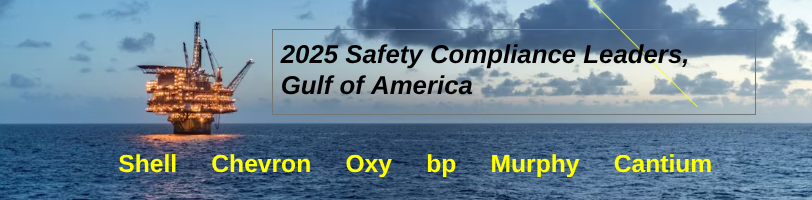

Shell topped the list followed by Chevron, Oxy/Anadarko, bp, Murphy, and Cantium.

Details and observations will be posted tomorrow.

Posted in Gulf of Mexico, Offshore Energy - General, Regulation, tagged 2025 safety compliance, AnadarkoOxy, bp, Cantium, Chevron, Gulf of America, INCs, Murphy Oil, Shell, top performers on February 4, 2026| Leave a Comment »

Shell topped the list followed by Chevron, Oxy/Anadarko, bp, Murphy, and Cantium.

Details and observations will be posted tomorrow.

Posted in energy policy, Gulf of Mexico, natural gas, Offshore Energy - General, tagged AAPG, BOEM, gas crunch, Gulf of America, Haynesville, ultradeep shelf gas, William DeMis on February 3, 2026| Leave a Comment »

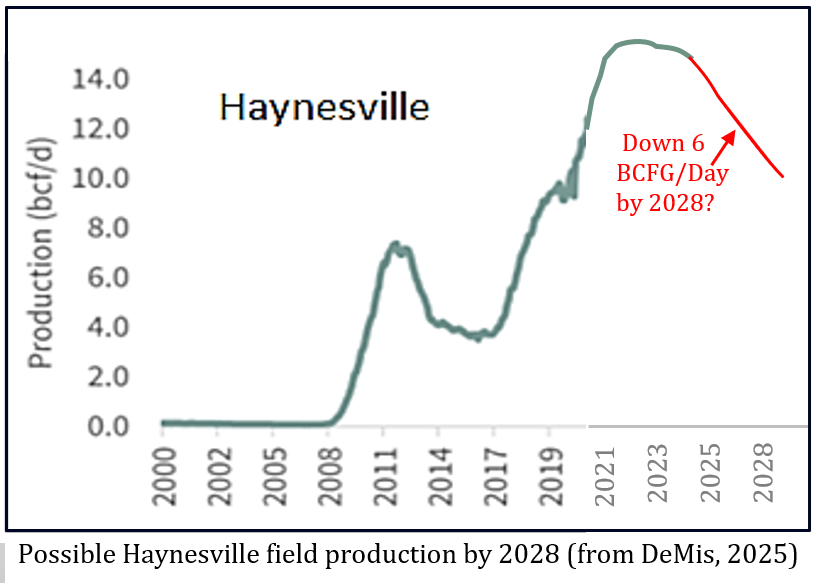

“We have not been finding enough new fields.” That’s William DeMis, president of Richelle Court, LLC, who said that, in addition to not finding enough, we keep erecting new ways to export what we’re not finding.

The way, he said, to avert the coming shortage is for people to find new sources of gas outside of Haynesville field, which for years, considering its proximity to the Gulf Coast, and the petrochemical plants of Southwest Louisiana, as well as pipelines, made it a swing producer for natural gas.

“But I can tell you from bitter experience over the last three years that finding people to fund greenfield exploration is darn near impossible. There is scant capital to drill natural gas wildcats in the U.S.” said DeMis.

Reiterating that it’s time for another look at ultradeep shelf gas in the Gulf. Should BOEM consider royalty incentives?

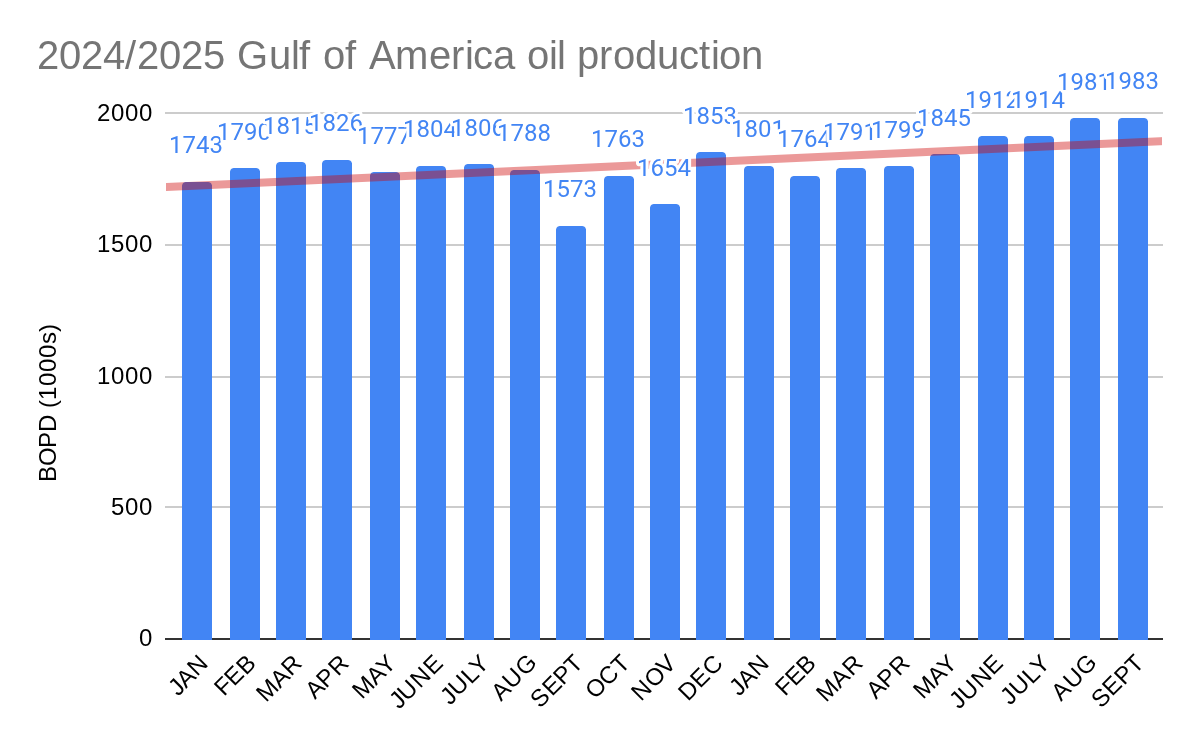

Posted in Gulf of Mexico, Offshore Energy - General, Uncategorized, tagged EIA data delayed, Gulf of America, November2025, oil production on February 2, 2026| Leave a Comment »

October 2025 Gulf of America oil production was the 2nd highest in history. As a result, the November data are much anticipated. Those data have been delayed from the scheduled date of 1/29/2026 until 2/6/2026. See the EIA advisory below

Petroleum Supply Monthly (PSM) data for November 2025 are scheduled for release on Friday, February 6, 2026.

The U.S. Census Bureau will release trade data (both imports and exports) for November 2025 on Thursday, January 29, 2026. As a result, we will delay release of PSM data for November 2025 from the original scheduled release date of January 30, 2026, until Friday, February 6, 2026. The delayed PSM release will allow us time to incorporate export data for November 2025.

Posted in accidents, Gulf of Mexico, Offshore Energy - General, Regulation, tagged 2025 safety compliance, fewest violations, Gulf of America, safety culture, safety leaders, top operating companies on January 30, 2026| Leave a Comment »

Next week, BOE will rank the 2025 Gulf of America Safety Compliance Leaders according to the number of incidents of non-compliance (INCs) per facility inspection.

How is your company’s safety culture?

Posted in Gulf of Mexico, Offshore Energy - General, UK, tagged acquisition, Gulf of America, Harbour Energy, LLOG on December 23, 2025| Leave a Comment »

The UK’s Harbour Energy is acquiring Louisiana’s LLOG Exploration Company for $2.7 billion in cash and $0.5 billion in shares.

“Today’s announcement delivers on Harbour’s long-standing ambition to establish a presence in the deepwater Gulf of America. With LLOG, we found the right combination of high-quality assets and a talented team, providing a strong strategic and cultural fit with our company. The transaction positions us as a leading player in a region with well-established infrastructure, a supportive fiscal and regulatory environment and opportunities for additional growth.”

LLOG was the 6th largest Gulf of America producer of both oil and gas in 2024 with production of 27 million bbls of oil and 34 BCF of gas. LLOG was the high bidder on 11 tracts in the recent BBG1 sale.

Harbour is not currently a Gulf of America leaseholder.

Reuters had reported that Shell was in advanced talks to acquire LLOG. Apparently, either Shell lost interest or Harbour made a more attractive offer.

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, tagged BOEM, Gulf of America, OCS Sale BBG1, questions answered, sale results on December 11, 2025| Leave a Comment »

See the updated comparison table in the previous BOE post.

The questions raised prior to the sale have been answered:

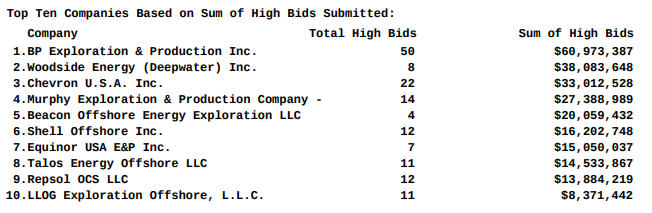

See the sale summary data. The top bidders list is pasted below.

Posted in energy policy, Offshore Energy - General, tagged Gulf of America, lease sale, Lease Sale BBG1, Leslie Beyer, Matt Giacona, oil and gas on December 10, 2025| Leave a Comment »

The sale was beautifully conducted by BOEM, and Leslie Beyer – Assistant Secretary for Land and Minerals Management, Dept of the Interior – and Matt Giacona, Acting BOEM Director, delivered strong messages in support of the OCS oil and gas program.

However, as a colleague commented just after the sale, it was beautiful but not big. He and I expected more given the time since the last sale and the attractive terms.

Below is a comparison with the previous 3 Gulf sales. More to follow.

| Sale No. | 257 | 259 | 261 | BBG1 |

| date | 11/17/2021 | 3/29/2023 | 12/20/2023 | 12/10/2025 |

| companies participating | 33 | 32 | 26 | 30 |

| total bids | 2233 | 2842 | 3161 | 219 |

| tracts receiving bids | 2143 | 2442 | 2751 | 181 |

| sum of all bids $millions | 198.5 | 309.8 | 441.9 | 371.9 |

| sum of high bids ($millions) | 101.7 | 263.8 | 382.2 | 279.4 |

| highest bid company block | $10,001,252.00 Anadarko AC 259 | $15,911,947 Chevron KC 96 | $25,500,085 Anadarko MC 389 | $18,592,086 Chevron KC 25 |

| most high bids company sum ($millions) | 46 bp 29.0 | 75 Chevron 108.0 | 65 Shell 69.0 | 50 bp 61.0 |

| sum of high bids ($millions) company | 47.1 Chevron | 108 Chevron | 88.3 Hess | 61.0 bp |

| most high bids by independent | 14-DG Expl. | 13-Beacon 13-Red Willow | 22-Red Willow | 14-Murphy |

1excludes 36 leases improperly acquired for carbon disposal purposes; 2excludes 69 leases improperly acquired for carbon disposal purposes; 3excludes 94 leases improperly acquired for carbon disposal purposes

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, tagged bp, carbon disposal, Chevron, Gulf of America, Lease Sale 257, Lease Sale 259, Lease Sale 261, Lease Sale BBG1, offshore oil and gas, Oxy, Red Willow, Shell on December 4, 2025| Leave a Comment »

Will the oil and gas lease sale boldly named Big Beautiful Gulf 1 (BBG1) live up to its grand name? Given the more favorable lease terms and the 2 year gap since the last sale, BBG1 should surpass the previous 3 sales (table below). Questions:

See the summary data below for the last 3 Gulf lease sales. We’ll fill in the blanks next week.

| Sale No. | 257 | 259 | 261 | BBG1 |

| date | 11/17/2021 | 3/29/2023 | 12/20/2023 | 12/10/2025 |

| companies participating | 33 | 32 | 26 | |

| total bids | 2233 | 2842 | 3161 | |

| tracts receiving bids | 2143 | 2442 | 2751 | |

| sum of all bids $millions | 198.5 | 309.8 | 441.9 | |

| sum of high bids ($millions) | 101.7 | 263.8 | 382.2 | |

| highest bid company block | $10,001,252.00 Anadarko AC 259 | $15,911,947 Chevron KC 96 | $25,500,085 Anadarko MC 389 | |

| most high bids company sum ($millions) | 46 bp 29.0 | 75 Chevron 108.0 | 65 Shell 69.0 | |

| sum of high bids ($millions) company | 47.1 Chevron | 108 Chevron | 88.3 Hess | |

| most high bids by independent | 14-DG Expl. | 13-Beacon 13-Red Willow | 22-Red Willow |

Posted in drilling, Gulf of Mexico, natural gas, Offshore Energy - General, tagged Blackbeard, Exxon, Freeport-McMoRan, Gulf of America, HPHT, lease sale, natural gas, Newfield, Treasure Island, ultra-deep gas on December 3, 2025| Leave a Comment »

“Natural gas and LNG are fast becoming the gravitational center of the global energy system, but some energy experts said the world is only beginning to grasp the scale of what’s to come.” ~Natural Gas Intelligence

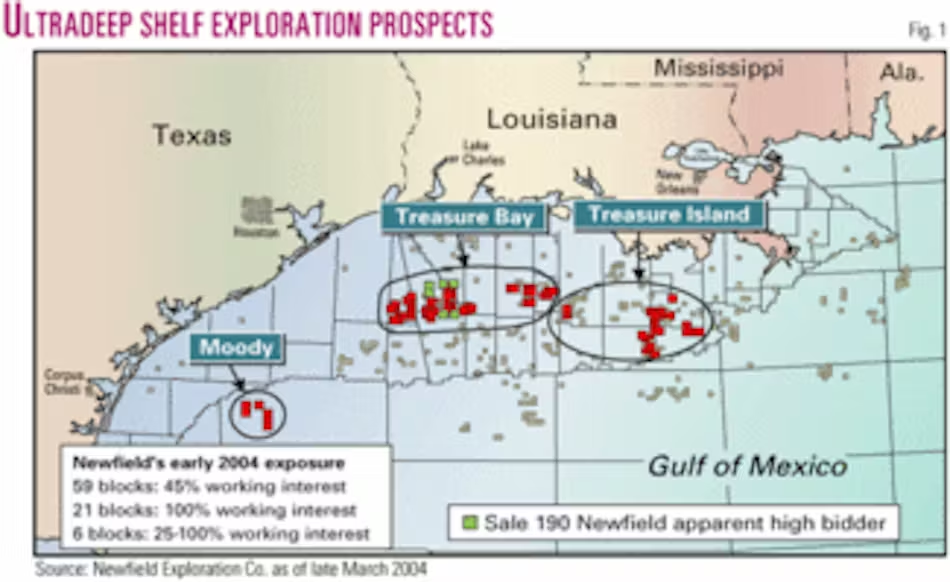

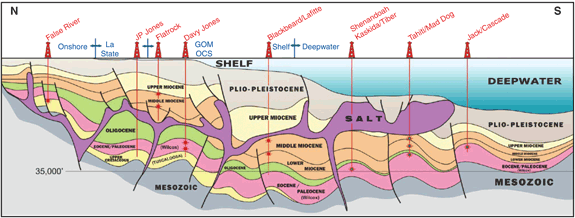

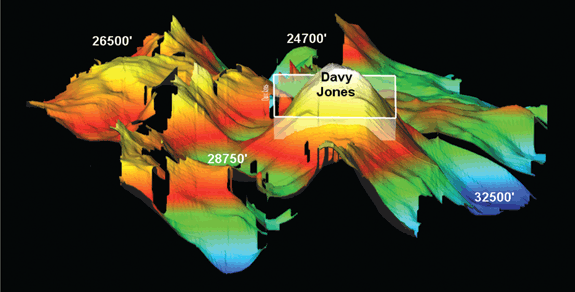

20 years ago Newfield, Exxon, and McMoRan drilled pioneering ultradeep wells targeting gas-prone reservoirs below salt welds in Miocene and older formations (diagrams below). The water depths were <100 feet but well depths exceeding 30,000 feet, and high temperatures and pressures, pushed the limits of drilling technology at the time. Noteworthy wells:

This program pioneered ultradeep drilling on the shelf, influencing later deepwater successes. Over the past 10 years, the deepwater industry has successfully demonstrated high pressure high temperature (HPHT) technology which could facilitate ultradeep exploration on the shelf.

Also, note that a company targeting hydrocarbons below 25,000 feet (true vertical depth subsurface) may earn an additional 3 years on their lease. (See the Notice for next week’s lease sale.) Will improved technology and demand expectations finally open the ultradeep gas frontier?

Posted in Gulf of Mexico, Offshore Energy - General, tagged 2 million bopd, Gulf of America, oil production, tropical storms on December 1, 2025| Leave a Comment »