BOEM’s new procedures, which have been published for public comment, seem reasonable. However, it would be helpful to learn more about the testing of the new methodology. (See the quote below). Further, would the rejected Sale 257 bid have been accepted? What was the LBCI for that tract? Would any accepted Sale 257 bids have been rejected? Would the outcome of other sales have been affected?

After a 2-year comprehensive technical review of the delayed valuation methodology, BOEM intends to replace the delayed valuation methodology with a statistical lower bound confidence interval (LBCI) at a 90 percent confidence level as a decision criterion for accepting or rejecting qualified high bids on tracts offered in OCS oil and gas lease sales. Following extensive testing of the alternative approaches using both historical and current lease sale tract data and existing BOEM cash flow simulation models, BOEM determined that the LBCI approach would be the most appropriate substitute for the delayed valuation methodology. The LBCI is a statistical concept that captures the lower bound of a range of values encompassing the true unknown mean of the risked present worth of the resources at the time of the lease sale. The LBCI incorporates the uncertainty of parameters unique to the valuation of each OCS oil and gas lease sale tract. These parameters may include, but are not limited to, subsurface characterization of reservoir properties, cost and timing of the development, and projected revenues. Unlike the delayed valuation methodology, the LBCI approach would not require that BOEM estimate the time delay period between the current OCS oil and gas lease sale and the projected next lease sale. As such, BOEM finds the LBCI to be a better approach going forward.

Federal Register

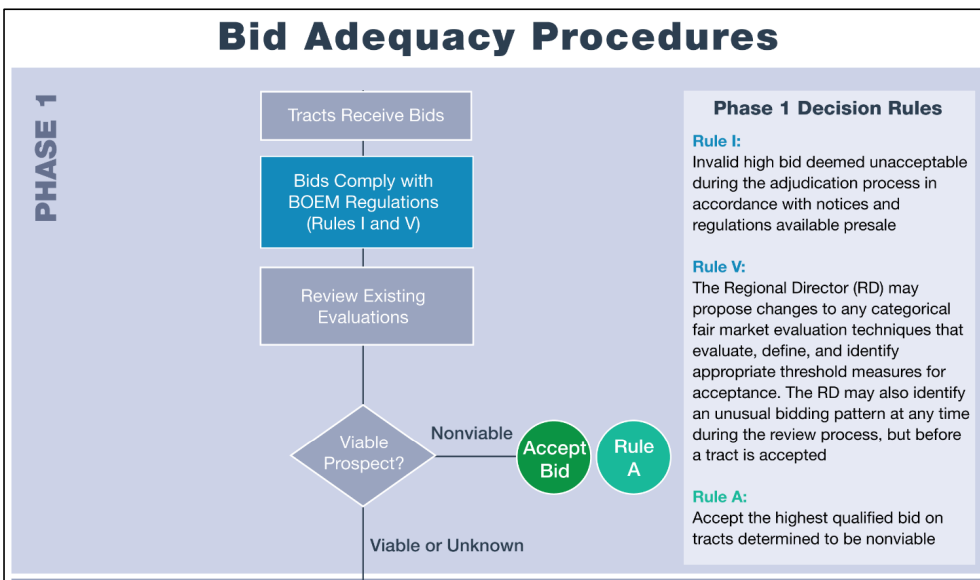

Below is the flow chart for the new procedures. It’s interesting that high bids on nonviable tracts are automatically (and gratefully) accepted! 😉

Leave a comment