Minimizing flaring and venting is important from both environmental and resource conservation standpoints.Flaring and venting volumes are also good indicators of how well production systems are designed, managed, and maintained.

The best performance indicators are the percentages of produced gas that are flared and vented both for oil-well gas (OWG, also known as associated or casinghead gas) and gas-well gas (GWG or non-associated gas).

Updated flaring and venting volumes for the Gulf of America have been compiled using monthly data submitted to the Office of Natural Resources Revenue (ONRR). This is the best data source because reporting is mandatory and strictly enforced, and flaring and venting are accounted for separately.

In assessing performance trends, it’s important to segment venting and flaring volumes for both OWG and GWG production. Venting produced gas (mostly methane) is a more significant environmental concern from both air quality and greenhouse gas (GHG) perspectives.

Flaring and venting data for 2019-2024 are summarized in the table below. All volumes are in millions of cubic feet (MMCF).

Notes and comments:

The more disappointing 2024 numbers are entered in red. The blue numbers, all related to OWG venting, are encouraging.

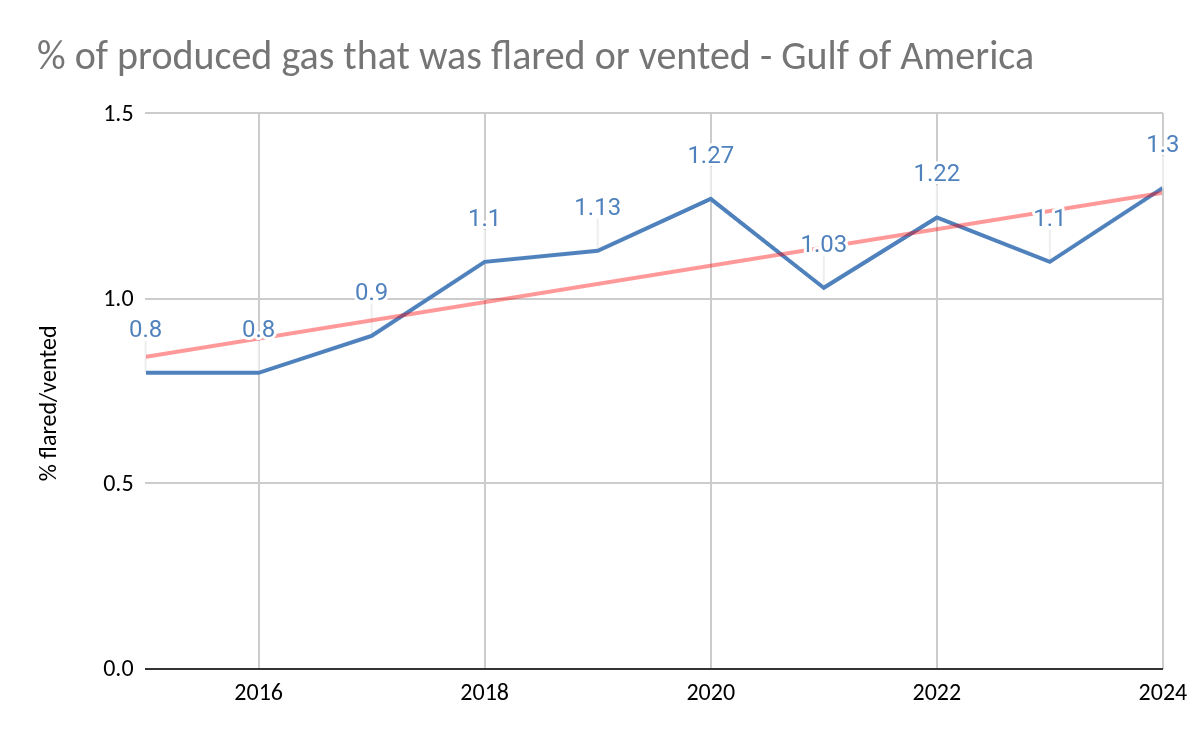

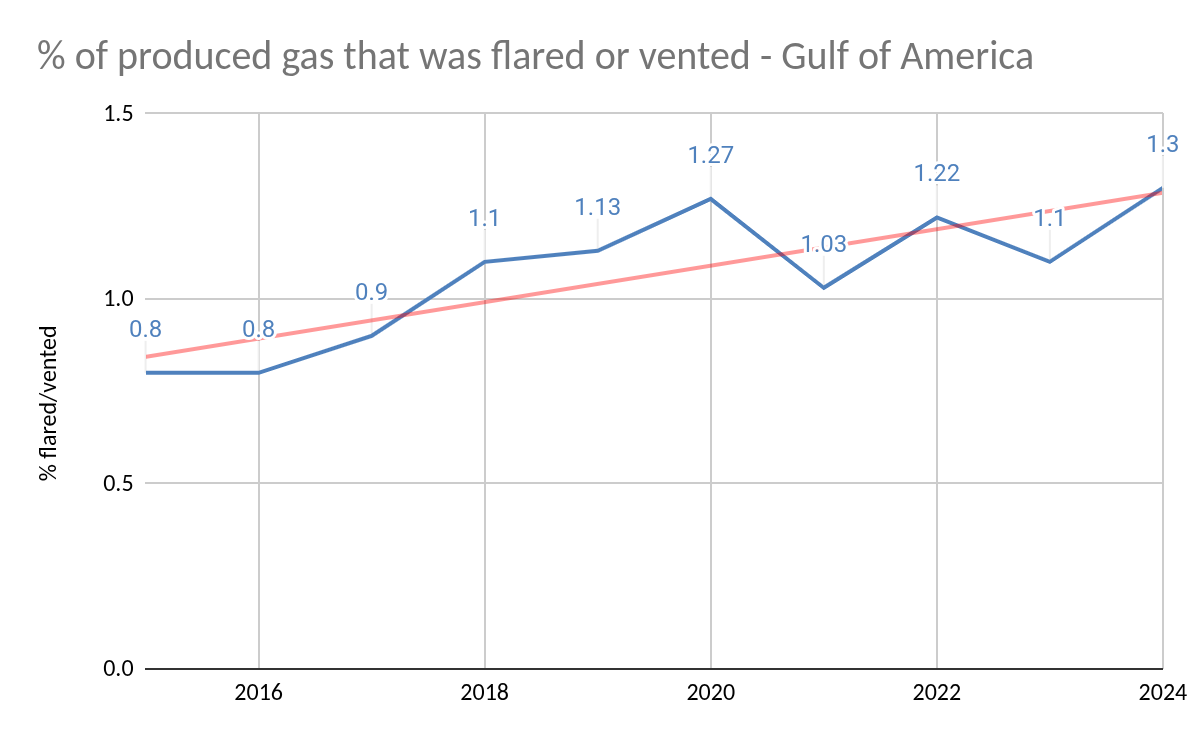

The % of all produced gas that was flared or vented in 2024 (1.3%) was the highest in the past 10 years (see the chart below the table). Until 2018, annual flaring/venting rates of <1% of production were commonly achieved. This should be the target going forward.

OWG flared increased significantly from 2023 levels, both in terms of the volume (7.26 billion cu ft) and the % of OWG produced (1.22%).

Production curtailments and restarts related to Tropical Storms Francine and Helene may have contributed significantly to the 2024 flaring increase. ONRR’s monthly reports show a near doubling of the average monthly flaring volume in Sept., when Francine and Helene shut-in 42% and 29% of oil production respectively. However, even if the Sept. flaring surge is normalized to the monthly average for the other 11 months, the total 2024 flaring still exceeds the 2023 volume by 361 MMCF.

The % of GWG vented in 2024 was the highest in the 6 year period and double the 2019, 2020, 2021 rates. Inefficiencies associated with the dramatic decline in GWG production, down 41.5% from 2023, may be a contributing factor.

The continued decline in OWG venting to only 0.16% in 2024 is encouraging. The decline should be sustainable given that most OWG is now produced at modern deepwater platforms equipped with efficient flare stacks.

Given the significance of these data, from safety, conservation, and environmental perspectives, a more comprehensive analysis by the offshore industry and regulators should be a priority.

As the chart indicates, the % of flared or vented Gulf of America gas production increased over the past 10 years. This trend is presumably due, at least in part, to the sharp increase in the % of gas production from oil wells (associated gas), which have a higher flaring rate. In 2024, 87% of Gulf gas production was from oil wells.

Flaring/venting summary tables and comments, updated through 2024, will be posted later in the week.

The Safety Alert is attached. Per BSEE, the fires resulted from an accumulation of gas caused by improperly installed or disconnected exhaust vent piping on gas starters.

Incident 1: Two workers sustained burns to the hands, arms, and face. BSEE investigators discovered that the engine’s air intake hose was disconnected, which may have allowed gas-enriched air to be drawn into the carburetor causing the backfire.

Incident 2: While attempting to start the gas engine of a pipeline pump, the lead mechanic sprayed ether into the engine’s carburetor. The exhaust vent piping for the starter had not been installed. The combination of the gas-rich atmosphere and ether caused the engine to backfire and ignited the accumulated gas. The lead mechanic, sustained burns to his face, arms, and hands.

The Alert includes important recommendations for proper venting, mechanical integrity awareness training, maintenance, and the use of gas detectors and a temporary fire watch during engine startup.

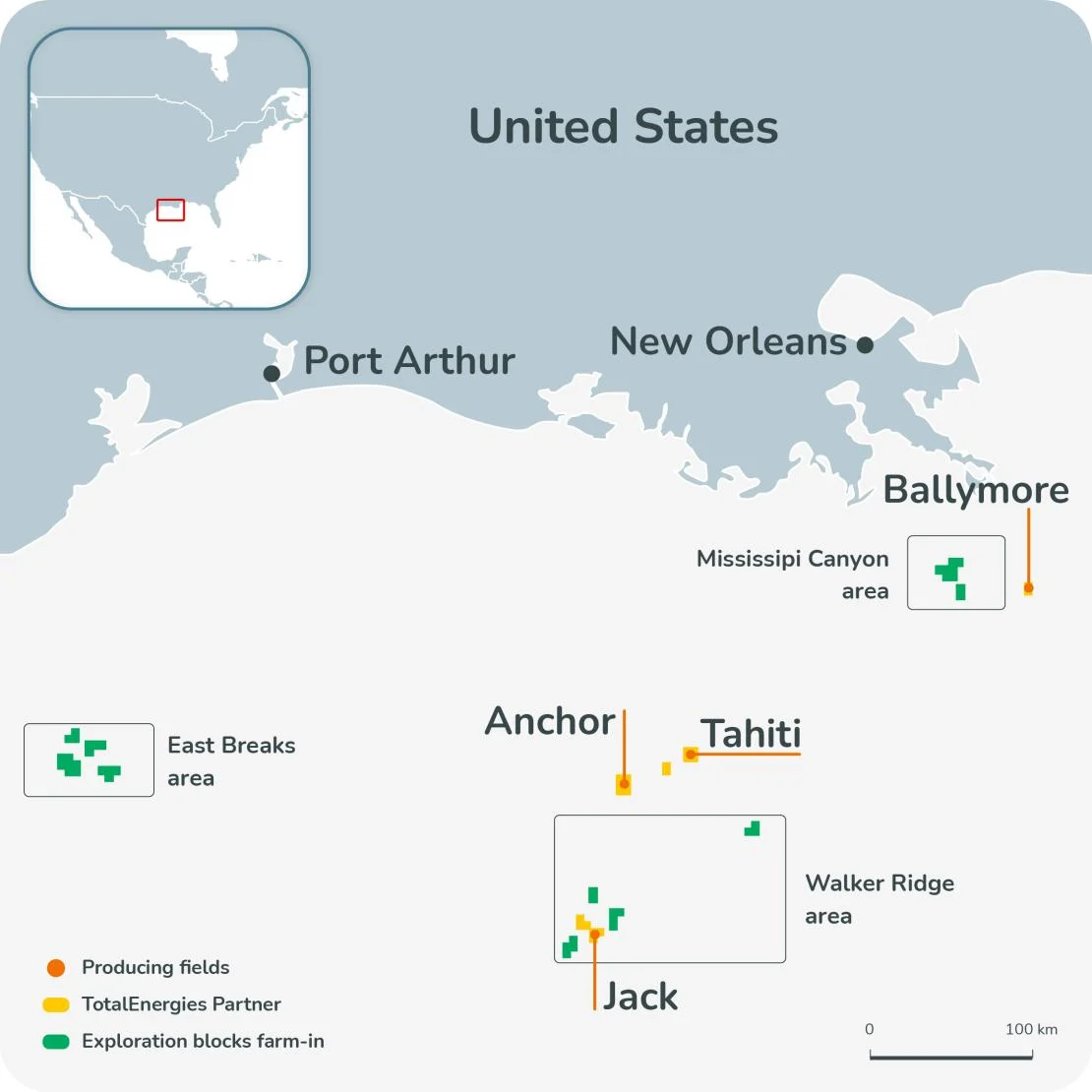

This week Total announced the acquisition of a 25% working interest in 40 Chevron leases in the Gulf of America. Total already owned interest in Chevron’s producing Ballymore (40%), Anchor (37.14%), Jack (25%), and Tahiti (17%) fields. Ironically, Federal regulations prohibited Total from jointly bidding with Chevron for any of those leases at the time of the sales. How does that make sense?

Total did not submit a single bid in any of the past 4 Gulf of America lease sales. Perhaps they prefer to acquire interest in blocks previously leased to companies like Chevron. That is a reasonable acquisition strategy. However, farm-in acquisitions yield no bonus dollars to the Federal government. Wouldn’t it have been in the government’s best interest if some of those acquisition dollars were spent at lease sales where the bonus bids go to the US Treasury?It’s long past time to remove the joint bidding restrictions!

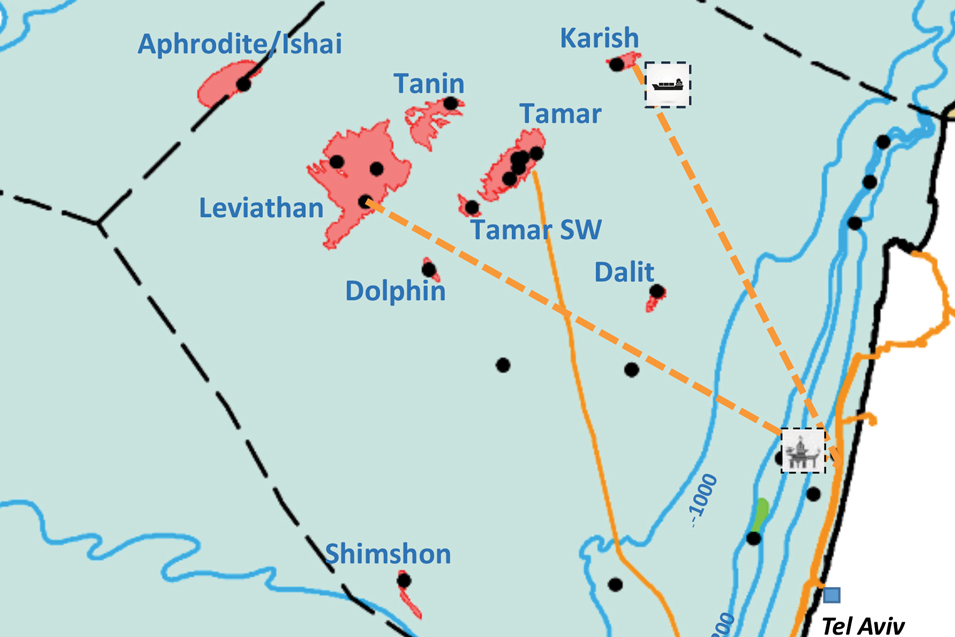

Two of Israel’s three offshore gas fields are shut-in as a precaution. As a result, exports to Egypt and Jordan has been curtailed. The Tamar field continues to supply Israel’s gas needs.

Summary table:

field (operator)

2024 production (billion cubic meters) (% of Israel’s total)

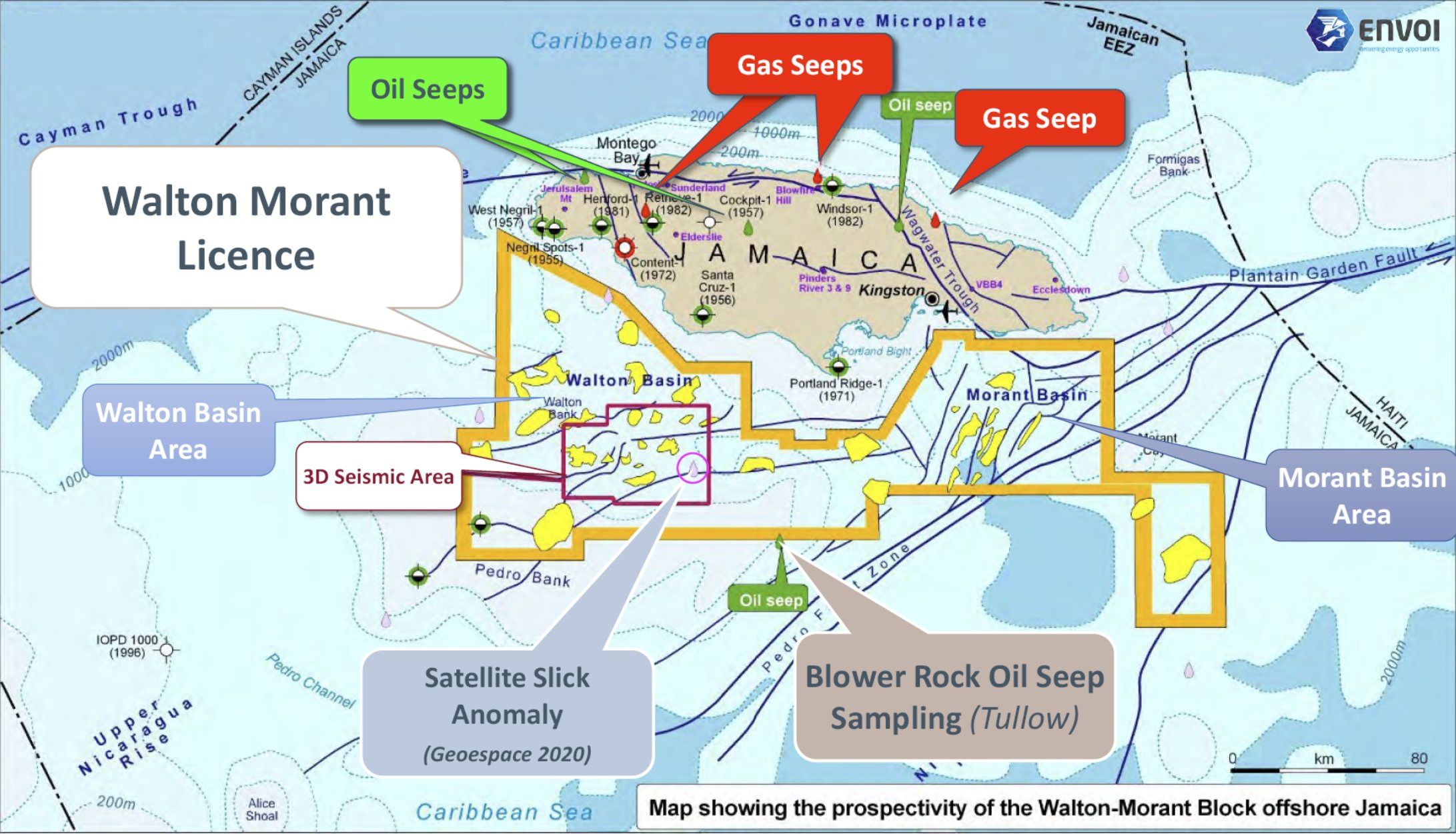

While Jamaica’s Walton Morant Block has impressive potential, that doesn’t equate to oil and gas reserves, and speculation about the “next Guyana” is highly premature.

The block’s licensee, United Oil & Gas (UOG), lacks the financial resources to fulfill its drilling commitment, and is thus dependent on finding industry partners. The Government of Jamaica has generously granted multiple license extensions to UOG, the latest through 1/31/2028.

Will UOG succeed in their quest for partners? Is the confidence expressed below justified? Stay tuned.

#UOG CEO Brian Larkin: “We’re in the best position yet — interest is real, and it’s backed by evidence provided to our NOMAD.”

🔹Hydrocarbon shows in all 11 historical wells confirm an active petroleum system 🔹Licence secured through to January 2028 pic.twitter.com/dfogPhpCnH

— United Oil & Gas (LON:UOG) (@UOGPLC) June 12, 2025

🔹 7Bn bbl potential — same source rock & economics as Exxon's Stabroek 🔹 $8/bbl dev. cost | $25/bbl break-even 🔹 Comparable to Guyana & Namibia — but Jamaica remains wide open for entry 📈 Scale like this is rare pic.twitter.com/ZfQda5DQ5Q

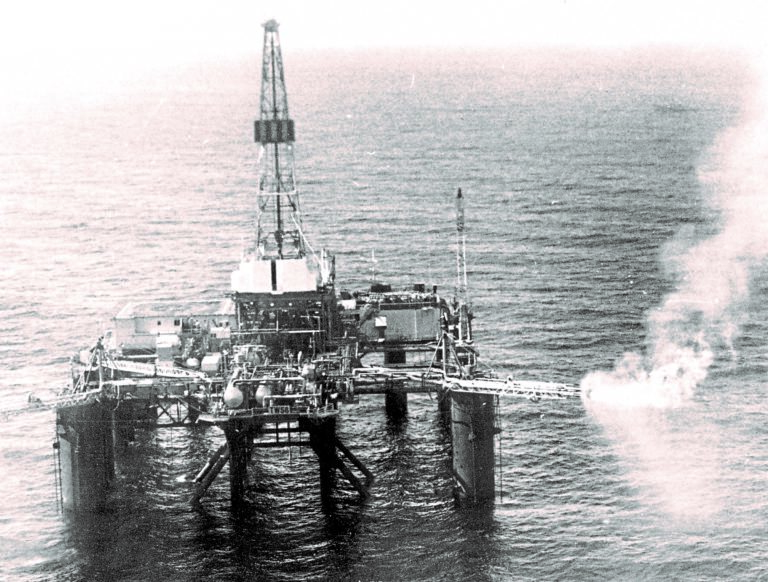

Argyll first productionQueen Elizabeth inaugurates the Forties fieldQueen Elizabeth: a day of “outstanding significance in the history of the United Kingdom” and a “critical milestone in the development of our energy resources.”

JL Daeschler recalls the inauguration of production at the Argyll field (18 June 1975) and Forties field (3 Nov 1975):

While some were bitter that Hamilton Brothers, a company owned by 2 brothers from Denver, was able to start production before British giant BP, there was never a race between the companies.

Instead there was a broad industry effort to initiate production during a financial crisis.

All operators exercized caution. We learned slowly with safety in mind. There was a great transfer of knowledge between operators small and big.

BP’s Forties field was a major achievement – designed for 400,000 bopd. 240 miles of 36″ pipeline were required (110 miles offshore and 130 miles onshore). The biggest delay was associated with the pipeline system, not the platform or wells.

The Hamilton Brothers Argyll field project (30,000 bopd) was not comparable in magnitude, requiring only a few wells and short infield flowlines.

The inauguration of Argyll (photo above) was with the UK Energy Minister, Ferris and Fred Hamilton, and a Greek tanker captain. There was minimal promotion and PR followup.

Contrast that with the Forties inauguration (photo above), a big event featuring Queen Elizabeth!

Converted semi-submersible initiates production at the Argyll fieldin the UK sector of the North SeaBritish Secretary of State for Energy Tony Benn, center, with Frederic Hamilton and Captain Harry Koutsoukos opening a valve to release the first oil from the North Sea into the BP refinery on the Isle of Grain in 1975.

Congratulations to JL Daeschler and other North Sea pioneers!Your important contributions to the UK and the world have not been forgotten.

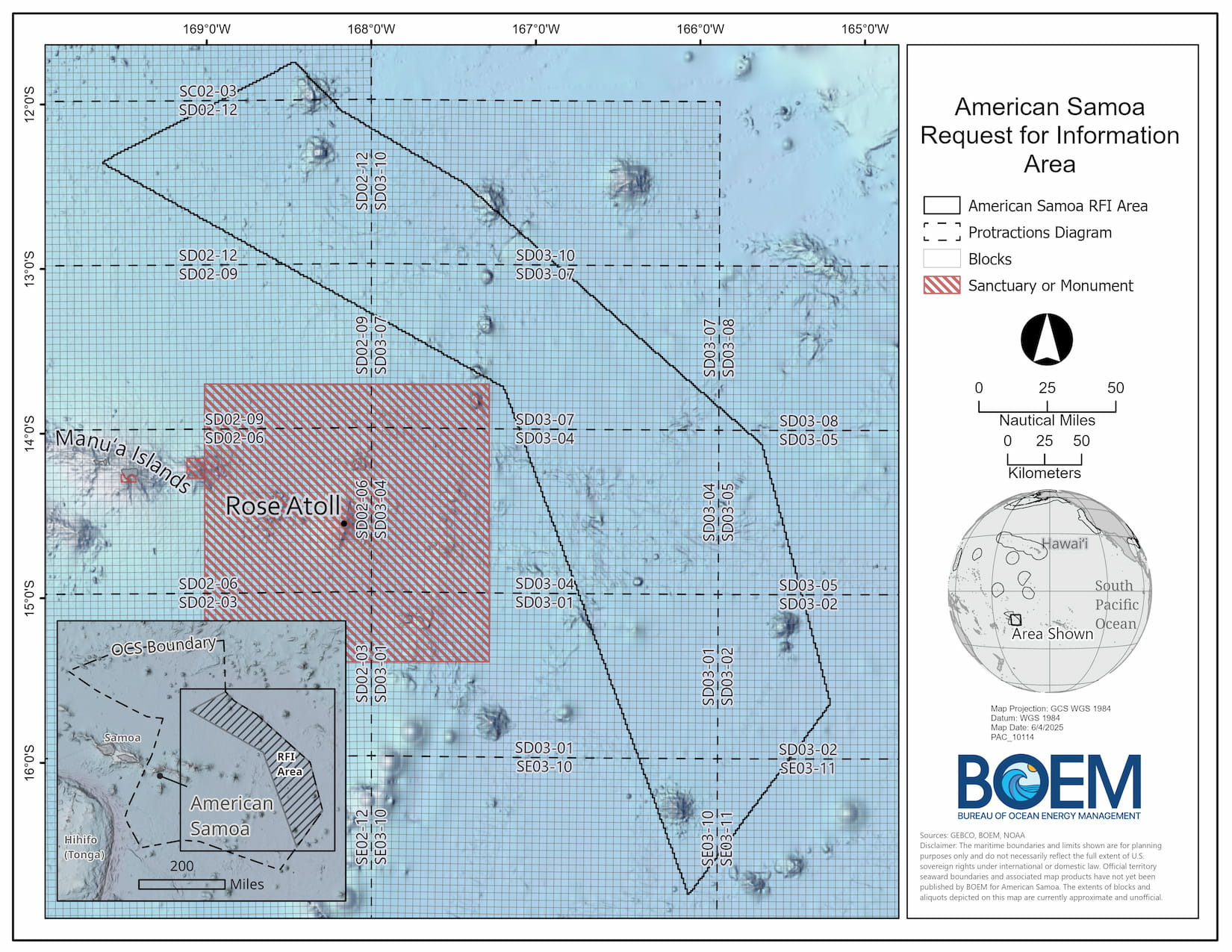

For those who want to provide input on an American Samoa marine minerals sale, now is your chance. See the attached Request for Information and Interest.

Iranian media reports a “massive explosion” following an Israeli drone strike on the South Pars gas field in the southern port city of Kangan. According to a 2019 report, the field accounts for 74 per cent of the country’s gas production.

Judging by available video (below), it appears that onshore processing facilities were struck and not the offshore infrastructure.

Israeli forces reportedly struck Iran’s South Pars Phase 14 refinery, one of the world’s largest natural gas extraction facilities. pic.twitter.com/d94SdIJC0I