A group of international shipping companies and their subsidiaries tentatively agreed Wednesday to pay $96.5 million to Houston-based Amplify Energy Corp. to dismiss one of the last remaining lawsuits over the oil spill, which sent at least 25,000 gallons of crude into the waters off Huntington Beach in October 2021.

Whoever blew up the Nord Stream pipelines was not entirely successful in that one of the Nord Stream 2 lines was apparently undamaged. What is next for that line? Will the two Nord Stream 1 and the other Nord Stream 2 pipelines be repaired?

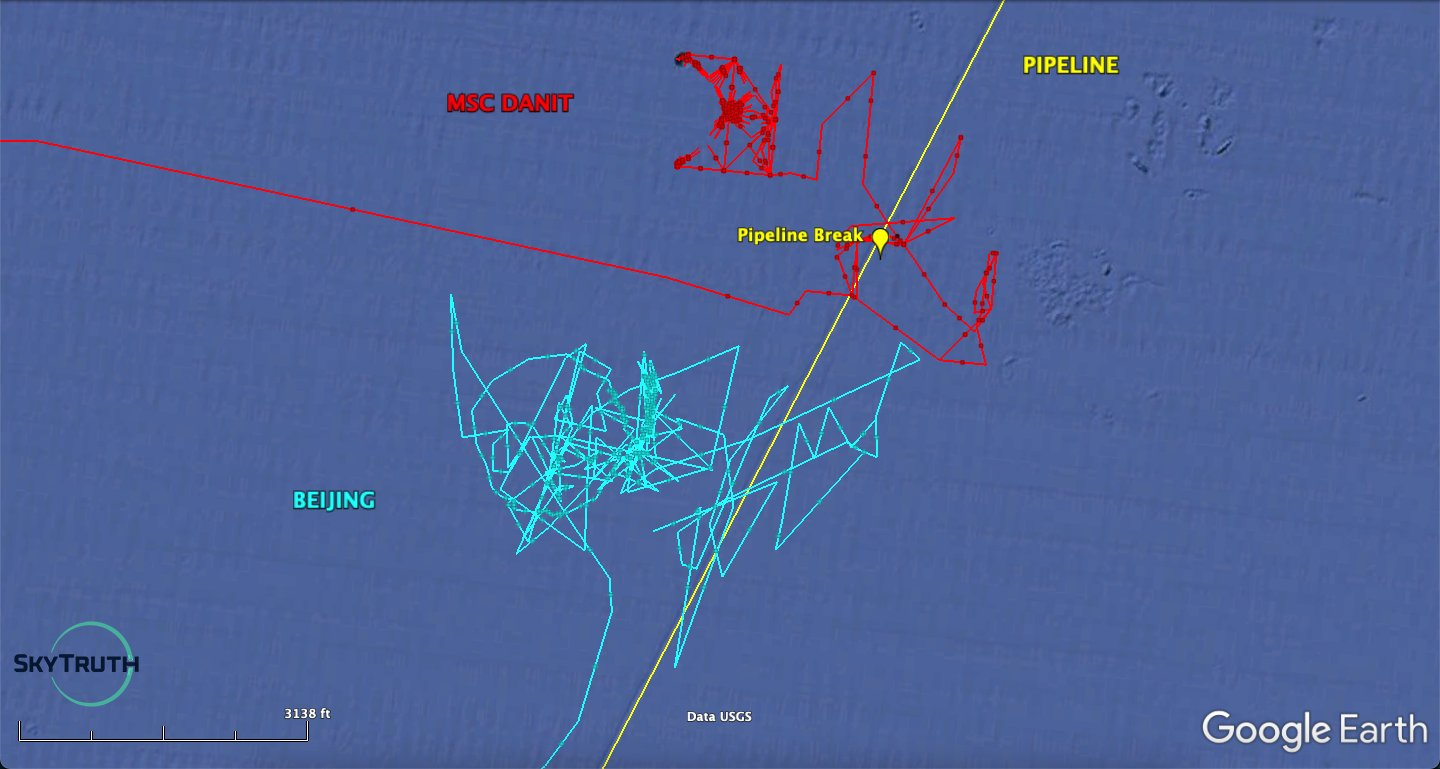

Glomar Worker continues to check both strings of NordStream 2 pipeline.

Likely objective is to check String B integrity for certification to be re-commissioned, and to assess cost/scope of repairing String A.

The state-owned Chinese oil explorer surrendered operating control of those assets to quell U.S. national security concerns, said two people familiar with the agreement who asked not to be named because the terms aren’t public.

The 2019 annual production record remains intact at 1.897 million bopd, but could be exceeded in 2023 if (1) projected deepwater startups are on schedule, (2) prices remain above $70/bbl, (3) depletion is effectively managed, and (4) the hurricane season is again favorable

The “energy transition” will not affect oil and gas demand for the foreseeable future, more nuclear power plants are not being built, and shale has its limitations. We better not neglect what is left of the OCS oil and gas program.

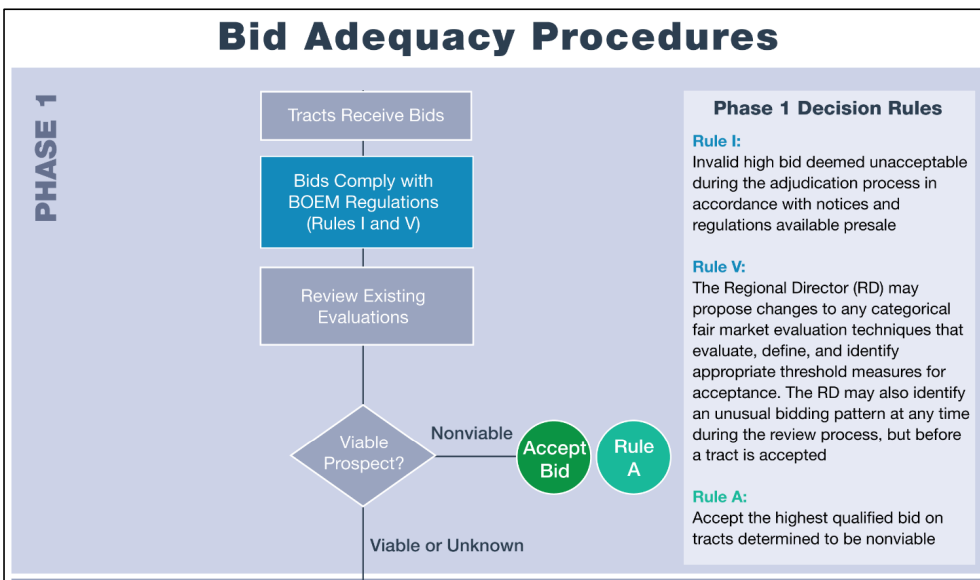

BOEM’s new procedures, which have been published for public comment, seem reasonable. However, it would be helpful to learn more about the testing of the new methodology. (See the quote below). Further, would the rejected Sale 257 bid have been accepted? What was the LBCI for that tract? Would any accepted Sale 257 bids have been rejected? Would the outcome of other sales have been affected?

After a 2-year comprehensive technical review of the delayed valuation methodology, BOEM intends to replace the delayed valuation methodology with a statistical lower bound confidence interval (LBCI) at a 90 percent confidence level as a decision criterion for accepting or rejecting qualified high bids on tracts offered in OCS oil and gas lease sales. Following extensive testing of the alternative approaches using both historical and current lease sale tract data and existing BOEM cash flow simulation models, BOEM determined that the LBCI approach would be the most appropriate substitute for the delayed valuation methodology. The LBCI is a statistical concept that captures the lower bound of a range of values encompassing the true unknown mean of the risked present worth of the resources at the time of the lease sale. The LBCI incorporates the uncertainty of parameters unique to the valuation of each OCS oil and gas lease sale tract. These parameters may include, but are not limited to, subsurface characterization of reservoir properties, cost and timing of the development, and projected revenues. Unlike the delayed valuation methodology, the LBCI approach would not require that BOEM estimate the time delay period between the current OCS oil and gas lease sale and the projected next lease sale. As such, BOEM finds the LBCI to be a better approach going forward.

BOEM published their Sale 257 Decision Matrix on Friday (2/24/2023), and my previous speculation regarding the rejected Sale 257 high bid has proven to be partially incorrect. The rejected high bid was submitted by BP and Talos and was for Green Canyon Block 777. BOEM’s analytics assigned a Mean of the Range-of-Value (MROV) of $4.4 million to that tract, which tied for the highest MROV for any tract receiving a bid. The BP/Talos bid was $1.8 million or just 40% of BOEM’s MROV. BOEM’s tract evaluation is interesting given that the other bid on this wildcat tract (by Chevron, $1.185 million) was considerably lower than the rejected BP/Talos bid.

The Sale 257 bid that I thought might have been rejected was for lease G37261. This lease was never issued per the lease inquiry data base and the final bid recap. BHP’s bid of $3.6 million for that tract (Green Canyon Block 79) was more than 5 times BOEM’s MROV of $576,000, and was accepted per the decision matrix. Why was the lease never issued?

Both Green Canyon 79 and 777 should again be for sale in legislatively mandated Sale 259, which will be held in just a few weeks on March 29, 2023, just 2 days prior to the deadline. It will be interesting to see what the bidding on those tracts looks like.

Meanwhile, Exxon and BOEM are still mum about the 94 Sale 257 oil and gas leases that Exxon acquired for carbon sequestration purposes.Note the large patches of blue just offshore Texas on the map above. These leases were all valued by BOEM at only $144,000 each, which is equivalent to the minimum bid of $25/acre. This valuation reflects the absence of perceived value for oil and gas production purposes. Exxon bid $158,400 for each tract, $27.50/acre or 10% higher than the minimum bid. Given that (1) the Notice of Sale only provided for lease acquisition for oil and gas exploration and production purposes, and (2) it was common knowledge that these tracts were acquired for carbon sequestration, should these bids have been rejected?

An international regulatory colleague brought this puzzling RigZone article to my attention. Quotes:

“From one perspective, one can look at the overall absence of risk – from this perspective, we can easily say that either the United Kingdom’s North Sea or Canada’s Nova Scotian continental shelfis the safest region for offshore oil and gas operations right now,” Robak told Rigzone.

“Canada’s offshore industry accounts for approximately one million barrels per day, and its geographic location along the Nova Scotian continental shelf has been a benefit in that there is little to no risk to its continued operation on a day-to-day basis,” Robak said.

Comments:

Scotian shelf production ceased in 2018. All facilities were fully abandoned and decommissioned by November 2020. So yes, Scotian shelf oil and gas operations are the safest in the world, along with operations in the US Atlantic and other regions where there is zero activity.

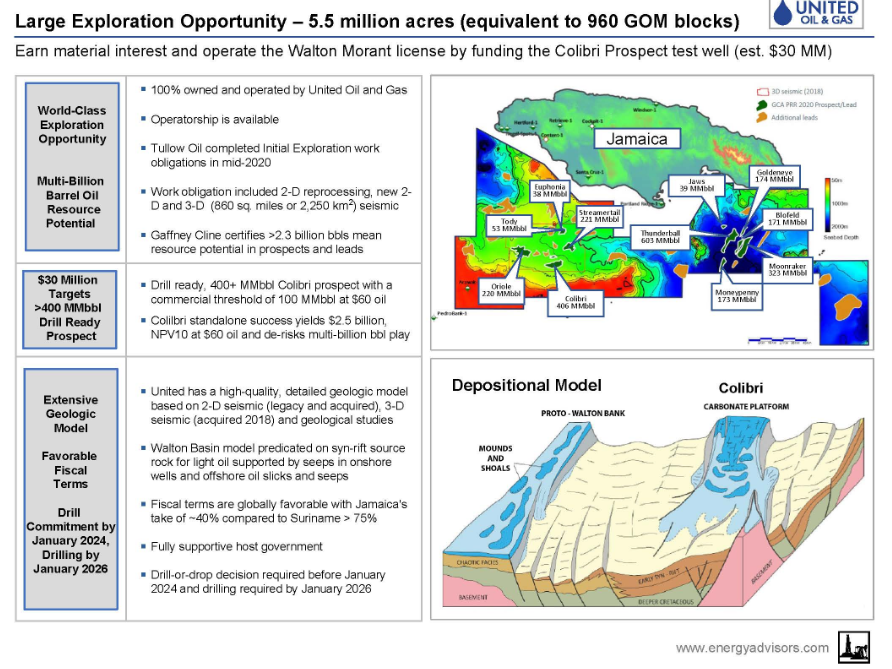

Gaffney, Cline & Associates have audited the drill-ready target prospect with mean resources of 400 MMbbls

Standalone success on hitting the mean target is expected to achieve NPV10 of $2.5 billion at $60 oil

The test well cost is estimated to be $30 million and provides exposure to own a material interest in the entire license

The initial target is a carbonate platform and shows strong evidence of reservoir trap and intact seal, Cretaceous kitchen source and live oil seeps

Recent advanced seismic relative dispersion technical work provides further evidence of reservoir porosity and permeability, the presence of a seal, and additional reservoir potential

The License, formerly owned by Tullow, is well-supported by the Jamaican government with attractive fiscal terms

While it’s highly unlikely that wind turbine siting activities are responsible for the alarming number of whale deaths, some of the vociferous wind industry defenders would have been among the first to point the finger at oil and gas operations if there were any in the US Atlantic.

Some quotes from a recent USA Today article followed by BOE comments:

“It’s just a cynical disinformation campaign,” said Greenpeace’s oceans director John Hocevar. “It doesn’t seem to worry them that it’s not based in any kind of evidence.” (Comment: World class chutzpah on the part of Greenpeace, the master of disinformation.)

Gib Brogan, a campaign director with Oceana, an international ocean advocacy group, said those opposed to wind power are using a spate of whale deaths in the area as an opportunity. (Comment: Does Oceana suddenly find this type of opportunism to be shocking?)

“Groups opposed to clean energy projects spread baseless misinformation that has been debunked by scientists and experts,” said JC Sandberg, chief advocacy officer with the American Clean Power Association, a renewable energy trade group. (Comments: Use of the term “clean energy” is clever advocacy that serves to discredit other forms of energy. All energy sources have pros and cons, environmentally and otherwise. Wind and solar have significant visual, space preemption, navigation, wildlife risk, and intermittency issues, and are heavily dependent on subsidies and mandates. When all issues are considered, one could argue, as we have, that offshore gas, particularlynonassociated gas, is perhaps the environmentally preferred energy alternative.)