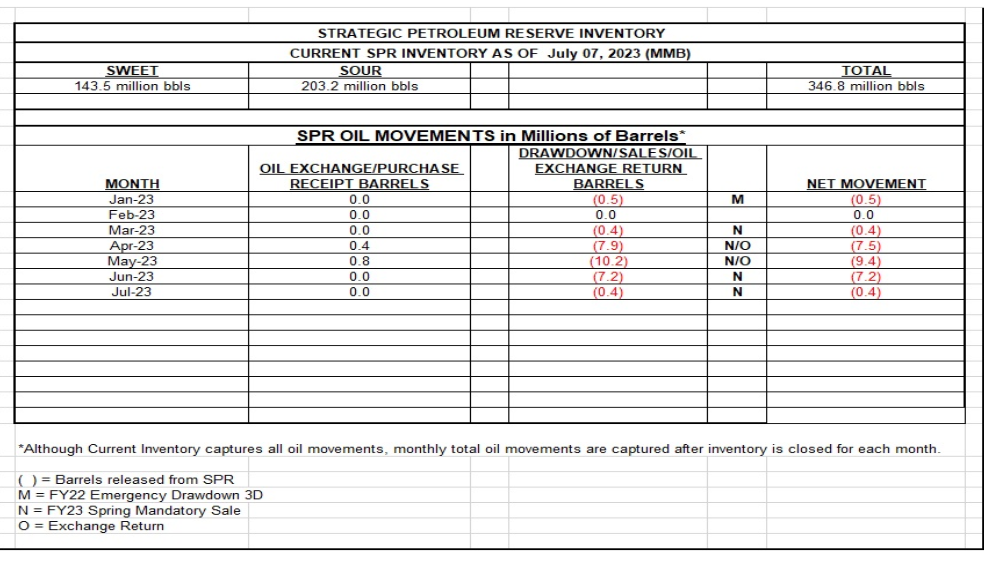

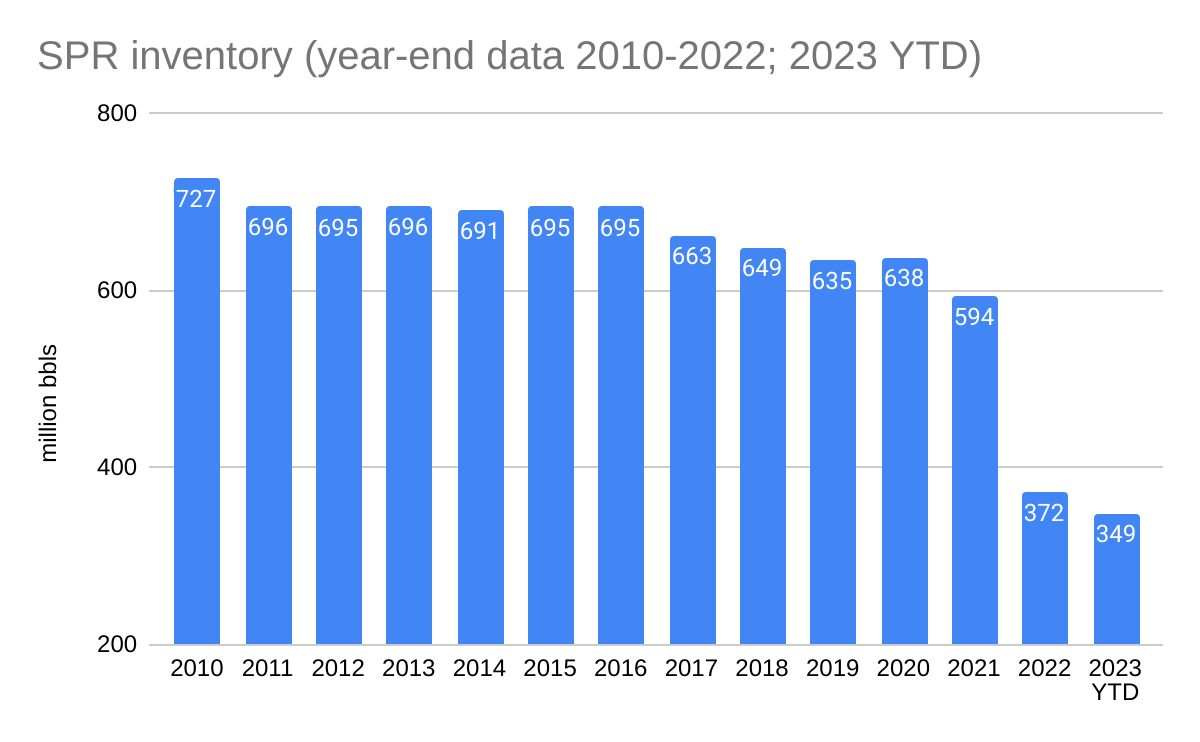

The Strategic Petroleum Reserve has held steady at 346.8 million bbls for the past 3 weeks. DOE’s latest update is as of 7/28/2023.

Archive for the ‘energy policy’ Category

SPR: at least it’s not going down

Posted in energy policy, tagged SPR depletion, Strategic Petroleum Reserve on July 31, 2023| Leave a Comment »

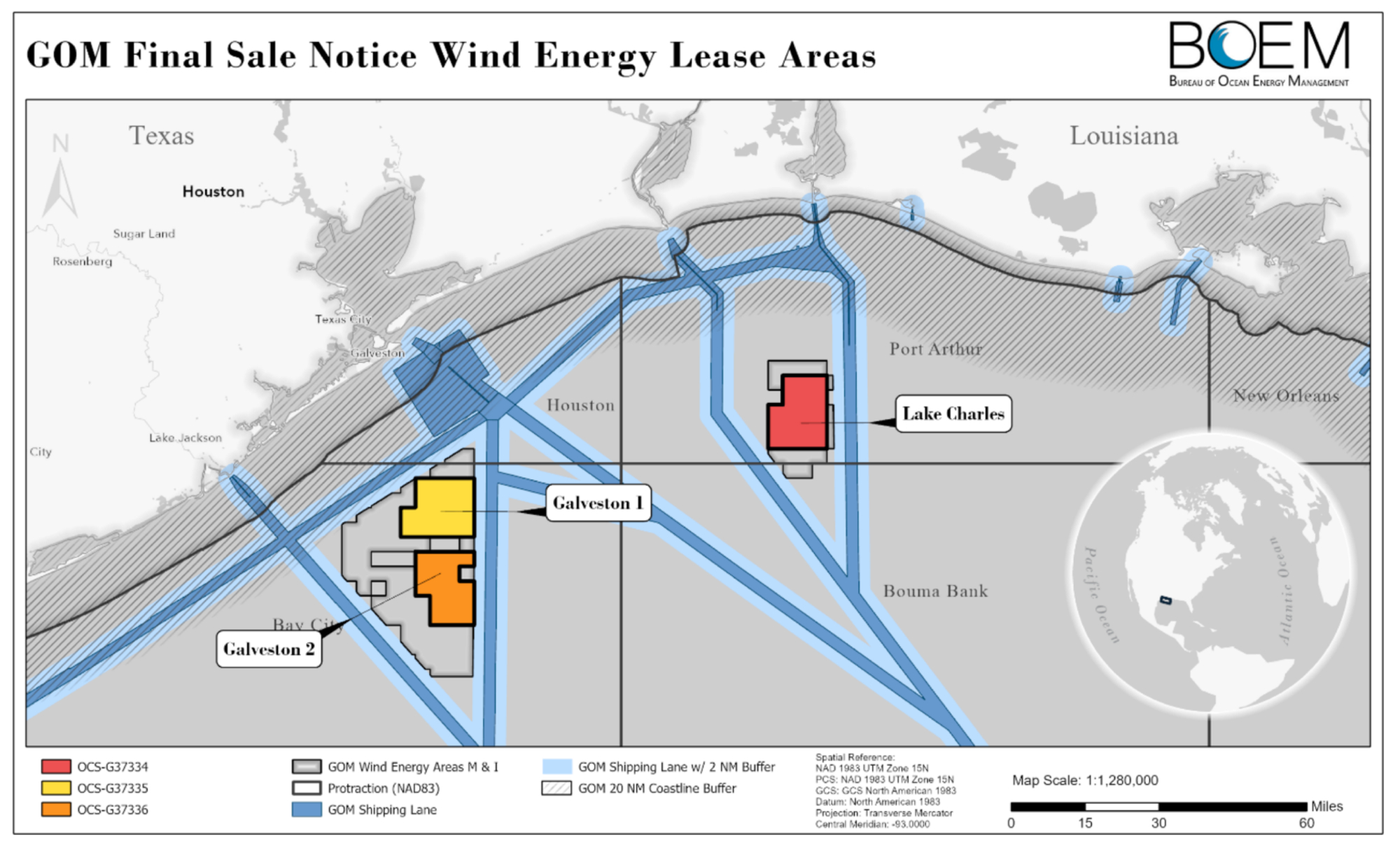

Good work by BOEM in siting the Gulf of Mexico wind leases, but their analysis misidentifies 94 oil and gas leases

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, Offshore Wind, tagged CCS, CCS regulations, Gulf of Mexico wind auction, wind leases on July 26, 2023| Leave a Comment »

BOEM’s Final Sale Notice for the upcoming Gulf of Mexico wind auction identifies 3 lease areas (see map below). Wind operations in these areas should not significantly conflict with other GoM activities, including oil and gas operations.

Those who followed Exxon’s recent lease acquisitions may be amused by the map below from BOEM’s siting analysis document. The 94 Exxon leases acquired at Oil and Gas Lease Sale 257 (yellow blocks) are misidentified as “Carbon Capture Lease Blocks.” As has been discussed at length on this blog (most recently here), Sales 257 and 259 were oil and gas lease sales. Although Exxon’s intentions are now well known, they may not conduct carbon sequestration operations on these leases unless they are competitively reissued or converted. (Is BOEM’s siting document implying that conversion of the Exxon leases is a fait accompli?) The regulations for such conversions, and for CCS operational activities, have yet to be promulgated. A draft of these regulations is expected later this year, and the comments should be spirited and diverse.

Opportunity to formally comment on offshore carbon sequestration is on the horizon

Posted in CCS, energy policy, Gulf of Mexico, Offshore Energy - General, Regulation, tagged carbon sequestration, CCS, DOI, Exxon, infrastructure bill, Lease Sale 257, Lease Sale 259, Ocean Dumping, OCSLA on July 18, 2023| Leave a Comment »

ENERGYWIRE has reported that the Department of the Interior will publish the legislatively mandated carbon sequestration rule later this year. Given that even close followers of the OCS program were completely unaware of the enabling legislative provisions prior to their enactment, the proposed DOI rule will provide the first opportunity to formally comment.

Within the oil and gas industry and the environmental community, there are considerable differences of opinion about carbon sequestration in general, and more specifically, offshore sequestration. All interested parties are encouraged to submit comments on these important regulations.

Some background information on the sequestration legislation and subsequent actions:

- 11/15/2021: The “Infrastructure Investment and Jobs Act” was enacted with surprising late additions to facilitate offshore carbon sequestration. These provisions:

- amend the OCS Lands act to authorize “the injection of a carbon dioxide stream to sub-seabed geologic formations for the purpose of long-term carbon sequestration.”

- exempt CO2 injection from the restrictions on ocean dumping by stipulating that such injection “shall not be considered to be material (as defined in section 3 of the Marine Protection, Research, and Sanctuaries Act of 1972.” Without this exemption, CO2 streams would clearly be “material,” as defined in 33 U.S.C. 1402, and would be subject to the stringent requirements of that act.

- direct that “not later than 1 year after the date of enactment of this Act, the Secretary of the Interior shall promulgate regulations to carry out the amendments made by this section.” (This deadline has been missed, which is rather common for such directives.)

- authorize $2.5 billion in Federal funding for commercial CCS projects and much more for other carbon capture and sequestration (CCS) activities.

- 11/17/2021: Two days after the enactment of this legislation, Exxon was the sole bidder on 94 nearshore tracts with very limited oil and gas production potential. This was an oil and gas lease sale and there were no provisions for carbon sequestration leasing. Nonetheless, Exxon was awarded leases for all 94 tracts.

- 3/29/23: Exxon bid at Sale 259 on 69 nearshore tracts with little oil and gas potential. Once again, this was strictly an oil and gas lease sale and Exxon’s CCS intentions were clear. Nonetheless, the leases were awarded.

Exxon and other companies intend to commercialize carbon sequestration, and Exxon projects an astounding $4 trillion CCS market by 2050. Such a market will of course be dependent on mandates and subsidies, and the costs will ultimately be borne by taxpayers and consumers.

Is it not a bit unsavory and hypocritical for hydrocarbon producers to capitalize on the capture and disposal of emissions associated with the consumption of their products? Perhaps companies that believe oil and gas production is harmful to society should exit the industry, rather than engage in enterprises that sustain it.

More:

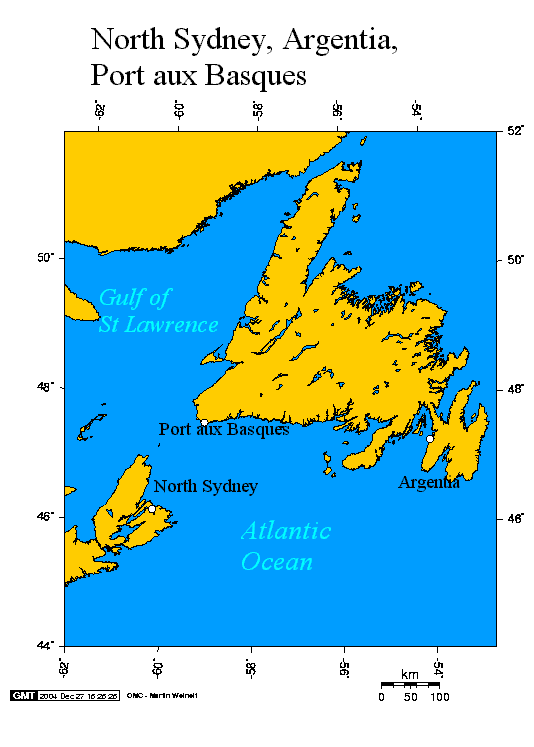

Jones Act workaround is good for Newfoundland

Posted in Canada, energy policy, Offshore Energy - General, Offshore Wind, Regulation, tagged Argentia, Jones Act, monopiles, Newoundland, Wind Energy on July 17, 2023| Leave a Comment »

The Jones Act, protectionism at its finest, was enacted 113 years ago, and stipulates that vessels which transport merchandise or people between two US points must be US built, flagged, owned, and crewed. Congress tightened the screws further by ordaining that offshore energy facilities, including wind farms, are US points. That precludes the transportation of wind turbine components from US ports to offshore wind farms.

The Jones Act has thus provided an opportunity for the Port of Argentia, a former US Navy base in southeast Newfoundland, and the port is set to become a key node in the offshore wind supply chain. Monopiles constructed in Europe will be stored in Argentia, until they are delivered to US wind farms in the North Atlantic. Kudos to the folks at the Port of Argentia for taking advantage of this opportunity.

SPR: more red ink

Posted in energy policy, tagged DOE, SPR depletion, SPR refill, Strategic Petroleum Reserve on July 14, 2023| Leave a Comment »

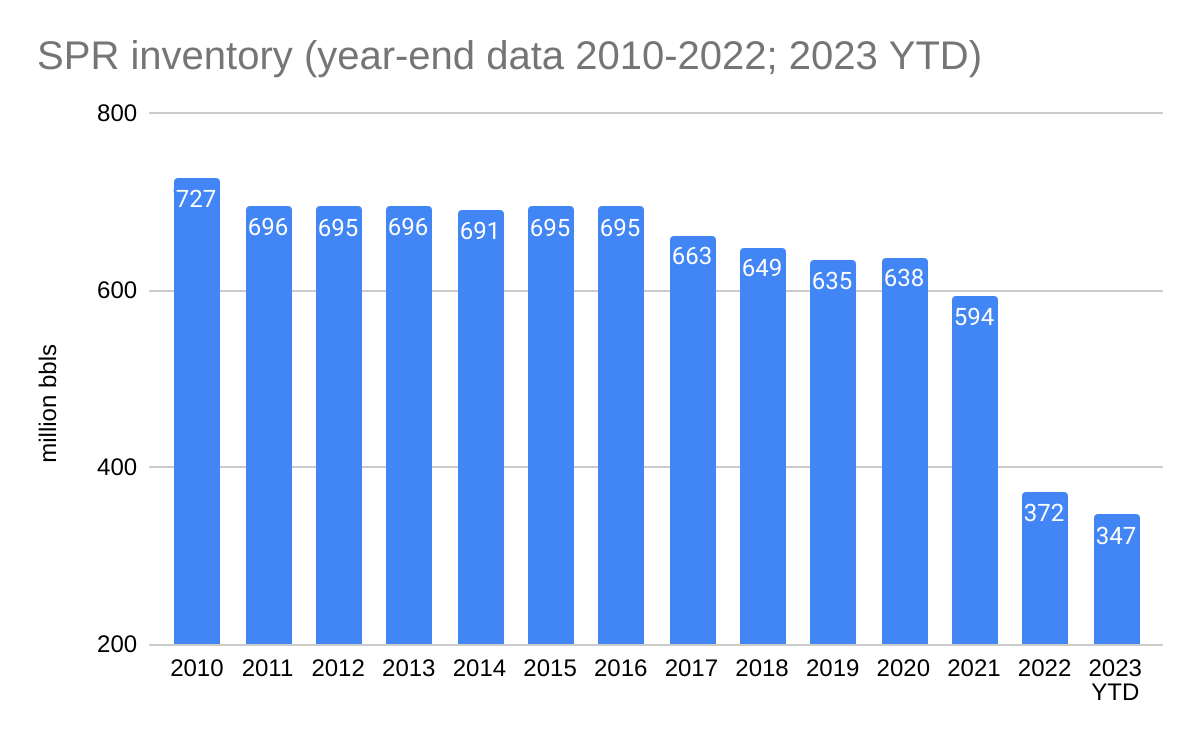

The Strategic Petroleum Reserve is ⬇ to 346.8 million barrels, the lowest volume since August 19, 1983, when the SPR was still being filled.

But fear not, 6 million barrels, which is less than 1/4 of the amount withdrawn just in 2023 YTD, are to be added in the fall, and Secretary Granholm assures us that the SPR will be refilled (but not completely and maybe not until the Administration’s second term 😀).

Keep in mind that DOE only intends to buy when prices are <$72/bbl, that the maximum refill rate is 685,000 bopd, and that acquisition, operational, and maintenance delays are to be expected .Filling the reserve to its 727 million barrel capacity was a 28 year process.

More on decommissioning, bankruptcy, and compliance

Posted in decommissioning, energy policy, Gulf of Mexico, Offshore Energy - General, tagged bankruptcy, BSEE, compliance, decommissioning, Matagorda Island on July 12, 2023| Leave a Comment »

For the first time in the history of the US offshore oil and gas program, taxpayers will be funding the plugging of OCS wells. This should be viewed as a collective failure by government and industry. Nearly 34 years have passed since the Alliance bankruptcy, the first of many wake-up calls, and we still haven’t figured this out.

Per BSEE’s recent announcement, Federal funds will be used to plug wells in the Matagorda Island (MI) area of the Gulf of Mexico (see map below). Based on a BSEE presentation and BSEE borehole data, these wells were drilled by Matagorda Island Gas Operations LLC, a company that filed for bankruptcy in 2014.

Prior to the bankruptcy filing, Matagorda Island Gas was cited for 112 violations on 108 inspections. This INC/inspection rate is approximately double the Gulf of Mexico (all operators) rate in a typical year (0.52 in 2022), and is 4 to 25 times higher than the rate for the 2022 Honor Roll companies.

BOEM’s proposed financial assurance rule (decommissioning): preliminary observations

Posted in California, decommissioning, energy policy, Gulf of Mexico, Regulation, tagged BOEM, decommissioning, financial assurance, proposed rule, reverse chronological order on July 10, 2023| Leave a Comment »

Some preliminary thoughts about BOEM’s proposed revision to the decommissioning financial assurance regulations for US offshore oil and gas operations:

- BOEM has rather surprisingly proposed to eliminate consideration of a company’s compliance record in determining the need for supplemental financial assurance. An opposing view will be posted tomorrow.

- If a lease has proved reserves with a value of at least three times that of the estimated decommissioning cost, no supplemental financial assurance would be required. Comparing two imprecise and variable estimates is neither a simple nor reliable method for determining the need for supplemental financial assurance. BOEM should look at the history of the Carpenteria field (Santa Barbara Channel) and the reserve estimates that were provided to discount decommissioning risks. More on this at a later date.

- Transferor liability applies only to those obligations existing at the time of transfer; new facilities, or additions to existing facilities, that were not in existence at the time of any lease transfer are not obligations of a predecessor company and are considered obligations of the party that built such new facilities and its co- and successor lessees. This is a good policy, but is difficult to implement. Some of the complexities may need to be addressed. More later.

- The “reverse chronological order” provision was withdrawn in April, so there is no defined process for issuing decommissioning orders to predecessor lessees. Is it good policy to first issue such orders to companies who may have owned leases decades ago, in some cases prior to the establishment of transferor liability in the 1997 MMS “bonding rule?”

- The proposed rule would clarify that BOEM will not approve the transfer of a lease interest until the transferee complies with all applicable regulations and orders, including the financial assurance requirements. BOEM needs to be firmly enforce this policy. See tomorrow’s post.

- The proposed rule would not allow BOEM to rely upon the financial strength of predecessor lessees when determining whether, or how much, supplemental financial assurance should be provided. This is a good provision.

- BOEM proposes to use the P70 probabilistic value to set the amount of any required supplemental financial assurance. These estimates do not seem sufficiently conservative to protect other parties and the public in the event of default. This is particularly true after storm damage which can increase plugging costs more than tenfold.

- The probabilistic cost estimates were updated in 2020 and are based on data submitted subsequent to 2016 and 2017 NTLs. How often will these estimates be updated?

- The final rule should specify that funds may not be withdrawn from decommissioning accounts for operational purposes, and that BOEM approval is required for such withdrawals.

Holiday message: Opportunity + Ingenuity ➡ Energy Independence + Prosperity

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, Uncategorized, tagged energy independence, Exxon, Gulf of Mexico, Permian Basin on June 30, 2023| Leave a Comment »

As we approach the 4th of July, remember this:

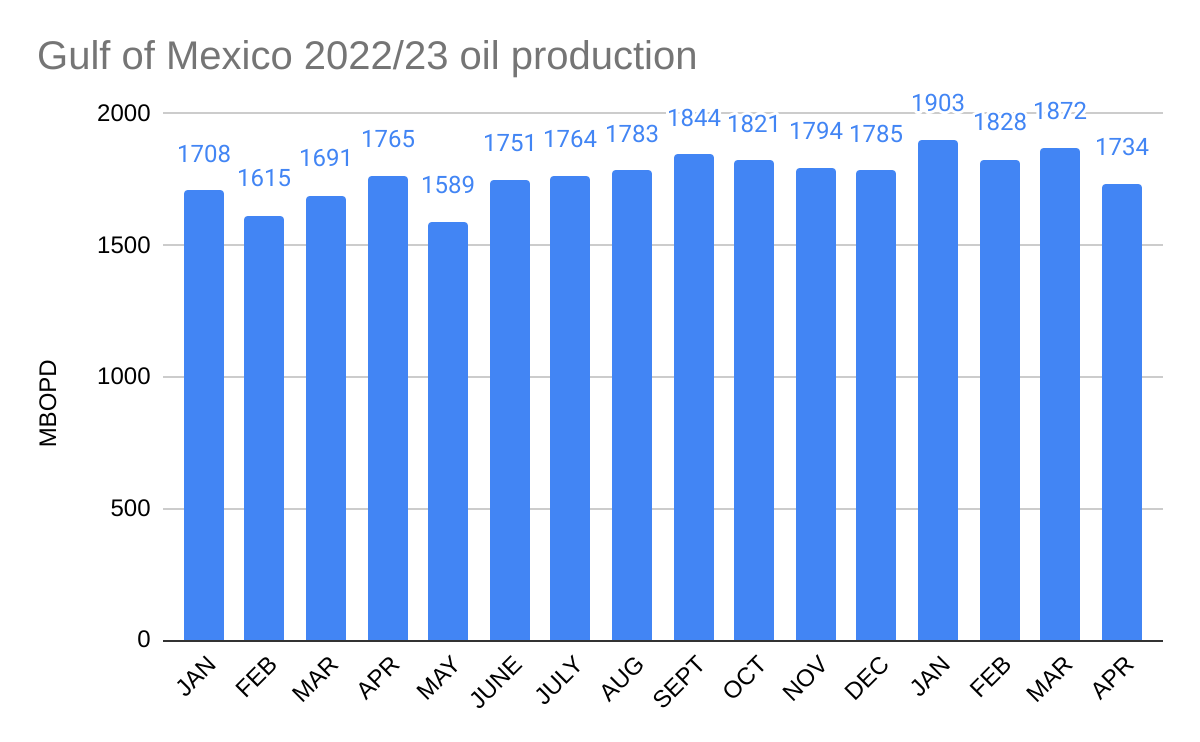

In 1979 Gulf of Mexico oil production had declined to 263 million barrels and many believed that further declines were inevitable. 40 years later, a record 693 million barrels were produced.

Onshore, lateral drilling and hydraulic fracturing capabilities are continuing. As a result, Exxon and others are predicting projecting higher recovery factors in the Permian Basin. Per Exxon CEO Darren Woods: “We are beginning to see the signs of some very promising new technologies that will significantly improve recovery.”

Opportunity + Ingenuity ➡ Energy Independence + Prosperity

GoM production slumps in April; SPR slide continues

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, tagged Gulf of Mexico production, SPR depletion, Strategic Petroleum Reserve on June 30, 2023| Leave a Comment »

Meanwhile, the Strategic Petroleum Reserve is down to 348.6 million barrels as of June 23, but 6 million barrels, a relative drop in the bucket, are to be added in the fall.

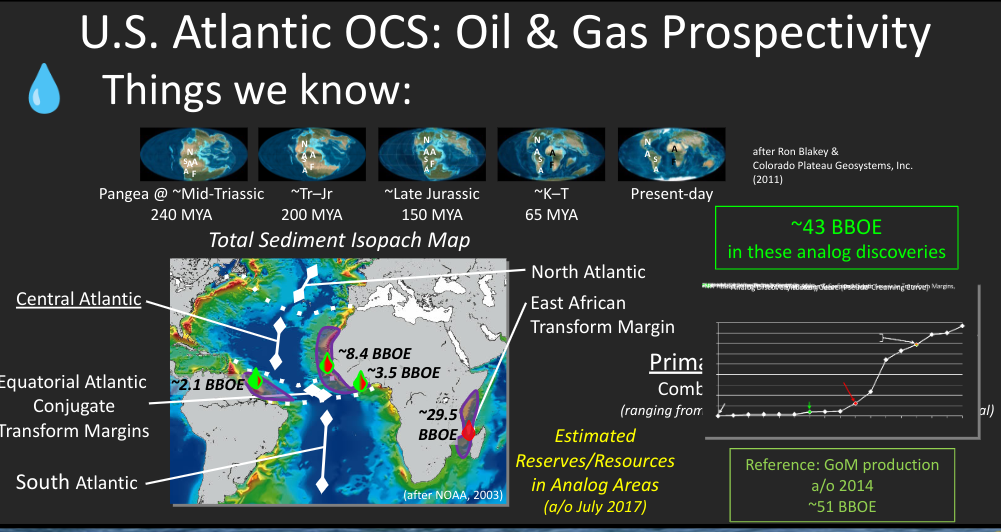

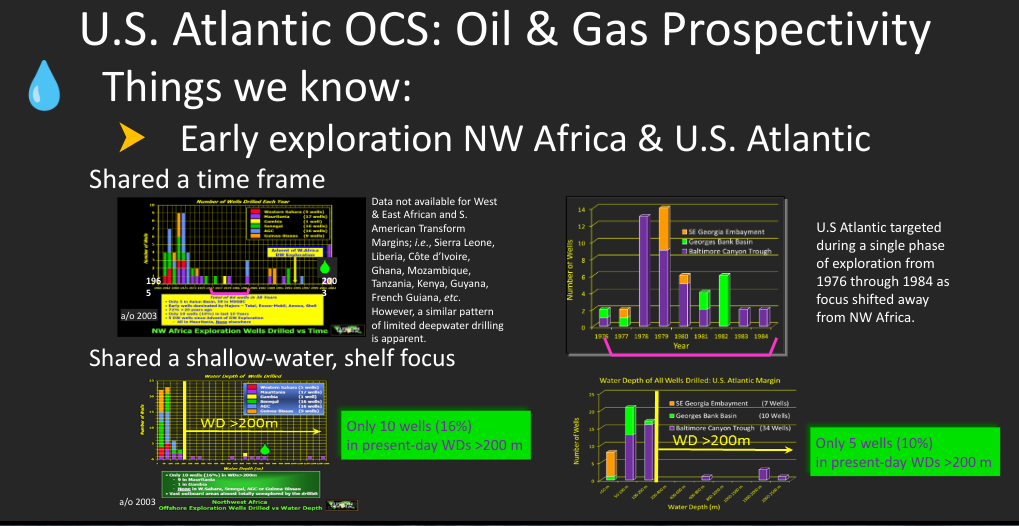

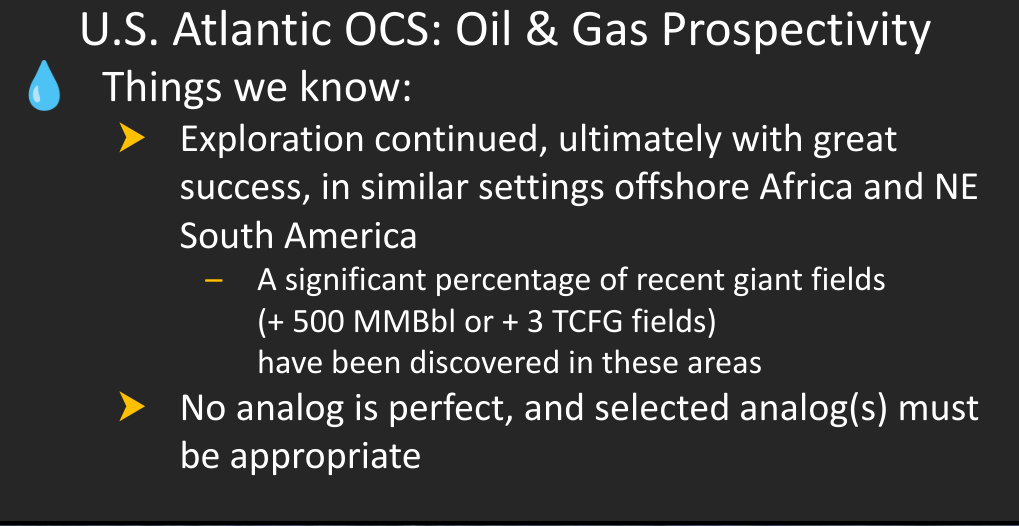

Pangea, Paul Post, West Africa, and the Atlantic oil and gas puzzle

Posted in energy policy, Guyana, Offshore Energy - General, tagged Atlantic oil and gas, BOEM, Mauritania, pangea, Paul Post, Senegal on June 20, 2023| Leave a Comment »

Until the late Triassic period, Virginia, the Carolinas, and Georgia were cojoined with Mauritania and Senegal as part of the Pangea super-continent. These Pangea neighbors share a common ancient geology.

Paul Post believed the untested West African analogs in the US Atlantic were highly prospective, and could contain >20 billion BOE. Paul was not alone in his thinking about Atlantic resource potential. Sadly, Paul is no longer with us 😥, so I’m sharing a few of his slides as a reminder of his important work. I have also attached his 2016 report and am linking the 2021 update.

Given the current Atlantic moratoriums and the steep legal, social, and political barriers that would have to be cleared, evaluating the US Atlantic is not imminent. However, nearly all Atlantic nations and their Caribbean and North Sea cousins have exploration programs and some have been wildly successful. Oil and gas consumption will be stable or growing for the foreseeable future, and it’s important to better understand the petroleum potential of our Atlantic continental margin.