4/17/2023 NTSB data base search results:

Posted in accidents, Gulf of Mexico, Offshore Energy - General, tagged bp, Gulf of Mexico, listing, Thunder Horse on April 14, 2023| Leave a Comment »

This picture was posted by MaritmePhoto. The”Blue Marlin” heavy lift vessel is arriving in Texas (2005) with the massive semisubmersible production platform “Thunder Horse” on board.

Above (from BOE archives): Pre-commissioning inspection of Thunder Horse

Thunder Horse has a most interesting history. The project was initially named Crazy Horse, but the name was changed out of respect for concerns raised by the Lakota nation. The massive structure is 136 m in length and 113 m in width, and is located in 6300′ of water in the Mississippi Canyon area of the Gulf of Mexico.

Many of you no doubt remember the near disaster during Hurricane Dennis (2005) when the platform was being commissioned. In light of the extensive pre-production hype for the “world’s largest production platform,” this was a costly and embarrassing incident for BP and the OCS program.

Per the findings of the MMS investigation team led by my former colleague David Dykes:

Findings indicate that failures associated with the hydraulic control system and its isolation on evacuation led to the partial opening of multiple hydraulically actuated valves in the ballast and bilge systems of the vessel. This allowed ballast water migration to take place, causing the initial listing (to approximately 16 degrees) of the vessel shortly after the hydraulic system was isolated.

The findings also indicate that ballast water migrated into manned spaces in the lower hull, via faulty and improperly installed check valves in the integrated ballast/bilge piping system. As the degree of list increased beyond the 16 degree mark, downflooding of seawater occurred, initially through overboard discharge lines and/or vents, and possibly later through the deck box as it entered the water. Since the PDQ was already listing at a 16 degree angle prior to the passage of Hurricane Dennis, wave action associated with the passage of the hurricane may also have contributed to the downflooding of seawater.

Although not an initiating event, failed Multiple Cable Transits (MCTs) and two unintended openings in the bulkheads allowed water transfer between watertight compartments, which led to extensive flooding and water damage in the lower hull.

Fortunately, there were no injuries. Repairs were made and production was finally initiated in June 2008.

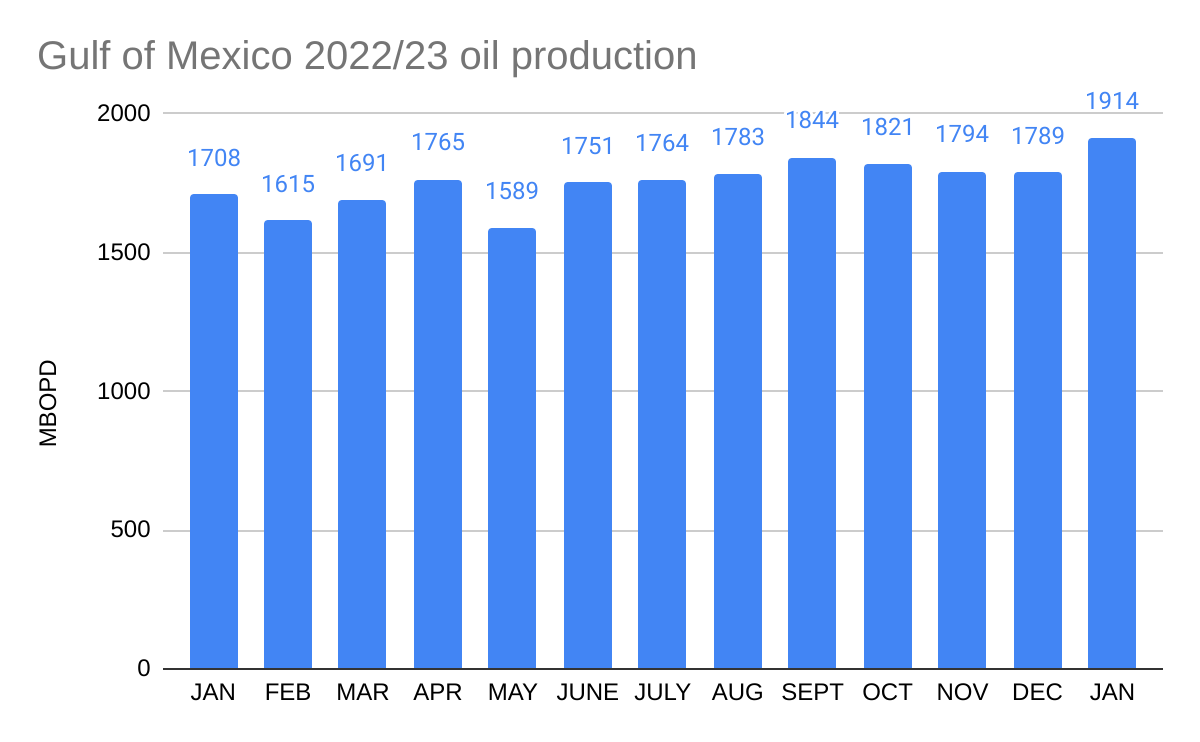

After recent subsea tieback expansions, Thunder Horse is reported to be producing 200,000+ boe/d. OPEC’s Monthly Market Report for April 2023 cites the Thunder Horse expansion as a key driver in the January 2023 GoM production increase (see excerpt below).

Posted in climate, Gulf of Mexico, Offshore Energy - General, tagged air emissions, BOEM, carbon intensity, excess methane, flaring, GOADS, Gulf of Mexico, ONRR, PNAS article, venting on April 11, 2023| Leave a Comment »

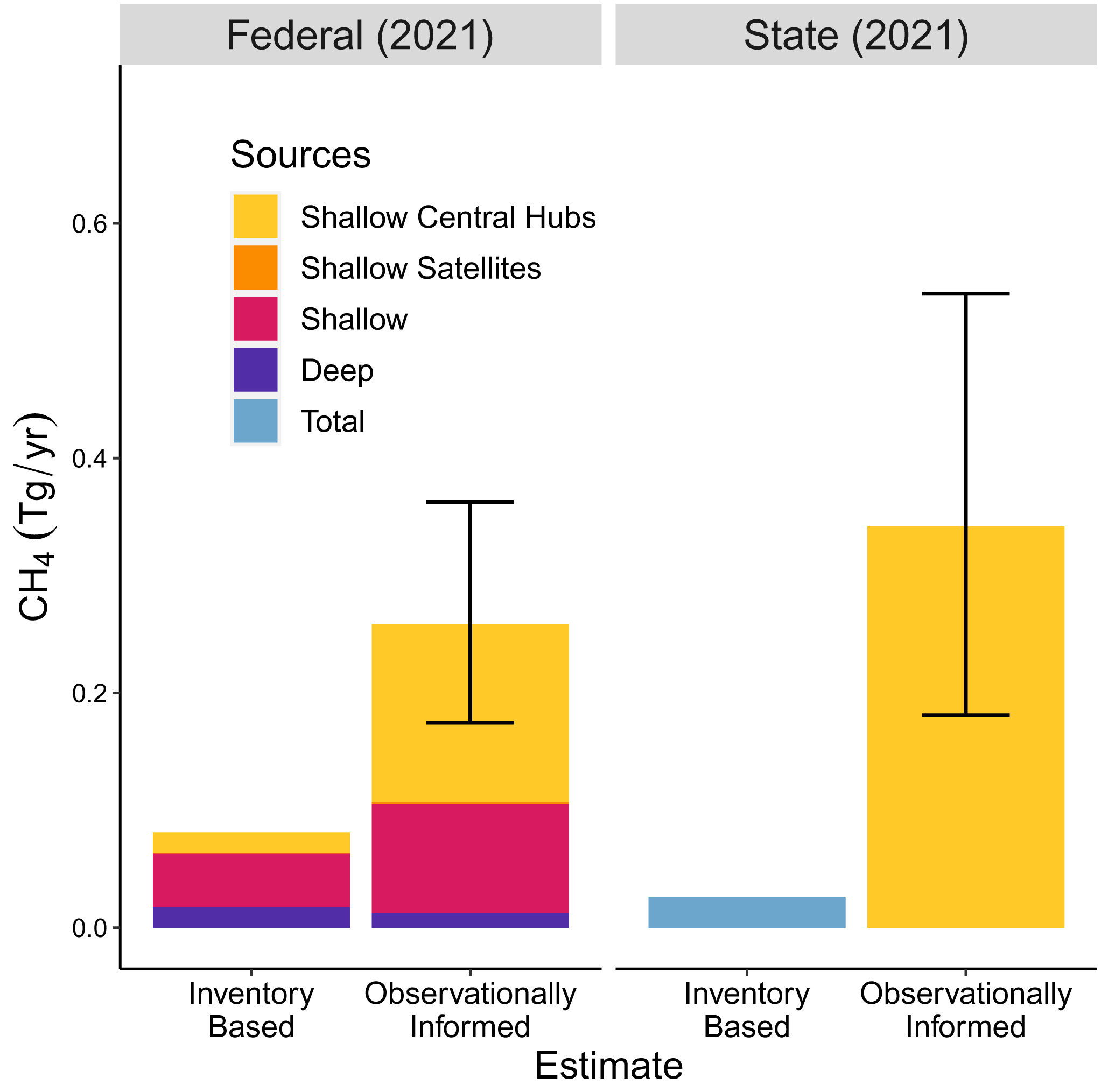

An interesting study published in the Proceedings of the National Academy of Sciences (PNAS) was brought to my attention by leading offshore energy historian Tyler Priest. The study used airborne observations and emissions reports to measure the carbon intensity (CI) of Gulf of Mexico oil and gas production. Their CI measure is grams of CO2 equivalent of greenhouse gas emissions per megajoule of energy produced.

The authors conclude that inventory emissions of CO2 (as reported to BOEM) “are generally consistent with observations from our aircraft survey, suggesting that combustion is well represented in the federal inventory.“

However, that is not the case for methane (CH4) emissions which are underestimated by the Federal inventories. As summarized in the chart below, deepwater facility methane emissions are consistent with the reported inventories, but shelf emissions in State and Federal waters differ significantly.

Comments:

Posted in drilling, Gulf of Mexico, Offshore Energy - General, tagged Arena Offshore, BOEM, bp, Cantium, deepwater drilling, Gulf of Mexico drilling, shelf drilling on April 6, 2023| Leave a Comment »

| DW expl | DW dev | shelf expl | shelf dev | |

| Anadarko | 5 | 1 | ||

| Arena | 22 | |||

| BOE | 1 | 4 | ||

| BP | 2 | 3 | ||

| Byron | 2 | |||

| Cantium | 20 | |||

| Chevron | 3 | |||

| Contango | 2 | |||

| Cox | 2 | |||

| Eni | 2 | 5 | ||

| EnVen | 5 | |||

| Greyhound | 2 | |||

| Hess | 2 | |||

| Kosmos | 1 | |||

| LLOG | 3 | 1 | ||

| Murphy | 4 | |||

| QuarterNorth | 2 | |||

| Shell | 25 | 9 | ||

| Talos | 2 | 8 | ||

| Walter | 1 | |||

| Woodside | 3 | 1 |

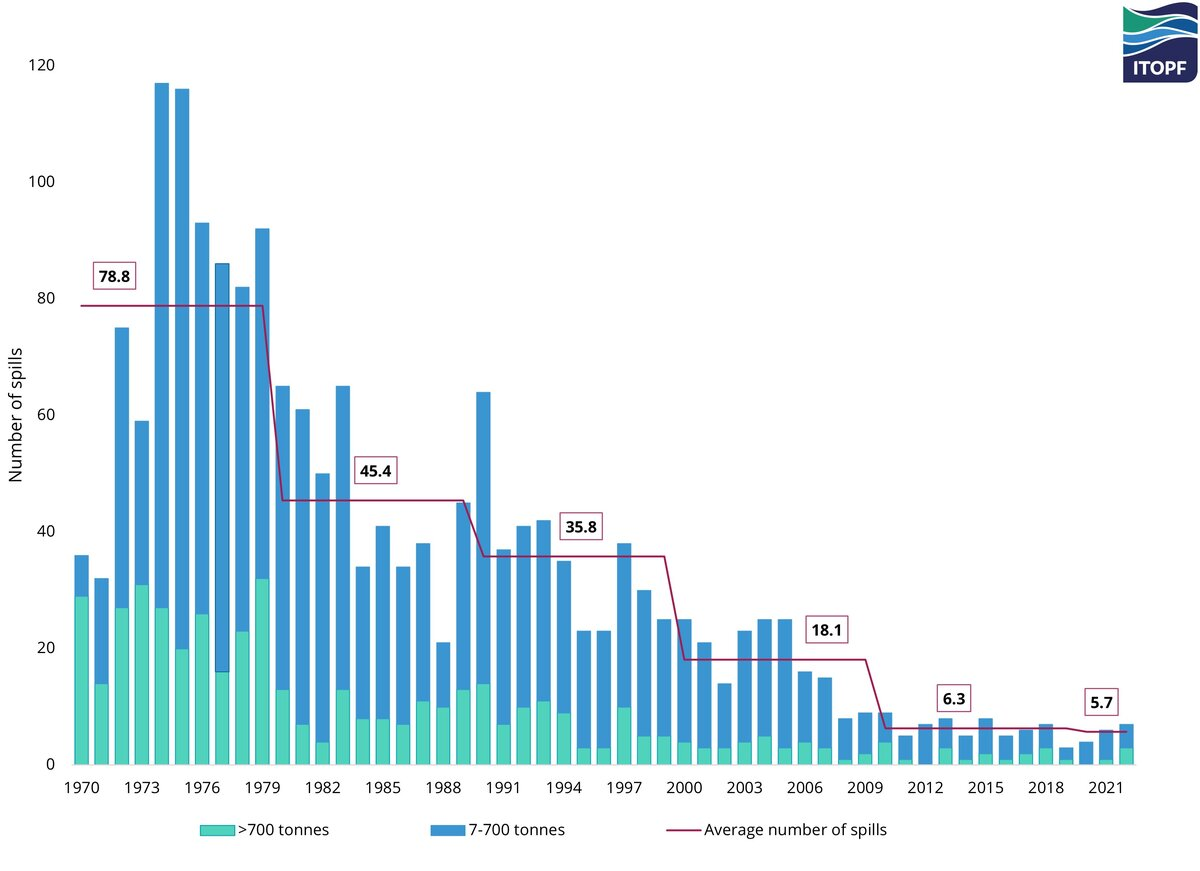

Posted in accidents, Gulf of Mexico, oil spill response, tagged Bob LaBelle, Cheryl Anderson, ITOPF, Melinda Mayes, offshore, oil spills on April 5, 2023| Leave a Comment »

Cheryl Anderson took oil spill data analysis to a level worthy of a world class offshore program. In my opinion, Cheryl was the top analyst in the history of the OCS program, a true Hall of Famer. Regardless of the politics of the day, she always stuck to the facts and resisted “spin,” and that was a trait her colleagues greatly admired.

Cheryl retired at the end of 2010 and her final update, with assistance from 2 other OCS program icons, Melinda Mayes and Bob LaBelle, was published in June 2012. That update is attached.

ITOPF also deserves mention for their comprehensive tanker spill data. A recent chart is pasted below. ITOPF’s data are nicely presented on their website. No such data are available for international offshore production.

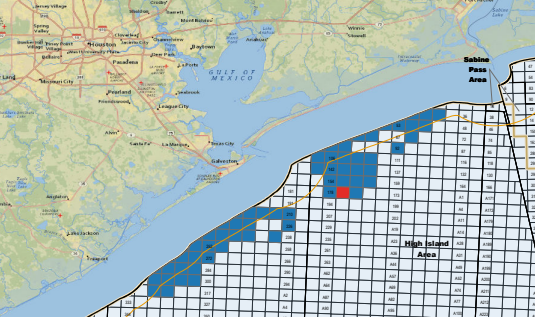

Posted in CCS, climate, energy policy, Gulf of Mexico, Offshore Energy - General, tagged CCS, Exxon, Focus Exploration, High Island 177, Lease Sale 259 on April 4, 2023| 2 Comments »

In addition to the 94 nearshore Texas leases Exxon acquired in Sale 257, the company was the sole Sale 259 bidder for all but one of 69 nearshore Texas blocks. The exception was High Island 177 (in red above). So who gets that lease?

If Exxon is just acquiring these leases for evaluation purposes in preparation for a possible CCS sale in the future, their lease acquisitions may be okay. If they are planning on retaining these leases for actual sequestration operations, that is not okay, at least not until a competitive process has been established for awarding or reclassifying such leases. To date, no lease terms or bid evaluation procedures have been proposed for carbon sequestration leases; nor has an environmental review been conducted pursuant to NEPA.

Questions about Gulf of Mexico carbon sequestrationPosted in Gulf of Mexico, Health, Offshore Energy - General, tagged BSEE, Coast Guard, Gulf of Mexico, offshore oil and gas facilities, sudden deaths on April 3, 2023| Leave a Comment »

In the past 2 years, at least 12 workers died suddenly at Gulf of Mexico facilities from “natural causes.” BSEE’s recent medical evacuation presentation provided information on 6 non-operational fatalities that occurred in 2022:

7/28: Employee (galley hand) was found in the bathroom non‐responsive with minimal electrical activity indicated on the EKG.

8/2 Advised of person down in the galley/T.V. area. Upon arrival in the area observed person on the floor being held by his supervisor. A white foam was coming out of his mouth and nose. Placed him on his side in order for the foam to drain. He was breathing and had a faint pulse. It was observed that he then appeared to stop breathing. Unable to find a radial or carotid pulse. CPR was started and AED was retrieved. AED instructions were followed. A shock was administered and CPR continued for approximately 50 minutes with no pulse or response.

8/18: Contract Personnel (CP) complained of not feeling well and went to his assigned room. It was noticed that CP did not come down for lunch and other personnel went to check on CP and CP was unresponsive.

9/7: CI was in galley of the M/V GO Triumph, waiting on weather, with co‐workers, when he made an exclamation and collapsed to the floor. Co‐workers and contract safety technician immediately ran to his aid. Breathing was sporadic for a minute then ceased and he was unresponsive.

9/23: At approximately 8:20 AM on September 23rd, platform personnel discovered an unresponsive employee (IP) face down on the deck. IP was rolled onto his back, evaluated, and CPR began. Other personnel were dispatched to retrieve AED and medical supplies, while one went to make notifications. Shortly after, personnel arrived with the AED, and it was applied to the IP. Personnel continued CPR while waiting for medical evacuation helicopter. At approximately 12:00 PM, IP was removed from facility by medical evacuation helicopter and subsequently, formally, pronounced dead.

10/21: Employee was assisting production personnel fueling the crane when he suddenly collapsed onto the platform deck and became unresponsive. Personnel on the platform quickly responded and immediately applied an AED to the Employee and began CPR. A medivac aircraft was dispatched for medical support assistance while platform personnel continued to resuscitate the

employee. Medivac personnel arrived on location and relieved personnel working on employee. Following an unsuccessful attempt to revive the employee, he was transported to Houma, La. and released to the Terrebonne Parish Coroner’s Office. Workers on the platform stated the employee was acting normal during breakfast time and during the morning safety meeting. The employee did not complain of any type of illness during the morning time prior to the event occurring.

Why are screened and presumably healthy offshore workers dying suddenly at what seems to be a historically high rate? Is this happening elsewhere in the offshore world? Is anyone investigating this disturbing trend? if not, why not?

As suggested in a previous post, further investigation should be a high priority for the Coast Guard and BSEE with appropriate medical assistance.

Posted in Gulf of Mexico, Offshore Energy - General, tagged 2023, Gulf of Mexico oil production, King's Quay, Murphy, Shell, Vito on March 31, 2023| Leave a Comment »

The encouraging start to 2023 GoM production is likely due, at least in part, to Shell’s Vito and Murphy’s King’s Quay ramping up production. Other deepwater startups should boost production later this year.

Posted in Gulf of Mexico, Offshore Energy - General, tagged Beacon, bp, Chevron, Equinor, Gulf of Mexico, Hess, Houston Energy, Lease Sale 259, Oxy, Red Willow, Shell, Top Ten, Woodside on March 31, 2023| Leave a Comment »

| company | no. of Sale 259 high bids (Sale 257 in parentheses) | total Sale 259 high bids ($ millions) |

| Chevron | 75 (34) | 108 |

| BP | 37 (46) | 46.7 |

| Shell | 21 (20) | 20.1 |

| Equinor | 16 (1) | 18.3 |

| Beacon | 13 (4) | 9.0 |

| Anadarko (Oxy) | 13 (30) | 8.6 |

| Red Willow | 13 (5) | 3.8 |

| Hess | 12 (2) | 8.3 |

| Woodside | 12 (8) | 6.3 |

| Houston Energy | 8 (5) | 11.6 |

Posted in CCS, energy policy, Gulf of Mexico, Offshore Energy - General, tagged GOM Shelf, Gulf of Mexico, Lease Sale 259, royalty rate on March 30, 2023| Leave a Comment »

As anticipated, the increase in royalty and rental rates appears to have further weakened interest in leases in the shallow waters of the Gulf of Mexico continental shelf. Note the sharp declines in both the number of blocks receiving bids and the bid amounts.

| lease sale | blocks with bids (excluding CCS bids) | sum of high bids ($million, excluding CCS bids) |

| 257 | 46 | $8.1 |

| 259 | 29 | $4.1 |