Exxon doubled down on their strategic CCS bidding; their only bids (69 in total) again appeared to be solely for carbon sequestration purposes. As previously noted, acquiring tracts for CCS purposes is not authorized in an oil and gas sale. Arguably, these bids should be rejected.

The other super-majors, BP, Chevron, and Shell, were active participants as were many independents.

It was good to see BOEM Director Liz Klein announcing bids. This shows respect for the OCS oil and gas program.

BOEM published their Sale 257 Decision Matrix on Friday (2/24/2023), and my previous speculation regarding the rejected Sale 257 high bid has proven to be partially incorrect. The rejected high bid was submitted by BP and Talos and was for Green Canyon Block 777. BOEM’s analytics assigned a Mean of the Range-of-Value (MROV) of $4.4 million to that tract, which tied for the highest MROV for any tract receiving a bid. The BP/Talos bid was $1.8 million or just 40% of BOEM’s MROV. BOEM’s tract evaluation is interesting given that the other bid on this wildcat tract (by Chevron, $1.185 million) was considerably lower than the rejected BP/Talos bid.

The Sale 257 bid that I thought might have been rejected was for lease G37261. This lease was never issued per the lease inquiry data base and the final bid recap. BHP’s bid of $3.6 million for that tract (Green Canyon Block 79) was more than 5 times BOEM’s MROV of $576,000, and was accepted per the decision matrix. Why was the lease never issued?

Both Green Canyon 79 and 777 should again be for sale in legislatively mandated Sale 259, which will be held in just a few weeks on March 29, 2023, just 2 days prior to the deadline. It will be interesting to see what the bidding on those tracts looks like.

Meanwhile, Exxon and BOEM are still mum about the 94 Sale 257 oil and gas leases that Exxon acquired for carbon sequestration purposes.Note the large patches of blue just offshore Texas on the map above. These leases were all valued by BOEM at only $144,000 each, which is equivalent to the minimum bid of $25/acre. This valuation reflects the absence of perceived value for oil and gas production purposes. Exxon bid $158,400 for each tract, $27.50/acre or 10% higher than the minimum bid. Given that (1) the Notice of Sale only provided for lease acquisition for oil and gas exploration and production purposes, and (2) it was common knowledge that these tracts were acquired for carbon sequestration, should these bids have been rejected?

Last year, BOE featured 5 deepwater platforms that were under construction: Shell’s Vito and Whale, Murphy’s King’s Quay, bp’s Argos, and Chevron’s Anchor. These floating production units are noteworthy for their lighter, smaller designs. King’s Quay was the first to produce, beginning last April. The spotlight is now on Vito which began producing today. Vito’s peak production should reach 100,000 boe. The other 3 platforms are expected to begin production this year or next.

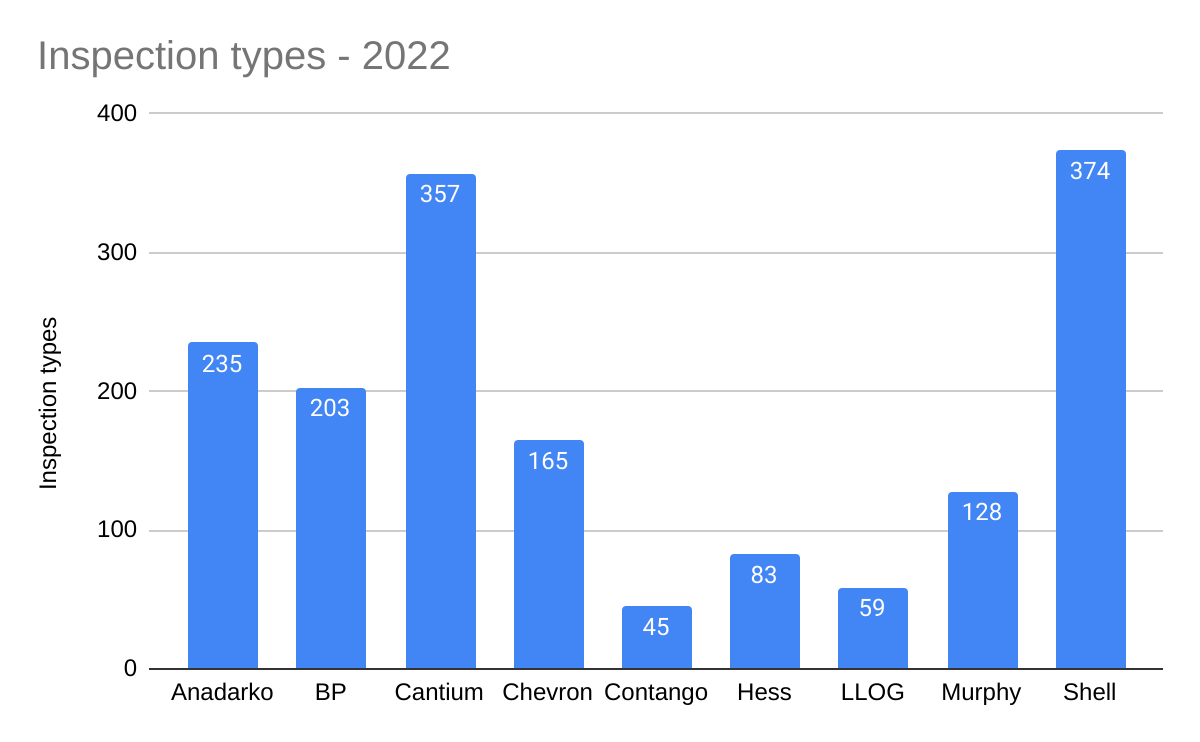

The Honor Roll companies for 2022 (listed alphabetically) are Anadarko (Oxy), bp, Cantium, Chevron, Contango, Hess, LLOG, Murphy, and Shell.

Our criteria:

Must average <0.3 incidents of noncompliance (INCs) per facility-inspection.

Must average <0.1 INCs per inspection-type. (Note that each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). On average, each facility-inspection included 3.25 types of inspections in 2022. Here is a list of the types of inspections that may be performed.)

Must operate at least 3 production platforms and have drilled at least one well (i.e. you need operational activity to demonstrate compliance and safety achievement).

May not have a disqualifying event (e.g. fatal or life-threatening incident, significant fire, major oil spill). Due to the extreme lag in updates to BSEE’s incident tables, investigation and news reports are used to make this determination.

Pacific and Alaska operations will be considered separately.

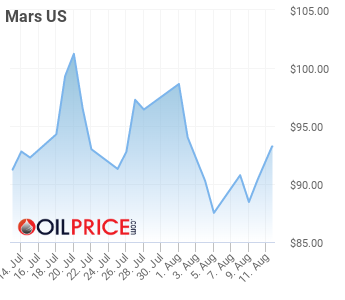

This is a good example of the interconnectivity of deepwater projects with major Shell, Chevron, and Equinor facilities shut-in as a result of a relatively minor downstream pipeline incident.

Mars crude price appears to have reacted to the shut-in news:

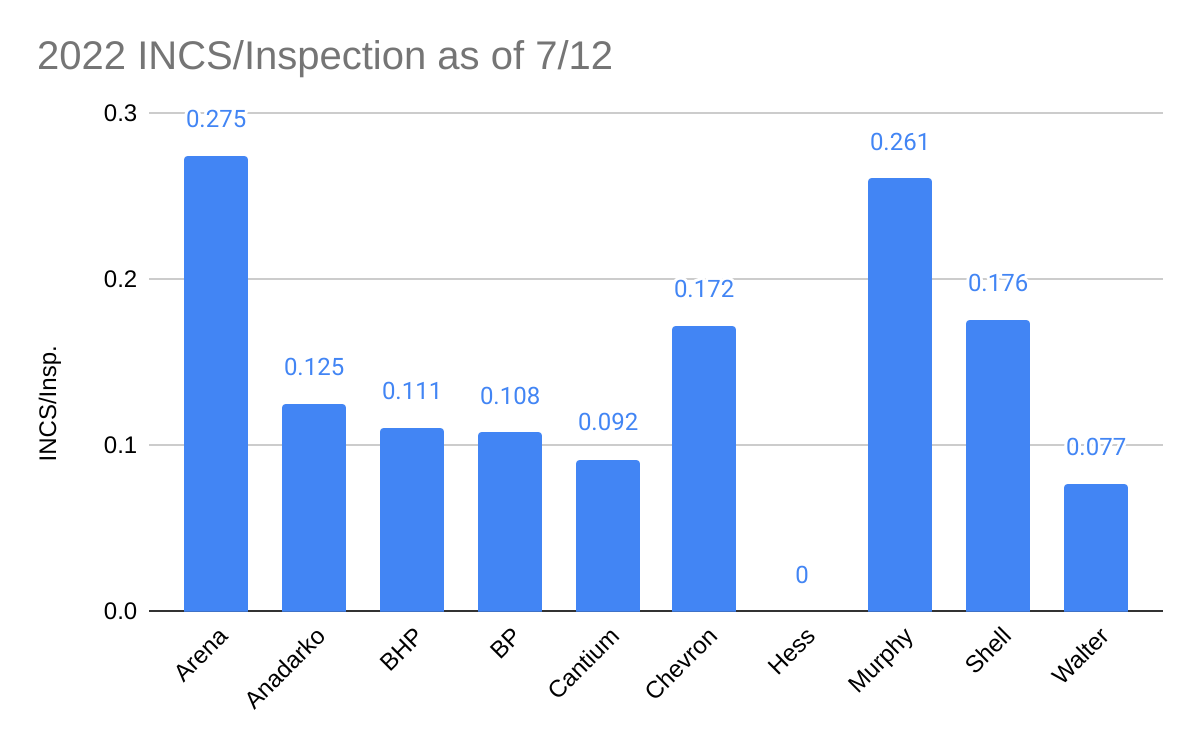

Operating companies (listed alphabetically): Arena, Anadarko (Oxy), BHP, bp, Cantium, Chevron, Hess, Murphy, Shell, and Walter

Criteria:

Must average <0.3 incidents of compliance (INCs) per inspection. (This is less than half the GoM 2022 YTD average of 0.64 INCs/inspection.)

Must operate at least 3 production platforms.

Must have drilled at least one well.

Pacific and Alaska operations will be considered in a separate post.

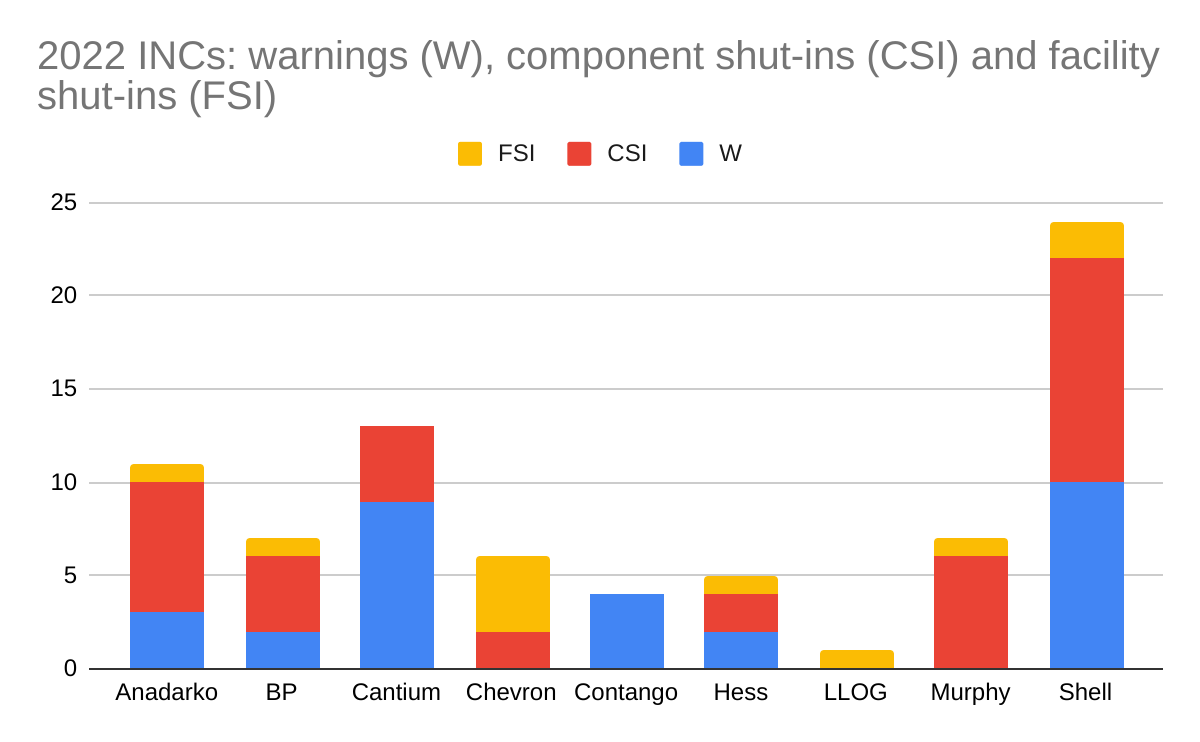

Comments:

Impressive performance by Hess: 21 inspections and no INCs

Cantium and Walter averaged less than 0.1 INCs/inspection. The INC rates for Anadarko (Oxy), BHP, and BP were only slightly higher.

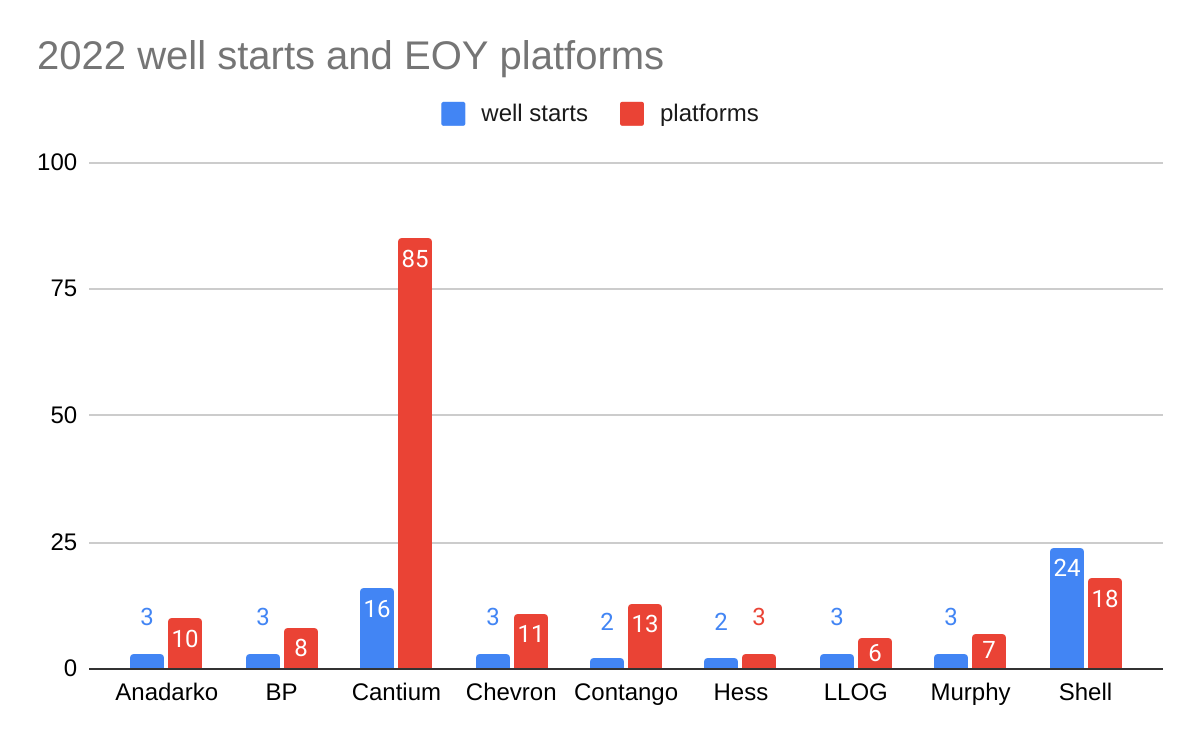

Among the Honor Roll companies, Shell (highest production, 9 deepwater platforms, and 13 well starts) and Arena (115 shelf platforms and 12 well starts) were the deepwater and shelf activity leaders.They thus had the highest INC exposure.

Although CSI and FSI INCs are typically more significant than W INCs, that is not always the case, so the INCs have not been weighted by type.

As has been previously noted, more inspection data should be readily available online. At a minimum, the specific INC (type) numbers (e.g. P-103, G-110, etc) should be posted so the public can better assess performance. Absent this information, interested parties are left to speculate about the significance of the violations.

While compliance is not synonymous with safety, most experienced observers believe there is a strong correlation. In the 1990’s, John Shultz, a PhD candidate at Carnegie Mellon Univ., studied US offshore facilities and safety data and developed expert and regression models to predict the likelihood of accidents and spills. That was a data rich era in that there were ~4000 US offshore platforms (more than twice the current number) and ~100 well starts/month (>10 times the current rate). In John’s thesis, he found that INCs are a very good predictor of accidents and spills. The offshore world has changed and further study of the correlation between compliance and safety performance is highly recommended.

Chevron may be the only GoM operator to own its helicopter fleet. Data on their safety performance relative to GoM helicopter contractors do not appear to be available online.

Their news release focuses on hurricane preparedness and the benefits of owning their fleet. I’m not sure how significant these advantages are given that other companies can ensure similar availability through their contracts. A comparative analysis would be of interest.

“Other companies that depend on contracted helicopters to evacuate can’t create their own schedule and might have to start departing the platform days in advance,” said Jose Jaramillo, manager of Chevron’s aircraft operations in the Gulf of Mexico. “With our own helicopters on standby, we have more flexibility in determining when to safely shut down the platform, and after the storm passes, we can quickly remobilize, assess our facilities and bring production back online days faster.”

The leading causes, not all inclusive, of the accidents since 1999 are listed below, and secondary causes of these events include 13 related to helideck size or design related issues. • 21 engine related, • 25 loss of control or improper procedures, • 18 helideck obstacle strikes, • 13 controlled flight into terrain, and • 12 other technical failures

Kudos to Mike Wirth. It’s nice to see a CEO with some backbone. Most importantly, he defended his employees and their vital contribution to society.

“Chevron and its 37,000 employees work every day to help provide the world with the energy it demands and to lift up the lives of billions of people who rely on these supplies. Notwithstanding these efforts, your Administration has largely sought to criticize, and at times vilify, our industry. These actions are not beneficial to meeting the challenges we face and are not what the American people deserve.”

The comment that follows is interesting. Perhaps he wants to hear from the Climate Policy Office?

“Chevron will engage in this week’s meeting with Secretary Granholm. I encourage you to also send your senior advisors to this meeting, so they too can engage in a robust conversation.”

Ballymore will be produced with 3 seafloor wells (6540′ water depth) that are expected to transport 75,000 bopd via a three-mile subsea tieback to Chevron’s Blind Faith floating production unit. Per BOEM, the Ballymore field was discovered in December, 2017. First production is expected to be in 2025.

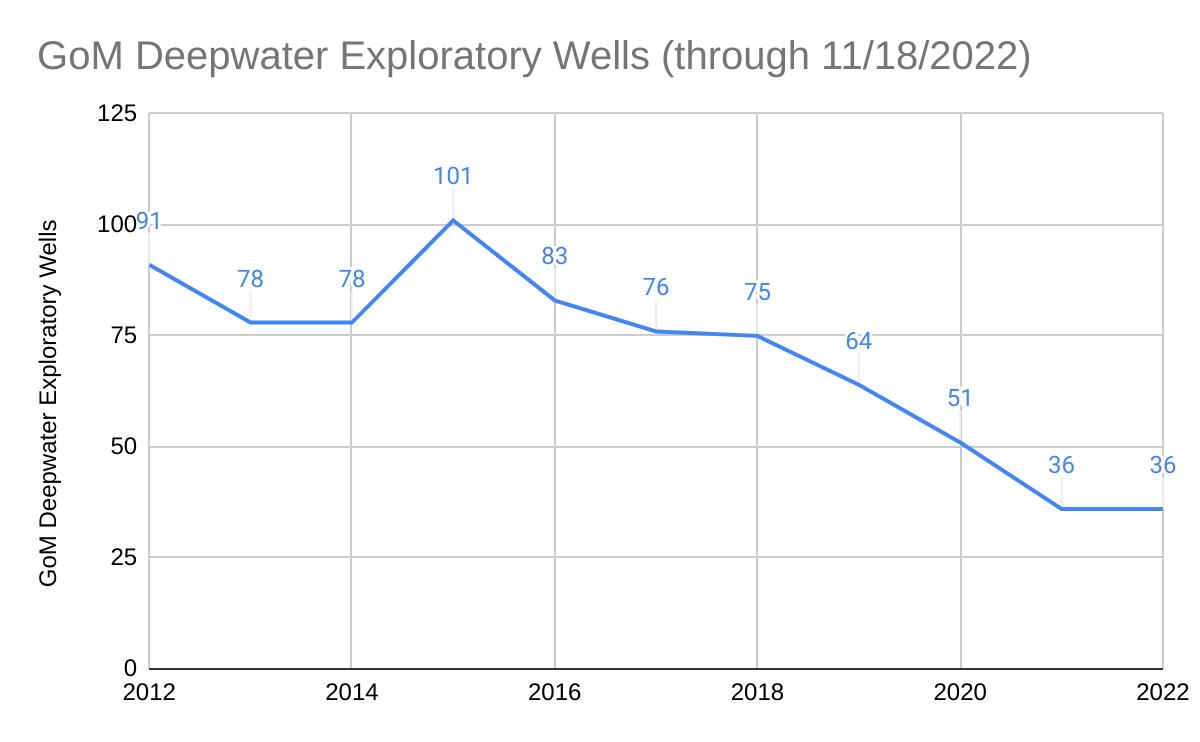

As these projects demonstrate, deepwater development takes time and is often dependent on related projects on other leases. This is why future production is dependent on regular, predictable lease sales.