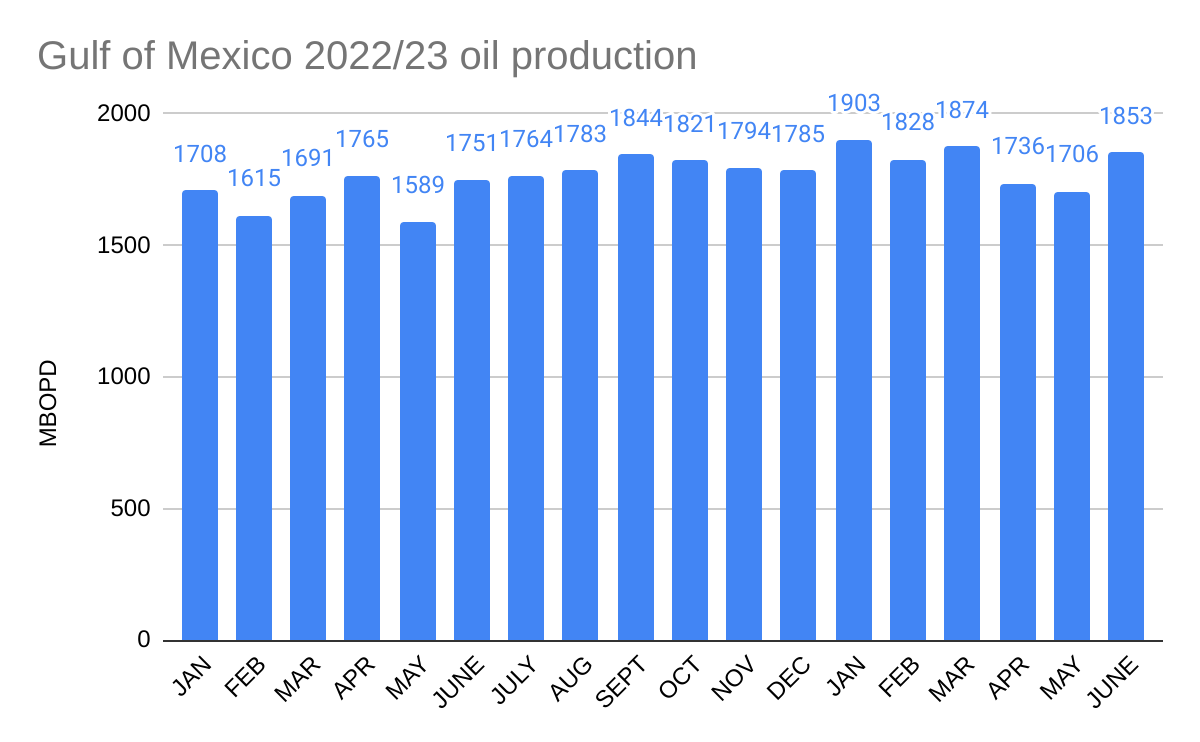

Gulf of Mexico oil production increased to 1.853 bopd in June which is more in line with production at the beginning of the year and the EIA 2023 forecast. Production remains well below BOEM’s 2.0 million bopd forecast for 2023.

Posted in Gulf of Mexico, Offshore Energy - General, tagged BOEM, EIA, Gulf of Mexico production on September 1, 2023| Leave a Comment »

Gulf of Mexico oil production increased to 1.853 bopd in June which is more in line with production at the beginning of the year and the EIA 2023 forecast. Production remains well below BOEM’s 2.0 million bopd forecast for 2023.

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, tagged API, BOEM, Chevron, injunction, Lease Sale 261, Louisiana, Rice's whale on August 31, 2023| Leave a Comment »

The court filing is attached. See the previous post on this matter.

This Court should grant Plaintiffs—the State of Louisiana, the American Petroleum Institute (“API”), and Chevron U.S.A. Inc. (“Chevron”)—a preliminary injunction and prevent those unlawful provisions from permanently disrupting the result of the fast-approaching lease sale (which Congress has directed must occur by September 30, and which cannot be delayed without causing Plaintiffs even more serious injury).

Posted in Gulf of Mexico, Offshore Wind, tagged Gulf of Mexico, interest rates, Orsted, supply chain, tax credits, wind leases on August 30, 2023| Leave a Comment »

Yesterday was not a good day for US offshore wind. Not only was the Gulf of Mexico wind lease sale disappointing, but Orsted announced US impairments of $2.3 billion causing their share price to fall to the lowest level in more than 4 years.

Unsurprisingly, Orsted management assumes no responsibility for the company’s poor performance, blaming supply chain problems, high interest rates and “a lack of new tax credits.” Outsiders might suggest that there were other factors such as irrational exuberance in the acquisition of wind leases at inflated prices, and unrealistic expectations regarding a complementary power source that is dependent on government mandates and subsidies.

“The situation in U.S. offshore wind is severe,” Chief Executive Mads Nipper told reporters on a conference call.

Reuters

Posted in Gulf of Mexico, hurricanes, tagged Blind Faith, Chevron, Gulf of Mexico, Idalia, Petronius on August 29, 2023| Leave a Comment »

Genesis, which is being decommissioned, has been fully evacuated. BSEE will no doubt have information on all evacuations and shut-ins tomorrow.

Posted in Gulf of Mexico, Offshore Energy - General, Offshore Wind, tagged Galveston, Gulf of Mexico wind auction, Lake Charles, RWE Offshore on August 29, 2023| Leave a Comment »

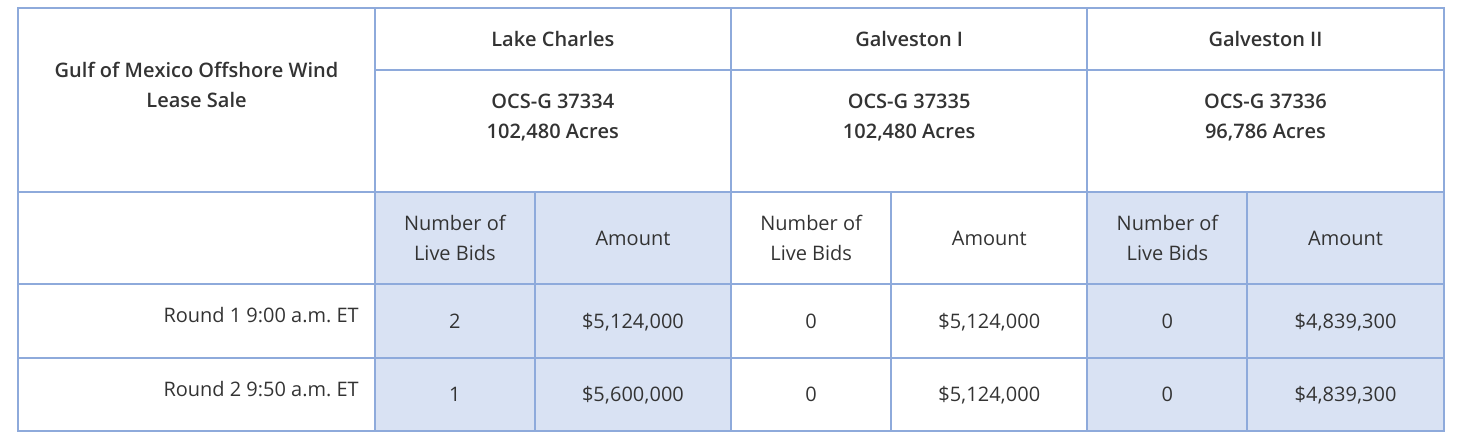

Only 1 of the 3 tracts was sold, and the amount bid was a modest $5.6 million. Given the extensive lease sale planning and promotion, this would seem to be a rather embarrassing outcome.

RWE Offshore US Gulf LLC won the Lake Charles tract. Neither of the 2 Galveston tracts received bids. RWE’s headquarters are located in Essen, Germany.

By comparison, the 5 California offshore wind leases, each of which is smaller and in far deeper water than the GoM tracts, received bids of $130 to 173 million. These leases were sold in December 2022. Smaller Atlantic wind tracts have also received much higher bids. State mandates and subsidies no doubt contributed to the inflated bidding in the Atlantic and Pacific.

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, Regulation, tagged API, BOEM, Chevron, Lease Sale 261, Louisiana, Rice's whale on August 26, 2023| Leave a Comment »

See the attached document.

From a regulatory policy standpoint, this appears to be a strong filing. Operationally, the most important points pertain to the costly and premature Rice’s whale restrictions first discussed on this blog.

Most notably, the plaintiffs seek (p.39):

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, Regulation, tagged BOEM, Gulf of Mexico, Lease Sale 261, NOAA, Rice's whale, Senator Manchin on August 25, 2023| Leave a Comment »

In addition to the lease stipulation, the entire expanded Brice’s whale area has been excluded from the lease sale. Senator Manchin strongly criticized that decision:

Let me be clear, the exclusion of more than 6 million productive acres from the upcoming offshore oil and gas lease sale in the Gulf of Mexico based on a settlement reached in the name of protecting Rice’s whale while conveniently only targeting oil and gas is yet another example of this Administration’s intentional undermining of the strong energy security provisions in the Inflation Reduction Act.

Senator Manchin

Posted in accidents, Gulf of Mexico, IRF, Offshore Energy - General, tagged BSEE, Coast Guard, IRF, OCS incidents, offshore safety, regulatory fragmentation, safety trends on August 24, 2023| Leave a Comment »

Per the BSEE presentation attached below:

Slide 13: “In 2022, the rate of occupational fatalities, reported for activities on facilities where BSEE has primary investigation authority, decreased to being near the historical national average of approximately 0.9 fatalities per 25,000 full time equivalent workers per year. However, considering all offshore risk factors, including helicopter transportation, diving, marine transfer, and COVID-19 exposures, the occupational fatality rate for all OCS activities has remained high since 2019.“

Slide 15: “In 2022, the TRIR for both production and construction operations increased to the highest levels recorded since 2010 and remained high even after discounting the impact of COVID-19 illnesses. The TRIR for drilling and well operations, however, remained near their historical lows.“

Comments:

Posted in California, decommissioning, Gulf of Mexico, Offshore Energy - General, Regulation, tagged BOEM, compliance and safety, decommissioning, financial assurance, oil and gas reserves, proposed rule on August 22, 2023| Leave a Comment »

The attached comments were submitted to BOEM via Regulations.gov. The comments address specific provisions of the proposed rule and include a recommendation to hold companies fully accountable for their lease transfers, but not for subsequent transfers in which they are not a party.

Do I get a t-shirt for being one of the first 2000 entries? 😀

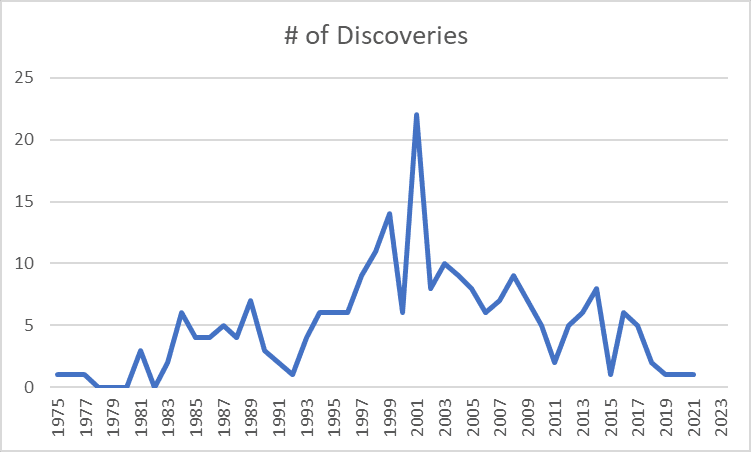

Posted in Gulf of Mexico, Offshore Energy - General, tagged deepwater field discoveries, Gulf of Mexico on August 18, 2023| Leave a Comment »

Per our previous post, “Ominous signs for the future of Gulf of Mexico production,” Lars Herbst has plotted (below) deepwater GoM field discoveries dating back to the early days of deepwater drilling operations.

These are official USGS, MMS, and BOEM data (depending on the era) for field discoveries in >1000′ of water. Note that the last discovery was in March 2021.

This is a discouraging graphic given that the deepwater GoM is currently the only option for significant new US offshore production.