Tyler Priest, the leading historian on US offshore oil and gas operations, has published another gem. His book, Offshore Oildom, is a fascinating account of the history of the technologically innovative and economically important, yet highly controversial, OCS Oil and Gas program. His bookis highly recommended.

Consider this recommendation by Daniel Yergin:

“Tyler Priest, a preeminent historian of energy and the environment, explores how a single well drilled off a pier near Santa Barbara in 1898 gave rise to a major American industry—offshore oil and gas. In spirited prose, Priest demonstrates how this U.S. industry was created not only by innovation, creative engineering, and complex execution; it was also the result of fierce political battles.” ~Daniel Yergin, Pulitzer Prize–winning author of The Prize: The Epic Quest for Oil, Money, and Power and The New Map: Energy, Climate, and the Clash of Nations

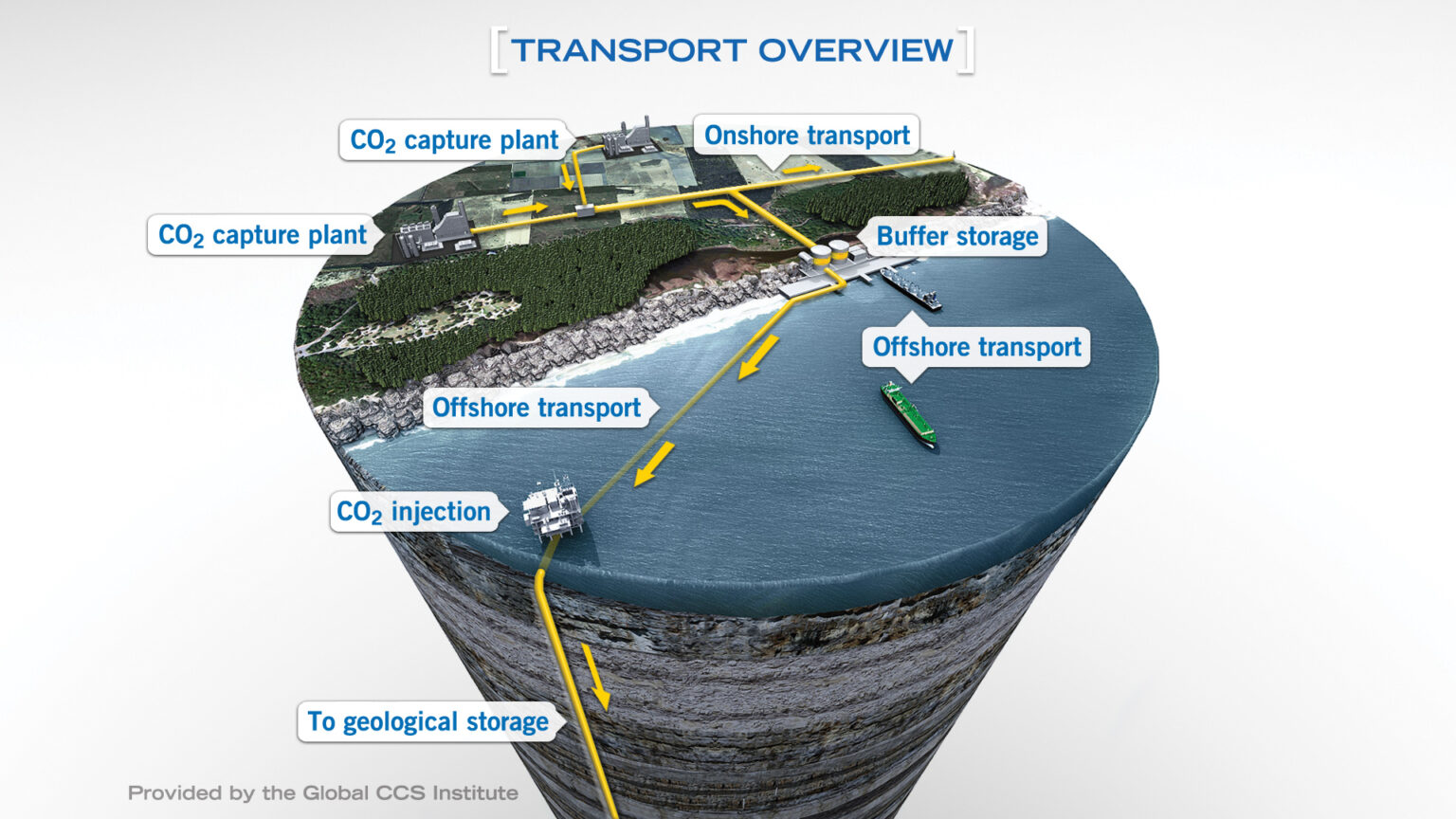

Unsurprisingly, the carbon capture and sequestration (CCS) hype is fading fast. No other carbon strategy is so strongly opposed by both climate change activists and skeptics.

Support for CCS seems to be limited to those seeking to profit from subsidies, mandates, and disposal fees. In 2022, Exxon projected a $4 trillion CCS market by 2050. Pipe dream?

“Highlights” of the Gulf of America OCS carbon disposal era:

amended the OCS Lands act to authorize “the injection of a carbon dioxide stream to sub-seabed geologic formations for the purpose of long-term carbon sequestration.”

exempted CO2 injection from the restrictions on ocean dumping by stipulating that such injection “shall not be considered to be material (as defined in section 3 of the Marine Protection, Research, and Sanctuaries Act of 1972.” Without this exemption, CO2 streams would clearly be “material,” as defined in 33 U.S.C. 1402, and would be subject to the stringent requirements of that act.

directed that “not later than 1 year after the date of enactment of this Act, the Secretary of the Interior shall promulgate regulations to carry out the amendments made by this section.” (This deadline is long past, which is not uncommon for such legislative directives.)

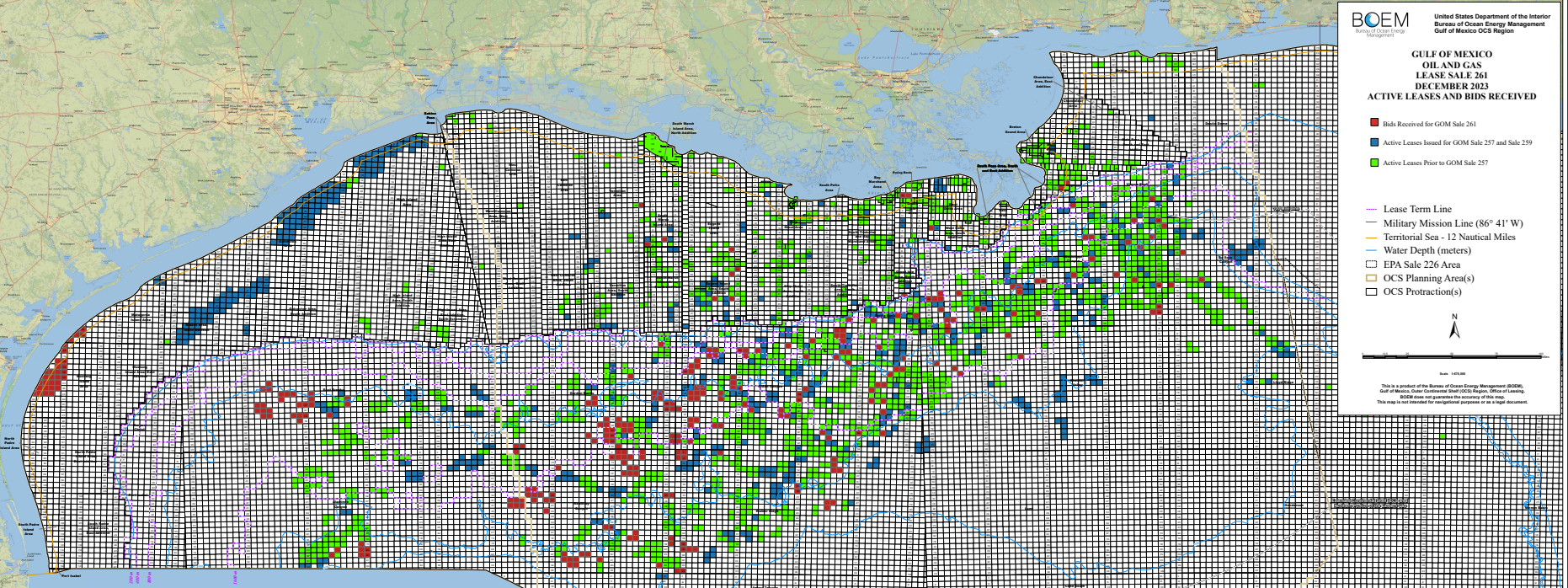

11/17/2021: Not coincidentally, two days after the enactment of this legislation, Exxon was the sole bidder on 94 nearshore tracts with very limited oil and gas production potential. This was an oil and gas lease sale and there were no provisions for carbon sequestration leasing. Nonetheless, Exxon was awarded leases for all 94 tracts. As a result of litigation delaying the issuance of Sale 257 leases until Oct.1, 2022, those 5 year leases will expire in 2027.

3/29/23: Exxon bid at Sale 259 on 69 nearshore tracts with little oil and gas potential. Once again, this was strictly an oil and gas lease sale and Exxon’s CCS intentions were clear. Nonetheless, the leases were awarded.

6/25/2025: For the first time ever, the Federal government felt compelled to stipulate the obvious (proposed lease sale notice for OCS Sale 262) – that an Oil and Gas Lease Sale is only for oil and gas exploration and development.

Gulf of America lease map: 199 oil and gas leases were wrongfully acquired for carbon disposal purposes. At Sale 261, Repsol acquired 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon had acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

Even those of us who are supporters of responsible offshore oil and gas production find it a bit unsavory that some companies are looking to cash in on (and virtue signal about) carbon collection and disposal at the public’s expense. Perhaps companies that believe oil and gas consumption is harmful to society should be seeking to reduce production rather than engaging in enterprises intended to sustain it.

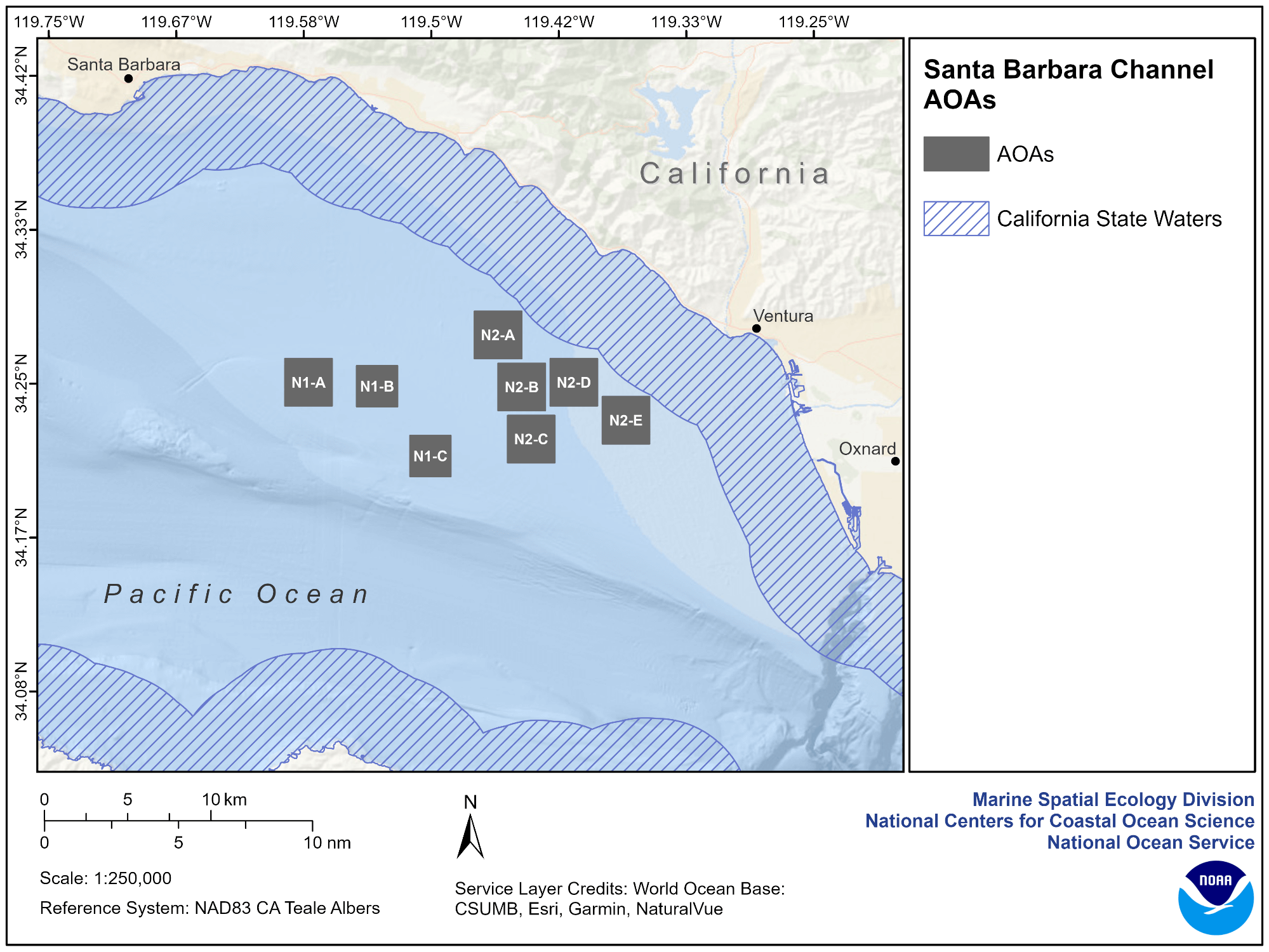

NOAA is touting marine aquaculture and has published Programmatic Environmental Impact Statements for Aquaculture Opportunity Areas (AOAs) in the Gulf of America and offshore Southern California. This is a positive step.

While the focus of these EIS documents is on distinct AOAs separated from oil and gas facilities, NOAA might also have discussed the potential for synergy with existing platforms. The reef effect of platforms can be sustained and new fishery ventures supported by converting older platforms to aquaculture facilities (Rigs-to-Roe/Redfish/Rockfish) rather than decommissioning them.

According to a paper published in 2014 by marine ecologist Dr. Jeremy Claisse of Cal Poly Pomona, the oil and gas platforms off the coast of California are the most productive marine habitats per unit area in the world. “Even the least productive platform was more productive than Chesapeake Bay or a coral reef in Moorea,” said Dr. Love. (Milt Love, UCSB biologist)

…and should be an integral part of Job Safety Analyses!

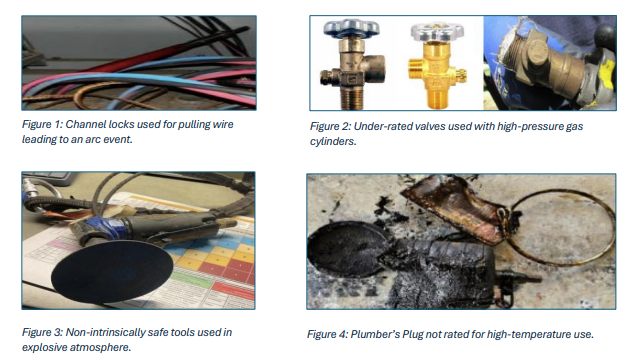

According to BSEE, there is a recurring trend of equipment misuse contributing to fire and explosion hazards during offshore oil and gas operations in the Gulf of America.

Workers have used tools not rated for electrical work on live circuits (Figure 1) and mismatched hydraulic or pneumatic tools for high-pressure systems (Figure 2). In several cases, non-intrinsically safe hand tools were used in explosive atmospheres, including mudrooms and drilling floors.

The latest Baker Hughes Rig Count Report shows only 10 rigs actively drilling in the Gulf. All are at deepwater locations – 7 in the Mississippi Canyon area, 2 in Green Canyon, and 1 in Alaminos Canyon. Per the BSEE borehole file, Shell accounts for most of the current MS Canyon wells and the Alaminous Canyon well. Beacon is also drilling in the MS Canyon, and the Green Canyon well appears to be a Chevron operation.

Only Anadarko/Oxy, Beacon/BOE, BP, Chevron/Hess, Shell, and Talos have spudded deepwater exploratory wells in 2025 YTD. Arena and Cantium are the only shelf drillers – all development wells.

Technological advances and extensions of past discoveries have sustained Gulf production, but declines are certain over the longer term if drilling activity doesn’t increase. Oil price uncertainty is an issue, but that’s always the case. Semiannual lease sales are now legislatively required and the terms will be attractive, so those issues are off the table. Let’s see what the bidding looks like at the upcoming sale.

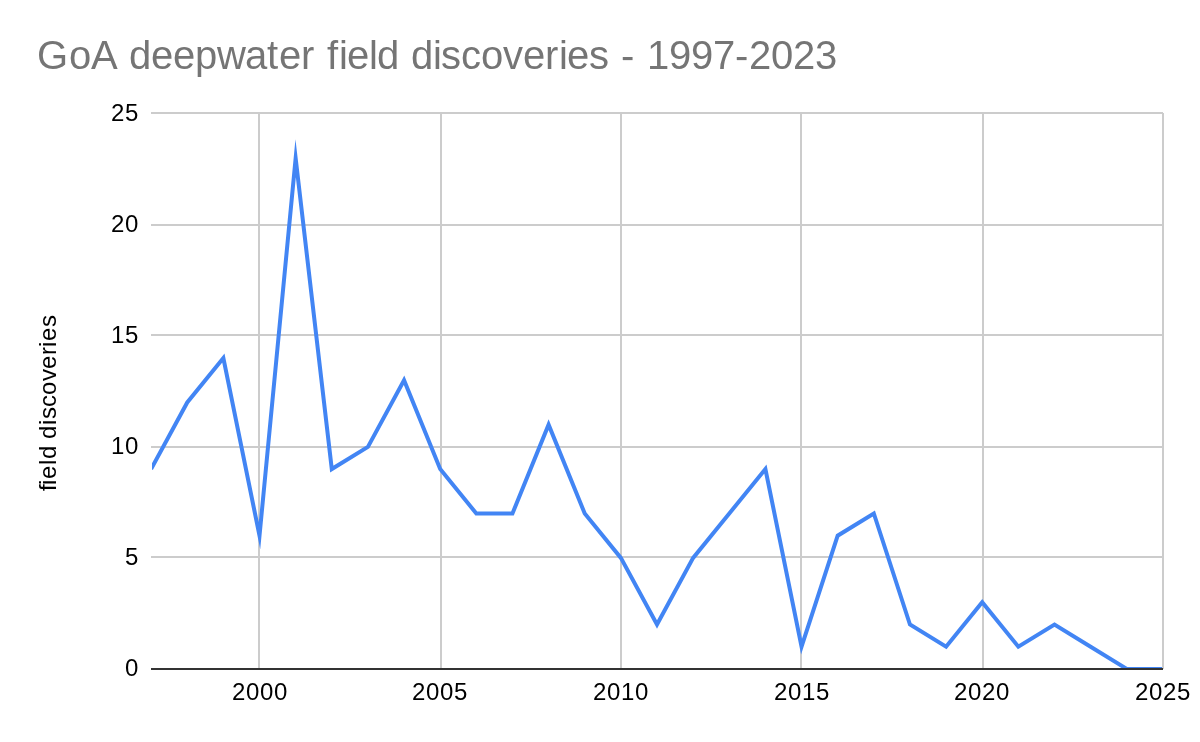

The decline in deepwater discoveries (BOEM data below) is particularly discouraging. Per BOEM, the last deepwater field discovery was in March 2023.

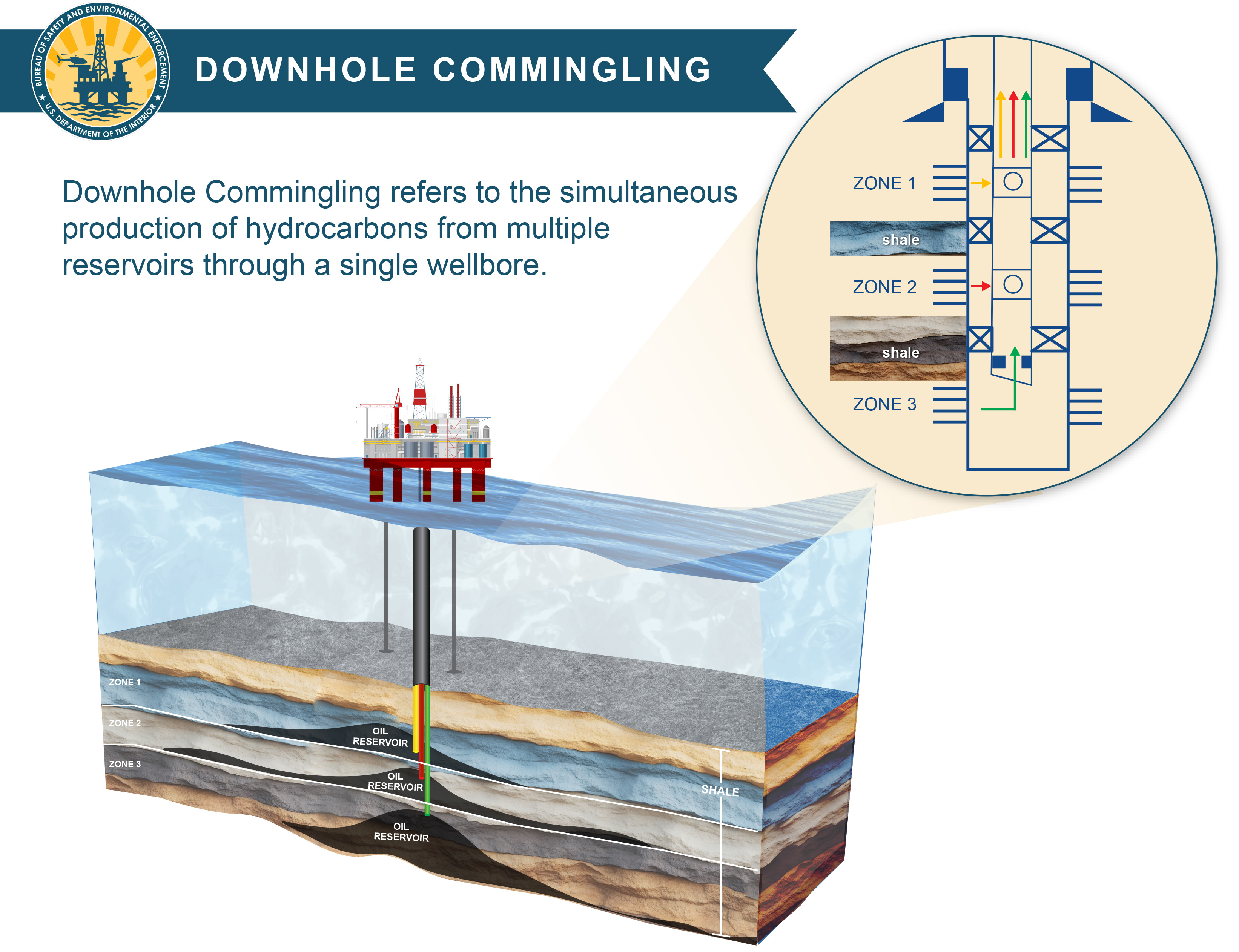

The “One Big Beautiful Bill Act of 2025” (OBBB), Public Law 119-21, which was signed into law on July 4, 2025, includes a significant offshore production directive (section 50102) that has received little public attention:

“The Secretary of the Interior shall approve a request of an operator to commingle oil or gas production from multiple reservoirs within a single wellbore completed on the outer Continental Shelf in the Gulf of America Region unless the Secretary of the Interior determines that conclusive evidence establishes that the commingling—(1) could not be conducted by the operator in a safe manner; or (2) would result in an ultimate recovery from the applicable reservoirs to be reduced in comparison to the expected recovery of those reservoirs if they had not been commingled.”

This is, to the best of my knowledge, the first time in the history of the OCS oil and gas program that Congress has directed the safety regulator to approve well completion practices that could increase safety, environmental, and resource conservation risks.

Rather than calling for the operator to demonstrate that a downhole commingling plan is safe and optimizes resource recovery, the plan must be approved unless BSEE proves conclusively that the operation could not be conducted safely or that resource recovery would be reduced. This is the antithesis of the operator responsibility doctrine, a fundamental principle of the OCS regulatory program, and safety management principles that call for the operator to demonstrate that safety, environmental, and resource conservation risks have been effectively addressed.

Only 40 days after the OBBB was signed, BSEE published a direct final rule implementing the downhole commingling directive. This is warp speed for promulgating a Federal regulation! In keeping with the rush to finalize the rule, the preamble asserts that “notice and comment are unnecessary because this rule is noncontroversial; of a minor, technical nature; and is unlikely to receive any significant adverse comments.”

I intend to submit comments prior to the Sept. 12 deadline. These comments will assert that the rule does not qualify for an exemption from the Administrative Procedures Act’s public review and comment requirement. I will also recommend that BSEE consider hosting a public forum during the comment period to present their research on downhole commingling and discuss the risk mitigations.

Below are some of the issues/questions that should be considered during the public comment period:

BSEE’s own fact sheet acknowledges the well-known pressure differential, crossflow, and fluid compatibility risks associated with downhole commingling. The public should have the opportunity to provide input on the extent to which “intelligent completions” and other production technology are effective in mitigating these risks.

The industry-funded Univ. of Texas (UT) study, which led to a relaxation of downhole commingling restrictions, was specific to the “unique Paleogene Gulf of Mexico fields.” Does BSEE have evidence that supports the applicability of the study to other fields?

The authors of the UT study acknowledged that their findings were based on a “simple but reasonable geological base case model.” They also acknowledged the need for “a more comprehensive study using advanced geological models to explore additional geological features.” What are BSEE’s plans for additional research?

Should an independent assessment of Gulf of America downhole commingling safety and resource recovery risks be conducted before finalizing a rule that essentially mandates approval of all applications?

BSEE’s April 2025 policy change raised the allowable pressure differential for commingling production in Paleogene (Wilcox) reservoirs from 200 psi to 1500 psi. Unlike the policy update, the new rule includes no boundaries whatsoever.

What criteria will BSEE use in determining that there is “conclusive evidence” that a commingling request would be unsafe or would reduce ultimate resource recovery? Will BSEE disapprove any requests outside the parameters in the current policy guidance or subsequent updates?

There are many more issues that remain to be discussed, which is why the downhole commingling rule should be published in draft form, with a comment period of at least 90 days.

We preferred the House version, but the Senate Parliamentarian killed the provisions that reduced the risk of litigation and processing delays.

Whether justified or not, the royalty rate is now capped at 1/6 and a 10-year deepwater lease term is locked in.

The favorable terms and assurance of regular GOA lease sales put the ball squarely in industry’s court. We are looking for a good showing at Sale 262, including some new bidders and the return of some prominent companies.

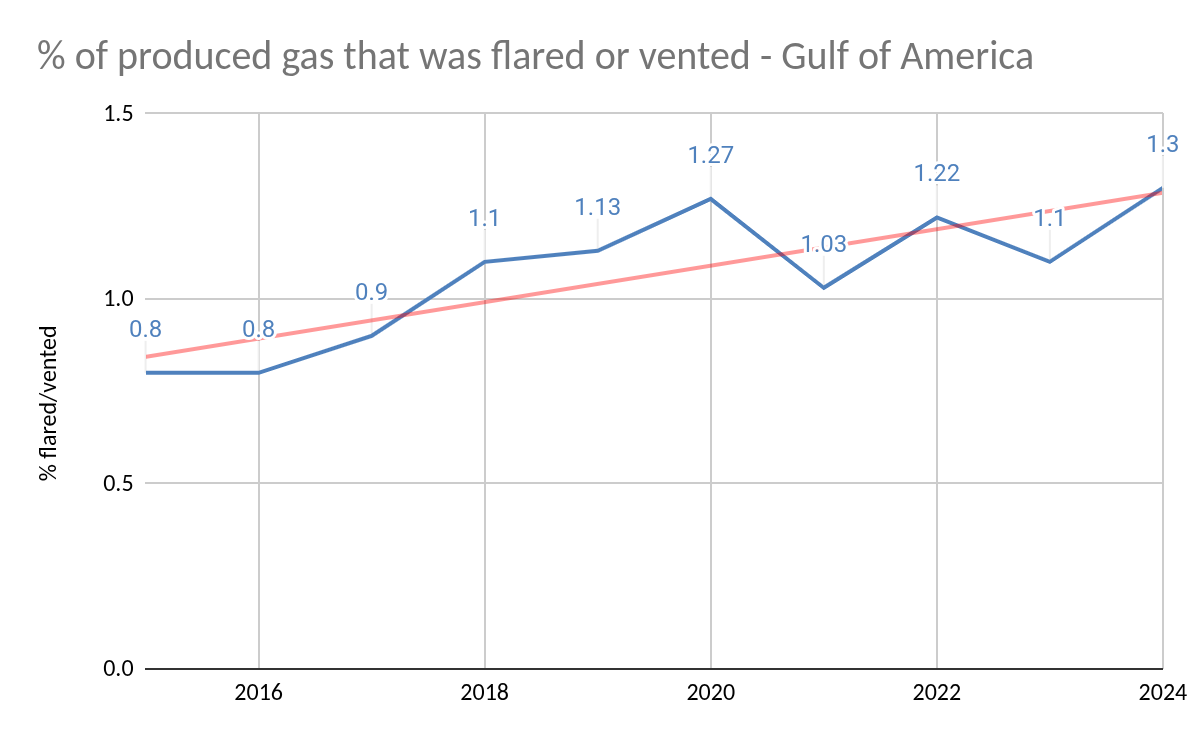

As the chart indicates, the % of flared or vented Gulf of America gas production increased over the past 10 years. This trend is presumably due, at least in part, to the sharp increase in the % of gas production from oil wells (associated gas), which have a higher flaring rate. In 2024, 87% of Gulf gas production was from oil wells.

Flaring/venting summary tables and comments, updated through 2024, will be posted later in the week.

The Safety Alert is attached. Per BSEE, the fires resulted from an accumulation of gas caused by improperly installed or disconnected exhaust vent piping on gas starters.

Incident 1: Two workers sustained burns to the hands, arms, and face. BSEE investigators discovered that the engine’s air intake hose was disconnected, which may have allowed gas-enriched air to be drawn into the carburetor causing the backfire.

Incident 2: While attempting to start the gas engine of a pipeline pump, the lead mechanic sprayed ether into the engine’s carburetor. The exhaust vent piping for the starter had not been installed. The combination of the gas-rich atmosphere and ether caused the engine to backfire and ignited the accumulated gas. The lead mechanic, sustained burns to his face, arms, and hands.

The Alert includes important recommendations for proper venting, mechanical integrity awareness training, maintenance, and the use of gas detectors and a temporary fire watch during engine startup.