My friends and former colleagues in Southern California do not live in areas that were devastated by the recent fires.

However, Nabil Masri, one of our outstanding petroleum engineers, sent this picture taken from his driveway in Camarillo during the “Mountain Fire” in November. His home was in an evacuation warning area, and the family was packed and ready to go. Fortunately, things improved and they did not have to evacuate.

As expected, the White House announced the largest ever permanent ban on offshore oil and gas leasing in the US, and to the best of my knowledge, anywhere in the world.

The sheer magnitude of the ban makes other such withdrawals appear modest by comparison. It’s amazing how bold Presidents (and their handlers) become when they are about to leave office.

The permanent ban includes:

The entire Atlantic Outer Continental Shelf (OCS): While there are no current oil and gas leases in the US Atlantic, the region is highly prospective and could contain more than 20 billion barrels of oil equivalent (BOE).

The Eastern Gulf of Mexico: This is the OCS area that many petroleum geologists find most attractive. The best prospects are >100 miles from shore which minimizes coastal risks, and the high natural gas potential aligns with Florida legislation supporting the use of gas for power generation.

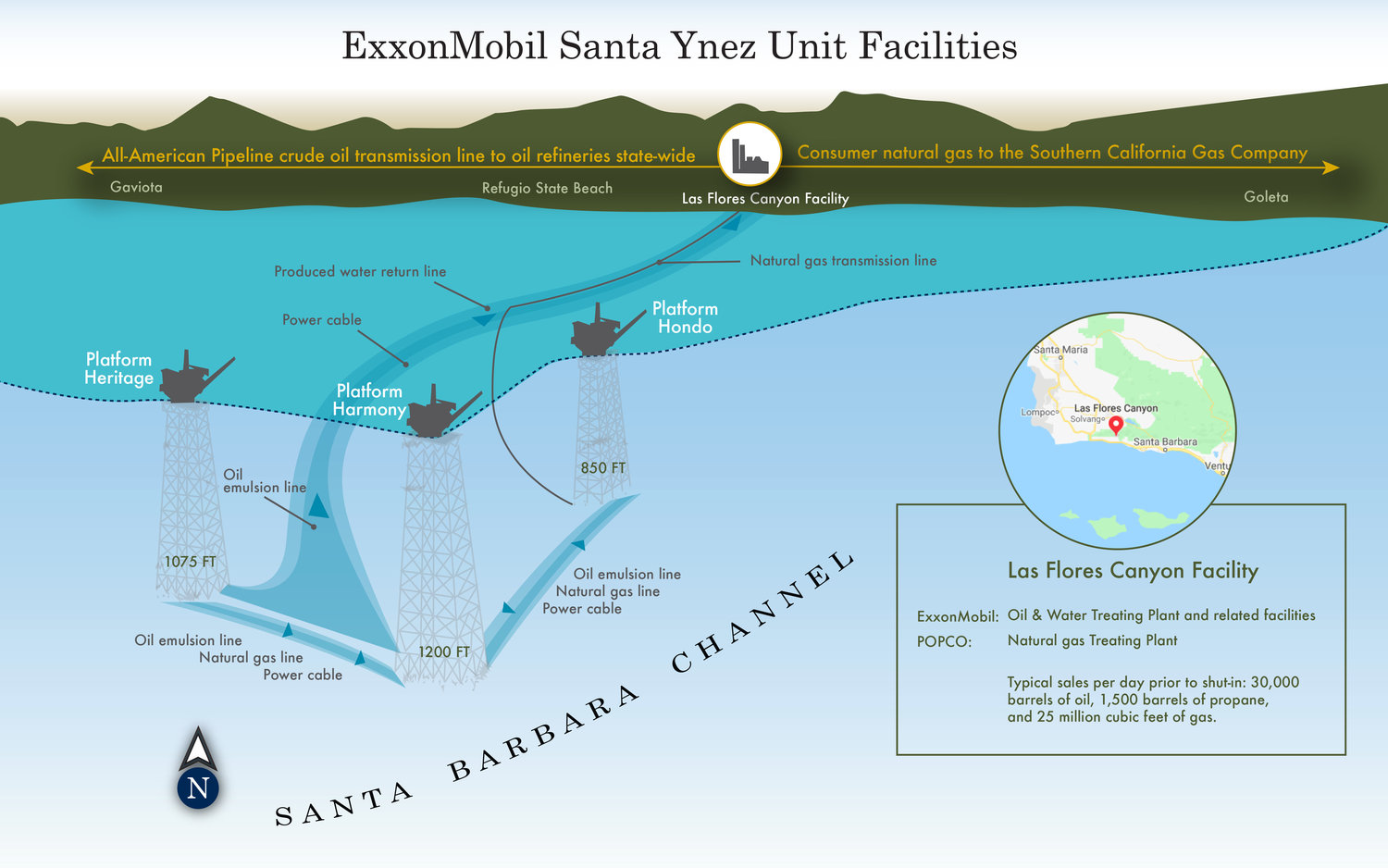

The entire Pacific OCS: While the resources are substantial, their loss has been a foregone conclusion for 25 years. When you can’t even decommission old platforms or restore production on important existing facilities (i.e. the Santa Ynez Unit), how can you possibly expect to issue new leases?

The remainder of the OCS offshore western Alaska. The wishes of the majority of Alaskans, who support offshore exploration and development, have been largely ignored for decades.

President-elect Trump has vowed to reverse President Biden’s leasing ban, but that may not be so easy. This is not a matter of simply reversing an executive order. Sec. 12(a) of OCSLA grants the authority to withdraw lands to the President and does not provide for reversal by future Presidents. The attached NYU Law brief concludes that “a subsequent president lacks authority to restore previously withdrawn lands to the federal oil and gas leasing inventory.”

The new Administration will no doubt have a different view than that expressed in the NYU Law brief, but any reversal decision will likely be challenged in court.

Those who wrote and approved Sec. 12(a) should have had more foresight. However, 72 years ago the authors presumably thought Presidents would only use the authority to remove small, especially sensitive areas from leasing consideration, and never thought that a President would remove both of our oceans and much of the Gulf of Mexico!

Congress could of course reverse the Biden bans, but given the complexity of offshore energy issues, such legislation may be difficult to pass.

Attached is an excellent Scientific American article featuring BOE contributor and decommissioning specialist John Smith, former colleague and marine biologist Dr. Ann Bull, and Dr. Milton Love, the leading authority on California’s offshore platform ecosystems.

I had the pleasure of taking a highly informative boat tour around Platform Holly with Dr. Love and a group of international visitors. Holly, which is pictured at sunset in the BOE header, is among the platforms awaiting decommissioning.

Dr. Love on the total removal of California offshore platforms:

“As a biologist, I just give people facts,” he says. “But I have my own view as a citizen, which is: I just think it’s criminal to kill huge numbers of animals because they settled on a piece of steel instead of a rock.”

The Santa Barbara County Planning Commission has approved the transfer of the onshore pipeline from Exxon to Sable Offshore. Although the Environmental Defense Center (EDC) is appealing that decision to the Board of Supervisors, the Board’s vote will likely be a 2-2 tie. Supervisor Hartmann’s property is close to the pipeline and she has recused herself from votes on the matter. A 2-2 vote would be a win for Sable, because a tie vote means the planning commission decision stands.

As an investment, Sable is a “pure California permitting play,” which means the risks are high. The company’s chances for success are almost entirely dependent on receiving the necessary approvals from State and local agencies.

Sable’s share price soared to $23.43 on 9/3 after the company reached agreement with Santa Barbara on the installation of required pipeline valves. The price bounced further to $28.30 on 9/19 before falling sharply to $19.43 on 10/9 after being cited for failing to get California Coastal Commission approval to install the required valves. The price rebounded to $24 following the County Planning Commission’s approval of the transfer from Exxon to Sable before settling at $23 on Friday, the date of the EDC appeal.

Expect the financial and psychological roller coaster ride to continue.

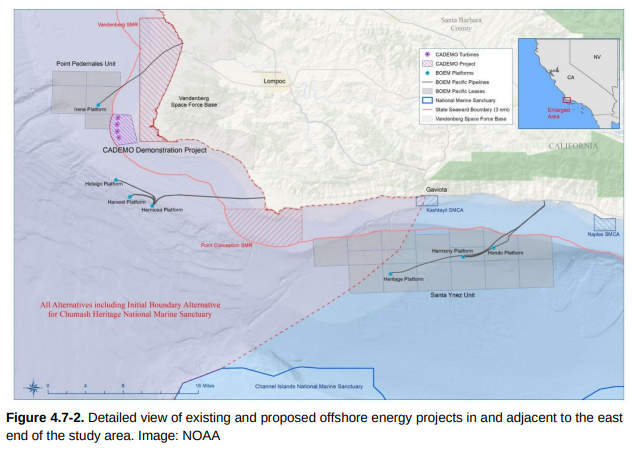

Almost 40 years ago, four large oil and gas platforms were installed in the beautiful offshore area that was part of our Santa Maria District (Pacific Region of the Minerals Management Service). Those platforms are now within the boundaries of the Chumash Heritage National Marine Sanctuary (see map above).

We watched those platforms being installed, inspected the drilling and production operations, and performed a myriad of other duties including the curtailment of offshore operations prior to launches from Vandenberg AFB. Those Vandenberg launches weren’t always perfect as this link clearly demonstrates. Even knowing that, it was still a bit unnerving when missiles were recovered during post-abandonment site clearance trawls.

All four of those Santa Maria District platforms are now on terminated OCS leases. All were installed by companies that are now part of Chevron Corp. (Chevron, Texaco, and Unocal). They are currently maintained by Freeport-McMoRan Oil & Gas, with Chevron retaining financial responsibility for decommissioning.

Platform

Install yr.

installed by

water depth (ft)

Est. removal weight (short tons)

wells drilled

Harvest

1985

Texaco

675

35,150

19

Hermosa

1985

Chevron

603

30,868

13

Hidalgo

1986

Chevron

430

23,384

14

Irene

1985

Unocal

242

8,762

26

BSEE reports that the 46 wells on Harvest, Hermosa, and Hidalgo have been plugged and tested, and that the well conductors have been removed. No information has been posted on the status of the wells at Platform Irene, but presumably they are (or will soon be) plugged in accordance with BSEE regulations.

Will the inclusion of these platforms in the Chumash Marine Sanctuary further complicate the already difficult decommissioning process? Decommissioning specialist John Smith thinks it may:

“In addition to the BOEM and BSEE approval process, Chevron and FMC are going to be dealing with the NOAA permitting regime for Sanctuaries. Those permitting and environmental compliance requirements are extensive. NOAA’s NEPA documentation for West Coast marine sanctuaries will also need to be amended to include the Chumash.”

So the “Mission Impossible” that is California OCS decommissioning now has yet another complex regulatory element.

“Even though most of the SYU facilities are outside the Sanctuary, the proximity of the operations to the Sanctuary is problematic. The Chumash are now going to be a co-manager of the Sanctuary, adding another player in the process. Sable is going to obtain multiple Federal, State and local permits to restart SYU, and law suits are likely at every stage of the process.”

Equinor reports that all 5 Hywind turbines have been returned to service after being towed to Norway as part of a 4-month maintenance campaign.

Even though the turbines had only been in operation since 2017, Equinor puts a positive spin on the 4-month maintenance outage, declaring total victory:

“The successful completion of the maintenance campaign on Hywind Scotland is a testament to the collaborative efforts of our teams and partners. As the world’s first floating offshore wind farm, Hywind Scotland has demonstrated the immense potential of floating wind. Through this maintenance campaign, we’ve gained valuable insights that will help us refine maintenance practices and optimise this technology for the future. By sharing our learnings, we aim to contribute to the growth and development of the floating wind industry.”

Some of the folks in Scotland have a different take as evidenced in this video:

Meanwhile, the turbines planned for offshore Central California will also have to be towed to shore for major maintenance. Nearby harbor areas like Morro Bay (pictured below) would be overwhelmed by the large structures and the maintenance and repair operations. Central Coast residents are not enamored with “another attempt to industrialize the coast.” Towing the towers to LA/Long Beach, albeit rather distant from the leases, would seem to be the preferred option for such work.

Looking forward, the first power generation from floating wind turbines on the Central Coast is forecast for 2034. Betters may want to take the over!

Per a related post, the full SpaceX lawsuit is attached. It’s mostly exhibits, so don’t be intimidated by the length.

This excerpt summarizes the case nicely:

“Rarely has a government agency made so clear that it was exceeding its authorized mandate to punish a company for the political views and statements of its largest shareholder and CEO. Second, the Commission is trying to unlawfully regulate space launch programs—which are critical to national security and other national policy objectives—at Vandenberg Space Force Base (the Base), a federal enclave and the world’s second busiest spaceport.”

Even Gov. Newsome sides with SpaceX saying “I’m with Elon.”

Will this case teach the Commission some humility? Probably not, but we shall see.

The California Coastal Commission, which exercises enormous power and limited restraint, is making headlines for preventing SpaceX, arguably America’s most extraordinary company, from increasing the number of satellite launches from the Vandenberg Space Force Base, a Federal facility. The Coastal Commission made this decision just 3 days before SpaceX’s awe inspiring rocket booster catch in Texas:

Sable Offshore, despite being spawned by super-major Exxon, is a relative minnow compared to SpaceX, at least politically. The restart of production from Sable’s Santa Ynez Unit is facing another obstacle now that the Coastal Commission has entered the fray.

Sable argues that repair and maintenance activities are exempt from Coastal Act permitting requirements, and have been conducted under their existing permits for 35+ years.

The Commission does not like to see its authority questioned, and is influenced by groups whose sole objective is to prevent the restart of production. We’ll see how this sorts out.

Center for Biological Diversity photo of pipeline repair work as published by Noozhawk

Meanwhile, Elon Musk did not hold back after the Commission’s decision not to allow an increase in the number of launches from Vandenberg:

“The California Coastal Commission should be dissolved as an organization. An utterly insufferable and misanthropic group of Karens if there ever was one! Their idea of the perfect coastline is one where there are zero humans or even signs of human! Anyone who has had any dealings with them will attest to this. They should not exist.”

Platform Holly, California State waters in the Santa Barbara Channel, formerly operated by Venoco

Platform Holly sits immediately offshore from the Univ. of California at Santa Barbara, and UCSB scientists have studied the platform and surrounding ecology extensively. Multiple studies have shown that production from Holly reduced natural seepage and methane pollution from shallow formations beneath the Channel. Platform Holly was thus a “net negative” hydrocarbon polluter.

The natural seepage in the Santa Barbara Channel was important to the earliest inhabitants of the area. The Chumash used the tar for binding and sealing purposes, including caulking their canoes. Since Holly shut down in 2015 following the Refugio pipeline spill, offshore workers and supply boat crews have reported a considerable increase in gas seepage.

Earlier this month, it was reported that well plugging operations at Holly had now been completed, but decisions regarding the final decommissioning of the platform remain.

Venoco declared bankruptcy in 2015 and the State of California became the platform owner. According to the State Lands Commission, Exxon will pay the costs for decommissioning the platform. This is because Exxon acquisition Mobil operated the platform from 1993-1997 before Venoco became owner.

The most recent Holly development is that Venoco has settled its law suit with Plains, the company responsible for the 2015 Refugio pipeline spill that halted production from Holly. Terms of the settlement have not been disclosed.

Note: As an aside, I’m curious as to whether Mobil provided a decommissioning guarantee as part of the sale to Venoco or whether the State is simply holding ExxonMobil accountable as a legacy owner. If it’s the latter, why isn’t bp (bp acquisition Arco was Holly’s operator from 1966-1993) also liable? Is it a matter of Mobil being the more recent predecessor owner?

Outstanding non-political Keith Morrison commentary on the LA fires

Posted in California, Uncategorized, tagged commentary, Keith Morrison, LA fires on January 13, 2025| Leave a Comment »

Read Full Post »