An internal memo from the U.S. Interior Department suggesting that the agency set the highest possible royalty fee on potential oil and gas development before last year’s Cook Inlet lease sale is drawing blowback from the Democratic chair of the Senate Energy and Natural Resources Committee.

West Virginia Sen. Joe Manchin said in a statement he was “appalled” by the memo, which he said was leaked and prioritized a “radical climate agenda” over the energy needs of Alaskans and the U.S.

Anchorage Daily News

From the decision memo:

While a 16 ⅔ percent royalty may be more likely to facilitate expeditious and orderly development of OCS resources and potentially offer greater energy security to residents of the State of Alaska, a reasonable balancing of the environmental and economic factors for the American public favors the maximum 18 ¾ percent royalty for Cook Inlet leases.

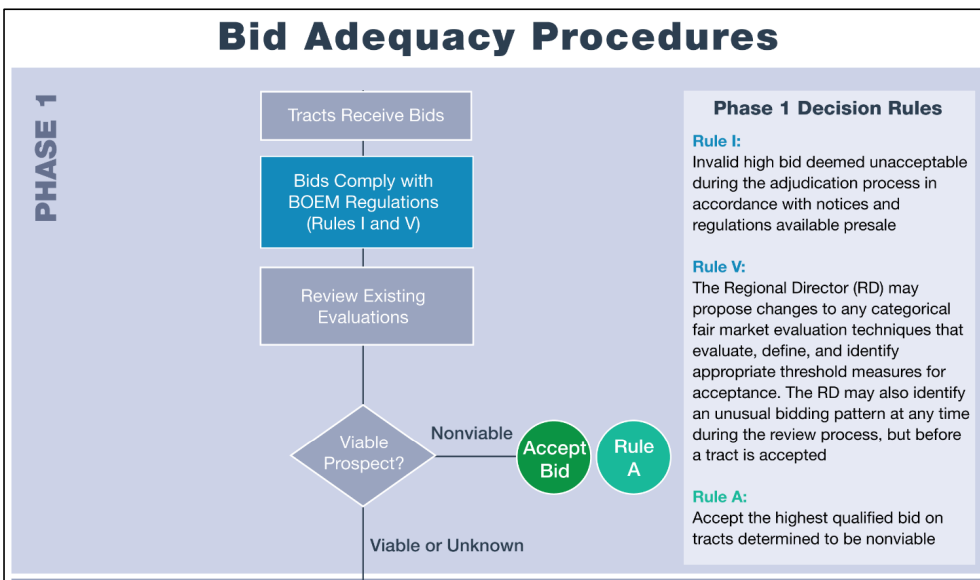

Sale 258 Decision Memo

The lower royalty rate probably would not have made much difference in the outcome of this sale, which only drew one bid, but the attitude expressed in the decision memo is rather disappointing given the Department’s mission, as expressed in the OCS Lands Act, to make resources available for expeditious and orderly development.

What might have made the sale more attractive was royalty suspensions, Option D.5.b (below). This would have been the best means of supporting the objectives of Senator Manchin, the other authors of the congressional leasing mandate, and the State of Alaska.

Option D.5.b: Offer Royalty Suspensions

BOEM could offer royalty suspensions with the goal of making resources available for expeditious and orderly development. However, BOEM does not recommend royalty suspensions as the recommended lease term options are expected to balance the goals outlined earlier in this memo

Sale 258 Decision Memo

Those who are concerned by the Sale 258 Decision Memo should be more troubled by the Proposed 5 Year Leasing Plan, most notably this stunning sentence which justifies the minimalist plan and signals a phasing out of offshore oil and gas leasing:

“The long-term nature of OCS oil and gas development, such that production on a lease can continue for decades makes consideration of future climate pathways relevant to the Secretary’s determinations with respect to how the OCS leasing program best meets the Nation’s energy needs.“

5 Year Leasing Program, p.3

Read Full Post »