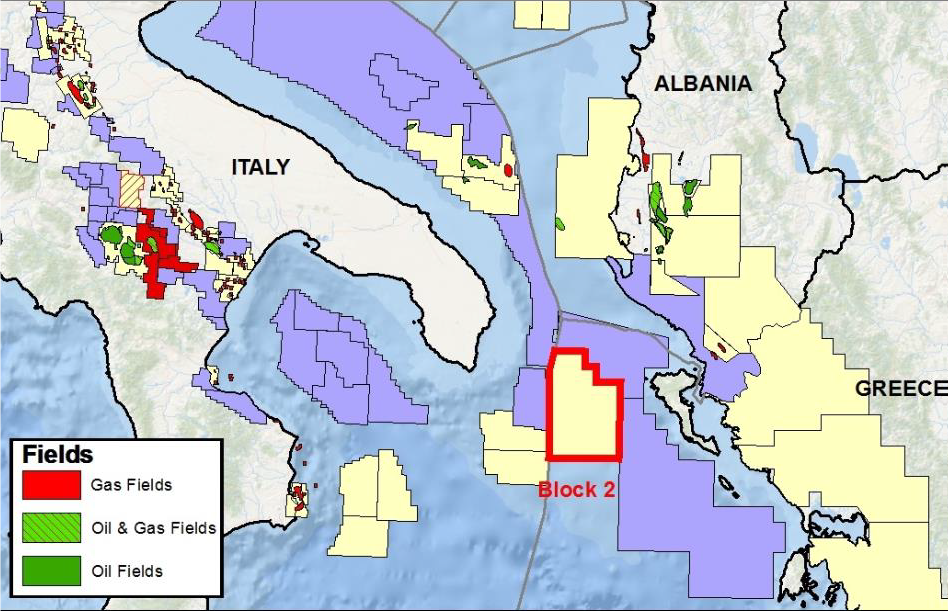

Location: In the Ionian Sea 30 km west of Corfu Island (note: that’s 18.6 miles, not the 125 mile buffer that Florida views as sacred)

Water depth: 500 to 1,500 m

Block size: 2,422.1 sq Km, the largest unexplored offshore structure in the Mediterranean (note: Gulf of America leases are only 23.3 sq km or < 1% as large)

First drilling: late 2026 or early 2027. This will be the first exploratory offshore drilling in Greece since 1981!

Energean’s participation is set at 30%, down from 75%.

Helleniq participation is now 10%, down from 25%.

Energean will remain the operator during the exploration stage.

In the event of a commercial discovery, Exxon will assume the operatorship during the development phase.

Andreas Shiamishis, CEO of HELLENiQ ENERGY: “Greece is emerging as one of Europe’s newest and promising regions for hydrocarbon exploration and development. This transaction represents a positive step not only for the joint venture partners, but also for the Greek economy.”

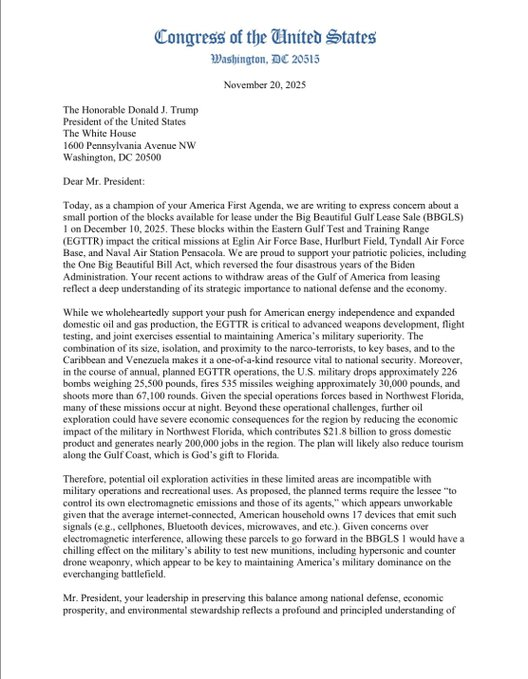

Will the oil and gas lease sale boldly named Big Beautiful Gulf 1 (BBG1) live up to its grand name? Given the more favorable lease terms and the 2 year gap since the last sale, BBG1 should surpass the previous 3 sales (table below). Questions:

Which majors will be the most active bidders? Chevron? Shell? BP? Oxy/Anadarko?

Will former Gulf of Mexico stalwarts Exxon and Conoco Phillips participate for the first time in years? Probably not, but US super-majors should participate in the US offshore program.

How many companies will submit bids? Would like that to be a number >35.

How many tracts will receive bids? A number >300 would be very encouraging.

Will the total high bids exceed $400 million?

Will we see an increase in shelf interest?

Which independents will be the most active?

After the not-so-clever carbon disposal acquisitions in the last 3 sales, will the number of carbon disposal bids be zero? For the first time ever, the Federal government felt compelled to stipulate the obvious (see the proposed notice for OCS Sale 262) – that an Oil and Gas Lease Sale is only for oil and gas exploration and development.

See the summary data below for the last 3 Gulf lease sales. We’ll fill in the blanks next week.

Sale No.

257

259

261

BBG1

date

11/17/2021

3/29/2023

12/20/2023

12/10/2025

companies participating

33

32

26

total bids

2233

2842

3161

tracts receiving bids

2143

2442

2751

sum of all bids $millions

198.5

309.8

441.9

sum of high bids ($millions)

101.7

263.8

382.2

highest bid company block

$10,001,252.00 Anadarko AC 259

$15,911,947 Chevron KC 96

$25,500,085 Anadarko MC 389

most high bids company sum ($millions)

46 bp 29.0

75 Chevron 108.0

65 Shell 69.0

sum of high bids ($millions) company

47.1 Chevron

108 Chevron

88.3 Hess

most high bids by independent

14-DG Expl.

13-Beacon 13-Red Willow

22-Red Willow

1excludes 36 leases improperly acquired for carbon disposal purposes; 2excludes 69 leases improperly acquired for carbon disposal purposes; 3excludes 94 leases improperly acquired for carbon disposal purposes

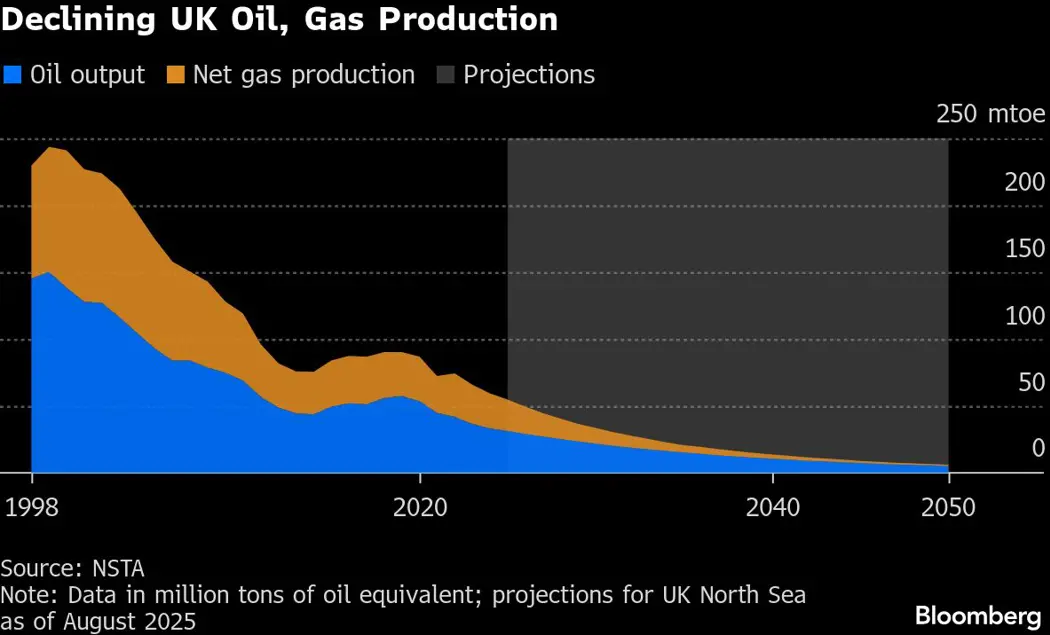

JL Daeschler, other North Sea veterans, and those of us who once admired the UK offshore program, lament the sad plight of their oil and gas industry and the destruction of the economy in northeast Scotland.

Incomprehensibly, the UK has retained the Energy Profits Levy, which requires North Sea operators to hand over 78% of their diminished profits to the Treasury. Most have regrettably chosen to do business elsewhere. Investment in the UK North Sea is at a record low and a study from Robert Gordon University says jobs are being “quietly” lost at a rate of 1,000 a month.

The UK government is grudgingly allowing some tieback production to existing facilities, but this will do little to stem the industry’s decline. JL notes that this limited infield development is not the type of new field investment needed to grow production and sustain the service industry (rigs, boats, helicopters, equipment, etc.).

“The term energy transition somehow sounds like it is a well-lubricated slide from one reality to another. In fact, it will be far more complex: Throughout history, energy transitions have been difficult, and this one is even more challenging than any previous shift.”

Related article in the WSJ: “Europe’s Green Energy Rush Slashed Emissions—and Crippled the Economy”

“European politicians pitched the continent’s green transition to voters as a win-win: Citizens would benefit from green jobs and cheap, abundant solar and wind energy alongside a sharp reduction in carbon emissions. Nearly two decades on, the promise has largely proved costly for consumers and damaging for the economy.”

“Europe largely took an “or” strategy: It raced to replace fossil fuels with solar, wind and biomass by taxing carbon heavily, subsidizing renewables and closing scores of fossil-fuel power plants. Britain, which pioneered the use of coal for energy, last year became the first large industrialized country to shut all of its coal-fired power plants. It has also banned new offshore oil-and-gas drilling. Denmark plans to eliminate gas for home heating by 2035. Around one-fifth of Germany’s municipal utilities plan to shut down their gas networks in coming years, according to an October survey by the utilities’ trade association.”

On my favorite holiday, I’m sending best wishes to BOE readers of all persuasions. Offshore energy issues can be divisive, even among friends, and I’m grateful for the opportunity to share information and opinions.

My wife and I will be spending Thanksgiving with my daughter’s family including our 6 grandchildren, none of whom have expressed interest in being offshore safety regulators (no higher calling 😉).

Belated holiday wishes to our friends in Canada where Thanksgiving is celebrated in October, and cheers to those living where a similar fall holiday is observed.

In JPMorgan’s view, the stage is set for a potential decline of as much as 50% in oil prices through the end of 2027, taking Brent crude down to the low $30s per barrel range from its current level of around $63.50.

Will bearish forecasts by JPMorgan and others temper bidding at the highly anticipated, and long awaited, Gulf lease sale to be held on 12/10/2025? Probably not for these reasons:

Given the longer term nature of deepwater development, production will not begin for years following lease issuance. Note that anticipated first production for 3 new high-pressure deepwater projects, Kaskida, Sparta, and Tiber, will be 23, 16, and 21 years after the field discovery dates.

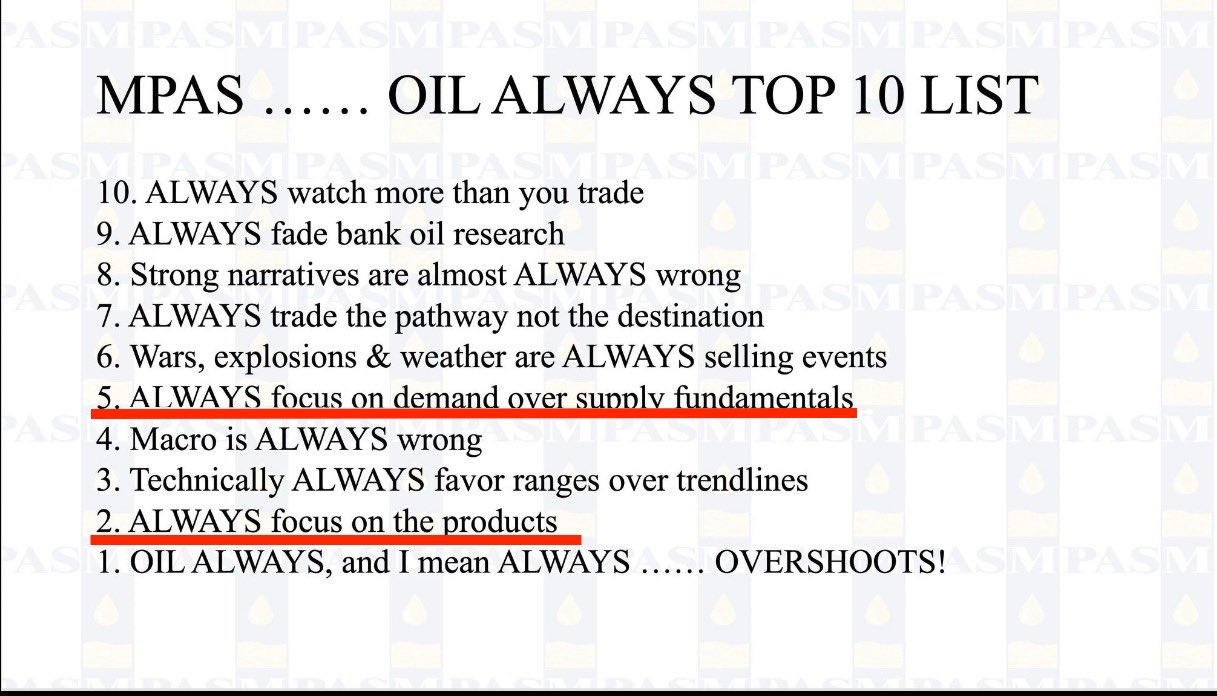

To the extent that price forecasts are reliable at all (see no. 9 in the image below), the degree of uncertainty for longer term forecasts is particularly high.

The sale has to live up to its name Big Beautiful Gulf 1 (BBG1). 😉

Member companies, which include major players such as Ørsted, Equinor, Vattenfall, RWE, and CIP, report quarterly data on accidents, near-misses, hazardous observations, and equipment damage. As is the case with most industry reporting schemes, anonymity is prioritized over transparency.

Sørensen asserts that the G+ wind industry data are incomplete: ”It shows that what is reported under the guidelines has gone down, and also that there is a cut off on what is being reported that does not include the full value chain on the industry.” He notes that a contractor to Northland Power from Canada, a member of G+, was involved in a 2024 workplace accident in Taiwan that resulted in three fatalities. (It’s also noteworthy that Equinor’s 2024 Empire Wind fatality was not included.)

Sørensen: ”There have been no significant improvements in the last 10 years. Safety in offshore wind is neither getting worse nor better. There are no signs of that.”

”I’m speaking up because we owe people the truth. If we’re not honest about the actual safety conditions in offshore wind, we can’t change them. Misinformation about workplace safety creates a dangerous illusion that everything is “under control”, while too many people are getting hurt. But when we dare to speak about reality as it is, we create the foundation for a safer, faster, and truly sustainable energy transition,” Sørensen says.

”And then it becomes difficult to learn if you have to wait for something to go through 57 gates and down past legal,” he says. (Sound familiar?)

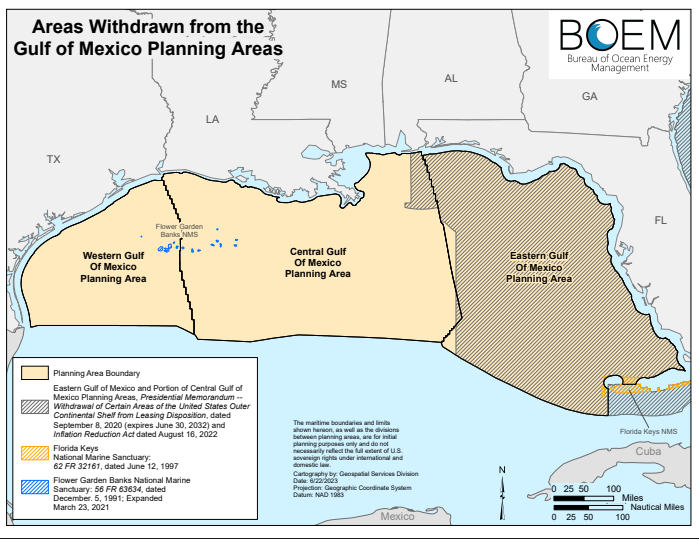

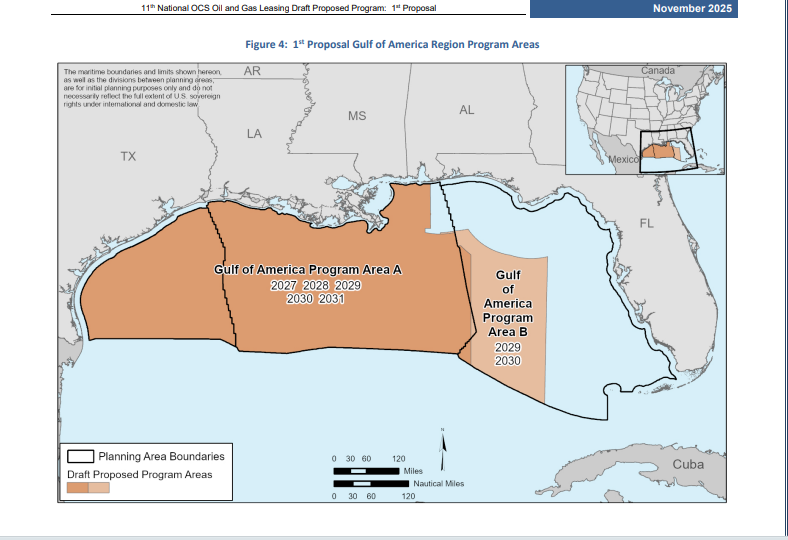

A specific description of the proposed Florida buffer in the Eastern Gulf is found in a footnote on page five of the Draft Proposed Program (DPP):

2 Includes a 100-mile coastal buffer off the coast of Florida and the area eastward of a line extending south from a point approximately 25 miles west of Tallahassee, Florida.

Draft Proposed Program2020 Trump Withdrawal

The 100 mile buffer seems like a reasonable proposal that minimizes the risk of coastal impacts without significantly reducing the oil and gas resource potential. However, the 125 mile buffer established in the Gulf of Mexico Security Act (2006) and the 2020 Trump withdrawal (see the comparison above) has become sacrosanct, and Gov. DeSantis and the Florida delegation oppose any change:

President Trump’s 2020 memorandum protecting Florida’s eastern Gulf waters represents a thoughtful approach to the issue.

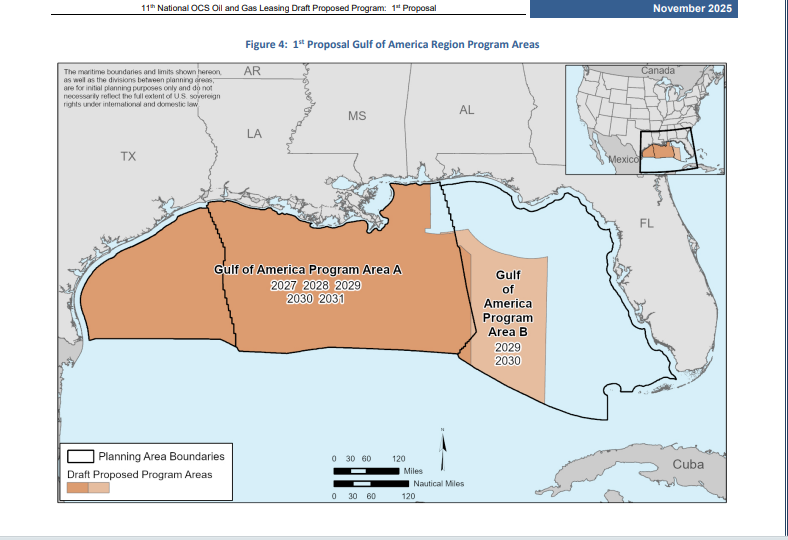

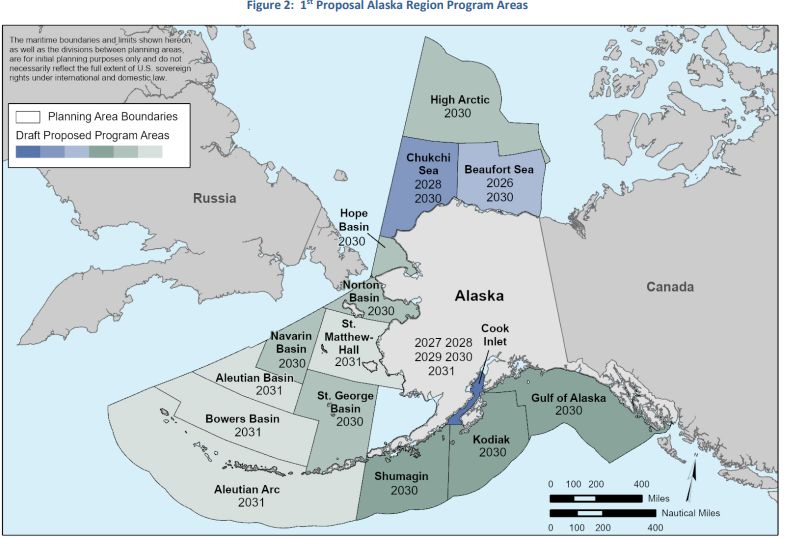

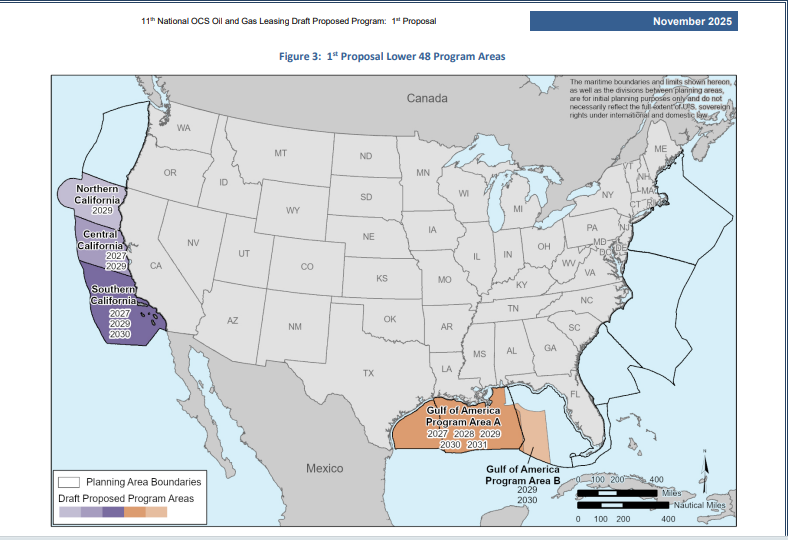

The press release and full program are linked. It looks like the most recent leaks were accurate. See the maps below with the locations and dates. This will stir the pot!

Conceptually, this technologically advanced polymetallic nodules collection system looks great. The big challenge that John Smith sees is with the number of moving parts. The numerous manipulators operating at such depths could be prone to breakdowns which reduce recovery rates and significantly increase operating costs.

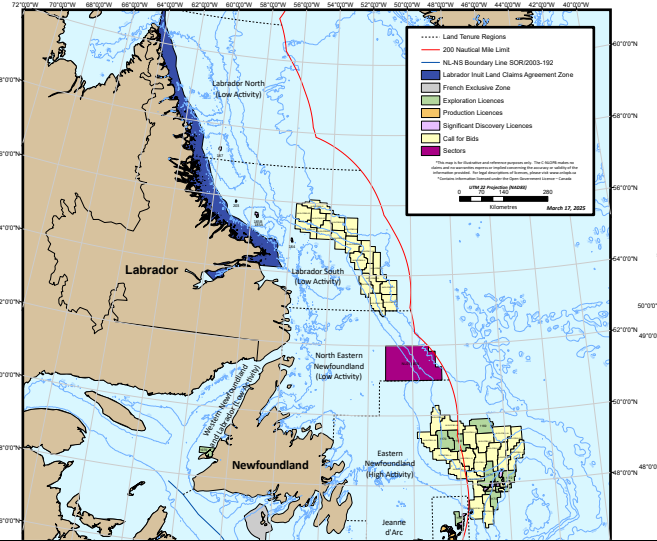

Difficult operating conditions, high costs, and relatively modest oil price projections are no doubt factors contributing to the absence of bids. Energy NL has also pointed to the “complex, inconsistent and burdensome regulatory system” as a contributing factor.

Newfoundland’s newly elected Premier, Tony Wakeham, has said his Progressive Conservative Government will advocate for the cancellation of the emissions cap as it is a cap on production. He also supports incentives for offshore oil and gas projects such as an investment tax credit or the former Petroleum Incentive Program and indicated he would work with Energy NL to review incentives that could be implemented provincially.

The C-NLOER is committed to “review its land tenure system in collaboration with governments and others, to identify opportunities to enhance competitiveness in the Canada-Newfoundland and Labrador Offshore Area.”