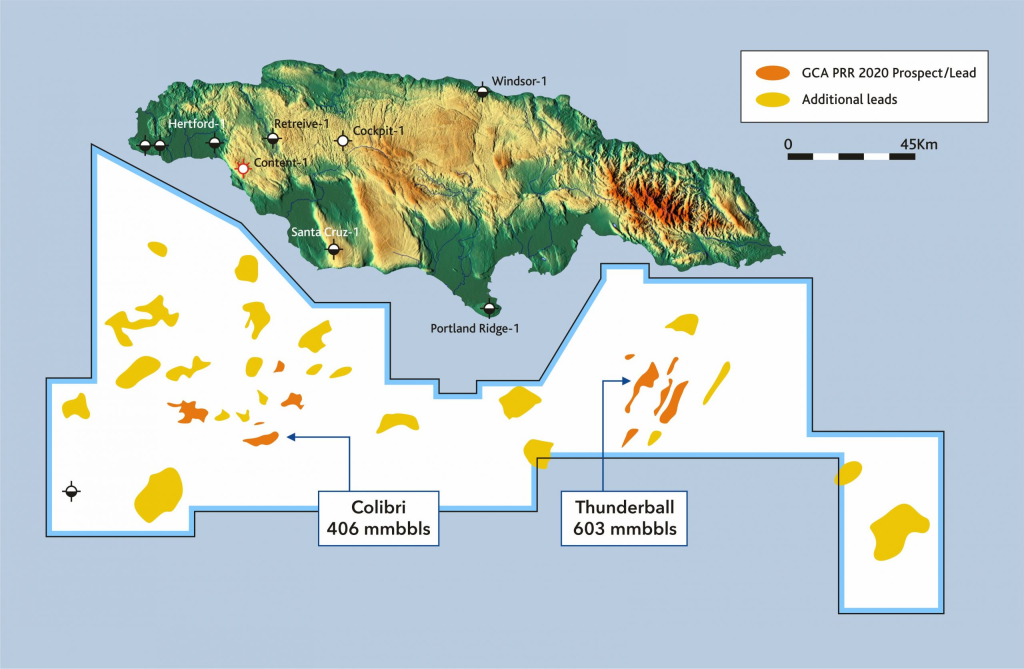

United Oil and Gas excels at promotion and isn’t shy about making bold statements. Can they find a strong partner and move their Jamaican exploration program forward?

The term “string of pearls” was used about 30 years ago to describe discoveries in the Beaufort Sea and on adjacent Alaska lands. Although they were modest individually (by Arctic standards), the sense was that these discoveries would collectively support sustained production in the region. While there has been some success in that regard, the optimistic expectations have not been realized.

Below is a recent United Oil & Gas presentation to prospective investors. Previous Jamaica posts.

… for their coverage of the Vineyard Wind turbine blade incident and their investigative reporting. From a recent Current article (emphasis added):

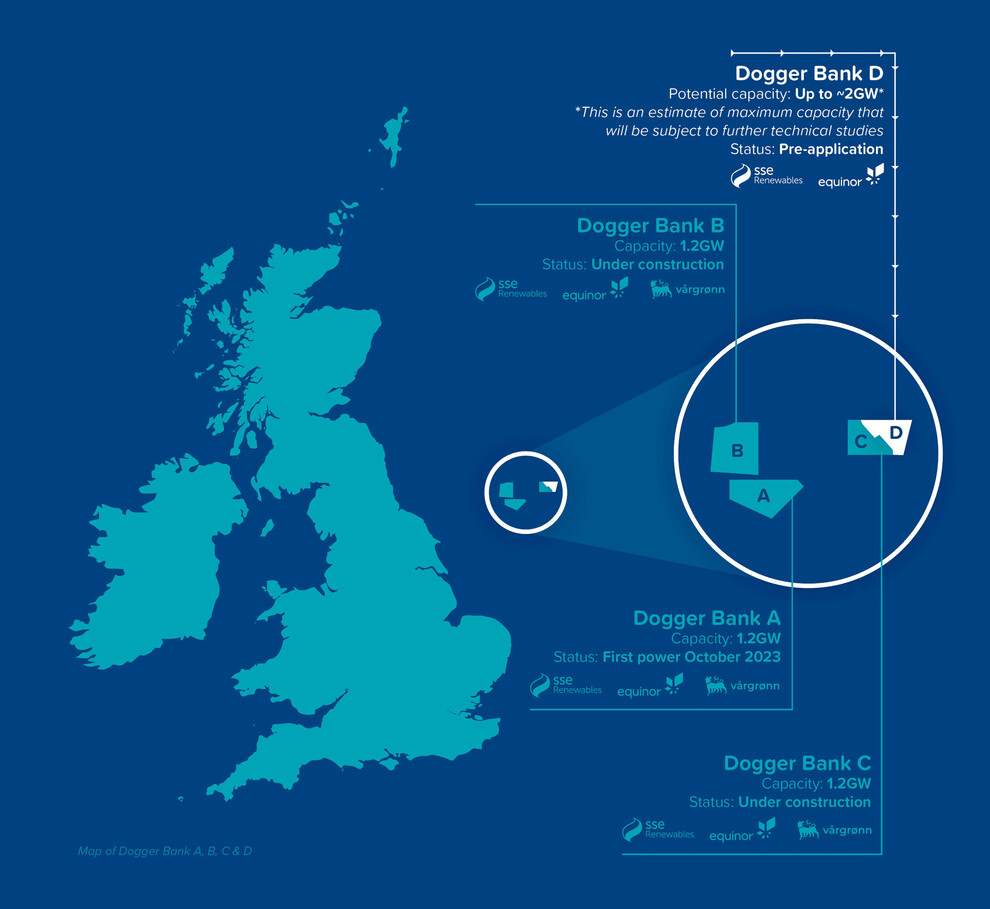

“The technology may not be new, but the size and scale of the Haliade-X turbine is novel for the offshore wind industry. And these jumbo-sized turbines have only recently been installed in just two locations in the world within the last year – at Vineyard Wind off Nantucket, and the Dogger Bank Wind Farm off the northeast coast of England. The Haliade-X turbine blades – which are supposed to have at least a 25-year lifespan – have suffered failures in both locations.“

“At the Dogger Bank Wind Farm – which is being completed in three sections which combined will make up the largest offshore wind farm in the world – the first GE Vernova Haliade-X turbine was installed in the fall of 2023 and began producing power on Oct. 10. But little is known about the blade failure that occurred just months later during the first week of May 2024. The damaged blade was disclosed by Dogger Bank’s owners – SSE Renewables, Equinor, and Vårgrønn – a week after the incident. In a statement, the companies said only that “damage was sustained to a single blade on an installed turbine at Dogger Bank A offshore wind farm.”

“One reason the turbine blade incident at the Dogger Bank may not have generated more attention at the time is that the wind farm is located 100 miles off the coast of England, rather than just the 15 miles in the case of Vineyard Wind and Nantucket. If any debris was generated, it would have a far wider area to disperse in before nearing land – if it made it that far at all.“

Interestingly per the Current:

The Haliade-X turbine is the same one Orsted – a partner in Vineyard Wind – is planning to use for offshore wind farms slated for the waters off New Jersey and Maryland.

Land-based turbines have come apart in Sweden, Germany, Lithuania, Cypress, Brazil, and the US (and presumably elsewhere).

Greater transparency regarding turbine incidents, both in the US and internationally, is clearly needed. As we have learned from decades of experience with the oil and gas industry, most companies prefer reporting systems (if any) that protect details and information about the responsible parties from public disclosure. It’s the responsibility of the regulators to make sure that incident data and investigation reports are timely, complete, and publicly available. This is made more difficult by the promotional role that government agencies have assumed for offshore wind.

“The order comes as the bureau continues its oversight and investigation into the July 13, 2024, turbine generator blade failure. The order continues to prohibit Vineyard Wind 1 from generating electricity from any of the facilities or building any additional wind turbine generator towers, nacelles, or blades. This order also requires Vineyard Wind 1 to submit to BSEE an analysis of the risk to personnel and mitigation measures developed prior to personnel boarding any facility. Vineyard Wind 1 is not restricted from performing other activities besides those specifically directed for suspension or additional analysis. For example, Vineyard Wind 1 is still permitted to install inter-array cables and conduct surveys outside of the damaged turbine’s safety exclusion zone.”

BSEE also advises that they are conducting their own investigation, and promises to release the findings to the public.

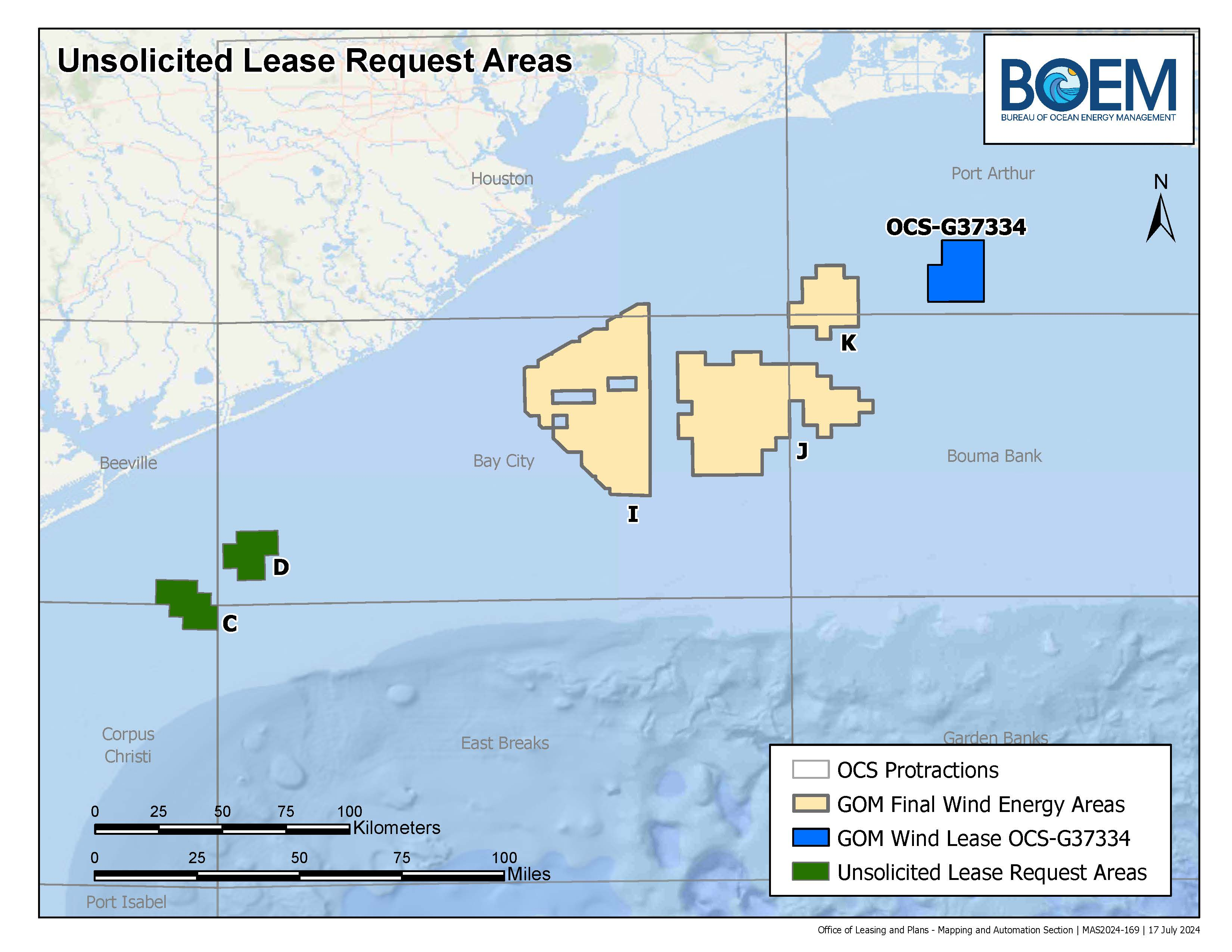

Hercate lease request – C & D. Wind areas that were considered for 2nd GoM sale – I, J, & K. Active RWE lease – blue.

GoM wind leasing update:

BOEM’s highly promoted 2023 GoM wind sale was a bust. The sole bidder, the German company RWE, acquired a single lease.

BOEM’s second GoM wind sale failed to get off the ground. Because only one company expressed interest in participating, that sale has been cancelled.

BOEM is now surveying interest in other GoM areas as a result of an unsolicited lease request from Hercate Energy.

If BOEM does not receive competing indications of interest, they may (and probably will) issue a noncompetitive lease to Hecate.

BOEM calls Hercate an “industry leader.” However, per their website, Hecate is mainly a solar energy company with only 2 wind projects. Both of those wind projects are onshore (Kentucky), and are “in development” (i.e. not yet operating). Hercate is no doubt a fine company, but have they demonstrated the technical expertise and financial strength needed for offshore wind development?

BOEM’s aggressive wind leasing policy stands in stark contrast to their current oil and gas policy. Not a single oil and gas sale will be held in 2024. Were it not for a provision in the “Inflation Reduction Act,” the last 3 GoM sales (257, 259, and 261) would probably not have occurred.

The new 5 year oil and gas leasing plan confirms that the Dept. of the Interior (DOI) has no intention of fulfilling their statutory oil and gas leasing mandate. In announcing the new 5 year plan, DOI boasted that the plan includes the fewest sales (3) of any plan in the history of the program. DOI strongly implied that the only reason those 3 sales were included was to sustain the wind program.,

When we drafted the OCSLA amendments that authorize offshore wind leasing, we envisioned complementary and synergistic programs, not a dogmatic pro-wind bias. As experts like Daniel Yergin have repeatedly warned, the notion that wind energy can eliminate the need for oil and gas is pure folly.

July 24 (Reuters) – The amount of electricity produced by wind farms in the U.S. fell to a 33-month low on Monday, forcing power generators to crank up natural-gas fired plants to keep air conditioners humming during a hot summer day.

Over the past few years, much of the money energy firms have invested in new generation has gone into renewable power sources like wind and solar. But when the wind stops blowing and the sun does not shine, gas is still needed to keep the lights on.

Funny how that works! Being trendy and highly promoted doesn’t make you reliable!

GE Vernova’s SEC filing for the second quarter of 2024 is attached. The Vineyard Wind turbine blade incident, the main reason for the sharp decline in their stock value in mid-July, is described as follows:

VINEYARD WIND OFFSHORE WIND FARM. We are the manufacturer and supplier of turbines and blades and the installation contractor for Vineyard Wind 1 offshore wind farm in the Atlantic Ocean (Vineyard Wind), at which we have installed 24 of 62 Haliade-X 220m wind turbines to date. Subsequent to the period covered by this report, a wind turbine blade event occurred at Vineyard Wind. Debris from the blade was released into the Atlantic Ocean and some has washed ashore on nearby beaches. On July 15, 2024, the U.S. Bureau of Safety and Environmental Enforcement (BSEE) issued a suspension order to cease power production and the installation of new wind turbines at the project site, pending an investigation of the event. As of the date of the filing of this report, we are currently engaged in a root cause analysis of the incident. We do not have an indication as to when BSEE will modify or lift its suspension order. Under our contractual arrangement with the developer of Vineyard Wind, we may receive claims for damages, including liquidated damages for delayed completion, and other incremental or remedial costs. These amounts could be significant and adversely affect our cash collection timelines and contract profitability. We are currently unable to reasonably estimate what impact the event, any potential claims, or the related BSEE order would have on our financial position, results of operations and cash flows

“Within only two to three years of commercial operation, the GE wind turbine generators have exhibited numerous material defects on major components and experienced several complete failures, at least one turbine blade liberation event, and other deficiencies,” alleged AEP.

“While we continue to work to finalize our root cause analysis, our investigation to date indicates that the affected blade experienced a manufacturing deviation,” said GE Vernova CEO Scott Strazik. “We have not identified information indicating an engineering design flaw in the blade or information of a connection with the blade event we experienced at an offshore wind project in the UK, which was caused by an installation error out at sea. We are working with urgency to scrutinize our operations across offshore wind. Pace matters here. But we are going to be thorough, instead of rushed.”

“It’s been 11 days since the event, and just to reinforce from the start, we have no indications of an engineering design flaw,” Strazik said. “We have identified a material deviation or a manufacturing deviation in one of our factories that, through the inspection or quality assurance process, we should have identified. Because of that, we’re going to use our existing data and reinspect all of the blades we’ve made for offshore wind. For context, this factory in Gaspé, Canada where the material deviation existed we’ve made about 150 blades.

Any comments from the CVA, assuming there was one?

Meanwhile, Nantucket will renegotiate their “Good Neighbor Agreement” with Vineyard Wind. Is this a lesson for other municipalities?

🚨 Nantucket Select Board chair Brooke Mohr just announced that the town intends to renegotiate the terms of the Good Neighbor Agreement with Vineyard Wind.

“The emergency has also revealed the inadequacy of Vineyard Wind’s coordination & communication required by the GNA” pic.twitter.com/bkaVJs6r5k

GE Vernova retained Arcadis US, Inc., to perform an initial assessment of environmental considerations associated with the presence of the blade debris in the water and along the shoreline. That report is attached. Linked is a Nantucket Current article on the assessment.

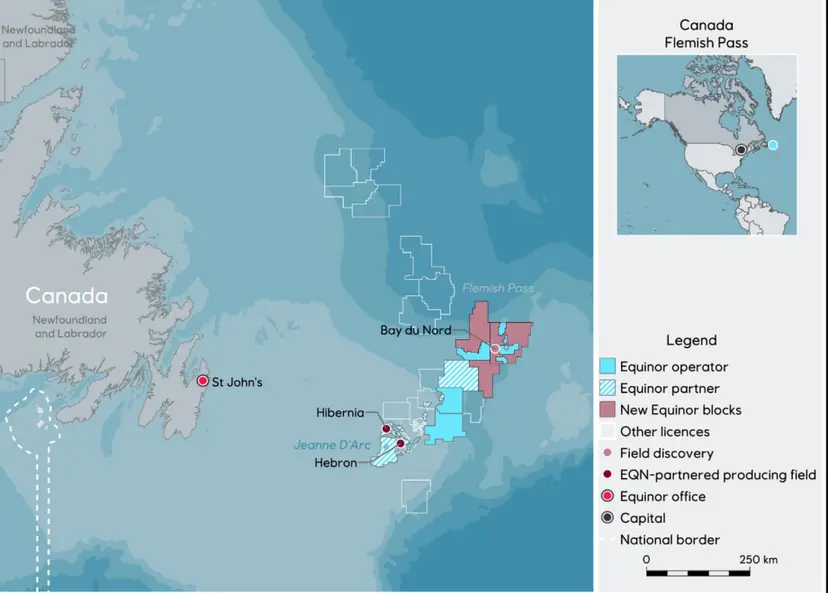

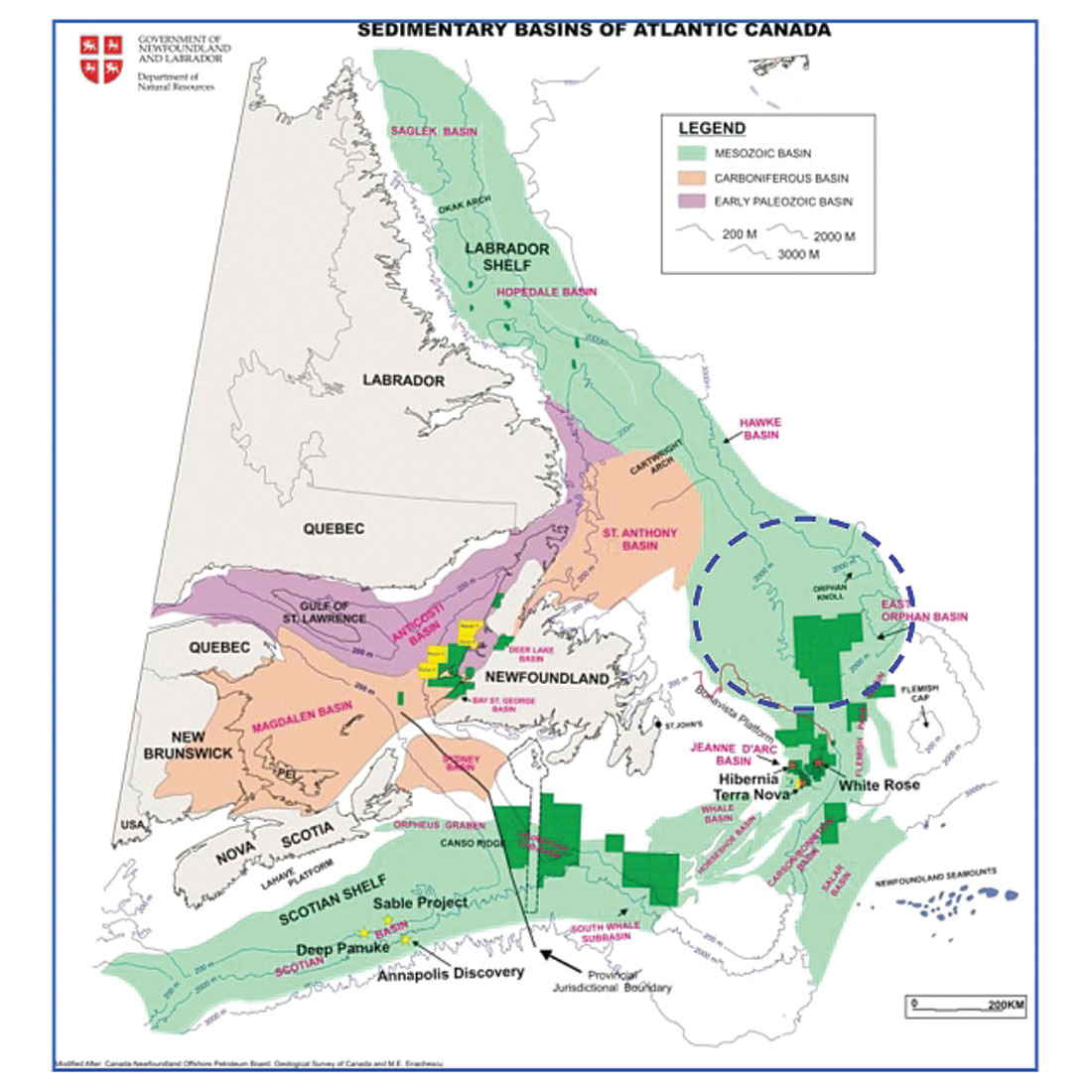

Per the CNLOPB weekly activities report, Equinor spudded the important Sitka C-02 well in the Flemish Pass area on July 10, 2024. This well will help clarify the resource potential in the Bay du Nord project area with the goal of better defining development plans.

Meanwhile, operations on Exxon’s important Persephone well in the Orphan Basin have now been ongoing for 2 months. Some type of announcement by Exxon is expected after operations are completed and the well has been plugged.

expressed “strong concerns and outrage” over the fractured Vineyard Wind turbine blade and the debris that washed ashore on Nantucket.

said the foam and fiberglass debris have “potential negative and adverse impact[s]” on the environment, marine life, and human health.

said fragments in the water pose a threat to shellfish, which are a crucial part of both the marine food web and also ingested by humans.

commented that the potential contamination of shellfish with fiberglass and other materials could have severe consequences for human consumption and public health.

criticized the lack of communication from federal officials to the tribe.

called for an “immediate stoppage” of offshore wind construction in U.S. waters until they can be evaluated for microfractures and other damages.