SANTA BARBARA, Calif. — A controversial oil project on California’s Central Coast remains unresolved after the Santa Barbara County Board of Supervisors deadlocked 2-2 on a vote regarding a permit transfer for a pipeline linked to the 2015 Refugio oil spill. The stalemate means Sable Offshore Corp.’s application remains pending without approval or denial, leaving the next steps up to the company.

“They still have a pending application with no action taken on it,” said Kelsey Gerckens Buttitta, public information officer with Santa Barbara County. “It hasn’t been approved or denied. It’s now up to Sable to decide what to do next.”

The Board voted 2-2 to uphold the approval of the transfer of permits from Exxon to Sable. The tie vote meant the appeal of the previous approval failed.

Interestingly, one of the Supervisors reportedly slammed the California Coastal Commission for being politically motivated and abusing the law.

This will be the Board’s “first and last chance to have any influence over restarting the pipeline, and thus allowing the three offshore platforms to begin drilling again.” (Expect initial production to be from existing wells supplemented over time with new drilling, well workovers, and recompletions.)

The Board has limited authority in this matter: “The county’s legal advisors and energy planners have told the supervisors that there are no grounds to say no. It is not up to them to determine whether Sable’s liability insurance is enough to cover the costs of a reasonable worst-case oil-spill scenario; it’s only up to them to ascertain whether Sable has filed a certificate of insurance with the proper state agency.“

“All the essential questions regarding the pipeline’s safety measures are in the hands of California state agencies, headquartered in cities far away, with names so confusing that even people working there can’t tell you what the acronyms mean.” (see Regulatory fragmentation)

Interesting tidbits: “Danielson (the Sable representative) let me know that he would not be answering these questions. He was cordial, but he was not happy about a recent Independent story featuring attorney Linda Krop of the Environmental Defense Center perhaps Sable’s most implacable and formidable opponent, expounding in an unchallenged format on what a threat the pipeline still posed. Interviewing Krop was Victoria Riskin, herself a committed anti-oil advocate. Actress and Montecito resident Julia Louis-Dreyfus — of Seinfeld and Veep fame — apparently liked the article enough to send it to her social media followers.“

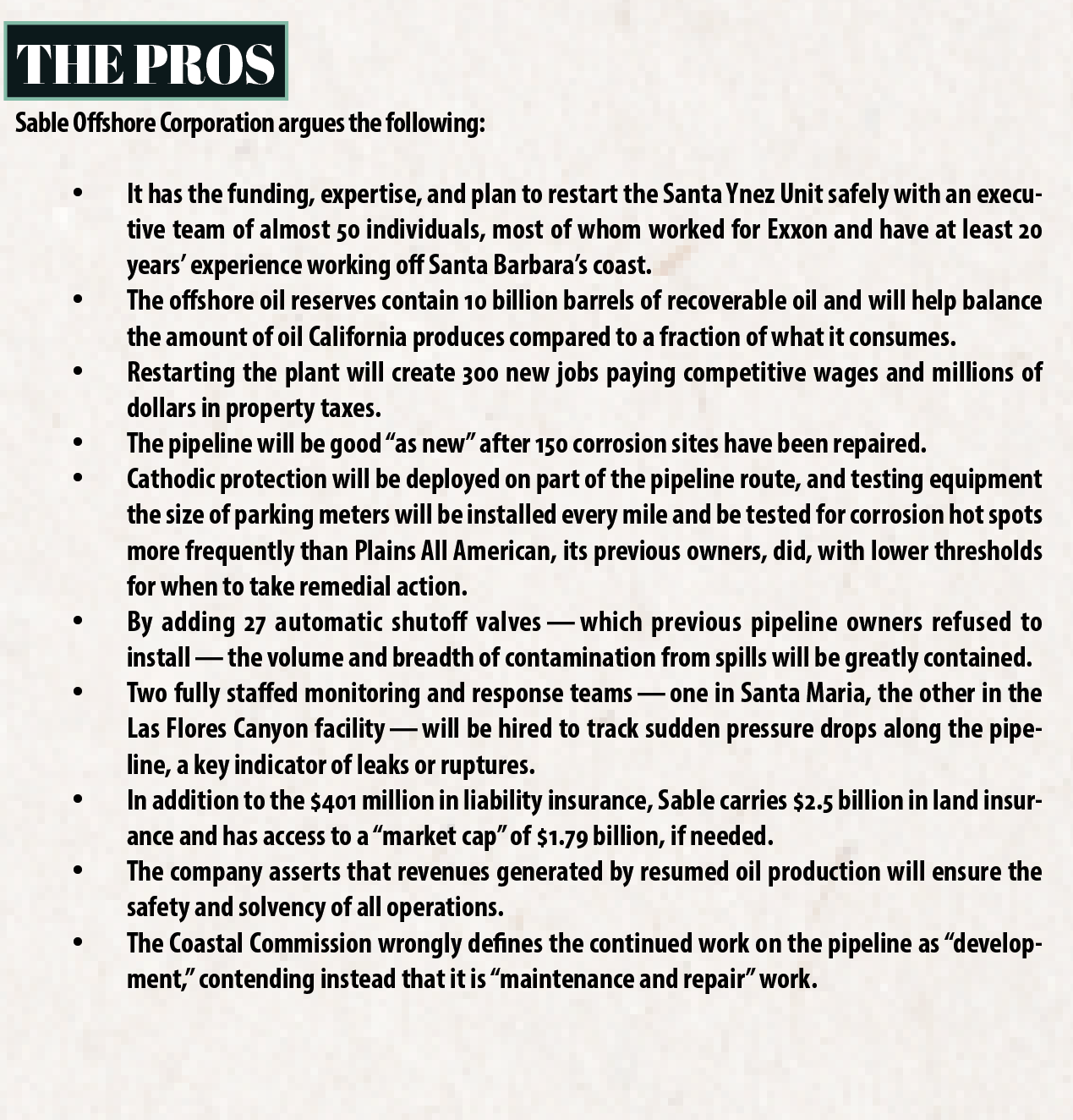

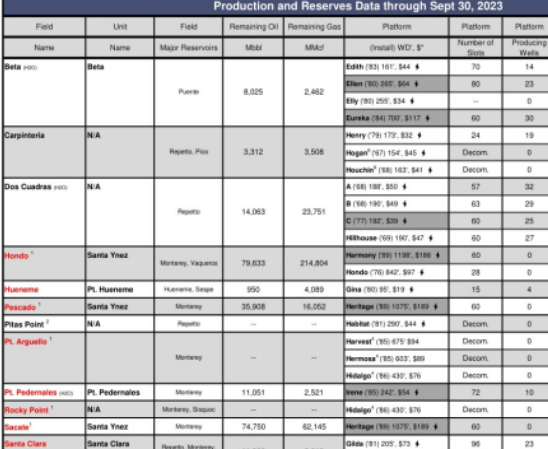

Below are the pros and cons of the SYU restart as cited by the Independent. (Clarification: The 10 billion bbl oil reserves number (“pros” slide) is at least an order of magnitude too high and is perhaps a typographical error. BSEE’s June 2023 data sheet (excerpt pasted at the end of this post) indicates remaining oil reserves of 190 million bbls for the 3 SYU fields. Adding the gas reserves ups the total to 243 million bbls of oil equivalent (boe). Additional reserves could likely be confirmed with new extended reach wells, but anything more than 1 billion bbls would be highly unlikely. Sable’s investor presentation (p.5) indicates 646 million bbl of Remaining Total Net Estimated Contingent Resources.)

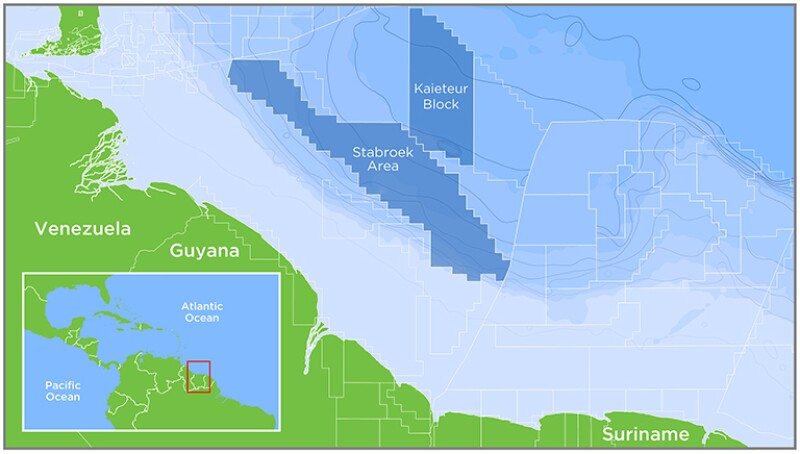

Chevron is not buying the Stabroek share; they are buying the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership.

As an offshore operator, Exxon has been highly responsible from a safety standpoint. However, the company is not reluctant to stretch the envelope when it comes to contract rights. The most recent example was their acquisition of 163 GoM oil and gas leases for carbon disposal purposes, contrary to the terms of the sale notice and lease contracts.

Interestingly, Exxon’s partner in this dispute is state-owned China National Offshore Oil Corporation. CNOOC acquired their 25% Stabroek share when they purchased Nexen, a Canadian company (sound familiar?). Both the Canadian and US governments had reservations about this acquisition and nearly nixed the deal. Would either government bless that acquisition today?

An International Chamber of Commerce arbitration panel will hear the Stabroek case in May 2025, and the final decision is expected by September 2025.

Exxon CEO Darren Woods’ is concerned that US withdrawal from the Paris climate agreement would threaten carbon capture and sequestration (CCS), the foundation for which is government mandates and generous taxpayer subsidies.

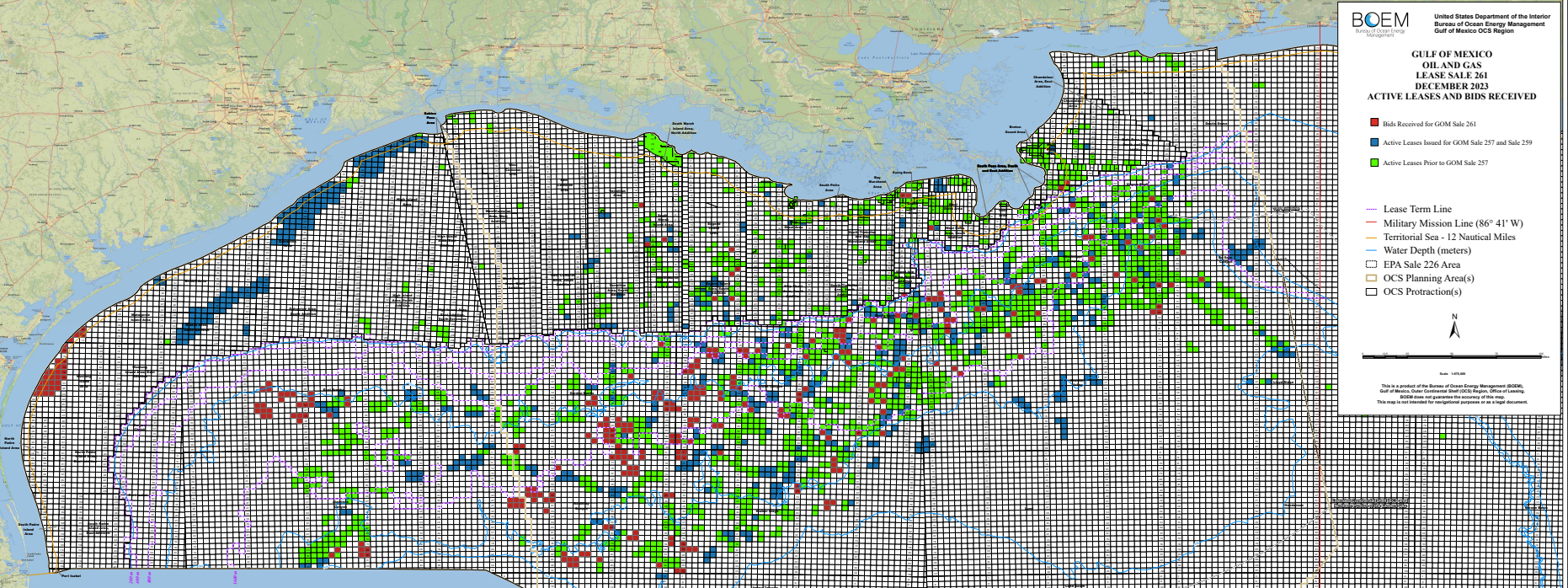

Exxon sought an edge over CCS competitors by improperly acquiring 163 OCS oil and gas leases (map below) for carbon disposal purposes. Conversion of these leases is not authorized, which means they will expire at the end of their primary (5 year) term absent legislative or regulatory action.

The only solid support for CCS is from companies hoping to benefit from subsidies and charges to industries and individual energy consumers. It’s time to end the Federal government’s CCS programs.

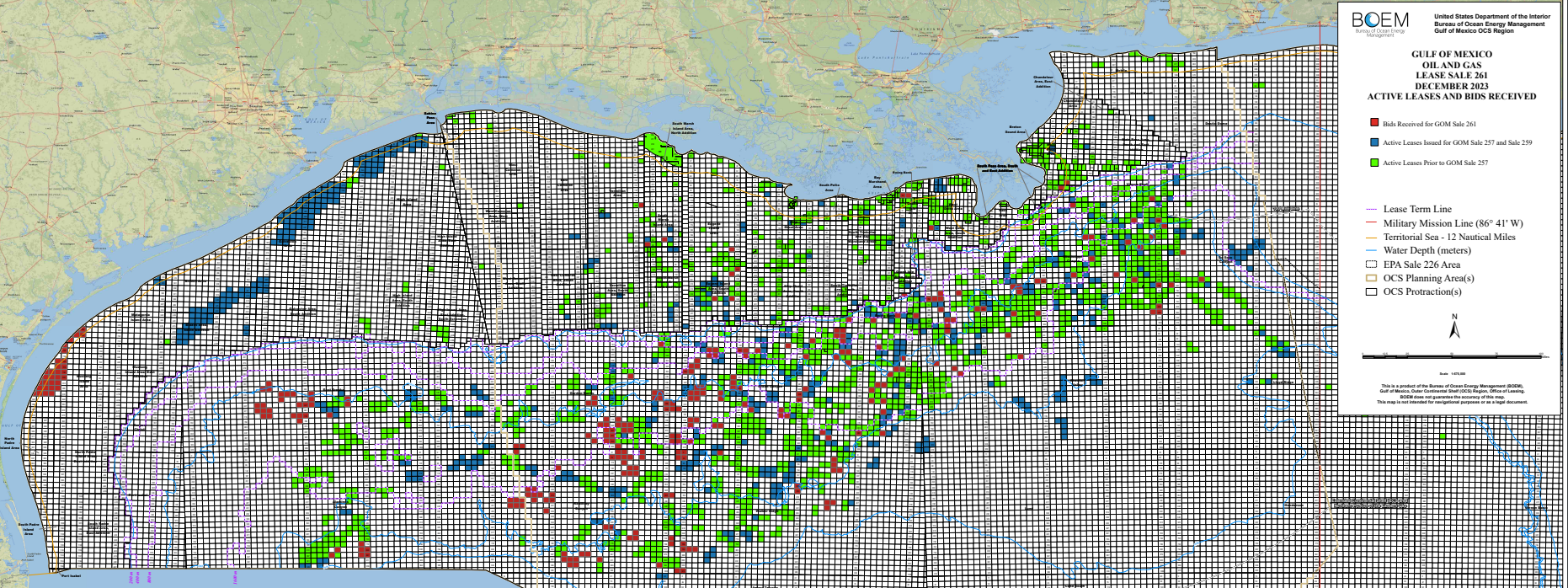

199 oil and gas leases were wrongfully acquired at Sales 257, 259, and 261 with the intent of developing these leases for carbon disposal purposes. Repsol was the sole bidder at Sale 261 for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

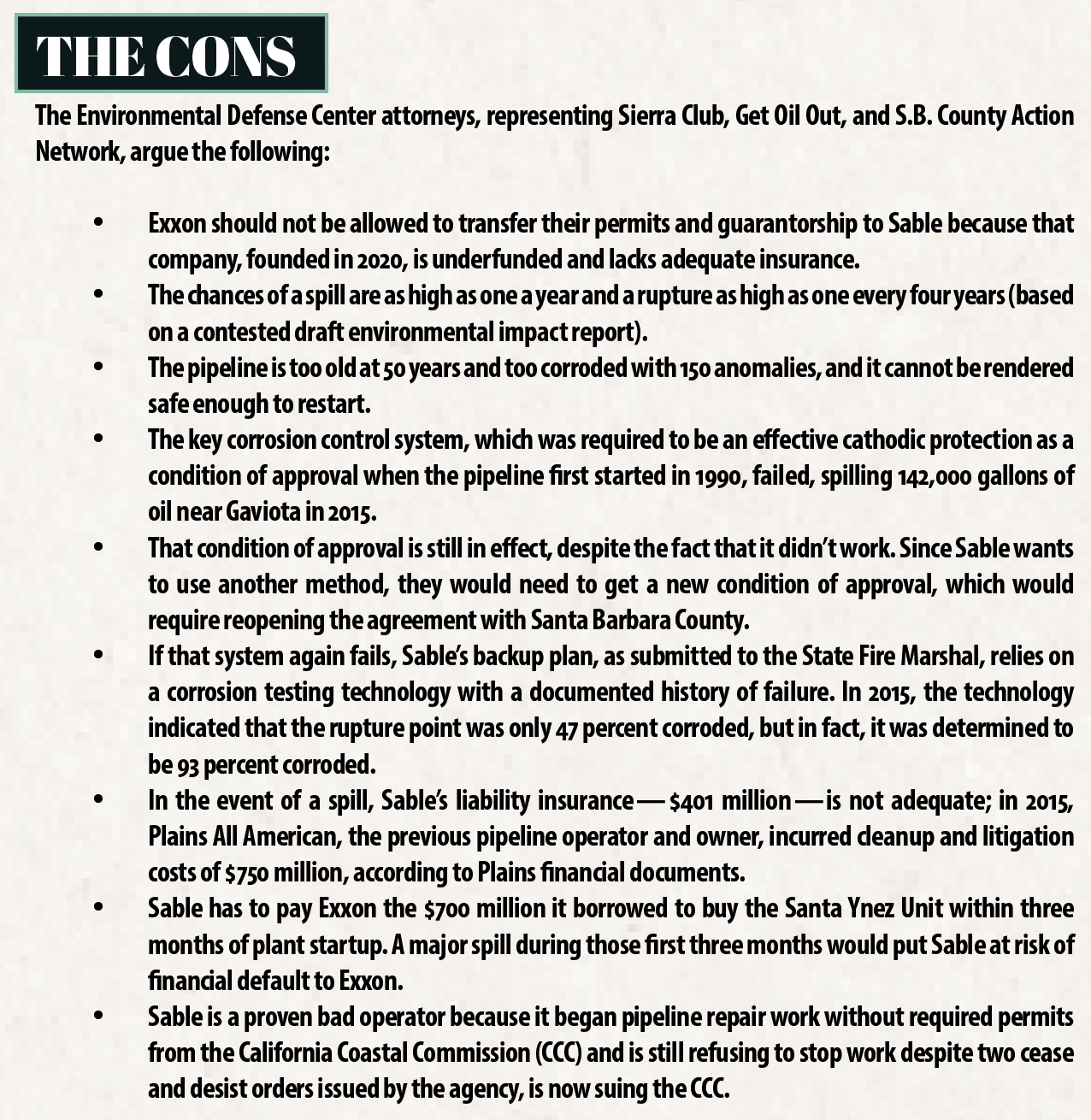

The Santa Barbara County Planning Commission has approved the transfer of the onshore pipeline from Exxon to Sable Offshore. Although the Environmental Defense Center (EDC) is appealing that decision to the Board of Supervisors, the Board’s vote will likely be a 2-2 tie. Supervisor Hartmann’s property is close to the pipeline and she has recused herself from votes on the matter. A 2-2 vote would be a win for Sable, because a tie vote means the planning commission decision stands.

As an investment, Sable is a “pure California permitting play,” which means the risks are high. The company’s chances for success are almost entirely dependent on receiving the necessary approvals from State and local agencies.

Sable’s share price soared to $23.43 on 9/3 after the company reached agreement with Santa Barbara on the installation of required pipeline valves. The price bounced further to $28.30 on 9/19 before falling sharply to $19.43 on 10/9 after being cited for failing to get California Coastal Commission approval to install the required valves. The price rebounded to $24 following the County Planning Commission’s approval of the transfer from Exxon to Sable before settling at $23 on Friday, the date of the EDC appeal.

Expect the financial and psychological roller coaster ride to continue.

199 oil and gas leases were wrongfully acquired at Sales 257, 259, and 261 with the intent of developing these leases for carbon disposal purposes. Repsol was the sole bidder at Sale 261 for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

Despite false starts by Exxon and Repsol (see above summary), no carbon sequestration (disposal) leases may be issued or developed until implementing regulations have been promulgated. In that regard, no news is good news for those who are less than enamored with CO2 disposal in the Gulf of Mexico.

The implementing regulations will be controversial. Most operating companies prioritize GoM production over GoM disposal. Most environmental organizations are strongly opposed to CO2 disposal schemes that sustain fossil fuel production and benefit fossil fuel producers. Taxpayers are leery of subsidizing these projects and absorbing increased costs for energy and consumer goods.

The Administration is, of course, well aware of this opposition and will not be publishing implementing regulations prior to the election. The next Administration, regardless of the election outcome, will no doubt take a hard look at these issues before proposing regulations.

The few oil and gas producers that are rather cynically hoping to cash in on CO2 disposal in the GoM will therefore have to wait, perhaps for a long time.

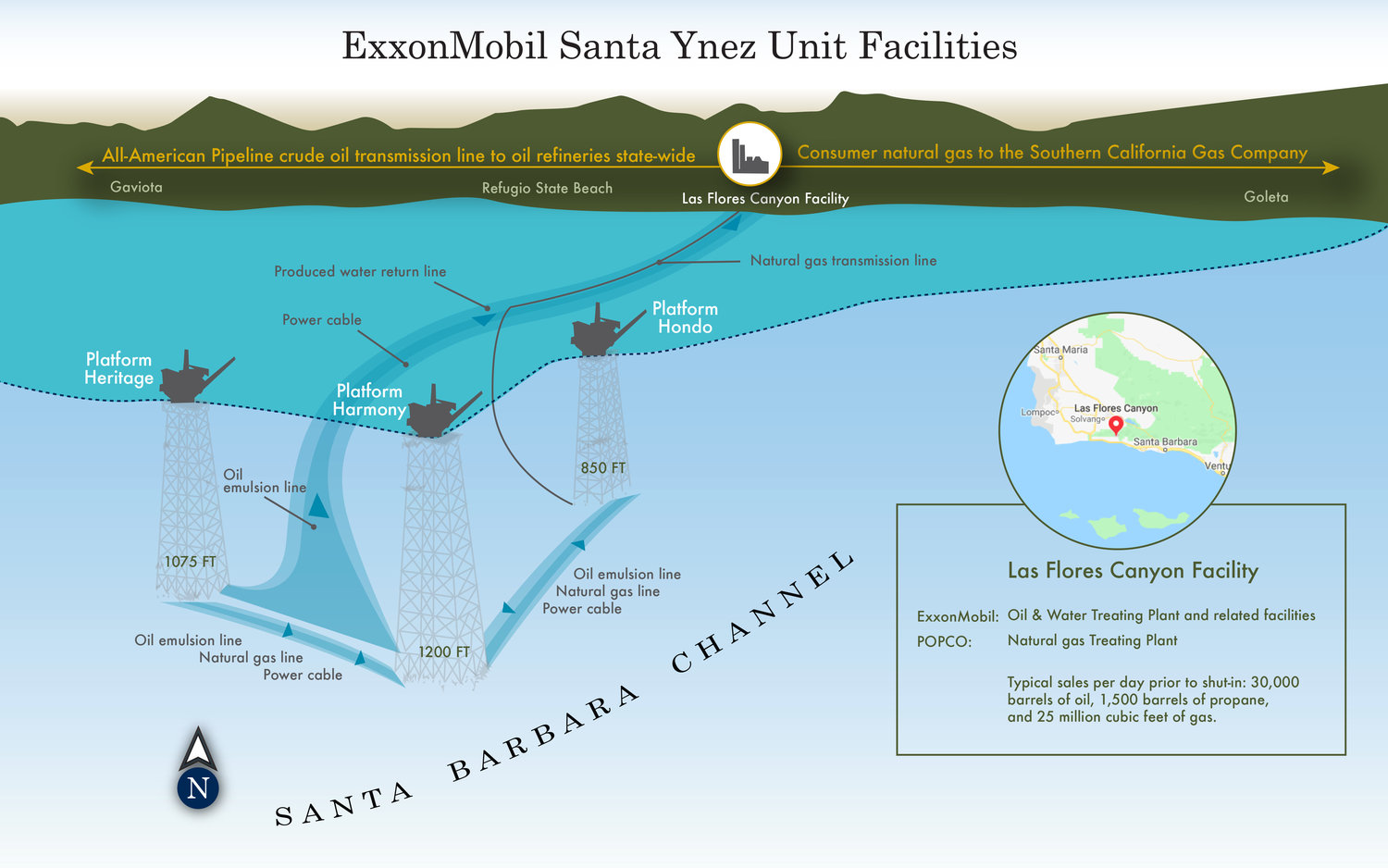

Platform Holly, California State waters in the Santa Barbara Channel, formerly operated by Venoco

Platform Holly sits immediately offshore from the Univ. of California at Santa Barbara, and UCSB scientists have studied the platform and surrounding ecology extensively. Multiple studies have shown that production from Holly reduced natural seepage and methane pollution from shallow formations beneath the Channel. Platform Holly was thus a “net negative” hydrocarbon polluter.

The natural seepage in the Santa Barbara Channel was important to the earliest inhabitants of the area. The Chumash used the tar for binding and sealing purposes, including caulking their canoes. Since Holly shut down in 2015 following the Refugio pipeline spill, offshore workers and supply boat crews have reported a considerable increase in gas seepage.

Earlier this month, it was reported that well plugging operations at Holly had now been completed, but decisions regarding the final decommissioning of the platform remain.

Venoco declared bankruptcy in 2015 and the State of California became the platform owner. According to the State Lands Commission, Exxon will pay the costs for decommissioning the platform. This is because Exxon acquisition Mobil operated the platform from 1993-1997 before Venoco became owner.

The most recent Holly development is that Venoco has settled its law suit with Plains, the company responsible for the 2015 Refugio pipeline spill that halted production from Holly. Terms of the settlement have not been disclosed.

Note: As an aside, I’m curious as to whether Mobil provided a decommissioning guarantee as part of the sale to Venoco or whether the State is simply holding ExxonMobil accountable as a legacy owner. If it’s the latter, why isn’t bp (bp acquisition Arco was Holly’s operator from 1966-1993) also liable? Is it a matter of Mobil being the more recent predecessor owner?

While exploration technology has improved significantly, the success rate for wildcat exploratory wells is still only about 30%. According to Rystad, only eight of the 27 high-impact wells drilled in 2023 resulted in commercial discoveries.

In baseball terms, the smaller independents are typically singles hitters, drilling development wells and gleaning reserves from established fields. The majors tend to be home run hitters. They swing hard and often miss, but when they hit, the rewards are great!

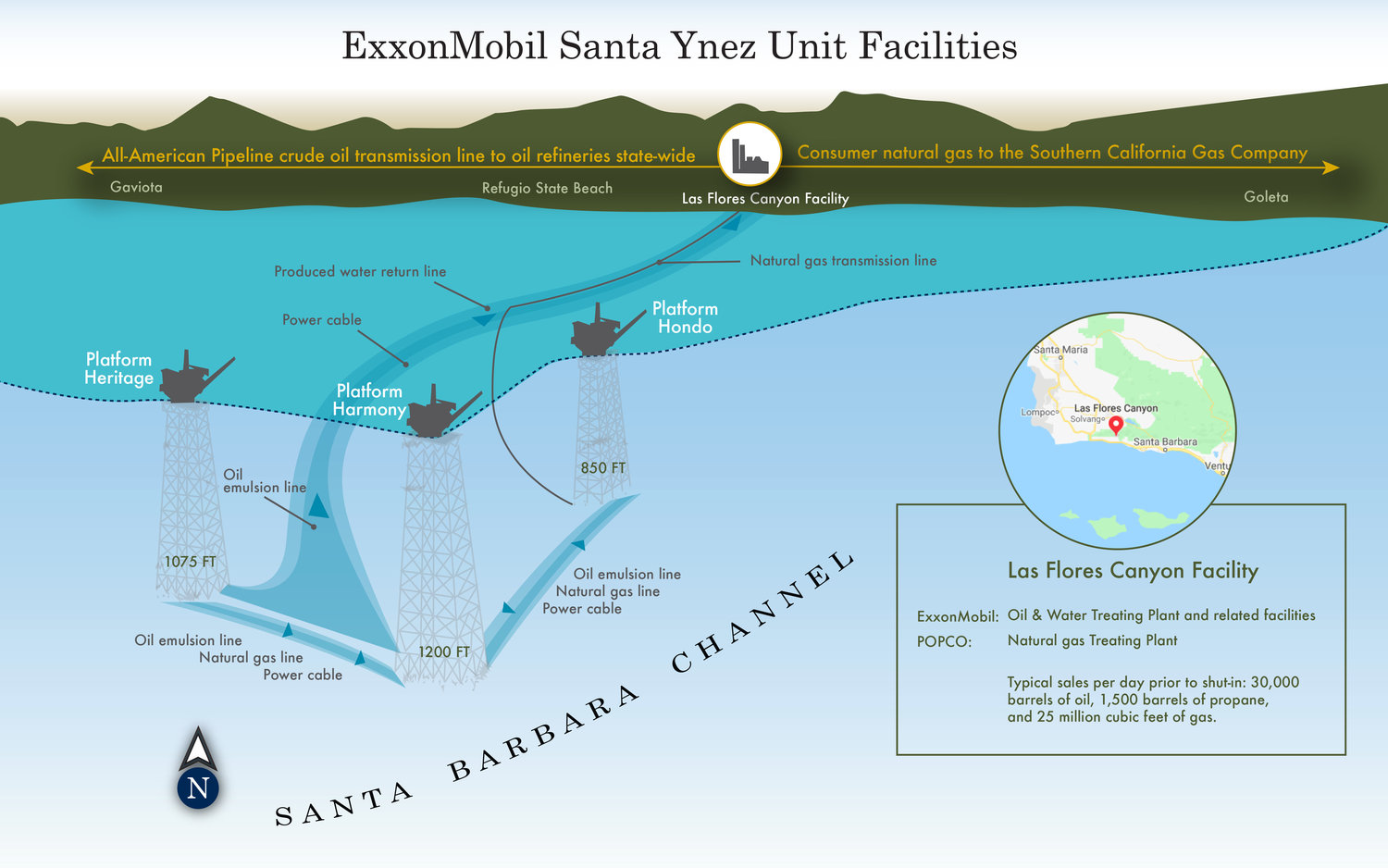

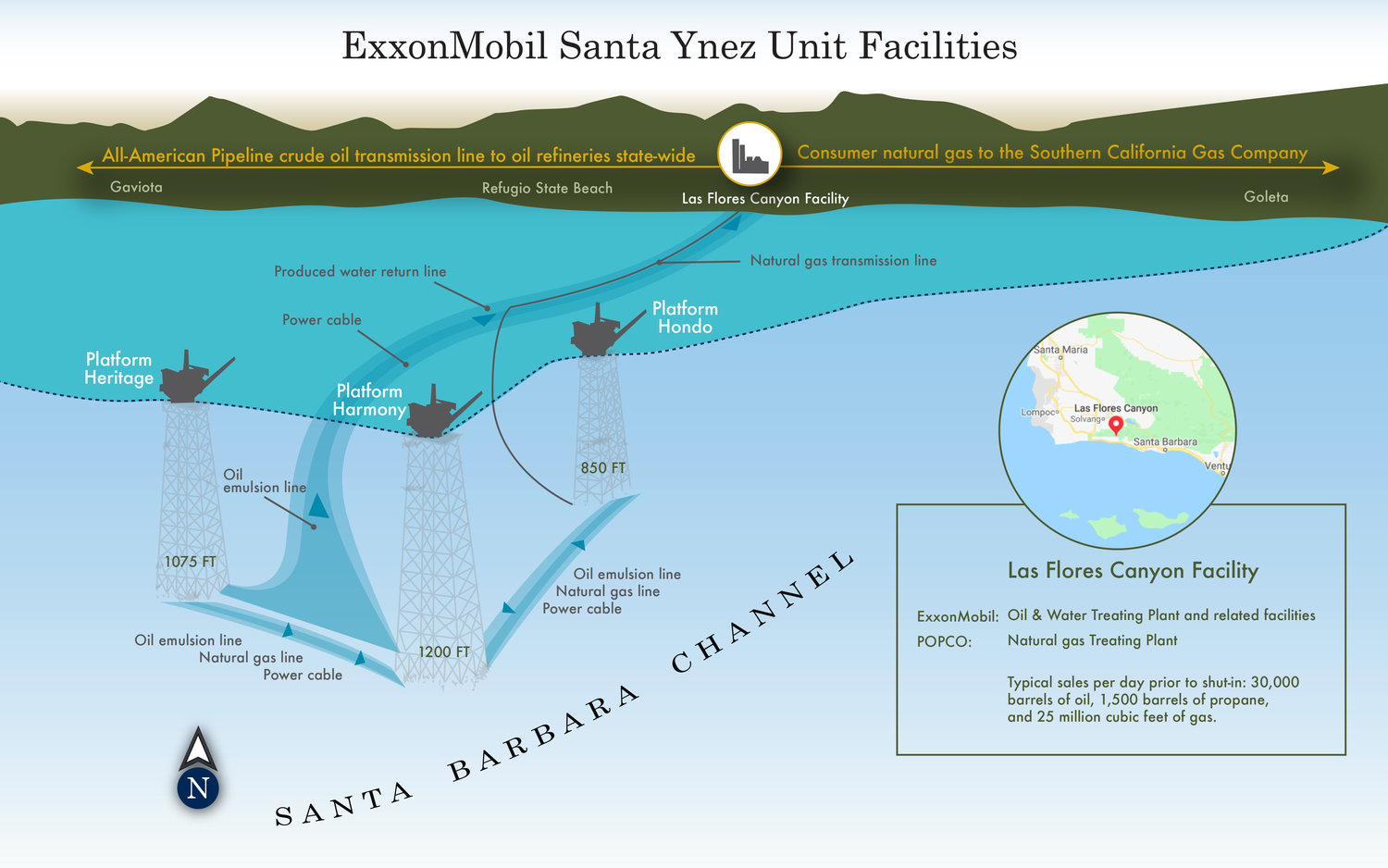

Sable’s stock price soared after the company reached an agreement with Santa Barbara County that will allow them to comply with the California Fire Marshall’s requirement to install shutdown valves on the onshore pipeline that failed in 2015. That pipeline is necessary to transport production from the Santa Ynez Unit, which is currently operated by Sable.

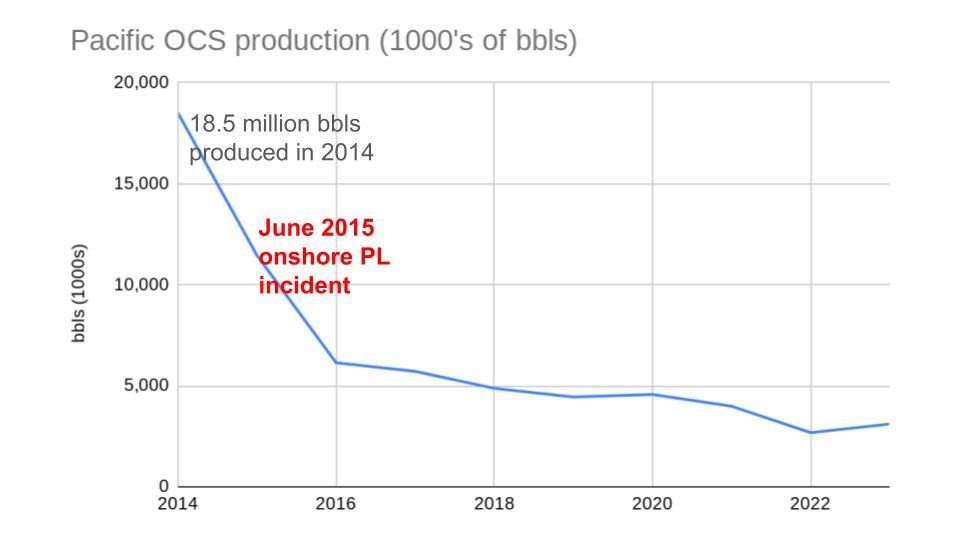

The significance of a resumption of SYU production is illustrated in the chart below. The 3 SYU platforms accounted for more than 2/3 of Pacific OCS production before the Refugio pipeline spill in June 2015.

This agreement with the County is a major step forward, but there are still regulatory and legal hurdles to clear before production resumes.

In the SEC filing that announces the agreement with Santa Barbara County, Sable affirms their 2024 restart expectations. However, a resumption of production in 2024 is highly unlikely given the administrative challenges that remain. A restart in 2025 would be a major accomplishment and a very good outcome for Sable.

Pasted below is the full text of the SEC filing (emphasis added):

Santa Barbara County (the “County”), on August 30, 2024, acknowledged that the County does not have jurisdiction over Pacific Pipeline Company’s (“PPC”) installation of 16 new safety valves in the County along PPC’s Las Flores Pipeline System (the “Pipeline”) in accordance with Assembly Bill 864. The County’s acknowledgement was delivered in the form of a conditional settlement agreement dated August 30, 2024 (the “Safety Valve Settlement Agreement”) among the County, PPC and PPC’s parent company Sable Offshore Corp. (“Sable”), and a subsequent acknowledgement by the County’s planning and development staff.

The Safety Valve Settlement Agreement is predicated upon a prior settlement agreement between PPC’s predecessor in interest, Celeron Pipeline Company, and the County in a federal case styled Celeron Pipeline Company of California v. County of Santa Barbara (Case No. CV 87-02188), which was executed in 1988.

Pursuant to the Safety Valve Settlement Agreement, PPC agreed to the following additional surveillance and response enhancements in the County:

i. PPC will create a Santa Barbara County-based Surveillance and Response Team, trained in PPC’s Tactical Response Plan, which will be responsible for timely initial incident response and equipped with key resources to deploy in early containment, particularly for those regions of the Pipeline between Gaviota and Las Flores Canyon;

ii. PC will provide Santa Barbara first responders with additional training and equipment to assist in PPC’s incident response efforts; and

iii. PPC will undertake the following Pipeline system enhancements: (1) install and operate and maintain primary and secondary Operations Control Centers in Santa Barbara County, and (2) refurbish the Gaviota pump in its existing station.

PPC, Sable and the County have further agreed, in the Safety Valve Settlement Agreement, to file a stipulation to dismiss the pending lawsuit, Pacific Pipeline Company and Sable Offshore Corp. v. Santa Barbara County Planning Commission and Board of Supervisors (Case No. 2:23-cv-09218-DMG-MRW) within 15 days of final installation of all 16 underground safety valves in the County.

Sable affirms that initial restart of production from Sable’s Santa Ynez Unit is expected in fourth quarter 2024.