JL Daeschler is a pioneering subsea engineer and artist extraordinaire who is a native of France (Brittany) and lives in Scotland. He has shared 2 more of his exceptional drawings. (Click on the images to enlarge.)

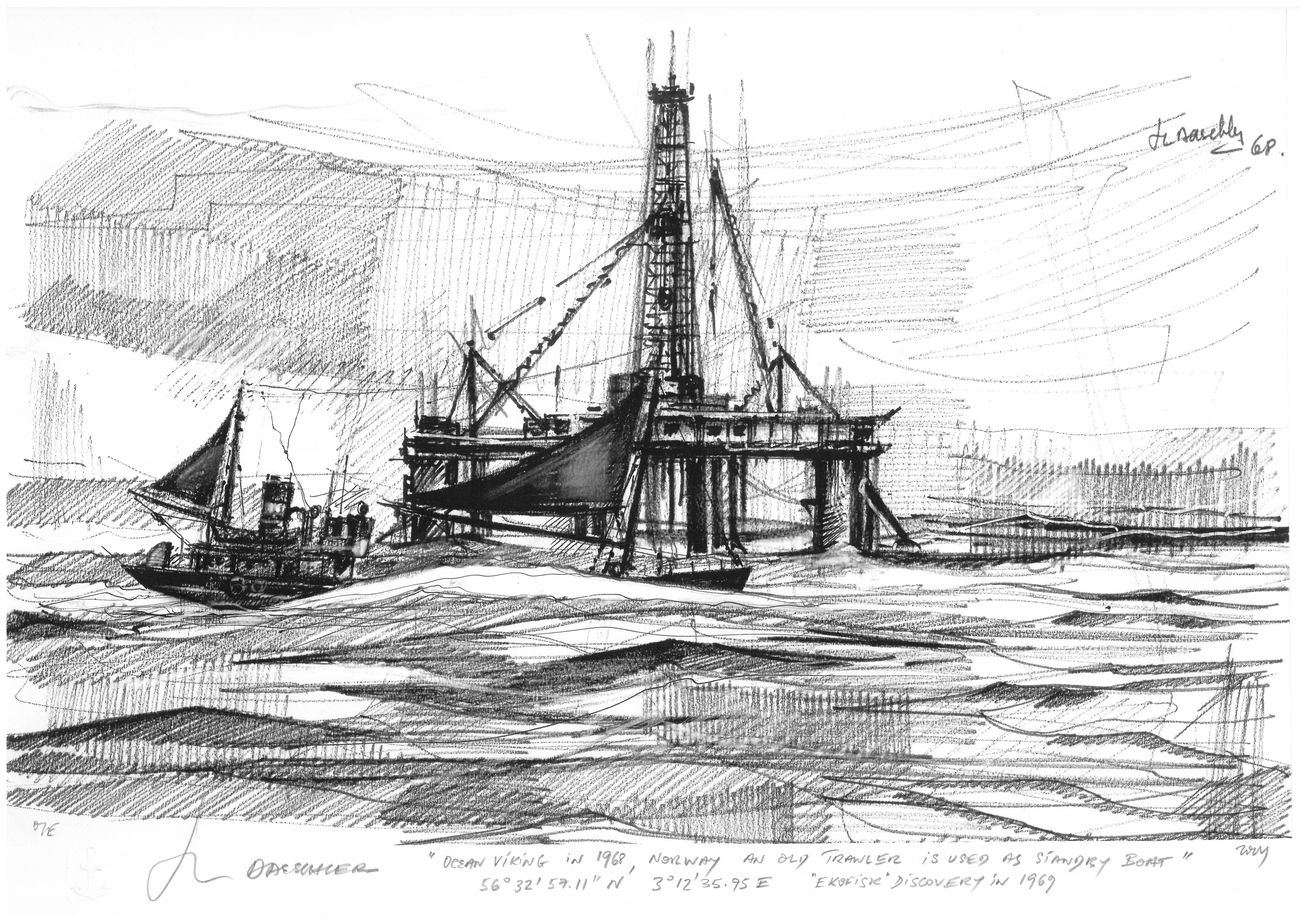

This is a drawing of the Ocean Viking (Odeco) in the Norwegian North Sea in 1968. The rig was built in Oslo as a sister ship to the Ocean Traveler, which was already working at the same location. The Ekofisk field was discovered later in 1969. The mast-type derrick could be lowered for long ocean tow or bridge clearance. It would have been difficult to evacuate a 100 + personnel to the standby vessel, a decommissioned trawler. Things have changed so much in 56 years!Inclined jack up legs with rack and pinion drive ( Marathon Le Tourneau), Gulf of Mexico

The table in the Sale 259 bid rejections post has been corrected below. That table incorrectly reported that subsequent bids for Keathley Canyon Blocks 745 and 789 were rejected at Sale 261. Those bids were in fact accepted. Houston Energy was identified as the submitter rather than Beacon Offshore Energy, the company that, per the bidding data, had the largest ownership share. (See the bidding partnership pasted below.)

The acceptance of those 2 bids significantly increases the net gain to the government as a result of the Sale 259 bid rejections. See the corrections in red to the table:

The active rig count in the GoM in 2001 was 148 (AL-4, LA-119, TX-25), which is >8 times the current Baker Hughes rig count of 18. The 2001 rig count was not a one year blip; the number of rigs active in the GoM exceeded 100 for the ten year period from 1994-2003.

While the current rig count is anemic by comparison, the capabilities of the fleet are anything but. Below is a list derived from drilling contractor status reports of deepwater rigs now operating in the Gulf.

All of these rigs are dynamically positioned and are capable of drilling in 12,000′ of water. They have dual derricks and 15,000 psi rated BOP rams (one has a 20,000 psi stack, and another can be upgraded to 20,000 psi). The annular preventers are rated at 10,000 psi. All have impressive storage and hook load capacities, the latest tubular handling equipment, advanced control systems, and efficient power generation.

Note that most of the rigs fly the flag of the Marshall Islands. This “flag of convenience” registration is preferred for reasons related to taxation and operational freedom. For the record, the fact that the Deepwater Horizon was registered in the Marshall Islands had little to do with the Macondo blowout. The DWH was subject to all Coast Guard and MMS regulations under the OCS Lands Act.

The main cause of the Macondo blowout was the poorly planned and executed well suspension operation. Certain equipment capability, maintenance, and employee training issues were contributing factors. However, with that said, the Marshall Islands report on the blowout candidly acknowledges that “the complexity of and interdependence between the drilling and marine systems and personnel suggests a need for increased communication and coordination between the flag State and coastal State drilling regulators.” Hopefully, that coordination is being achieved and the risks associated with the fragmented regulationof mobile drilling units are being effectively managed.

Contractor

Rig

Operator

Est. end date

Flag

Transocean

Deepwater Titan

Chevron

3/2028

Marshall Islands

Transocean

Deepwater Atlas

Beacon

4/2025

Marshall Islands

Transocean

Deepwater Poseidon

Shell

4/2028

Marshall Islands

Transocean

Deepwater Pontus

Shell

10/2027

Marshall Islands

Transocean

Deepwater Conqueror

Chevron

3/2025

Marshall Islands

Transocean

Deepwater Proteus

Shell

5/2026

Marshall Islands

Transocean

Deepwater Thalassa

Shell

2/2026

Marshall Islands

Transocean

Deepwater Asgard

Hess

4/2024

Marshall Islands

Stena

Evolution

Shell

4/2029

Marshall Islands

Noble

Stanley Lafosse

???

11/2024

Liberia

Noble

Valiant

LLOG

2/2025

Marshall Islands

Noble

Globetrotter I

Shell

5/2024

Liberia

Noble

Globetrotter II

Shell

5/2024

Liberia

Valaris

DS-18

Chevron

8/2025

Marshall Islands

Valaris

DS-16

Oxy

6/2026

Marshall Islands

Diamond Offshore

BlackHawk

Oxy

10/2024

Marshall Islands

Diamond Offshore

BlackHornet

bp

3/2027

Marshall Islands

Diamond Offshore

BlackLion

bp

9/2026

Marshall Islands

Short video about the Stena Evolution, the newest entry to the Gulf of Mexico fleet:

After 5 months of investigation, the Main Pass Oil Gathering (MPOG) system has finally been cleared for production. (The Coast Guard update only says that the pipeline passed the integrity test, but I assume the operators may resume production though the MPOG system.)

So what was the source of the November sheen and what was the basis for the 1.1 million gallon spill volume estimate? The sheen was not indicative of a spill of that magnitude. Did the Coast Guard et al assume a worst case loss from the MPOG system, even though no leak had been identified?

Is this the most oversight ever for a pipeline integrity test?

The removal and replacement of the spool piece and the subsequent integrity test of the MPOG line were conducted under the close supervision of the Unified Command and Pipeline and Hazardous Materials Safety Administration. During both operations, spill response vessels were on site, along with divers, remotely operated vehicles, helicopters equipped with trained oil observers and multi-spectral imaging cameras, and other containment and recovery equipment. No material discharge of oil was observed during these operations.

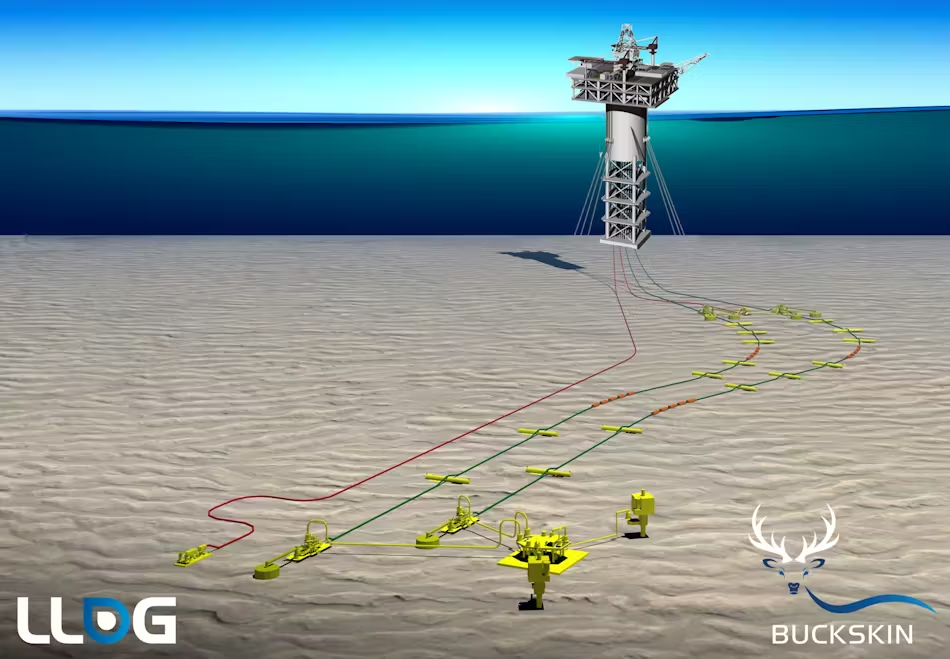

Houston, TX, March 29, 2024. Beacon Offshore Energy LLC (“Beacon”) announced today the completion of the divestment of its non-operated interests in certain fields in the deepwater Gulf of Mexico in accordance with a previously executed definitive agreement with GOM 1 Holdings Inc., an affiliate of O.G. Oil & Gas Limited. The divestment includes Beacon’s 18.7% interest in the Buckskin producing field, 17% interest in the Leon development, 16.15% interest in the Castile development, 0.5% interest in the Salamanca FPS/lateral infrastructure, and 32.83% interest in the Sicily discovery.

According to BOEM records, GOM 1 HOLDINGS INC, a Delaware company, registered with BOEM effective 3/15/2024. The parent entity, O.G. Oil & Gas Limited, is a privately held E&P company incorporated in 2017 and based in Singapore.

O.G. Oil & Gas Ltd is part of the Ofer Global Group, “a private portfolio of international businesses active in maritime shipping, real estate and hotels, technology, banking, energy and large public investments.”

After a partial takeover by O.G Oil & Gas Limited in 2018, New Zealand Oil and Gas is now 70% owned by the Ofer Global Group. Among other interests, NZ Oil and Gas produces from fields offshore Taranaki, NZ.

Because they are jointly and severally liable for safe operations and decommissioning, minority investors should take a strong interest in safety management and financial assurance. Investors should remember that partners are adversely affected by the mistakes of the operating company. Anadarko and Mitsubishi took a hit following the Macondo blowout. To what extent had they been monitoring bp’s risk and safety management programs for drilling operations?

… and you deniers are fully responsible. There’s a reason why Texas is the most affected state 😉

But fear not, we will line our shores with wind turbines, restrict offshore oil and gas leasing, and subsidize carbon disposal in the Gulf of Mexico. All of this “help” will have a negligible effect on the climate, which will continue to change as it always has and always will.

14 of the high bids at Gulf of Mexico Lease Sale 259 were rejected. Did those tracts receive bids at sale 261? What was the net gain or loss of revenue? See the summary bullets and table below

6 of the 14 tracts received no bids whatsoever

5 of the 14 tracts received higher bids that were accepted.

2 tracts received substantially higher bids that were again rejected

1 tract received a lower bid that was accepted

net bonus revenue gain to the govt from the bid rejections (pending re-offering at future sales): $1,032,877

net bonus revenue gain = 0.27% of the total high bids at sale 261

net loss in future rental and royalty payments: ????

For a net bonus revenue gain to date of only 1/4 of one per cent, 8 of the 14 sale 259 tracts with rejected high bids remain closed to exploration. The timing of any future sales is very much in doubt given the minimalist 5 year leasing plan and the associated legal challenges.

Current bid evaluation practices only make sense if regular lease sales are held on a predictable schedule, as has historically been the case.

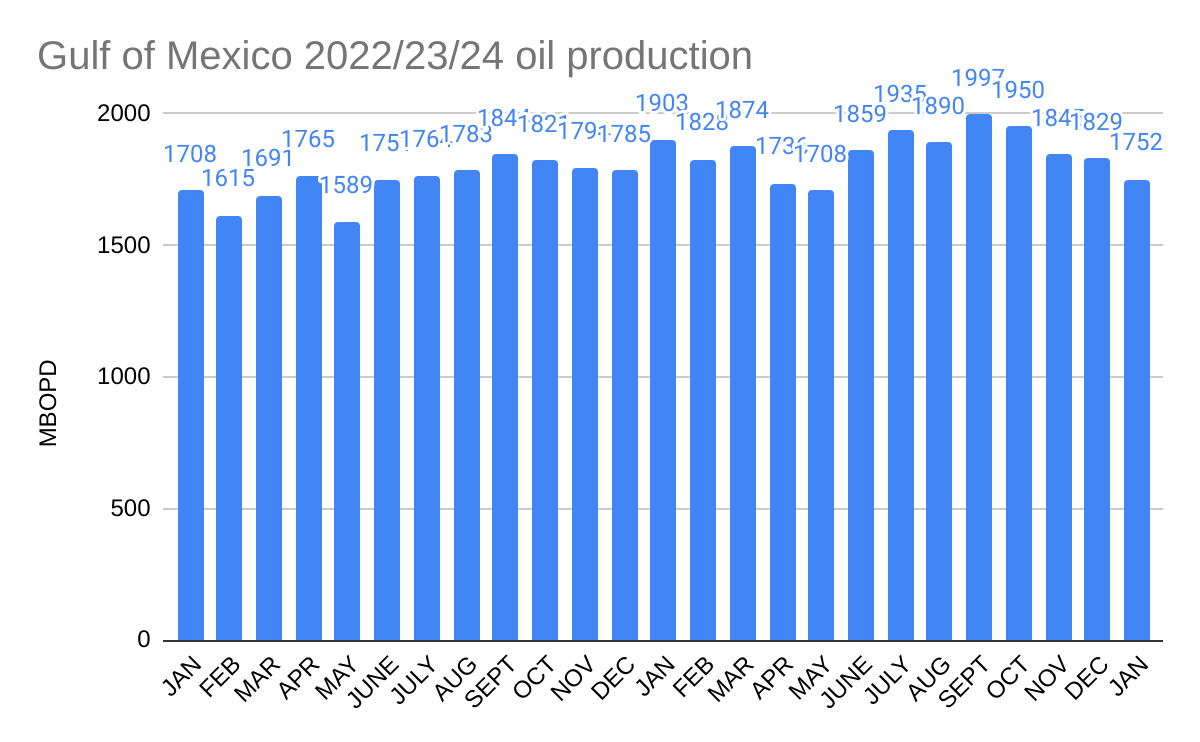

Average GoM oil production from Nov. to Jan. was more than 130,000 BOPD below the July to Oct. average. Production in Jan. 2024 was 245,000 BOPD lower than Sept. 2023 production. (See the table and chart below.)

The production shut-ins associated with the mysterious November sheen in the Main Pass area were no doubt a contributing factor to the decline, but the magnitude and duration of those shut-ins has not been disclosed. The source of the sheen has apparently still not been determined, nor has any information been provided on the status of the Federal investigation. The absence of transparency is disappointing.

Swimming upstream against the Federal policy current, Gulf of Mexico drilling is demonstrating impressive forward progress. Baker Hughes reports 22 active GoM rigs on 3/15/2024, an increase of 3 from the previous week.

Glancing at the charts, this appears to be the highest GoM rig count since Nov. 2019, and is double the recent low of 11 in 2022.

It’s unclear whether Baker Hughes is including the CCS drilling operation offshore Texas. If so, the actual oil and gas rig count is 21 rather than 22.

Baker Hughes also reports 1 active rig offshore California (decommissioning?) and 1 active rig offshore Alaska (Endicott or Northstar?)

Per Baker Hughes, no rigs are currently active offshore Canada.