Among the top 10 companies at Sale 261 (based on the number of high bids) are household names Shell, Chevron/Hess, Oxy/Anadarko, and bp, and international majors Equinor (Norway) and Woodside (Australia).

Lesser known companies have also become important deepwater players including two, Red Willow (owned by the Southern Ute tribe) and Houston Energy, that cracked the top 10 bidders list. Other emerging deepwater companies, Ridgewood, CSL Expl, Westlawn, Alta Mar, and CL&F were also active sale 261 participants. All of these companies bid in partnership with other independents.

Company

257

259

261

Red Willow

5

13

25

Houston Energy

5

9

18

Ridgewood

0

2

8

CSL Expl

1

1

3

Westlawn

0

3

5

Alta Mar

0

0

9

CL&F

0

0

3

Number of bids by emerging deepwater players at Sales 257, 259, and 261.

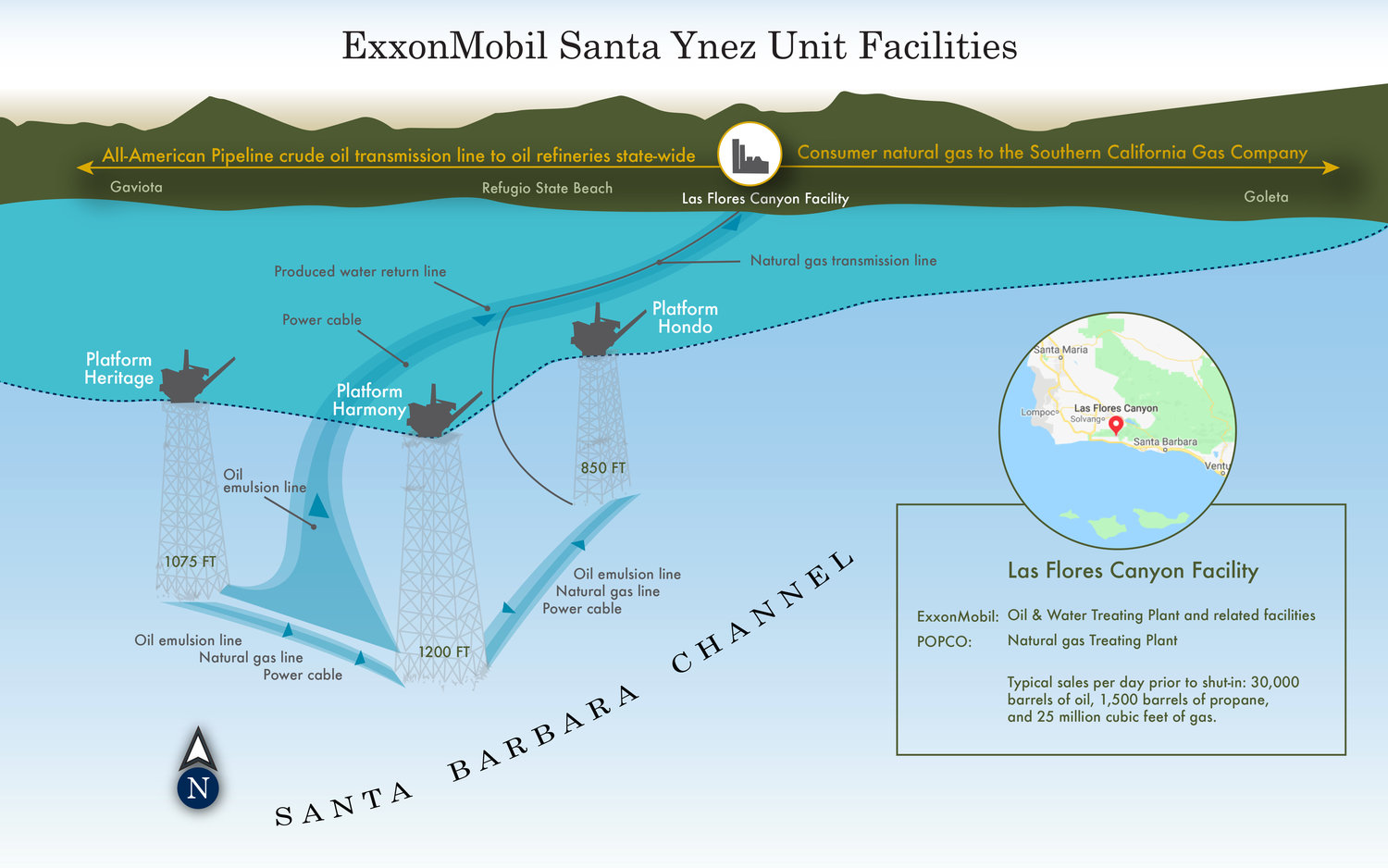

On December 7, 2023, the Bureau of Safety and Environmental Enforcement (BSEE) issued a Record of Decision (ROD) recommending the full removal of California’s 23 offshore oil platforms in federal waters, following a Programmatic Environmental Impact Statement (PEIS) conducted to assess decommissioning options for platforms, pipelines, and other related infrastructure. However, upon close review, the PEIS and ROD appear to have reached misguided and detrimental conclusions due to critical oversights in their analyses.

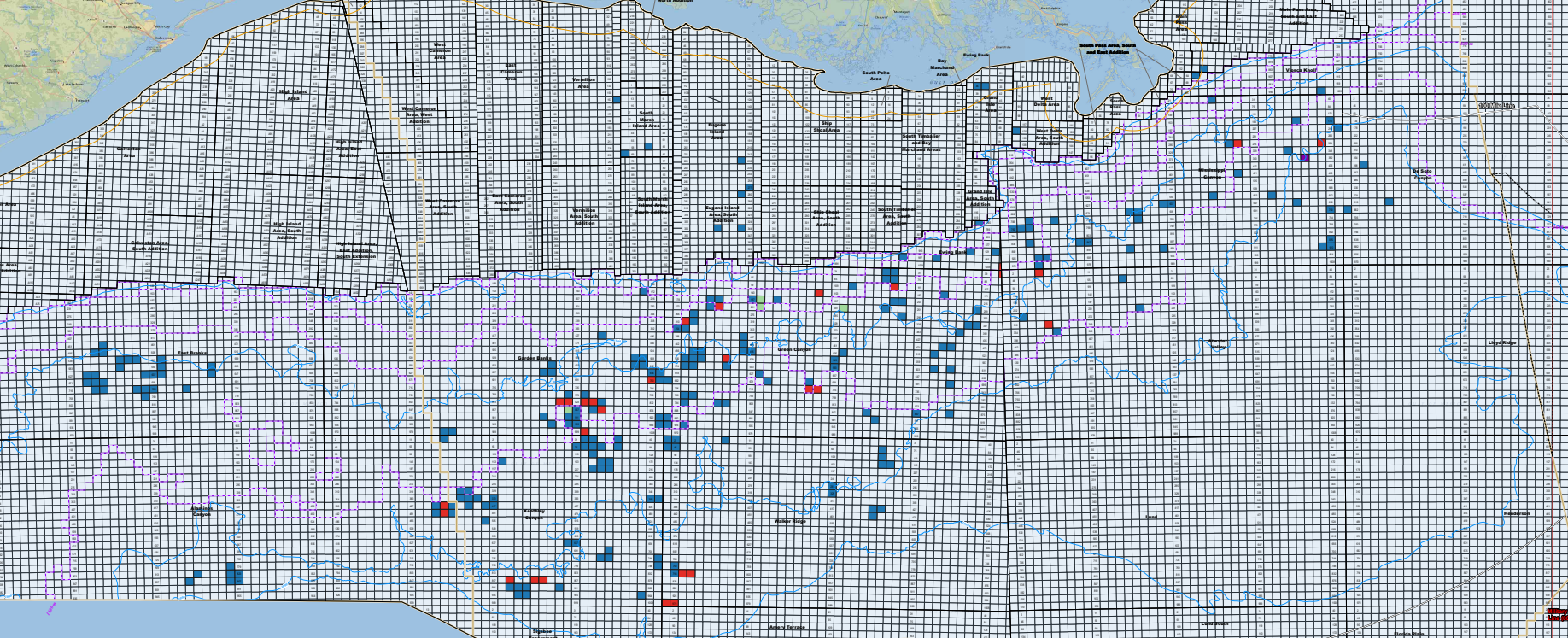

Sale 261: single bid tracts in blue, multi-bid tracts in red (2), green (3), and purple (5)

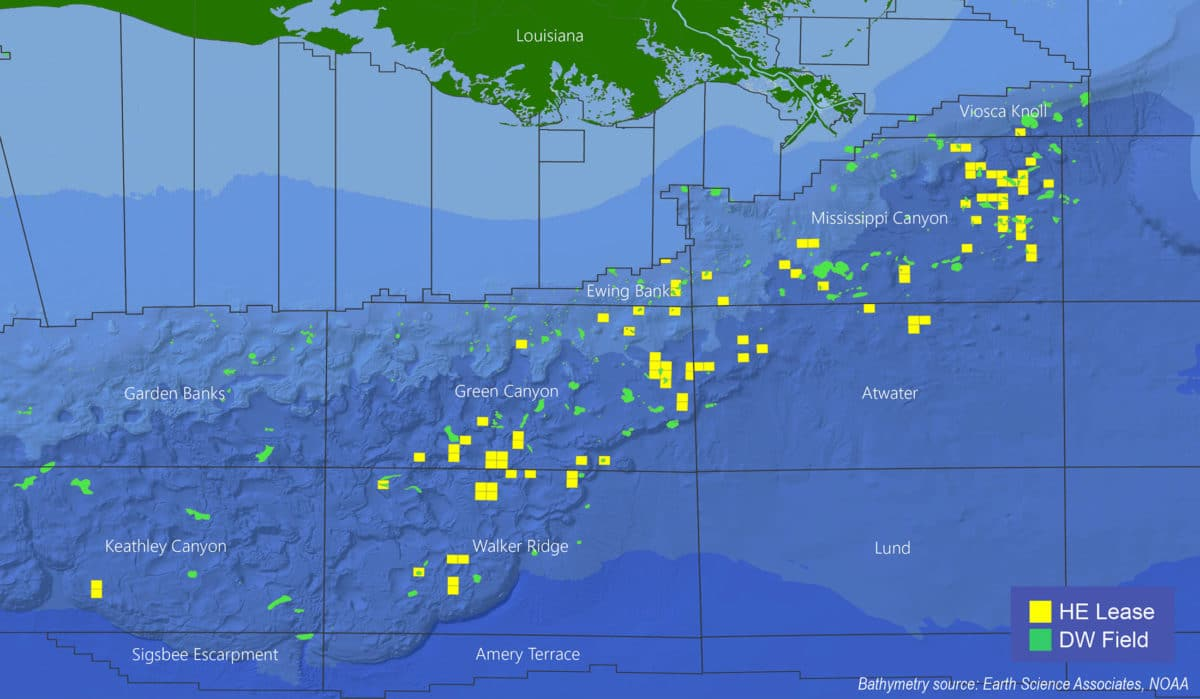

The interest of the majors and most independents has shifted entirely to deepwater prospects, as evidenced by the above graphic and sale data. Nonetheless, a few resourceful companies continue to find value in the shallow waters of the continental shelf.

“There’s an art to finding oil—particularly in the Gulf of Mexico. After decades of drilling, this world-class basin still holds vast potential for those skilled enough to unlock it. Arena energy is applying expert insight and advanced technology to identify new Gulf of Mexico oil and gas exploration opportunities. This is the art of oil finding in the 21st century.“

Arena Energy, a successful shelf operator for a quarter of a century, was the leading shelf bidder with 6 high bids. In 2023 Arena was once again the most active shelf driller with 20 well starts. They claim a 94% drilling success rate. Arena currently operates 123 platforms and is the GoM’s 7th ranked natural gas producer and the 11th ranked oil producer.

Cantium, another leading shelf operator, was the high bidder on 4 tracts. Cantium drilled 10 wells in 2023 and currently operates 86 platforms. Cantium claims to maintain “the highest level of operational safety and regulatory compliance by maximizing efficiencies and empowering employees,” and publicly available compliance data bear that out. Cantium was a BOE Honor Roll company for 2022, and a preliminary look at the data indicates that their 2023 performance was also excellent. Cantium is ranked 18th in both oil and natural gas production.

Byron Energy, which is headquartered in Australia, is the only international company investing in the GoM shelf. Byron was the high bidder on 2 tracts and currently operates 2 platforms. The company drilled 3 wells in 2023. Byron intends to continue focusing on the shallow waters of the Gulf.

Thoughts on the attributes of a successful shelf operator:

Bid alone and conduct operations independently to facilitate efficiency and timely decisions.

Lean and flat organizational structure for optimal communication and effective project management.

Skilled staff and state-of-the art exploration technology.

Outstanding contractor selection and oversight.

Safety, environmental, and compliance leadership, absent which your company won’t be around for long.

Think small. Gleaning old fields and producing modest new discoveries can be profitable!

Control growth and debt. Busts follow booms and highly leveraged companies are the most vulnerable.

Study the successful shelf operators and the failures. What did they do right and wrong?

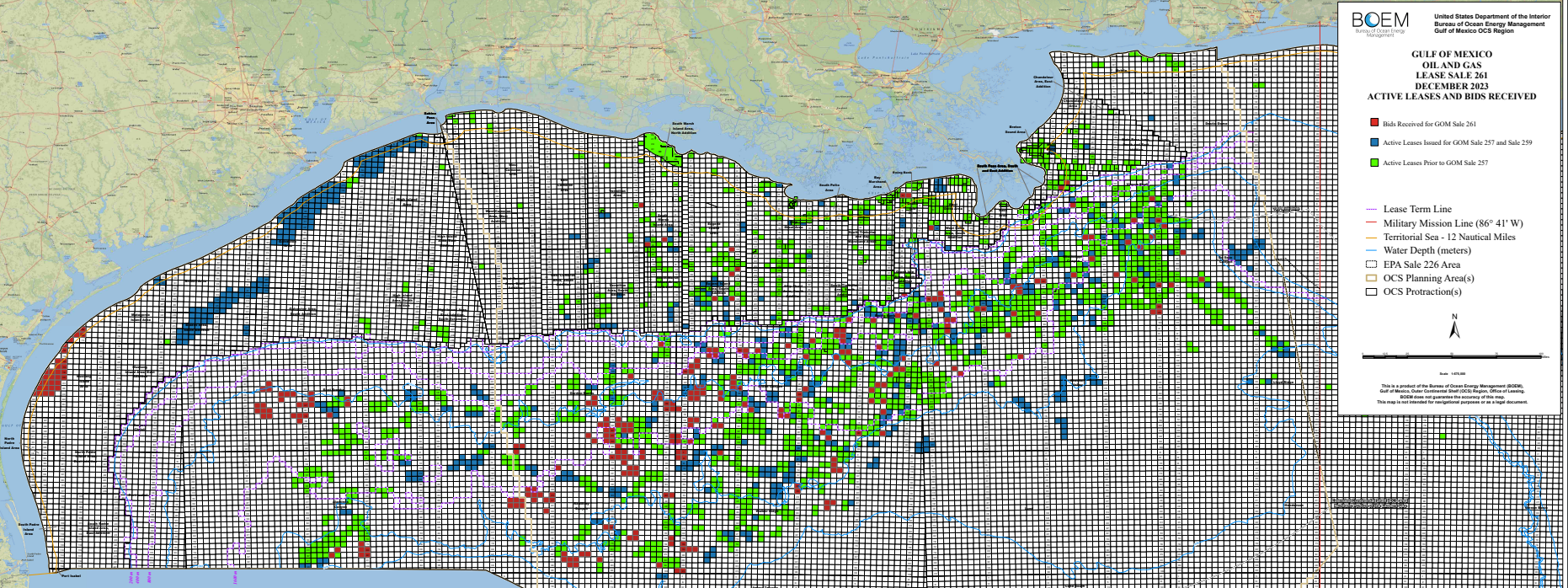

At Sale 261, Repsol was the sole bidder for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 and 259.

Why Repsol’s carbon disposal bids should be rejected (as Exxon’s Sale 257 and 259 bids should have been):

Sale 261 was an oil and gas lease sale. The Notice of Sale said nothing about carbon sequestration and did not offer the opportunity to acquire leases for that purpose. Therefore, the public notice requirements in 30 CFR § 556.308 were not fulfilled.

Because there was no draft or final Notice of Sale for sequestration (carbon disposal) leasing, interested parties did not have the opportunity to comment on tract exclusions, stipulations, bidding parameters, rental fees, royalties, and other factors pertinent to any OCS lease sale.

30 CFR § 556.308 requires publication of a lease form. No carbon sequestration lease form has been posted or published for comment.

Carbon sequestration operations were not considered in the environmental assessments conducted prior to this or any other OCS lease sale.

No evaluation criteria for carbon sequestration bids have been published.

Hopefully, the carbon sequestration regulations that are under development will preclude conversion of leases acquired at Sales 257, 259, and 261. At a minimum, these regulations should require a competitive process for converting any oil and gas leases.

The difference between the conversion of the Exxon and Repsol leases and the conversion of other existing oil and gas leases is that the Exxon and Repsol leases were acquired solely for the purpose of carbon disposal with no intention of oil and gas exploration and production. Also, they can conduct geophysical surveys on their extensive (arguably monopolistic) nearshore Texas lease holdings, which gives them an unfair competitive advantage should a carbon sequestration lease sale be held.

To their credit, Repsol bid legitimately on 9 oil and gas leases at Sale 261. Exxon did not participate in Sale 261, and their only participation in Sales 257 and 259 was for carbon disposal purposes. Prior to Sale 257, the company had not acquired an OCS lease since 2008.

The bankruptcy court’s priorities should be 1) minimizing safety and environmental risks and 2) protecting the public from the massive decommissioning liabilities.

Per the latest BOEM information, Cox and affiliates Energy XXI and EPL operate 477 platforms, which is 31% of the Gulf of Mexico total! (See the related information posted last June.) BSEE estimates that the decommissioning costs for these platforms will exceed $4.5 billion!

Per BSEE data, Cox and its affiliates were cited for 780 incidents of noncompliance (violations) in 2023. They thus accounted for 43% of all 2023 GoM INCs.

Questions:

How will taxpayers be protected from Cox’s $4.5+ billion decommissioning obligations?

What is the plan for both safely decommissioning facilities and operating those that remain?

Why was Cox allowed to continue expanding GoM operations without demonstrating financial assurance and operational competence?

How was a failing operator (Cox) selected just 8 months ago for a Federally funded (DOE) project to repurpose GoM facilities for carbon sequestration purposes?

The Cox bankruptcy is yet another costly lesson for Federal regulators. Moving forward, decommissioning and lease assignment policies must prioritize safety, environmental protection, and protection of the public’s financial interests.

On January 2, 2024, Chevron Corporation announced that for fourth quarter 2023, the Company will be impairing a portion of its U.S. upstream assets, primarily in California, due to continuing regulatory challenges in the state that have resulted in lower anticipated future investment levels in its business plans. The Company expects to continue operating the impacted assets for many years to come. In addition, the Company will be recognizing a loss related to abandonment and decommissioning obligations from previously sold oil and gas production assets in the U.S. Gulf of Mexico, as companies that purchased these assets have filed for protection under Chapter 11 of the U.S. Bankruptcy Code, and we believe it is now probable and estimable that a portion of these obligations will revert to the Company. We expect to undertake the decommissioning activities on these assets over the next decade.

OilNow has posted a good Guyana update. Production should reach 620,000 bopd in Q1 and grow to >1.2 million bopd in 2027/28. The growth in production is plotted below.

End of year data from gov.guyana for 2021-23. 2024 (Q1) and 2027 estimates are from OilNowMap shows locations of Exxon’s Guyana developments (current and planned)

Dr. Maurice (Mo) Stewart, an outstanding petroleum engineer, author, and teacher, passed away over the holidays after a long battle with ALS. Mo worked in the Office of Field Operations in the Gulf of Mexico Region of the US Geological Survey (which became part of the Minerals Management Service in 1982) while earning a PhD in Petroleum Engineering from Tulane University.

Mo specialized in production operations and the associated safety systems. He was the lead author of the production safety sections of the MMS operating regulations when they were completely revised in the 1980s. He authored or co-authored (with Ken Arnold) several textbooks and numerous technical papers on oil and gas processing. He was active on API technical committees and was a lecturer for the Society of Petroleum Engineers in the US and internationally.

Mo conducted training sessions for MMS staff at all levels of the organization. He was an outstanding speaker who spiced his presentations with anecdotes and slides from his many travels. His presentations were not just informative, they were highly entertaining!

After leaving MMS, Mo was an instructor and consultant in Indonesia, where he lived for some time, and throughout the world. His incredible life was brought to a sad end by an incurable disease. I’m grateful to have had the opportunity to work with such an outstanding engineer, dedicated safety professional, and all-around good guy. Bud

The 3rd quarter update by Jason Mathews and a followup inquiry confirm that there were no work-related fatalities associated with US OCS oil and gas operations in 2023! This major achievement deserves public recognition given that the zero fatality goal has long eluded offshore operators, contractors, and regulators.

In a proper safety culture, continuous improvement is the primary goal, and both good and bad outcomes must be carefully assessed. The 2023 zero-deaths milestone is thus tempered by life threatening incidents such as those described in the attached safety alert and investigation report. Address these issues, identify other potential problem areas, and continue to drive the culture forward. Be proud and confident through training, planning, and achievement, but be wary!