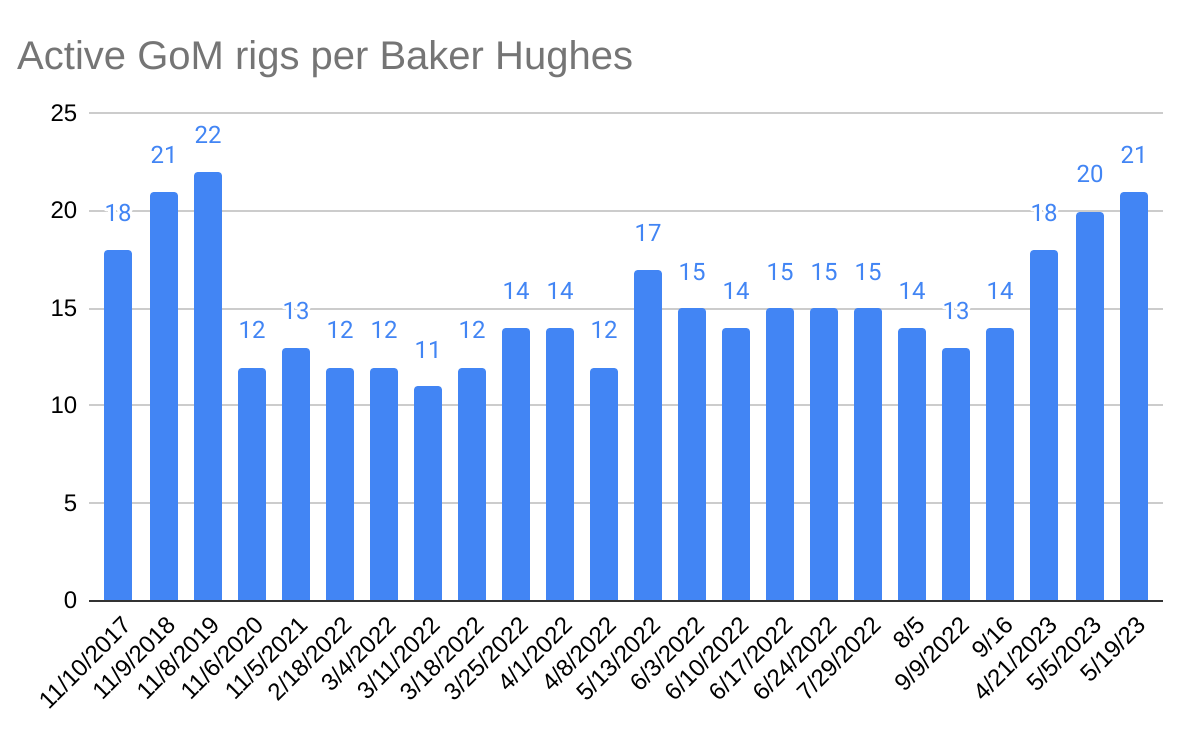

The latest Baker Hughes Rig Count Report shows only 10 rigs actively drilling in the Gulf. All are at deepwater locations – 7 in the Mississippi Canyon area, 2 in Green Canyon, and 1 in Alaminos Canyon. Per the BSEE borehole file, Shell accounts for most of the current MS Canyon wells and the Alaminous Canyon well. Beacon is also drilling in the MS Canyon, and the Green Canyon well appears to be a Chevron operation.

Only Anadarko/Oxy, Beacon/BOE, BP, Chevron/Hess, Shell, and Talos have spudded deepwater exploratory wells in 2025 YTD. Arena and Cantium are the only shelf drillers – all development wells.

Technological advances and extensions of past discoveries have sustained Gulf production, but declines are certain over the longer term if drilling activity doesn’t increase. Oil price uncertainty is an issue, but that’s always the case. Semiannual lease sales are now legislatively required and the terms will be attractive, so those issues are off the table. Let’s see what the bidding looks like at the upcoming sale.

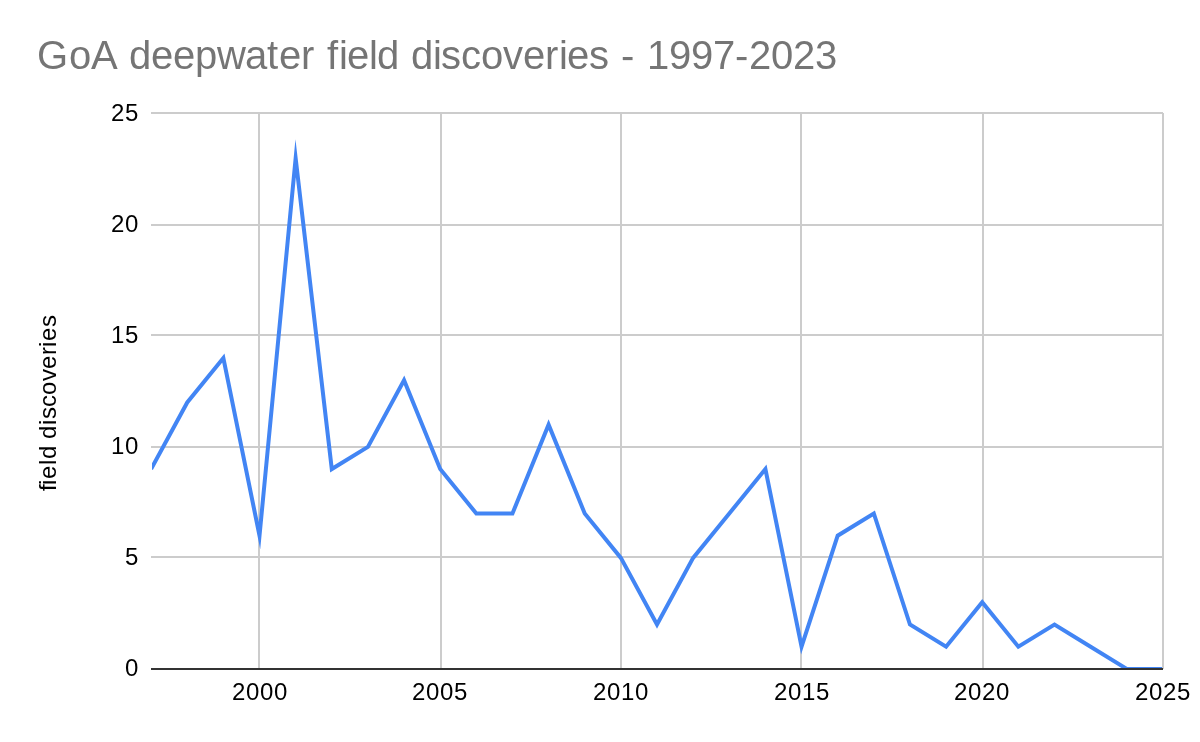

The decline in deepwater discoveries (BOEM data below) is particularly discouraging. Per BOEM, the last deepwater field discovery was in March 2023.

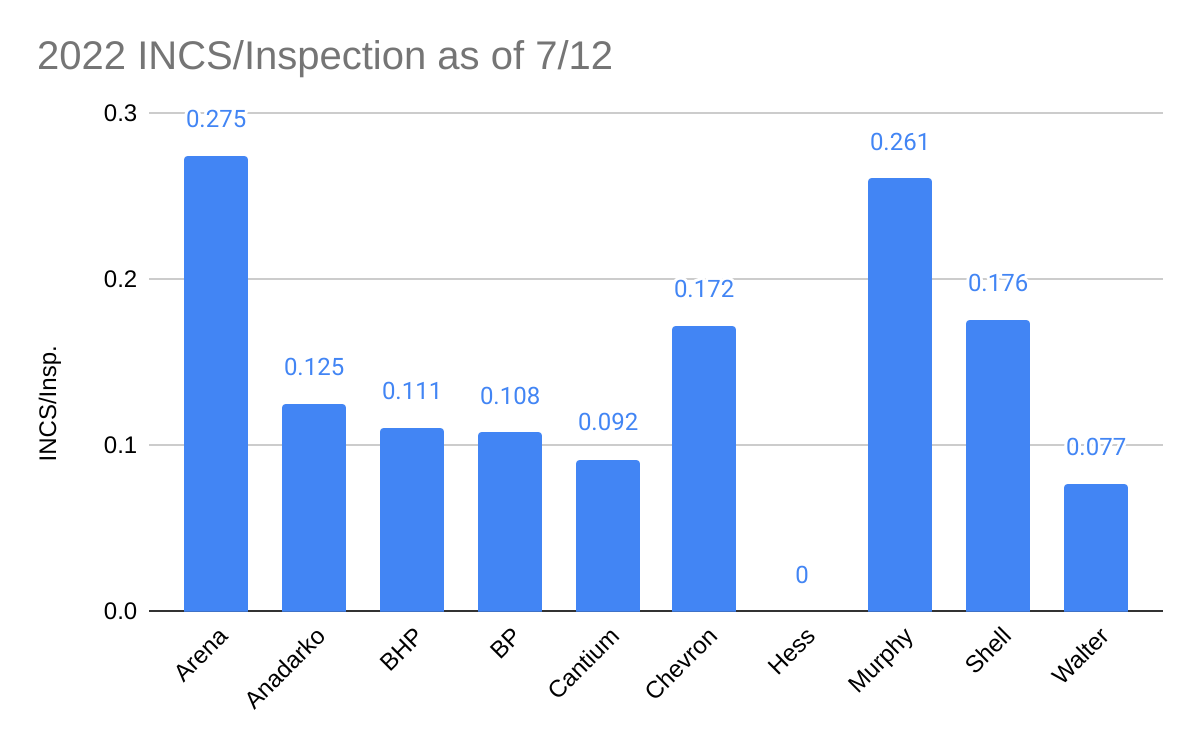

The 2024 Gulf of America Safety Compliance Leaders are ranked below according to the number of incidents of non-compliance (INCs) per facility inspection. To be ranked, a company must:

operate at least 2 production platforms

have drilled at least 2 wells during the year

average <1 INC for every 3 facility inspections (0.33 INCs/facility inspection)

average <1 INC for every 10 inspections (0.1 INCs/inspection). Note that each facility inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). In 2024, there were on average 3.4 inspections for every facility inspection.

District investigation reports are more timely and provide additional insights into safety performance. Impressively, Hess had no incidents warranting a District investigation, and was the only ranked operator with this distinction. I will comment more on the District reports in a future post

Chevron’s 2024 compliance record was among the best in the history of the US OCS oil and gas program. Was it the absolute best? Were it not for the FSI INC at a Unocal (Chevron) facility, one could unequivocally assert that it was. Further evaluation of that INC would be helpful. However, details on specific INCs are not publicly available, so the significance of that violation cannot be evaluated.

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

Chevron

1

0

1

2

117

0.02

311

0.006

BP

2

3

0

5

93

0.05

251

0.02

Anadarko

8

9

1

18

143

0.13

344

0.05

Hess

2

3

0

5

26

0.19

67

0.07

Walter

6

4

1

11

50

0.22

161

0.07

Shell

23

17

5

45

199

0.23

495

0.09

Cantium

24

8

0

32

123

0.26

537

0.06

Murphy

8

9

1

18

70

0.26

191

0.09

Arena

29

28

3

60

189

0.32

803

0.07

Gulf-wide

957

398

109

1464

3133

0.47

10664

0.14

Notes: Numbers are from published BSEE data; INC=incident of non-compliance; W=warning INC; CSI=component shut-in INC; FSI=facility shut-in INC; INCs/fac insp= INCs issued per facility inspection; each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc), in 2024, there were on average 3.4 inspections for every facility inspection

Not meeting the production facilities requirement to be ranked among the top performers, but nonetheless noteworthy, was the compliance record of BOE Exploration & Production (no relation to the BOE blog 😀). See their impressive inspection results below:

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

BOE

1

1

0

2

21

0.1

48

0.04

Transparency on inspections and incidents is important for a program that is dependent on public confidence. For independent observers to better evaluate industry-wide and company-specific safety performance, publication of the following information should be considered:

quarterly updates of the incident tables, as was once common practice

posting of violation summaries for inspections resulting in the issuance of one or more INCs

Per the BSEE borehole file, there were 2 deepwater exploratory well starts since 4/1/2023. The Shell well is another GoM milestone in that it is the 150th well spudded in >8000′ of water. The first was in the year 2000.

Operator

spud date

location

water depth

Chevron

5/5/2023

Mississippi Canyon 608

6678′

Shell

4/13/2023

Alaminos Canyon 728

8660′

Arena and Cantium continue to drive shelf drilling. Below are the shelf development wells since 4/1/2023:

Operating companies (listed alphabetically): Arena, Anadarko (Oxy), BHP, bp, Cantium, Chevron, Hess, Murphy, Shell, and Walter

Criteria:

Must average <0.3 incidents of compliance (INCs) per inspection. (This is less than half the GoM 2022 YTD average of 0.64 INCs/inspection.)

Must operate at least 3 production platforms.

Must have drilled at least one well.

Pacific and Alaska operations will be considered in a separate post.

Comments:

Impressive performance by Hess: 21 inspections and no INCs

Cantium and Walter averaged less than 0.1 INCs/inspection. The INC rates for Anadarko (Oxy), BHP, and BP were only slightly higher.

Among the Honor Roll companies, Shell (highest production, 9 deepwater platforms, and 13 well starts) and Arena (115 shelf platforms and 12 well starts) were the deepwater and shelf activity leaders.They thus had the highest INC exposure.

Although CSI and FSI INCs are typically more significant than W INCs, that is not always the case, so the INCs have not been weighted by type.

As has been previously noted, more inspection data should be readily available online. At a minimum, the specific INC (type) numbers (e.g. P-103, G-110, etc) should be posted so the public can better assess performance. Absent this information, interested parties are left to speculate about the significance of the violations.

While compliance is not synonymous with safety, most experienced observers believe there is a strong correlation. In the 1990’s, John Shultz, a PhD candidate at Carnegie Mellon Univ., studied US offshore facilities and safety data and developed expert and regression models to predict the likelihood of accidents and spills. That was a data rich era in that there were ~4000 US offshore platforms (more than twice the current number) and ~100 well starts/month (>10 times the current rate). In John’s thesis, he found that INCs are a very good predictor of accidents and spills. The offshore world has changed and further study of the correlation between compliance and safety performance is highly recommended.

Operating companies that produced >1 million bbls of oil or >1 BCF of gas in 2021 are listed in descending order based on oil production.

Both the total number of well starts and the number of exploratory wells are indicated

An INC is an Incident of Noncompliance (i.e. a violation). W=warning, CSI=component shut-in, and FSI=facility shut-in are the enforcement actions.

All of the below data are publicly available on the BSEE-BOEM websites.

2021 oil (MMbbls)

2021 gas (BCF)

2021/22 well starts total-expl

2021/22 INCs W-CSI-FSI

Shell

149.8

190.8

28-12

11-14-4

bp

114.0

82.7

5-2

6-3-4

Chevron

83.7

42.2

8-8

1-1-3

Anadarko (Oxy)

67.7

57.8

8-6

8-5-1

Hess

27.5

61.7

2-2

7-4-0

Murphy

25.1

50.0

7-7

4-8-1

LLOG

20.4

29.0

3-0

1-1-1

Talos

17.7

23.0

5-0

25-26-14

BHP

14.5

5.9

3-2

2-3-0

Exxon

13.2

2.3

–

1-1-1

Beacon

10.5

15.7

1-0

0-0-0

Fieldwood

10.4

24.7

–

685-235-91

EnVen

9.6

12.6

6-0

2-6-3

Kosmos

9.4

8.4

1-1

1-0-0

Arena

8.6

27.9

32-0

68-45-19

Walter

8.1

36.2

2-2

3-1-2

Cox

6.2

30.3

–

237-169-3

Eni

4.7

13.6

2-0

8-0-2

W&T

5.0

27.2

1-0

65-40-7

Cantium

4.5

5.5

18-0

23-15-2

QuarterNorth

4.2

8.3

–

no data

GoM Shelf

2.3

4.8

–

52-5-2

ANKOR

1.4

2.5

–

0-0-1

Byron

1.0

4.4

–

5-8-2

Renaissance

0.7

1.6

–

20-9-3

Sanare

0.3

4.5

–

38-20-3

Helis

0.2

1.2

–

1-0-2

Contango

0.03

5.0

–

4-0-0

Samchully

0.02

1.2

–

no data

Comments:

“Energy transition” companies Shell and bp still love the Gulf of Mexico, which is a good thing for them and us. Together they accounted for 42.4% of the 2021 oil production.

The top 4 producers, Shell, bp, Chevron (includes Unocal), and Anadarko accounted for 2/3 of GoM oil production, nearly all of which was from deepwater leases.

Those are impressive production numbers for Anadarko (Oxy). No wonder Warren Buffett likes Oxy stock.

The relative number of deepwater exploratory wells is mildly encouraging given our concerns about sustaining production.

Exploratory well determinations are rather subjective and may not be entirely consistent.

Understandably, no exploratory wells were drilled by Arena or Cantium, the companies responsible for most well operations on shelf (shallow water) leases.

Overall, the INC numbers are impressively low for the deepwater operators, with Chevron and LLOG standing out. BSEE does not post the specific violation information (more on this in an upcoming post), so it’s difficult to properly assess a company’s compliance record.

Unfortunately, incident data could not be included on the scoreboard. BSEE’s incident tables are badly out of date, and no 2021/2022 summaries have been posted.

Exxon production is limited to the Hoover Diana spar, which was installed 22 years ago. The largest US oil company has only drilled one GoM exploratory well (2018) in the past 5 years. Currently, their main GoM interest seems to be the sequestration (disposal) of onshore emissions. (More on this topic in an upcoming post.)