From a regulatory policy standpoint, this appears to be a strong filing. Operationally, the most important points pertain to the costly and premature Rice’s whale restrictions first discussed on this blog.

Most notably, the plaintiffs seek (p.39):

A preliminary and permanent injunction striking, setting aside, and enjoining BOEM from implementing the specific challenged provisions of the Final Notice of Sale and Record of Decision for Lease Sale 261;

An order vacating the specific challenged provisions of the Final Notice of Sale and Record of Decision for Lease Sale 261;

An order compelling Defendants to proceed with Lease Sale 261 on September 27, 2023, without the challenged provisions;

The expanded Rice’s whale area is based on a single 2022 study that concluded that Rice’s whales were “the most plausible explanation” for moan calls observed in the northwest GoM shelf break area. No Brice’s whales were sighted in the expanded area during this study. Is this sufficient basis for restrictions that threaten operations that are critical to our economy?

Stipulations are part of the lease contract and can be difficult to modify, even when the lessor and lessee are in agreement.

Why not rely on voluntary measures until further studies have been completed? The offshore industry has a good record of cooperation with the government to protect sensitive biological resources. The Flower Garden Banks is a good example of such cooperation.

In addition to the lease stipulation, the entire expanded Brice’s whale area has been excluded from the lease sale. Senator Manchin strongly criticized that decision:

Let me be clear, the exclusion of more than 6 million productive acres from the upcoming offshore oil and gas lease sale in the Gulf of Mexico based on a settlement reached in the name of protecting Rice’s whale while conveniently only targeting oil and gas is yet another example of this Administration’s intentional undermining of the strong energy security provisions in the Inflation Reduction Act.

The attached comments were submitted to BOEM via Regulations.gov. The comments address specific provisions of the proposed rule and include a recommendation to hold companies fully accountable for their lease transfers, but not for subsequent transfers in which they are not a party.

Do I get a t-shirt for being one of the first 2000 entries? 😀

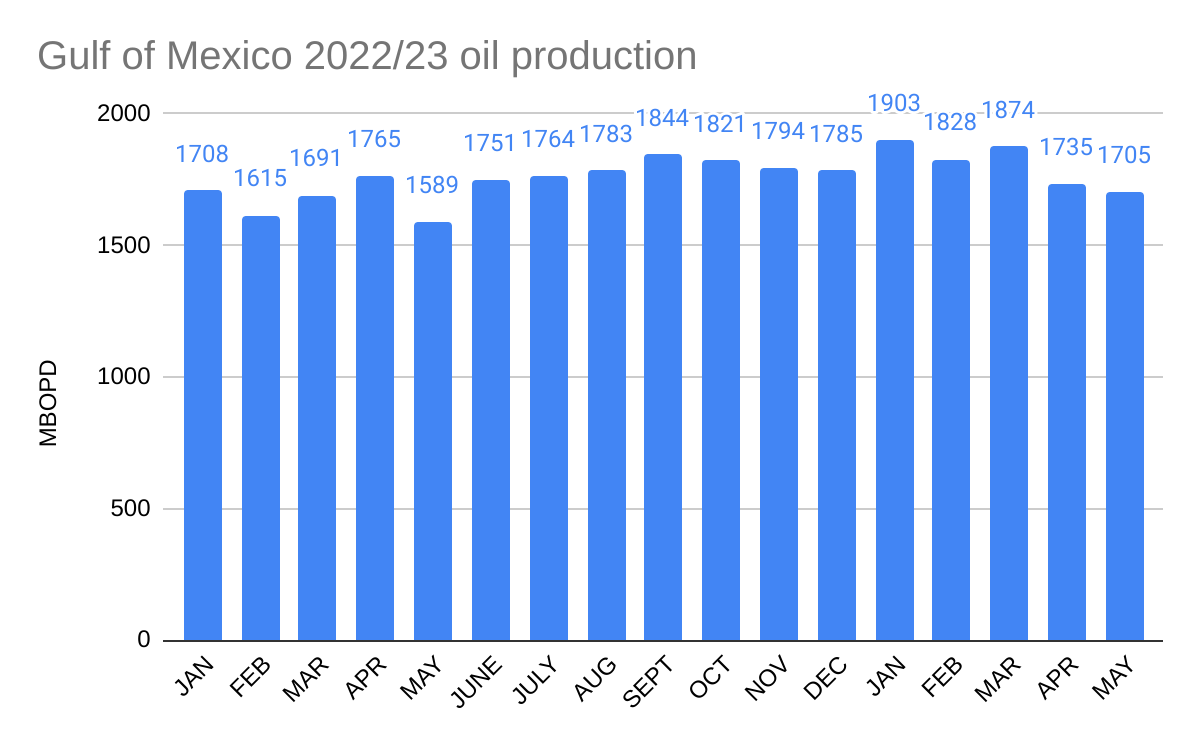

Gulf of Mexico 2023 oil production has dipped over the past 2 months, and is down 10% since January.

2023 production is reasonably well aligned with the EIA forecast which shows new production being offset by declines in existing fields.

Last year, BOEM forecast that production would average 2.0 million bopd in 2023. That forecast was justification for curtailing BOEM’s Proposed 5 Year Leasing Program. For the first time in the history of the OCS program, the primary concern of the program managers was that production might be too high for too long! This stunning quote from the 5 year leasing plan explains why so few lease sales were proposed:

“BOEM’s short-term (20-year) production forecast for existing leases shows steady growth from 2022 through 2024 and declining thereafter (see Section 5.2.1). The long-term nature of OCS oil and gas development, such that production on a lease can continue for decades makes consideration of future climate pathways relevant to the Secretary’s determinations with respect to how the OCS leasing program best meets the Nation’s energy needs.“

Attached is a settlement agreement between NOAA and 4 NGOs that could have major implications for deepwater oil and gas operations in the Gulf of Mexico.

As background, the Rice’s Whale (formerly Bryde’s whale) area has been expanded (see map above) such that it fences off deepwater leases by creating a barrier to vessel transportation. The expansion is based on a single study that concluded that Rice’s whales were “the most plausible explanation” for moan calls observed in the northwest GOM shelf break area. No Brice’s whales were sighted in the expanded area during this study. The authors do point to a 2017 sighting offshore Corpus Christi, which is apparently the only actual sighting of a Brice’s whale along the NW GoM shelf break.

The settlement agreement commits BOEM, presumably with their concurrence, to exclude the expanded area from future leasing, to issue a Notice to Lessees and Operators (exhibit 1 below) and to attach stipulations to new leases (exhibit 2). Because BOEM’s authority to impose major new requirements without proposing a regulation for public review and comment is questionable, the Notice (NTL) describes the restrictions as “recommended measures.” However, the liability risks associated with the failure to comply with this “guidance” would be unacceptable to most companies. Adding to the muddle, the language in the lease stipulation differs by making it perfectly clear that compliance is required.

The most troubling restriction from an operational standpoint:

“To the maximum extent practicable, lessees and operators should avoid transit through the Expanded Rice’s Whale Area after dusk and before dawn, and during other times of low visibility to further reduce the risk of vessel strike of Rice’s whales.“

Comments:

Deepwater facilities are typically far from shore, and a requirement to transit only between dusk and dawn, particularly in the winter, is unrealistic and onerous. This is further complicated by the speed limit provision.

Those who have worked offshore know that periods of low visibility are unpredictable and can extend for days. The low visibility transit restriction is thus highly punitive and increases operational risks on the vessels and at the facilities they serve.

The vague “to the maximum extent practicable” caveat provides little comfort for planners, managers, and crews, and is a de facto acknowledgement that the requirement is unreasonable.

These restrictions, coupled with the required Automatic Identification System data, open the door to endless challenges, especially given the keen interest of the litigious organizations that are parties in the settlement agreement.

Deepwater GoM operations are few in number and highly dispersed, which is a more important mitigating factor than those included in the agreement. More on this tomorrow.

In addition to the deepwater operations that will be much more difficult to supply, there are currently 81 production platforms within the expanded Rice’s whale area (100 to 400 m water depth).These include important facilities like Amberjack, Cognac, Cerveza, and Lobster. What are the implications for these platforms? Will they be required to have full-time whale observers? Can they only be supplied during daylight hours with good visibility? Why not consider using these platforms as bases for more definitive studies?

Further to the previous point, there are 103 existing leases in the 100-400 m depth zone that is now excluded from leasing? 90 of these leases are still in their primary term, and 21 were issued in the past 2 years. How will the contractual rights of these leaseholders be protected? (In fact, the value of all 1550 active leases in >100 m water depth is affected by this agreement.)

Have BSEE and Coast Guard been consulted on the practicality and safety implications of these requirements?

Deepwater operations have been ongoing in the GoM for 50 years, and there is no apparent evidence of impacts to this species. Why can’t the consultation process and any necessary followup studies be completed before decisions are made regarding operating restrictions?

Finally, BOEM’s third footnote in the NTL (pasted below), doesn’t demonstrate great confidence in the need for the onerous requirements that are being imposed.

“This is not meant to be construed as a blanket determination as to whether BOEM, at present, has determined that there is a “reason to believe” that incidental take may occur, within the meaning of the ESA, the consultation regulations, or BOEM’s regulations. Those decisions will be made on a case-by-case basis in accordance with BOEM regulations referenced below.” Comment: Huh??? How are these blanket restrictions case-by-case, and how are they being imposed without public review?

Keathley Canyon (KC) Block 96, the tract receiving the highest bid in the entire sale ($15,911,947 by Chevron), had a BOEM MROV of only $576,000. Clearly, Chevron and the government have a very different view of the value of this tract. BP was the second bidder for KC 96, and their bid ($4,003,103) was also considerably higher than BOEM’s MROV. This one will very interesting to follow.

The only bid that was rejected in Sale 257 was the BP/Talos bid of $1.8 million for Green Canyon Block 777. BOEM’s MROV in the Sale 257 evaluations was $4.4 million. BP again bid on GC 777 in Sale 259, but their bid was only $583,000 (even though BOEM’s Sale 257 evaluation was public information). BOEM’s MROV was reduced only slightly to $4.2 million, and they again rejected BP’s bid. We’ll see what happens in the next sale.

51 of the 230 accepted bids were >$1 million, all for deepwater tracts. All of the rejected bids were for deepwater tracts, and a higher percentage (4/14) were >$1 million. This makes sense given that the higher potential prospects are in deepwater.

These results demonstrate again that resource evaluation is far from an exact science. BOEM is not selling barrels of oil and cubic feet of gas. BOEM is evaluating prospects, and companies are bidding on the opportunity to explore these prospects.

Bidding strategies differ; the more companies participating, the better the long-term prospects for the OCS program.

In a draft rule published on June 29, 2023, BOEM proposes to discontinue using a company’s record of compliance in determining the need for supplemental financial assurance for decommissioning. BOEM’s full explanation for this surprising change is pasted at the end of this post.

Opposing view:

BOEM should be more attentive, not less, to safety performance and compliance data. If they were, taxpayers would have been better protected from the risks associated with the lease acquisitions by Fieldwood, Cox, Black Elk, Signal Hill, and others, and their subsequent bankruptcies.

Safe operations, as reflected in compliance and performance data, are critical to a company’s financial success.

BOEM wrongly infers that Incidents of Noncompliance (INCs) are solely dependent on the number and complexity of facilities. Decades of normalized compliance data have told us that there are marked differences among operators in terms of compliance and safety performance. Companies at the bottom of the performance table don’t usually survive.

Accidents are not mere matters of chance; management and culture matter.

Honor Roll companies, large and small, have superior compliance records, and in 2022 these companies had 50-90% fewer INCs/facility-inspection than the Gulf of Mexico average.

Does BOEM expect noncompliance leaders to be concerned about decommissioning obligations? The record shows that they are not.

Cox’s 2023 bankruptcy was predictable given their past safety performance. In 2022, Cox was a violations leader by any measure, and was responsible for 9 of the 30 safety incidents that were significant enough to require investigation by BSEE.

Fieldwood’s terrible 2021 safety performance has been discussed, and there was ample evidence of performance problems prior to their bankruptcy declaration in 2018. In 2016 and 2017 Fieldwood was, by far, the GoM violations leader with 818 INCs, 401 of which required a facility or component shut-in.

Ironically (or maybe not), the only other company that was even in the same noncompliance ballpark as Fieldwood in 2016 and 2017 was future Cox affiliate Energy XXI GOM. Energy XXI earned 465 INCs (240 shut-ins) during that 2 year period. Did BOEM object to or otherwise comment on the 2018 Cox-Energy XXI merger?

Black Elk Energy was new in 2007 and quickly became a violations leader. Between 2010 and 2012, BSEE cited Black Elk 415 times. 218 of these violations were serious enough to require facility or component shut-ins. On November 16, 2012, explosions at Black Elk’s West Delta 32 platform killed 3 workers, and 2 others suffered severe burns. Criminal charges and a complex bankruptcy followed. BSEE records show 1107 INCs during the company’s short history, 464 of which required facility or component shut-ins.

The rapid growth of Fieldwood, Cox, and Black Elk was in part facilitated by lax lease assignment and financial assurance policies. Operating companies should have to demonstrate that they can operate safety and comply with the regulations before they are approved to acquire more properties.

The Signal Hill sagawas documented nearly 2 years ago, and none of the questions raised in that post have been answered. Violations data and inspector feedback predicted the Signal Hill/POOI failure. Nonetheless, and despite the objections of regional staff, Signal Hill was allowed to tap into its decommissioning account to cover operating expenses. Responsibility for decommissioning Platforms Hogan and Houchin is still uncertain.

Given that BSEE, not BOEM, is responsible for safety and compliance, I sincerely hope that regulatory fragmentationwas not a factor contributing to BOEM’s decision to discontinue the use of compliance data in determining financial assurance needs.

BOEM’s explanation for the proposal to eliminate the record of compliance criterion:

BOEM also proposes to eliminate the existing “record of compliance” criterion found in the current version of § 556.901(d)(1)(v). BOEM has determined that the number of INCs a company receives correlates with the number of OCS properties it owns, not its financial stability, and therefore, BOEM has concluded that it is not an accurate predictor of its financial health. BOEM reviewed BSEE’s Incidents of Non-Compliance (INCs) records and its Increased Oversight List, which represent BSEE’s cumulative records of violations of performance standards on the part of OCS operators and lessees and determined that the number of incidents of non-compliance typically increases with the size and complexity of the operator’s or lessee’s operations, including the ratio of incidents to number of components. Because larger companies (regardless of credit score) tend to have more properties and components and therefore more INCs, BOEM determined that record of compliance criterion does not accurately predict financial default. BOEM’s review of this information confirmed the feedback BOEM received in response to the 2016 NTL, namely that companies with a large number of properties and facilities tended to receive a large number of INCs and had more individual properties on the Increased Oversight List. BOEM specifically requests comments regarding the use of fines and violations as a criterion in the determination of a company’s ability to fulfill decommissioning obligations, and any data or analysis addressing any correlation between the number of violations and the risk of financial default. BOEM also requests comments on whether the elimination of the INC’s criteria would create a disincentive to comply with regulations. BOEM also requests comment on whether or not the cost of decommissioning is likely to increase based on the type, quantity, and magnitude of previous violations.

On a related note, BOEM/BSEE should consider a followup to the John Shultz thesis which found that INCs are a very good predictor of accidents and spills.