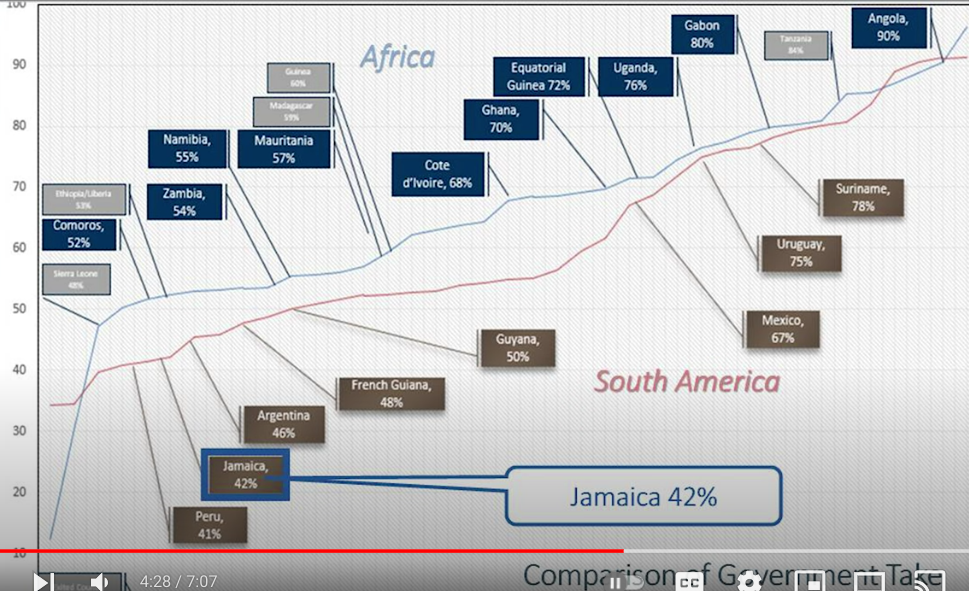

As reported in January, United Oil and Gas received a 2 year extension from the Government of Jamaica on their Walker Morant License. Below is a United video produced for prospective partners.

While the investment risk is undeniable, the reward potential is high.

Below is an interesting slide from the United presentation that compares the government’s take of production revenues for various African and S. American nations.

The Adjusted Delayed Value (ADV), which takes into account the effects of delaying bonuses and future royalty payments, ranged from 1.3 to 9.2 times the high bids.

Perhaps the closest calls were Chevron’s two Walker Ridge bids which had ADV to bid ratios of only 1.3 to 1.4.

The main concern going forward is the absence of a consistent, predictable leasing schedule for the 3.7% of the OCSthat may be considered for leasing. BOEM’s new methodology, which will be applied at the next lease sale (whenever that might be), does not require the bureau to estimate the delay period between the sale being evaluated and the projected next lease sale. Given that the new 5 year plan calls for a maximum of 3 lease sales, the gap between sales has become a much more significant factor just as the new guidance is being implemented.

The new 5 year “leasing plan” is intended to restrain OCS production in deference to “net zero” pathways. This strategy discourages interest from exploration and production companies. US offshore leases, which are by far the world’s smallest, are even less attractive when you don’t know if and when you will be able to acquire the nearby tracts that may be needed for economical deepwater development. This is not the way to obtain fair market value for public resources.

Block

No. of bids

High Bid ($)

MROV($) ADV($)

High Bidder

MROV/bid ADV/bid

MC 711

1

584,700

6,600,000 2,400,000

bp

11.3 4.1

MC 896

1

641,628

6,100,000 1,600,000

Shell

9.5 2.5

GC 182

1

800,085

3,900,000 2,600,000

Anadarko

4.9 3.2

GC 183

1

800,085

9,100,000 6,000,000

Anadarko

11.4 7.5

GC 226

1

800,085

2,100,000 1,600,000

Anadarko

2.6 2.0

GC 227

2

974,628

13,000,000 9,000,000

Shell

13.3 9.2

GC 345

1

1,095,615

13,000,000 5,300,000

Murphy

11.9 4.8

GC 346

1

845,815

5,100,000 2,000,000

Murphy

6.4 2.4

GC 549

1

800,085

15,000,000 6,900,000

Anadarko

18.7 8.6

AT 237

1

909,899

8,300,000 3,000,000

Equinor

9.1 3.3

WR 285

1

859,837

6,200,000 1,200,000

Chevron

7.2 1.4

WR 329

1

595,837

4,400,000 770,000

Chevron

5.7 1.3

MROV=Mean of the Range-of-Value ADV=Adjusted Delayed Value, which takes into account delaying bonuses and royalties

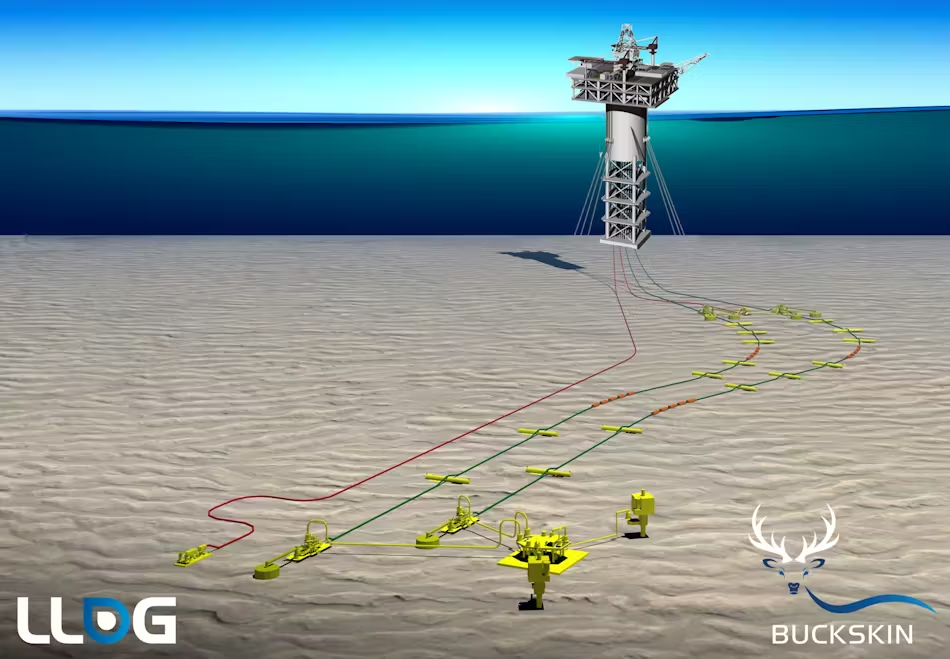

Houston, TX, March 29, 2024. Beacon Offshore Energy LLC (“Beacon”) announced today the completion of the divestment of its non-operated interests in certain fields in the deepwater Gulf of Mexico in accordance with a previously executed definitive agreement with GOM 1 Holdings Inc., an affiliate of O.G. Oil & Gas Limited. The divestment includes Beacon’s 18.7% interest in the Buckskin producing field, 17% interest in the Leon development, 16.15% interest in the Castile development, 0.5% interest in the Salamanca FPS/lateral infrastructure, and 32.83% interest in the Sicily discovery.

According to BOEM records, GOM 1 HOLDINGS INC, a Delaware company, registered with BOEM effective 3/15/2024. The parent entity, O.G. Oil & Gas Limited, is a privately held E&P company incorporated in 2017 and based in Singapore.

O.G. Oil & Gas Ltd is part of the Ofer Global Group, “a private portfolio of international businesses active in maritime shipping, real estate and hotels, technology, banking, energy and large public investments.”

After a partial takeover by O.G Oil & Gas Limited in 2018, New Zealand Oil and Gas is now 70% owned by the Ofer Global Group. Among other interests, NZ Oil and Gas produces from fields offshore Taranaki, NZ.

Because they are jointly and severally liable for safe operations and decommissioning, minority investors should take a strong interest in safety management and financial assurance. Investors should remember that partners are adversely affected by the mistakes of the operating company. Anadarko and Mitsubishi took a hit following the Macondo blowout. To what extent had they been monitoring bp’s risk and safety management programs for drilling operations?

… and you deniers are fully responsible. There’s a reason why Texas is the most affected state 😉

But fear not, we will line our shores with wind turbines, restrict offshore oil and gas leasing, and subsidize carbon disposal in the Gulf of Mexico. All of this “help” will have a negligible effect on the climate, which will continue to change as it always has and always will.

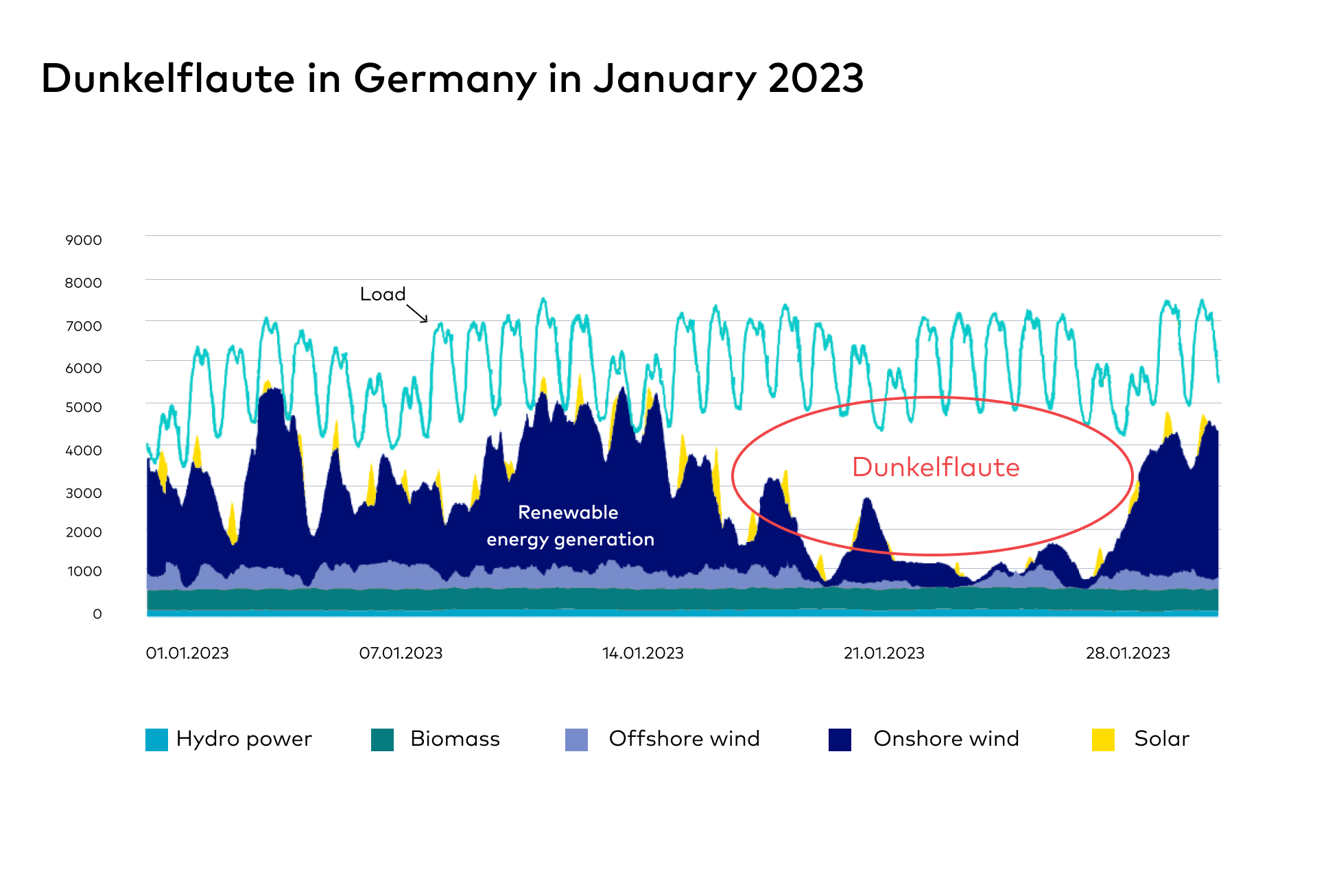

Add Dunkelflaute to the list of interesting and expressive compound German words. Die Dunkelflaute is a dark lull, a period of time in which minimal energy can be generated by the sun or wind. More specifically in German:

Die Dunkelflaute als sogenanntes Kofferwort beschreibt das gleichzeitige Auftreten von Dunkelheit und Windflaute. Diese Wetterlage entsteht typischerweise im Winter und sorgt für geringe Erträge aus Solar- und Windenergie bei gleichzeitig saisonal hohem Strombedarf. Eine Dunkelflaute kann mehrere Tage andauern. Kommen zu Dunkelheit und Windflaute noch niedrige Temperaturen hinzu, die für gewöhnlich den Strombedarf weiter ansteigen lassen, spricht man auch von “kalter Dunkelflaute.”

Note the prolonged Dunkelflaute (below) during which renewables provided minimal power in the middle of winter.

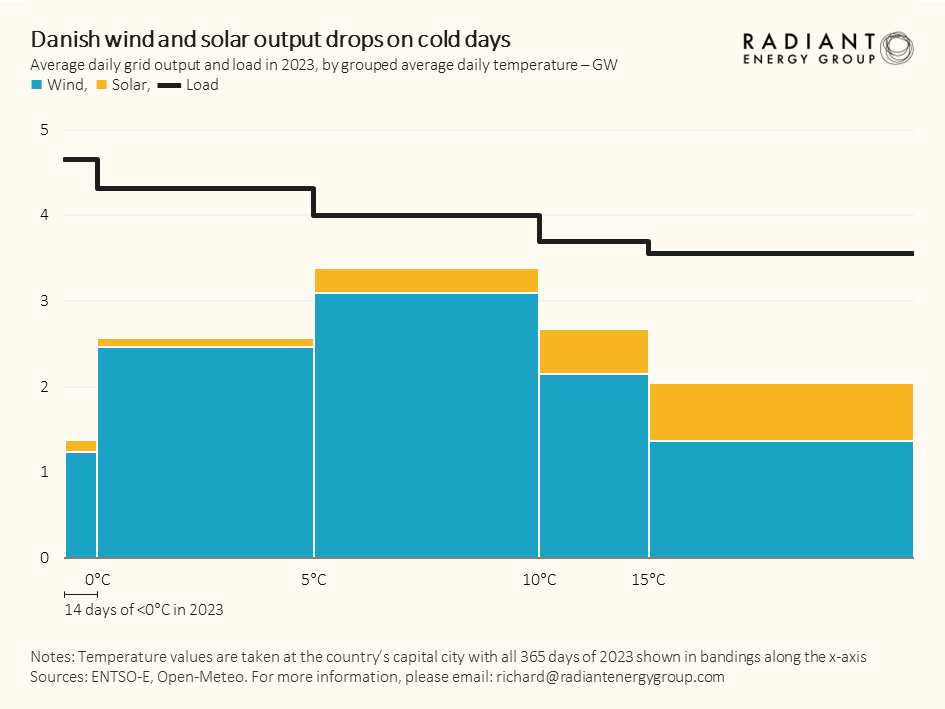

Unsurprisingly, wind and solar output are the lowest when the temperatures are the coldest. See the Danish summary for 2023 below. Note that wind output was also low when temperatures were above 15 deg. C.

Regional wind energy grids are not always an effective solution as Danish physicist Jens Christiansen, a nuclear energy advocate, has illustrated:

‘The wind always blows somewhere.’ Is that really true though? Here I’ve looked at the capacity factors of wind from five northern European countries in August The winds seem highly correlated, and there is almost a week-long period without significant wind anywhere.

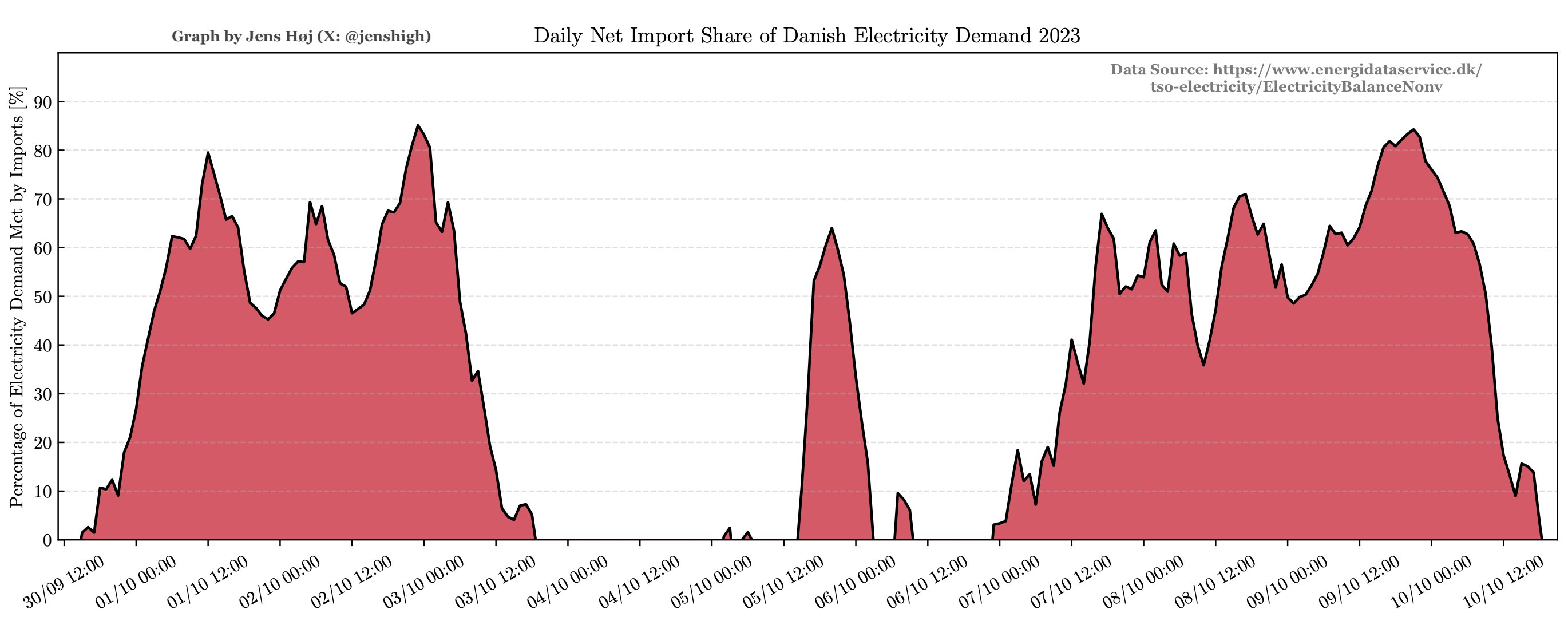

Christiansen illustrates Denmark’s reliance on imported electricity:

We need to talk about Denmark's enormous reliance on importing electricity!

A grid with a high penetration of wind and solar comes with a backside.

Often, for days at a time, imports account for more than 50% of the national electricity demand.

Paraphrasing Margaret Thatcher: “The problem with electricity imports is that you eventually run out of other people’s electricity.” In the U.S., California imports more electricity than any other state and typically receives between one-fifth and one-third of its electricity supply from outside of the state.

Given that massive battery storage is well beyond current capabilities and restrictions on electricity consumption and economic growth are undesirable, redundant or complementary power sources are essential for a reliable grid. Natural gas power generation is most responsive to variable demand, and is thus a good complement to variable sources like wind turbines and solar panels.

Citing rising oil prices, the DOE said, “We will not award the current solicitations for the Bayou Choctaw SPR site and will solicit available capacity as market conditions allow.” Three million barrels of oil had been slated for delivery to the Bayou Choctaw SPR site in August and September.

14 of the high bids at Gulf of Mexico Lease Sale 259 were rejected. Did those tracts receive bids at sale 261? What was the net gain or loss of revenue? See the summary bullets and table below

6 of the 14 tracts received no bids whatsoever

5 of the 14 tracts received higher bids that were accepted.

2 tracts received substantially higher bids that were again rejected

1 tract received a lower bid that was accepted

net bonus revenue gain to the govt from the bid rejections (pending re-offering at future sales): $1,032,877

net bonus revenue gain = 0.27% of the total high bids at sale 261

net loss in future rental and royalty payments: ????

For a net bonus revenue gain to date of only 1/4 of one per cent, 8 of the 14 sale 259 tracts with rejected high bids remain closed to exploration. The timing of any future sales is very much in doubt given the minimalist 5 year leasing plan and the associated legal challenges.

Current bid evaluation practices only make sense if regular lease sales are held on a predictable schedule, as has historically been the case.

I’m posting Sunday’s 60 Minutes segment that focused on deep sea mining and the failure of the US to ratify the UN Convention on the Law of the Sea (UNCLOS). Supplementary comments:

Most Federal employees involved with ocean energy policy, past and present, have supported US government ratification of UNCLOS.

The offshore industry has long supported UNCLOS. Industry trade associations, including API, IADC, and NOIA, are on the record as favoring ratification.

While concerns about UN management of deep sea mining access are understandable, some coordinated administrative structure is needed.

The Metals Company and other companies pursuing deep sea mining opportunities clearly disagree with the assertion that ocean floor mineral harvesting is not economically viable.

A new report ranks eight key energy industry sectors based on their ability to meet the growing demand for affordable, reliable, and clean electric power generation.

As governments around the nation attempt to impose a transition from traditional energy resources to energy sources open referred to as renewables, natural gas is the energy source that is best suited to integrate with the intermittency inherent in the use of wind and solar. Gas provides a reliable, affordable, and increasingly clean source of energy in both traditional and “carbon-constrained” applications.

Gas faces headwinds in the form of increasingly extreme net zero energy policies that will constrict supplies if implemented as proposed. Gas could also improve overall reliability if onsite storage was prioritized to help avoid supply disruptions that can occur in just-in-time pipeline deliveries during periods of extreme weather and demand.