April 2018:New Zealand is halting all new offshore oil and gas exploration to become a global leader in the fight against climate change, the centre-left government said Thursday, but opponents accused it of “economic vandalism”.

June 2024: The country’s coalition government is preparing to invite energy companies to resume exploration in the three major offshore fields that supply most of its gas. It comes after National Grid operator Transpower was last month forced to warn families to limit their electricity usage to avoid a shutdown during a cold snap.

Will the policy changes, the details of which remain to be announced, be sufficient to attract E&P investors?

…Rick Carrier became the first allied soldier to discover the Buchenwald concentration camp. The next day, April 11, 1945, he marched into the camp with Patton’s Third Army and liberated the prisoners.

More than a half century later, and after leading a successful effort to protect the American bald eagle, he was the first person to submit an offshore wind application to the Minerals Management Service.

Rick wanted nothing from the government except the opportunity to demonstrate his green hydrogen concept with a single turbine in the Atlantic. He did not ask for any subsidies or research grants. This war hero from the greatest generation just wanted to continue doing great things for the country and the world.

Unfortunately, the Energy Policy Act of 2005 had yet to be enacted, and the framework for permitting such projects had not been established. While we tried to find a way to make the project possible, the legal obstacles were too great.

It was an honor to have worked with Rick on his green hydrogen initiative. RIP.

CP’s acquisition of Marathon is an endorsement of shale production, most of which is from private lands. Sadly, these historically important OCS operators no longer have an interest in the Federal offshore sector.

Trinidad and Tobago (T&T), which has hadoil drilling operations since 1857, 2 years prior to the Drake well in Pennsylvania, closed another bidding round this week. In this Shallow Water Bidding Round, they received bids on 4 of the 13 blocks that were offered.

“These bid rounds are aimed at ensuring sustainable exploration and production and maximizing our country’s hydrocarbon resources. Following the successes of the 2021 Deep Water Competitive Bidding Round and the 2022 Onshore/Near Shore Competitive Bidding Round, this Shallow Water Competitive Bidding Round was the third in a series of bid rounds conducted by the Ministry of Energy and Energy Industries.”

Regular sales are even more important in the US given the small lease blocks and thus the need to have access to nearby resources for sustained production and efficient utilization of facilities.

Below are the blocks receiving bids in the T&T sale, and the size of those blocks. US lease blocks are approximately 23 sq km.

Sec. 12(a) of OCSLA (43 U.S. Code § 1341(a)): “The President of the United States may, from time to time, withdraw from disposition any of the unleased lands of the outer Continental Shelf.”

The language “from time to time” implies that withdrawing OCS lands from oil and gas leasing consideration is a casual exercise at the whim of the President for any particular reason. That is indeed how the provision has been implemented.

Alaska Presidential withdrawals are shaded (BOEM map)Atlantic and GoM withdrawals are shaded (BOEM map)

Over the last 8 years, Presidents Obama, Trump, and Biden have unilaterally exercised this authority without prior notice or opportunity for public comment. Their actions were timed to extend oil and gas leasing prohibitions well beyond their term in office (perhaps permanently), seek an edge in an upcoming election, or sacrifice OCS leasing in an attempt to placate opponents of another executive decision. More specifically:

In his last month in office, President Obama removed canyon areas of the Atlantic from leasing consideration “for a time period without specific expiration.”

In his last month in office, President Obama removed the Northern Aleutian planning area from leasing consideration “for a time period without specific expiration.”

Two months before the 2020 election, President Trump removed the South Atlantic planning area from leasing consideration through June 30, 2032.

Two months before the 2020 election, President Trump removed the Eastern Gulf of Mexico area from leasing consideration through June 30, 2032.

On March 13 2023, coincident with his approval of theWillow project (North Slope of Alaska), President Biden removed the remainder of the Beaufort Sea from leasing consideration “for a time period without specific expiration.”

In light of the rather cynical abuses of this authority and their potential economic and national security implications, Congress should consider repealing Sec. 12(a) of OCSLA or revising the language to limit the timing, scope, and duration of such withdrawals, and establish a process that prevents the withdraw of lands without fully considering the potential implications.

Florida HB 1645 (attached) was signed by Gov. DeSantis on 5/15/2024. The bill boosts natural gas, prohibits offshore wind turbines, and deletes references to climate change and greenhouse gases in state law. Given the State’s support for traditional energy sources, is it time to renew the dialogue about exploration and production in the Eastern Gulf of Mexico (EGOM)?

HB 1645 prohibits offshore and coastal wind development (p. 30), acknowledges that natural gas is critical for power resiliency, prohibits zoning regulations that restrict gas storage facilities and gas appliances (p.8), and relaxes permitting requirements for pipelines <100 miles long.

Given Florida’s energy preferences as expressed in this legislation, the State could assist regional energy planners by better defining its position on oil and gas leasing in the EGOM. What limits, in terms of lease numbers and minimum distances from shore, would best improve Florida’s energy supply options while further minimizing environmental risks?

As illustrated on the map below, the petroleum geology of the EGOM and Florida’s preferences are likely aligned in that the best prospects for oil and gas production are in deep water and more than 100 miles from the State’s coast.Does Florida support a 100 mile buffer?

The 4/20/2010 Macondo blowout was a tragic failure that has been, and will continue to be, discussed at length on this blog. We should also acknowledge that prior to Macondo 25,000 wells were drilled on the US OCS over a 25 year period without a single well control fatality, an offshore safety record that was unprecedented in the U.S. and internationally. We should also applaud recent advances in well integrity and control, including the addition of capping stack capabilities that further reduce the risk of a sustained well blowout.

Florida’s independent thinking on energy policy is commendable. That independence is contingent on importing petroleum products and natural gas from elsewhere in the Gulf region. Securing that supply over the intermediate and longer term should be a priority for Florida. In that regard, EGOM production is an important consideration.

BOEM’s “Rule to Streamline and Modernize Offshore Renewable Energy Development” is intended to “make offshore renewable energy development more efficient, [and] save billions of dollars. Unfortunately, the savings associated with relaxed decommissioning financial assurance requirements translates to increased risk for customers and taxpayers.

BOEM signaled their intentions on offshore wind (OSW) decommissioning three years ago when they granted a precedent setting financial assurance waiver to Vineyard Wind. Despite compelling concerns raised by commenters, the “streamlining” regulations have codified this decision.

Cape May County, New Jersey, was among the commenters objecting to BOEM’s departure from the prudent “pay as you build” financial assurance requirement. The County commented as follows (full comment letter attached):

“[e]nergy-utility projects are in essence traditional public-private partnerships where technical and financial risks are transferred to the private sector in exchange for the opportunity to generate revenues and profit. Under the proposed rule, the Federal government is instead transferring risks associated with decommissioning to the consumer rather than to the private sector.”

Cape May added:

“[w]hile BOEM believes that if a developer becomes insolvent during commercial activity that a solvent entity would assume or purchase control, the County believes this is a risky assumption as the most likely reason for default is that a constructed wind farm developer is unable to meet its contractual obligations set forth under a Power Purchase Agreement (PPA) because its energy production revenues are not in excess of its operating costs. A change of hands would not remove these circumstances or make the project profitable.”

Cape May and others also commented on the threat of premature decommissioning as a result of storm damage. In response, BOEM asserts that these risks have been addressed in the latest standard for North American offshore wind turbines (Offshore Compliance Recommended Practices: 2022 Edition (OCRP-1-2022)). However, design standards, particularly those for offshore facilities, are not static. The recommended practice for OSW is likely to change multiple times in the coming years as storm, operating, and turbine performance data are updated and analyzed. The design standard for Gulf of Mexico platforms has been repeatedly refined and improved and is now in its 22nd edition.

In their response to public comments on the decommissioning risks, BOEM repeatedly asserts that they can adjust the amount and timing of required financial assurance as they monitor a lessee’s financial health. Unfortunately, a company’s finances can change quickly and BOEM’s options will be limited when it does. Increasing the financial burden on a struggling company that is providing power to a regional power grid will not be a simple proposition.

“Exxon Mobil has led a persistent and apparently successful lobbying campaign behind the scenes to push the US federal government to adopt rules that would allow the conversion of existing oil and gas leases in the Gulf of Mexico into offshore carbon capture and storage (CCS) acreage, according to documents seen by Energy Intelligence and numerous interviews with industry players.”Energy Intelligence

The Energy Intelligence article documents the ongoing carbon disposal lobbying by Exxon and others. Those meetings are okay prior to publishing a Notice of Proposed Rulemaking (NPRM) for public comment. However, the article implies that the next step is a final rule: “Whether or not Exxon succeeds will become fully clear when the US issues final rules guiding CCS leasing, expected sometime this year.”

A final rule this year is unlikely, because an NPRM has to be published first for public comment. The only exception would be if BOEM was able to establish “good cause” criteria for a direct final or interim final rule in accordance with the Administrative Procedures Act. Such an attempt at corner cutting seems unlikely, especially in an election year when all regulatory actions are subject to additional scrutiny.

Exxon must have thought they had a clear path forward after 11th hour additions to the “Infrastructure Bill” authorized carbon disposal on the OCS, exempted such disposal from the Ocean Dumping Act, and provided $billions for CCS projects. Keep in mind that the Infrastructure Bill was signed just two days before OCS Oil and Gas Lease Sale 257, at which Exxon acquired 94 leases for carbon disposal purposes.

What the Infrastructure Bill did not provide is authority to acquire carbon disposal leases at an oil and gas lease sale. Now the lobbyists are apparently scrambling to overcome that obstacle administratively.

A single company or small group of companies should not be dictating the path forward for the Gulf of Mexico. Super-major Exxon is a relative minnow in the Gulf of Mexico OCS. They have not drilled an exploratory well since 2018, not drilled a development well since 2019, operate only one platform (Hoover, installed in 2000), ranked 11th in 2023 oil production, and ranked 29th in 2023 gas production.

Lastly, and most importantly, public comment on the myriad of technical, financial, and policy issues associated with GoM carbon disposal is imperative. That input is essential before final regulations are promulgated.

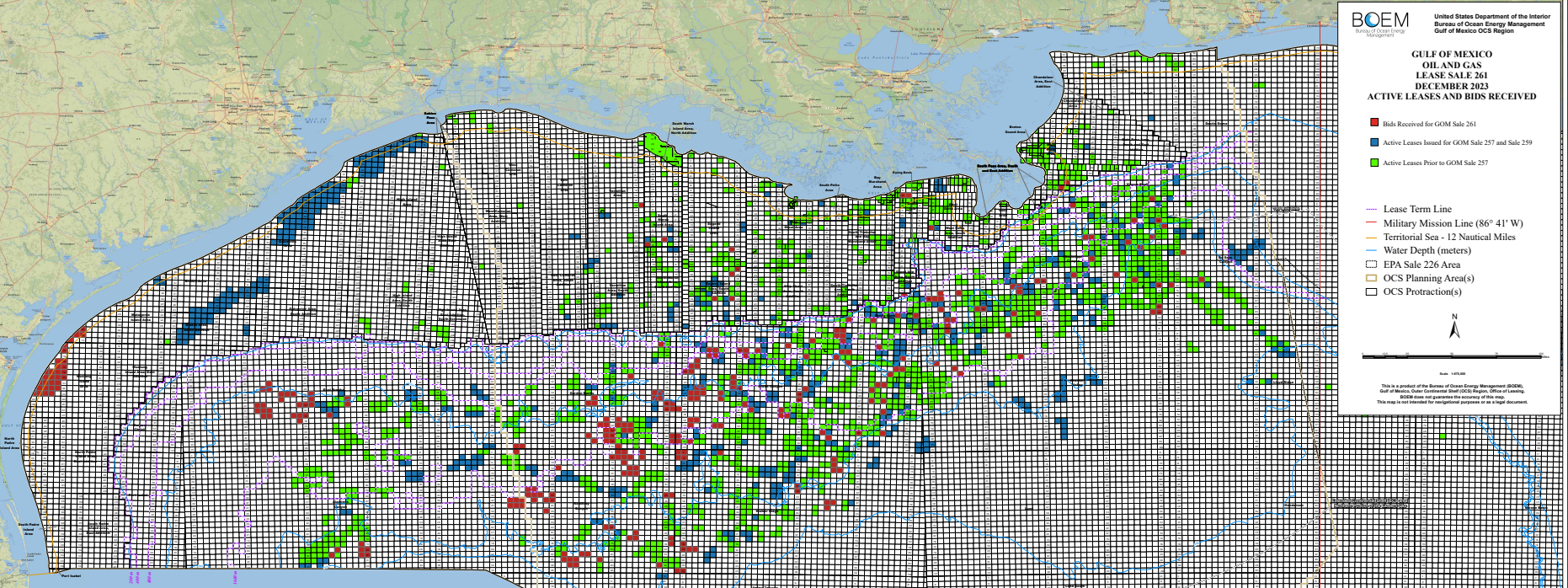

At Sale 261, Repsol was the sole bidder for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 and 259.

“Deepwater is back in vogue.” (Pablo Medina, Welligence)

“Newer deepwater projects have the attributes oil and gas companies are looking for: longer-term production, lower breakeven costs, big resource potentials and lower carbon emissions.” (Medina)

Capital spending on all-new deepwater drilling is poised to hit a 12-year high next year (Rystad)

Investment in all-new and existing deepwater fields could hit $130.7 billion in 2027, a 30% jump over 2023 (Rystad)

Deepwater resources offer lower carbon emissions intensity than shale and other tight oils, averaging 2kg of carbon dioxide per barrel less than shale. (Rystad)

“The return of offshore and deepwater operations is going to be a big topic at OTC, and Namibia is going to be talk of the show.” (James West, Evercore)

Enthusiasm for offshore has climbed with discoveries and technology breakthroughs. Namibia’s Mopane is forecast to hold as much as 10 billion barrels of oil. (Portuguese oil company Galp Energia)

Rates for some rigs have surpassed $500,000 a day and contract durations are lengthening as supply dwindles.

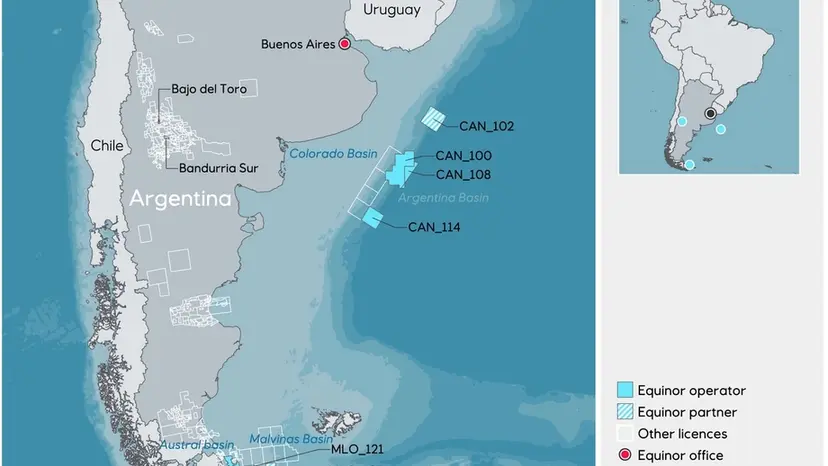

The Valaris DS-17 drillship is now on location to drill the Algerich-1 well for Equinor 315 km from Mar del Plata in 1527 m of water at Block CAN 100.

Concurrently, at the opposite end of the Pan American continents, the Stena DrillMAX is closing in on Exxon’s Orphan Basin location offshore Newfoundland to drill another high potential well.