The preliminary NTSB report was posted on 1/18/2023, but the final report has still not been published. Status update:

Will the investigators consider longstanding regulatory fragmentation issues? The most recent Coast Guard – BSEE MOA for fixed platforms added to helideck regulatory uncertainty by assigning decks and fuel handling to BSEE and railings and perimeter netting to the Coast Guard. This is the antithesis of holistic, systems-based regulation.

Last week, BOEM announced the acceptance of all 69 of Exxon’s Sale 259 carbon sequestration bids. This is despite these facts: (1) Exxon’s intentions were known, (2) there were no provisions for CCS bidding in the Notice of Sale, (3) no environmental review of CCS leasing was conducted, and (4) there are no procedures for evaluating CCS bids.

Absent some type of legislative maneuver, carbon sequestration is not authorized under these leases. If Exxon is just acquiring the leases for evaluation purposes in preparation for a possible CCS sale in the future, their lease acquisitions may be okay. If they are planning on retaining these leases for actual sequestration operations, that is not okay, at least not until a competitive process has been established for awarding or reclassifying such leases.

It’s also noteworthy that there was a second bidder for th blocks (in red above). Presumably that company, Focus Exploration, was interested in acquiring the tract for oil and gas exploration purposes. However, the Focus bid was a bit lower, so Exxon got the tract.

Along with Cox Operating, six affiliates also filed: MLCJR , M21K, EPL Oil & Gas, Cox Oil Offshore, Energy XXI Gulf Coast, and Energy XXI GOM.

The BOEM platform data base lists only Cox Operating (276 platforms), EPL (10 platforms), and Energy XXI GOM (26 platforms) as current operators of OCS platforms. However, according to the Cox Operating website, the company operates 600 producing wells on 500 structures. Presumably, ~200 of those structures are in State waters.

In 2020, the OPEC price war drove oil prices down, while stay-at-home orders and well shut-ins associated with the COVID-19 global pandemic sharply reduced production.

The debtors’ assets suffered significant damage from five named storms and hurricanes during 2020 and 2021, leading to further reductions in production. Comment: According to BSEE, 7 tropical systems affected GoM operations in 2021, so the number of storms is not in dispute. The extent to which maintenance or preparedness issues contributed to the damage is unknown.

In 2020, a foreign-flagged vessel struck a platform owned by one of the debtors resulting in major damage and substantial losses of production. Comment: Apparently, this is the incident being cited. According to the BSEE report, the operator (Cox) was not at fault. Per BSEE: (1) The navigational lights and foghorn on the platform were maintained and in operational order, (2) the allision was not due to any platform related error, and (3) the platform’s operator and safety system responded in accordance with the regulations.

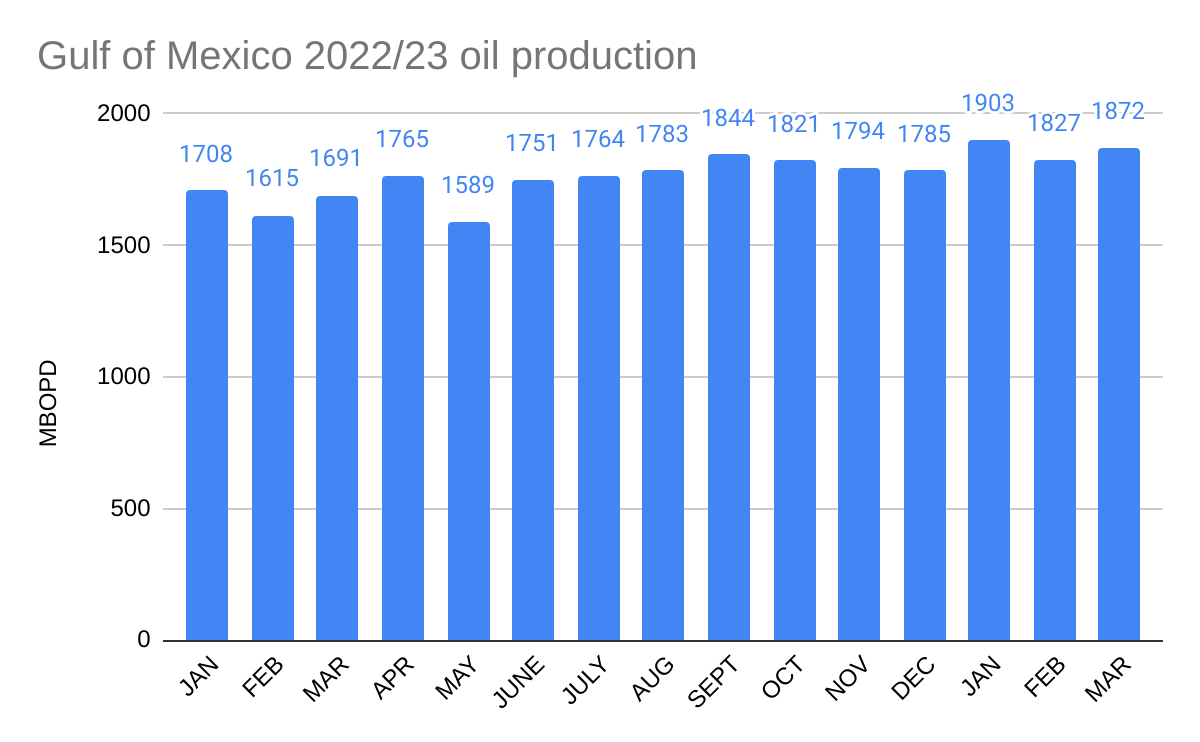

At this time, the debtors’ production volume is half what it was in 2019. Comment: Comparing the 2019 and 2022 production data, OCS oil and gas production are down by about 30% and 40% respectively. However, the 50% reduction figure seems reasonable given the likelihood of further reductions in State water production and in 2023.

A Metairie-based oil company that’s one of the largest independent operators still working in the state’s shallow coastal waters has filed for bankruptcy protection, leaving dozens of south Louisiana service and supply companies facing potential bankruptcies of their own.

Bankruptcy court documents show Cox’s estimated liabilities are close to $500 million – more than $200 million of which is owed to small businesses in the Houma-Thibodeaux and Acadiana areas.

Court documents indicate that Cox followed a path that led to financial trouble for other companies in recent years: using debt to acquire large fields of aging wells in shallow Gulf waters.

This blog is primarily concerned with the potential impacts of the bankruptcy on safety performance, the plugging of wells, and the decommissioning of old facilities. Per BOEM’s data base, Cox currently operates 276 Gulf of Mexico platforms, all in shallow shelf waters. The company is reported (Nola.com) to owe $8 million in bond premiums needed to support well plugging operations.

Cox has not been an active driller of late with only 2 well starts since 1/1/2022 (BSEE borehole file).

Cox has been a major generator of INCs (incidents of noncompliance) with 437 INCs YTD. Cox has been responsible for 47% of all GoM INCs in 2023. Cox’s INC to inspection ratio was 2.46 vs. a combined ratio of 0.50 (490/972) for all other GoM operators.

Cox is currently ranked 11th and 18th respectively in GoM gas and oil production with 7.2 billion cu ft and 1.8 million barrels produced YTD.

Per BOEM’s latest update, 137 of the 313 Sale 259 tracts receiving bids have now been accepted. No decision has been made on the other 176 high bids, including the 69 bids for carbon sequestration purposes. For the reasons previously expressed, I continue to believe those sequestration bids were invalid.

I believe the OOC is the world’s oldest trade association for the offshore oil and gas industry. The OOC was formed in 1948, five years before the enactment of the OCS Lands Act and just one year after the first Gulf of Mexico well was completed out of sight of land.

For much of their history, OOC had just a single, part-time employee. The organization has matured, but still operates in the same efficient manner, relying on subject matter experts from their member companies. Since the days of the OCS Orders, the OOC has consistently provided informed comments on operating regulations. As a regulator, I had issues with some of their comments over the years, but the dialogue was (almost😉) always polite and professional.

Congratulations to the OOC for the support they have provided for US offshore energy! Although many have had important roles, these former OOC representatives come immediately to mind for their contributions to offshore safety: John Rullman, Steve Brooks, Mark Witten, Sandi Fury, Dave Wisch, Ken Arnold, Charlie Williams, Phil Smith, Peter Velez, Allen Verret, Wanda Parker, Cort Cooper, Charlie Duhon, Jodie Connor, Craig Castille, Susan Hathcock, and Pat O’Connor. Many of these retired safety leaders, and current OOC Executive Director Evan Zimmerman, were recipients of MMS Offshore Leadership Awards.

This CBC story, which includes excellent video interviews, was brought to my attention by Newfoundlander Howard Pike, an engineer and offshore safety leader.

We know a lot about Rigs-to-Reefs, and the importance of active and reefed platforms in providing the habitat, shelter, and food that is necessary to increase biodiversity and productivity. However, the carbon reduction potential of artificial reefs has received little attention.

The linked CBC story is particularly interesting in that it includes interviews with artificial reef researchers who are assessing the carbon capture aspects. To date the results are encouraging:

As for the impact on climate change, the researchers say they have found some evidence that an artificial reef could hold more carbon compared to a natural reef.

Interestingly, none of Exxon’s 69 high bids for shelf leases have been accepted to date. Given that the Exxon bids were for tracts that are presumably considered “nonviable” from an oil and gas production standpoint, those bids should have been accepted by now were they deemed to be valid.

Perhaps BOEM, to their credit, is planning to reject the CCS bids as they may when an unusual bidding pattern has been identified. It is now quire clear (unlike in the immediate aftermath of Sale 257) that Exxon was seeking to acquire these leases for carbon sequestration purposes. That is not allowed given that both Sales 257 and 259 were oil and gas lease sales. As similarly noted for Sale 257:

Sale 259 was an oil and gas lease sale. The Notice of Sale said nothing about carbon sequestration and did not offer the opportunity to acquire leases for that purpose. Therefore, the public notice requirements for CCS leasing (30 CFR § 556.308) were not fulfilled.

Because there was no draft or final Notice of Sale for CCS leases, interested parties and the public did not have the opportunity to consider and comment on CCS leasing, tract exclusions, bidding parameters, and other factors.

30 CFR § 556.308 requires publication of a lease form. No CCS lease form was posted or published for comment.

CCS operations were not considered in the environmental assessments conducted prior to the sale.

No evaluation criteria for CCS bids have been published.

The NOIA/ICF report is favorable from a Gulf of Mexico perspective, but 2 general caveats should be highlighted:

“The estimation of the production related GHG for various crude oils and condensates is a complex process that is hindered by lack of public, up-to-date, and high-quality data.“

“There is considerable controversy regarding certain critical data including quantity of gas flared, operational flare efficiencies, and the volumes of methane releases along oil and gas supply chains.”

Comments:

More work is needed to better determine cold venting volumes:

Table 7, p. 13, of the NOIA/ICF report indicates venting (methane) emissions of 71,200 metric tons/year for GoM operations. That number is aligned with the 2017 GOADS data (70,488 tons per Table 6-11, p. 112).

The recent PNAS report found that much more gas is being vented: 410,000 – 810,000 tons annually. If the PNAS findings are accurate, venting is being significantly underestimated and/or under-reported.

Per ICF, lower flaring and venting volumes are the main reason for the GoM’s lower GHG emission intensity, so data accuracy is important. The difference between the government data and the PNAS findings (see table below) should be carefully assessed.

The NOIA/ICF report did not distinguish between GoM deepwater and shelf emissions.

The PNAS report indicates much higher methane emissions intensity on the shelf, as do most subjective assessments.

Future studies should provide separate GHG intensity data for shelf and deepwater facilities.

All production cannot be from the lowest emission intensity sources. The objective should be to minimize emissions from each source, not to eliminate production.GoM shelf operations have other advantages, most notably the production of nonassociated natural gas.