Regulatory fragmentation occurs when multiple federal agencies oversee a single issue. Using the full text of the Federal Register, the government’s official daily publication, we provide the first systematic evidence on the extent and costs of regulatory fragmentation. We find that fragmentation increases the firm’s costs while lowering its productivity, profitability, and growth. Moreover, it deters entry into an industry. These effects arise from regulatory redundancy and, more prominently, regulatory inconsistency between agencies. Our results uncover a new source of regulatory burden: companies pay a substantial economic price when regulatory oversight is fragmented across multiple government agencies.

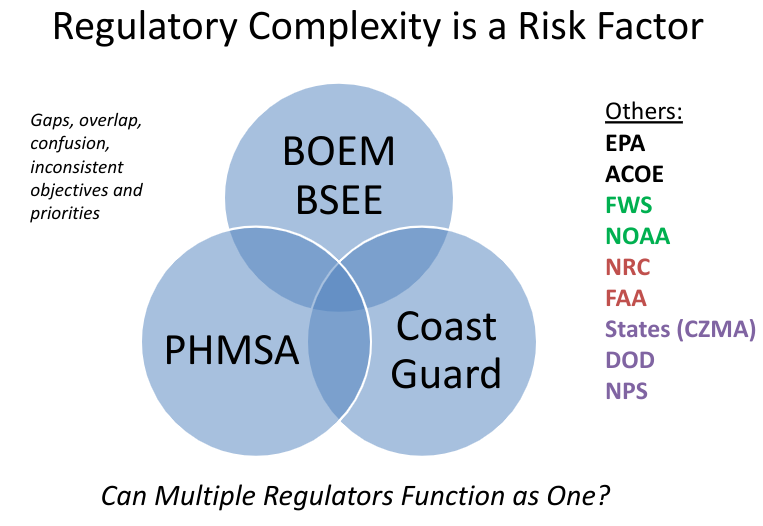

The US has a highly fragmented offshore regulatory regime that has become even more fragmented with the complex division of responsibilities between BOEM and BSEE. The slide below is from a presentation on this topic.

While the linked paper focuses on costs and productivity, fragmentation may also be a significant safety risk factor. A UK colleague once asseted that “overlap is underlap,” and I believe there is something to that. If multiple agencies have jurisdiction over a facility, system, or procedure, the resulting redundancy, inconsistency, and ambiguity may create significant gaps in industry and governmental oversight.

For example, regulatory fragmentation was arguably a significant factor in the most fatal US offshore fire/explosion incidents in the past 35 years – the South Pass B fire in 1989 and the Macondo blowout in 2010. More specifically:

South Pass 60 B: The investigation of the 1989 South Pass 60 B platform explosion that killed 7 workers noted the inconsistency in regulatory practices for the platform, regulated by DOI, and the pipeline regulated by DOT. Cutting into the 18-inch pipeline riser did not require an approved procedure, and the risks associated with hydrocarbon pockets in the undulating pipeline were not carefully assessed. Oversight by the pipeline operator was minimal, and the contractor began cutting into the riser without first determining its contents. A massive explosion occurred and 7 lives were lost.

One would hope that this major spill will lead to an independent review of the regulatory regime for offshore pipelines. Consideration should be given to designating a single regulator that is responsible and accountable for offshore pipeline safety (a joint authority approach might also merit consideration) and developing a single set of clear and consistent regulations.

Macondo: While the root causes of the Macondo blowout involved well planning and construction decisions regarding the casing point, cementing of the production casing, and well suspension procedure, the blowout would likely have been at least partially mitigated (and lives saved) if the gas detection system was fully operable, the emergency disconnect sequence was activated in a timely manner, flow was automatically diverted overboard, or engine overspeed devices functioned properly. Indeed, regulatory overlap led to underlap as summarized below:

Macondo contributing factor

jurisdiction

flow not automatically diverted overboard

DOI/USCG (also concerns about EPA discharge violations)

some gas detectors were inoperable

DOI/USCG

generators did not automatically shutdown when gas was detected

USCG/DOI

failure to activate emergency disconnect sequence in a timely manner (training deficiencies and chain-of-command complications)

USCG/DOI

engine overspeed devices did not function

USCG/DOI

hazardous area classification shortcomings

USCG/DOI

MOUs and MOAs are seldom effective regulatory solutions as they are often unclear or inconclusive, and tend to be more about the interests of the regulator and protecting turf. They also do nothing to ensure a consistent commitment among the regulators. In the case of the US OCS program, BOEM-BSEE have a greater stake in the safety and environmental outcomes given that offshore energy is the reason for their existence. That is not the case for any of the other regulators identified in the graphic above.

Oil and Energy Minister Terje Aasland takes over the constitutional responsibility for the Petroleum Safety Authority with effect from 11 May 2023. Labor and Inclusion Minister Marte Mjøs Persen previously held responsibility. With this, the government wishes to strengthen comprehensive and good management of HSE, safety and preparedness on the Norwegian continental shelf.

The transfer of responsibility to the Ministry of Oil and Energy (OED) is in line with the main principle in Norwegian administration that one ministry and one cabinet minister have the constitutional responsibility for the sector as a whole.

The Petroleum Safety Authority and the Norwegian Petroleum Directorate, the resource management agency, now report to the same ministry. Prior to a December 2003 decree that established the PSA, both the safety and resource functions were administered by the NPD.

Could this be the start of a trend toward better coordination of regulatory and resource management functions? If so, that would be a positive development. Fragmented oversight is neither in the best interest of safety nor resource management. (More on this in an upcoming post.)

There are a number of recent articles related to the Guyana Supreme Court ruling on Exxon’s financial assurance obligations. An Oil Now piece (quoted below) is the most informative. It seems that the Supreme Court decision is based on a provision of Exxon’s EPA permit and that EPA is siding with Exxon in this dispute.

The Guyana government and the Environmental Protection Agency (EPA) are set to appeal a recent Guyana Supreme Court ruling that determined that the EPA and ExxonMobil affiliate, Esso Exploration and Production Guyana Limited (EEPGL), breached the terms of the Liza 1 environmental permit. The permit was revised and granted to EEPGL last year for operations in the Stabroek Block, offshore Guyana.

Justice Sandil Kissoon granted several declarations, including that the EPA failed to enforce compliance by EEPGL of its Financial Assurance obligations to provide an unlimited Parent Company Guarantee Agreement and/or Affiliate Company Guarantee Agreement to indemnify and keep indemnified the EPA and the Government of Guyana against all environmental obligations of the Permit Holder (EEPGL) and Co-Venturers (Hess and CNOOC) within the Stabroek Block.

While acknowledging the court’s ruling, the Government of Guyana, as a major stakeholder, maintained in a statement that the Environmental Permit imposes no obligation on the Permit Holder to provide an unlimited Parent Company Guarantee Agreement and/or Affiliate Company Guarantee Agreement. The government believes that Justice Kissoon erred in his findings and that the ruling could have significant economic and other impacts on the public interest and national development.

Unlimited liability is a rather daunting and open-ended obligation that would trouble permittees in any industry.

In the US, the liability for oil spill cleanup costs is unlimited for offshore facilities, but there is a liability cap for the resulting damages. That cap is currently $167.8 million after a recent inflation adjustment. BP, of course, paid far more than that for damages associated with the Macondo blowout. BP’s costs, which amounted to an astounding $61.6 billion, were both voluntary and compulsory as a result of agreements and settlements. Keep in mind that the damage liability limit was only $75 million at the time. One can imagine what would have happened if a company with less financial strength or more inclination to fight had been responsible for the spill.

Dr. Malcolm Sharples, a leading marine engineer and offshore safety advocate, brought this Supreme Court’s decision and the resulting regulatory confusion to my attention.

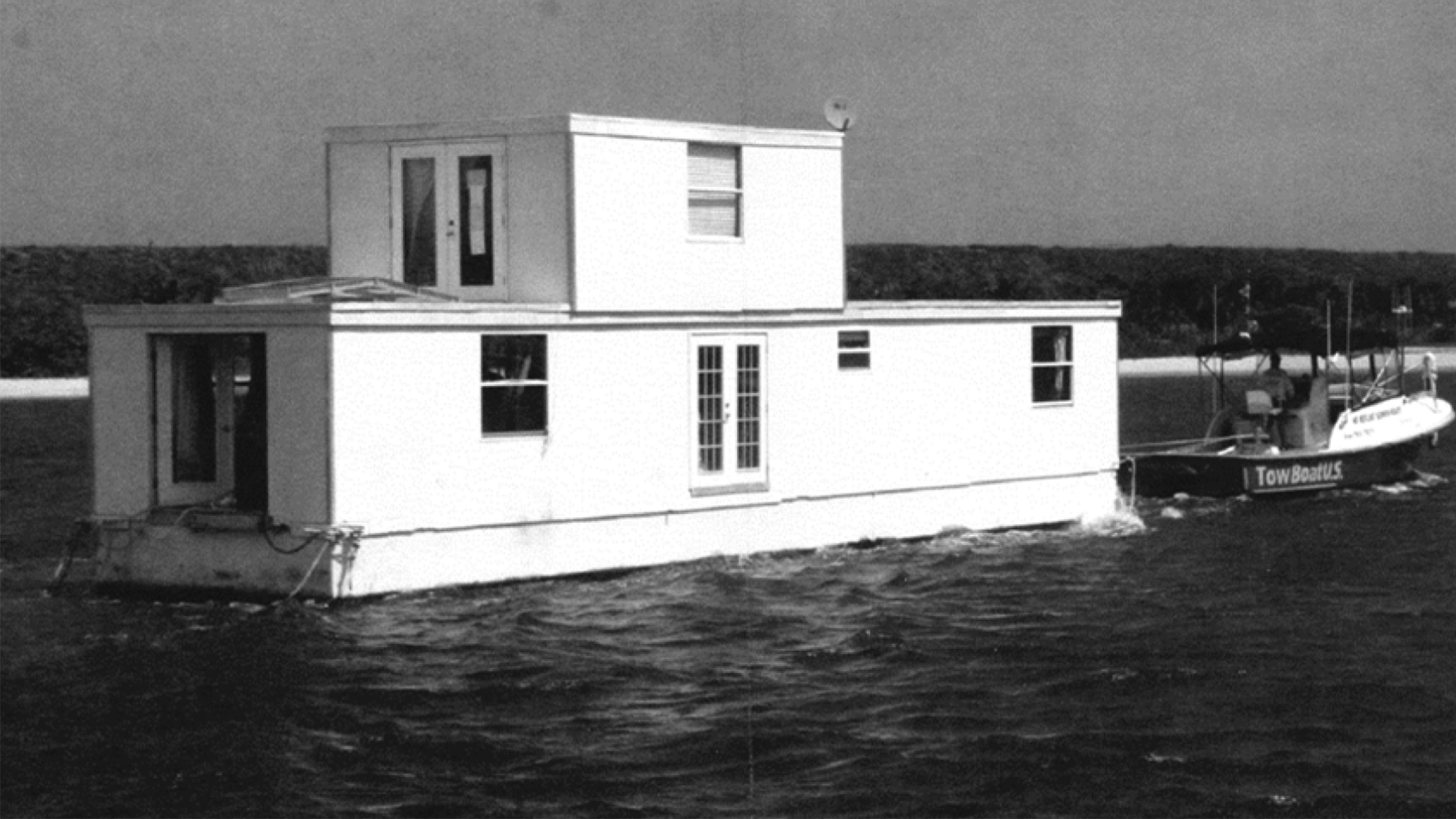

has created regulatory uncertainty for floating production facilities like this:

In a 7-2 decision, the court ruled that a gray, two-story home that its owner said was permanently moored to a Riviera Beach, Florida, marina was not a vessel, depriving the city of power under U.S. maritime law to seize and destroy it.

The floating production facilities are still subject to Coast Guard regulation and inspection pursuant to separate authority under the OCS Lands Act. The extent to which Coast Guard approval and inspection practices will change is not entirely clear. The Coast Guard will issue new certificates of inspection for these floating facilities, and new policy guidance is being developed.

Attached are answers that the Coast Guard provided to questions from the Offshore Operators Committee.

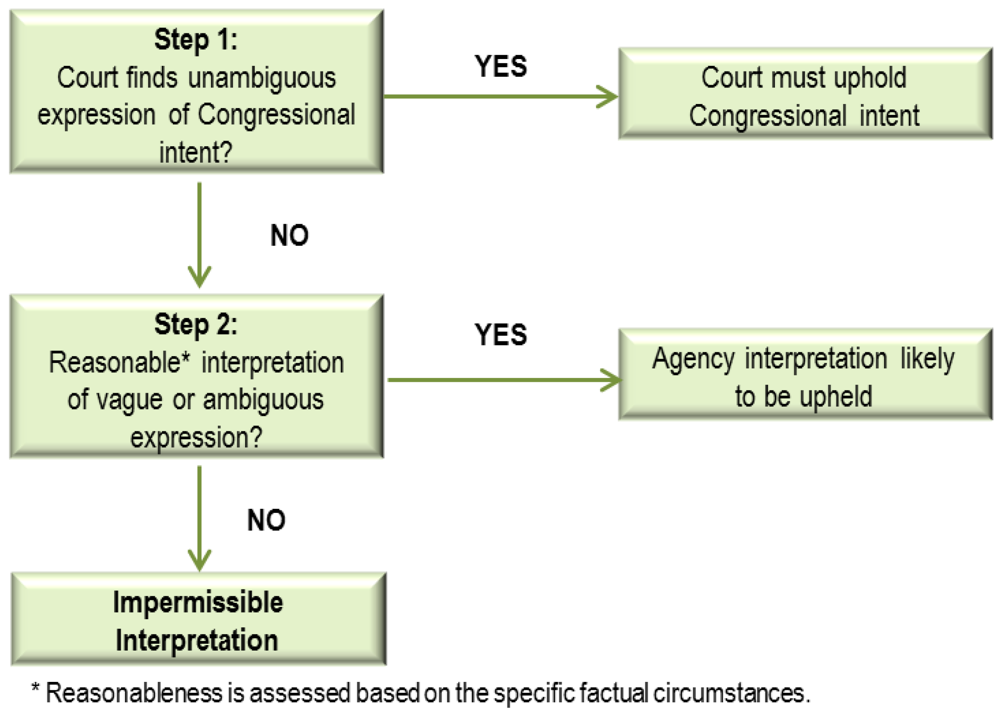

The Supreme Court will hear a case that could significantly scale back federal agencies’ authority, with implications for regulations affecting the US offshore program. The court could overturn a precedent known as the “Chevron doctrine” that instructs judges to defer to federal agencies when interpreting ambiguous federal laws.

Few Supreme Court doctrines have been stretched more by regulators and lower-court judges than Chevron deference, which says judges should defer to regulators’ interpretations when laws are supposedly ambiguous. The High Court agreed Monday to give Chevron a much-needed legal review.

One of the most important principles in administrative law, the “Chevron deference” was coined after a landmark case,Chevron U.S.A., Inc. v. Natural Resources Defense Council, Inc., 468 U.S. 837 (1984). The Chevron deference is referring to the doctrine of judicial deference given to administrative actions. In Chevron, the Supreme Court set forth a legal test as to when the court should defer to the agency’s answer or interpretation, holding that such judicial deference is appropriate where the agency’s answer was not unreasonable, so long as Congress had not spoken directly to the precise issue at question.

The OCS Orders were the foundation for the current operating regulations in the US and many states and other countries. They were logically organized, easily updated, and published for public comment prior to being finalized.

I have an email message indicating that the first OCS Order No. 1 (Identification of Wells, Platforms, and Structures) was signed on 1/31/1957 and the first OCS Order No. 2 (Drilling) dates back to 2/3/1958! (If anyone has access to the actual documents, please let me know.) The orders were developed much further in the 1970s and 1980s.

Contents of the 1/1980 Atlantic Orders:

OCS Order No. 1: Identification of Wells, Platforms, Structures, Mobile Drilling Units, and Subsea Objects

OCS Order No. 2: Drilling Operations

OCS Order No. 3: Plugging and Abandonment of Wells

OCS Order No. 4: Determination of Well Producibility

OCS Order No. 5: Production Safety Systems

OCS Order No. 6: Well Completions and Workover Operations

OCS Order No. 7: Pollution Prevention and Control

OCS Order No. 8: Platforms and Structures

OCS Order No. 9: Oil and Gas Pipelines

OCS Order No. 10 (reserved)

OCS Order No. 11: Oil and Gas Production Rates, Prevention of Waste, and Protection of Correlative Rights

OCS Order No. 12: Public Inspection of Records

OCS Order No. 13: Production Measurement and Commingling

There has been much discussion, particularly since the 1988 Piper Alpha tragedy, regarding the optimal approach to offshore safety regulation be it prescription, goal setting, safety cases, management systems, or some combination, and how to best influence facility, company, and industry safety culture.

My personal view is that the quality and type of regulations are not nearly as important as the people implementing them. My take:

Good regulators are more important than good regulations and are the key to a successful regulatory program.

Regulatorsmust understand and be committed to their organization’s mission and the strategy for achieving that mission.

While they should have a good understanding of the activities that they regulate, their focus is on challenging operators, not directing them.

Regulators should audit operator activities and carefully review incident and performance data. They should identify problems and concerns, but should not direct solutions.

Safety leaders should be applauded and poor performers should be penalized.

The quality of regulators is more important than the quantity.

Internal and external communication and collaboration are critical to their success.

Management should ensure that regulators are able to focus on their mission and that organizational distractions are minimized.

Senator Manchin and the Alaska delegation criticized the DOI decision memo for Sale 258. The memo implied that the highest allowable royalty rate was chosen to minimize bidder interest and limit future production. Unfortunately, the “Inflation Reduction Act,” which mandated these lease sales, was not particularly helpful in creating interest in the less attractive OCS tracts like those in the Cook Inlet and the shallower waters of the Gulf of Mexico.

Sec. 50261 of the IRA raised the minimum allowable royalty rate from 12 1/2% to 16 2/3%, while capping the maximum rate at 18 3/4%. This provision favors deepwater operators, typically majors and large independents, whose royalty rates were capped at 18 3/4%, the same rate as for previous OCS sales.

Conversely, the IRA royalty provisions penalize the smaller companies and gleaners who are critical to sustaining shallow water (shelf) operations, including environmentally favorable nonassociated (gas-well) natural gas production, by raising the minimum royalty rate to 16 2/3%. DOI exacerbated IRA’s impact by electing to charge the highest allowable royalty rate for Cook Inlet and GoM shelf leases. The net result was a 50% royalty rate increase from prior sales (12.5 to 18.75%).

The table below illustrates the royalty rate implications of the IRA language and the DOI decisions.

Area

Sale

Date

% royalty: <200m water depth

% royalty: >200m water depth

Cook Inlet

244

6/21/2017

12.5

12.5

GoM

256

11/18/2020

12.5

18.75

GoM

257

11/17/2021

12.5

18.75

Cook Inlet

258

12/30/2022

18.75

18.75

GoM

259

3/29/2023

18.75

18.75

Notes:

The base primary term for GoM shelf leases is only 5 years vs. 10 years for leases in .>800 m of water.

In lease year 8 and beyond the rental rates are nearly double for shelf leases vs. deepwater leases ($40/ac vs. $22/ac).

While deepwater development typically requires more time, the higher rental penalty for delayed shelf production (which must be approved by BSEE) is not warranted. $40/acre or $240,000 per year (plus inspection and permitting fees) is a high cost for a marginal shelf lease.

Cook Inlet Sale 244 drew 14 high bids totaling more than $3 million. Sale 258 drew only 1 bid of $64,000. While many factors influence lease sale participation, the 50% increase in royalty rate certainly made the Cook Inlet leases less attractive.

Other than the increased royalty rate, the terms for both Cook Inlet sales were essentially the same. The primary lease term was 10 years and the minimum bonus bid was $25/hectare for both sales. The rental rate was increased by only $3/hectare ($13 to $16).

This reminded me of an important Lawrence Livermore project that was funded by the Minerals Management Service in 1995. The study considered seismic hazard criteria for offshore platforms on the California OCS. My colleague Dr. Charles Smith, a structural engineer, had an important role in this research. Charles had been instrumental in the establishment of an earthquake measurement network in the Pacific Region. The measurement system at Platform Grace in the Santa Barbara Channel successfully recorded 5 earthquakes and the structural responses at multiple locations on the platform.

Lawrence Livermore and the other national laboratories have many outstanding scientists and engineers. The national labs do excellent work, although their studies are a bit pricey 😉

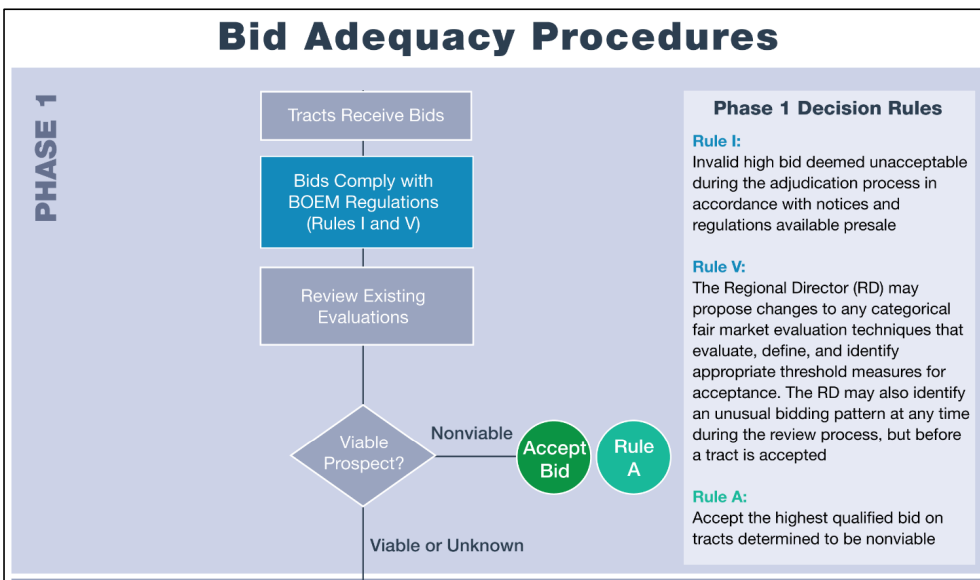

BOEM’s new procedures, which have been published for public comment, seem reasonable. However, it would be helpful to learn more about the testing of the new methodology. (See the quote below). Further, would the rejected Sale 257 bid have been accepted? What was the LBCI for that tract? Would any accepted Sale 257 bids have been rejected? Would the outcome of other sales have been affected?

After a 2-year comprehensive technical review of the delayed valuation methodology, BOEM intends to replace the delayed valuation methodology with a statistical lower bound confidence interval (LBCI) at a 90 percent confidence level as a decision criterion for accepting or rejecting qualified high bids on tracts offered in OCS oil and gas lease sales. Following extensive testing of the alternative approaches using both historical and current lease sale tract data and existing BOEM cash flow simulation models, BOEM determined that the LBCI approach would be the most appropriate substitute for the delayed valuation methodology. The LBCI is a statistical concept that captures the lower bound of a range of values encompassing the true unknown mean of the risked present worth of the resources at the time of the lease sale. The LBCI incorporates the uncertainty of parameters unique to the valuation of each OCS oil and gas lease sale tract. These parameters may include, but are not limited to, subsurface characterization of reservoir properties, cost and timing of the development, and projected revenues. Unlike the delayed valuation methodology, the LBCI approach would not require that BOEM estimate the time delay period between the current OCS oil and gas lease sale and the projected next lease sale. As such, BOEM finds the LBCI to be a better approach going forward.