Exploration and development have improved dramatically over the past 100 years, and have become much more efficient. Only 57 platforms are producing about 1.7 million barrels/day in the deepwater Gulf of Mexico. Still work to do and continuous improvement must always be the objective.

Perdido Platform, Gulf of Mexico, 7835′ water depth, 320km south of Freeport, Texas

The data in the paper appear to be reasonably accurate. However, there is one glaring error regarding Pacific operations, and the reference to the Macondo blowout in the environmental discussion is rather provocative and misleading.

Per the authors:

California wells are drilled in relatively shallow water—mostly less than 100 feet—while GoM wells can be in up to 10,000 feet of water.

With regard to the environmental risks, the Nature Energy paper’s reference to the Macondo blowout, while muted, is what some media outlets embraced. Per the authors:

Releases from improperly abandoned wells will probably be chronic and small compared with Macondo, but the underlying biochemical and ecological processes that influence the ecological impacts have many similarities.

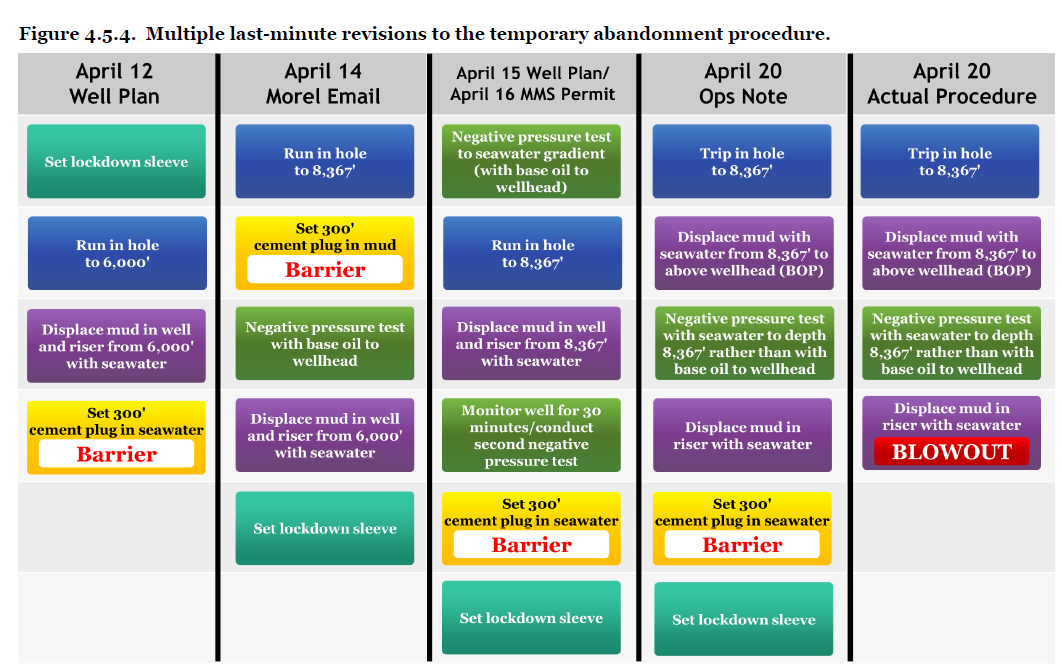

The Macondo well blew out while it was being suspended in preparation for subsequent completion operations. Ill advised changes to the well suspension plan were among the primary contributing factors to the blowout (see diagram below). The Macondo well was entirely different from the depleted end-of-life wells that are the subject of the paper.

Some media outlets ran with the Macondo angle, weak as it was. This ABC news piece featured numerous Macondo pictures. Other outlets noted that Macondo was a temporarily abandoned well, which it was not. The Macondo well never got to that point.

National Commission, Chief Counsel’s Report, p. 132

“BSEE will continue to evaluate the process for issuing decommissioning orders and will continue to issue decommissioning orders to jointly and severally liable parties on a case-by-case basis.“

Although the news release for BSEE’s final decommissioning rule asserts that the regulations “provide the certainty requested by industry,” that does not seem to be the case. The main change in the final rule was to delete the reverse chronological order (RCO) provision which called for issuing decommissioning orders to the most recent predecessor first. Instead, BSEE may continue to issue decommissioning orders arbitrarily.

While deleting the RCO provision may be advantageous for the regulator, and in some cases for the public, claiming that the decision provides certainty for industry is quite a stretch. BSEE may continue to issue a decommissioning order to anyone in the ownership chain, whether the company was a recent lessee or one that had owned the lease decades ago. Original or early lessees may be held liable for decommissioning old facilities regardless of subsequent damage, modifications, or neglected maintenance.

The absence of a defined procedure for issuing decommissioning orders may also expose BSEE to new legal challenges, particularly in cases where a company has not held the lease for decades. A 1988 letter from the Director of the Minerals Management Service to Amoco (attached below) explicitly relieves the assignor (predecessor) of decommissioning liability after the lease has been assigned. A revised bonding rule published on May 22, 1997 reversed that policy, but decommissioning liability for leases assigned prior to the 1997 rule may still be very much in question.

Another concern is the split jurisdiction for decommissioning between BSEE and BOEM. The financial, land management, operational, and environmental aspects of decommissioning are inextricably intertwined and attempts to divide these responsibilities between two bureaus with separate regulations is a prescription for gaps, overlap, inconsistency, inefficiency, disputes, and confusion. Decommissioning should be regulated holistically, not with separate “BOEM-only” and “BSEE-only” regulations.

Finally, wind facility decommissioning may prove to be even more challenging given the higher facility density and economic uncertainties. The regulatory regime needs to be clearly established early in the development phase.

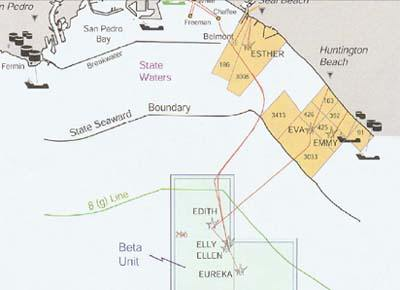

HOUSTON, April 10, 2023 (GLOBE NEWSWIRE) — Amplify Energy Corp. (“Amplify” or the “Company”) (NYSE: AMPY) today announced that it has received the required approvals from federal regulatory agencies to restart operations at the Beta Field. Initial steps to resume full operations will involve filling the San Pedro Bay Pipeline with production, a process which commenced over the past weekend and is expected to take approximately two weeks to complete. Following the line fill process, the pipeline will be operated in accordance with the restart procedures that were reviewed and approved by the Pipeline and Hazardous Materials Safety Administration (PHMSA).

Odd that the news release didn’t mention BSEE, the agency which would have had to approve the resumption of production.

18 months after the pipeline spill near Huntington Beach, settlements have been reached, fines have been paid, and production from the Beta Unit has resumed, but the Federal investigation report is still unavailable. Why?

One would hope that this spill will lead to an independent review of the regulatory regime for offshore pipelines. Consideration should be given to designating a single regulator that is responsible and accountable for offshore pipeline safety (a joint authority approach might also merit consideration) and developing a single set of clear and consistent regulations.

This reminded me of an important Lawrence Livermore project that was funded by the Minerals Management Service in 1995. The study considered seismic hazard criteria for offshore platforms on the California OCS. My colleague Dr. Charles Smith, a structural engineer, had an important role in this research. Charles had been instrumental in the establishment of an earthquake measurement network in the Pacific Region. The measurement system at Platform Grace in the Santa Barbara Channel successfully recorded 5 earthquakes and the structural responses at multiple locations on the platform.

Lawrence Livermore and the other national laboratories have many outstanding scientists and engineers. The national labs do excellent work, although their studies are a bit pricey 😉

A group of international shipping companies and their subsidiaries tentatively agreed Wednesday to pay $96.5 million to Houston-based Amplify Energy Corp. to dismiss one of the last remaining lawsuits over the oil spill, which sent at least 25,000 gallons of crude into the waters off Huntington Beach in October 2021.

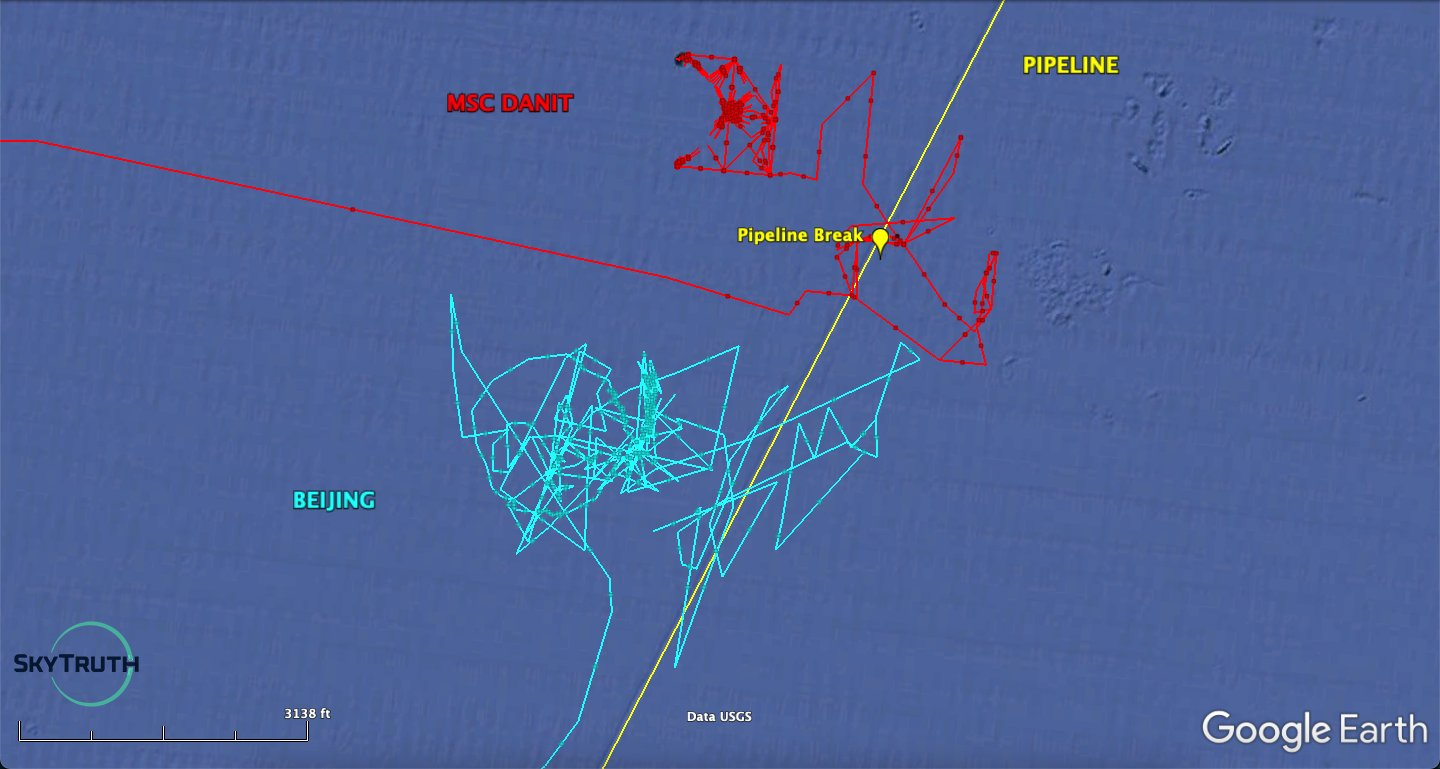

Per the LA Times, companies linked to the cargo ships accused of dragging anchors over Amplify Energy’s pipeline have agreed to pay $45 million to settle lawsuits. The ships were identified by Sky Truth (see above image) shortly after the spill (October 1, 2021).

Meanwhile, Amplify is suing the vessel owners for damaging the pipeline and failing to notify the authorities after the damage occurred. Amplify would seem to have a good case given that inspection reports indicate that the pipeline was in good shape prior to the anchor damage and that the Beta Unit platforms had a good safety and compliance record.

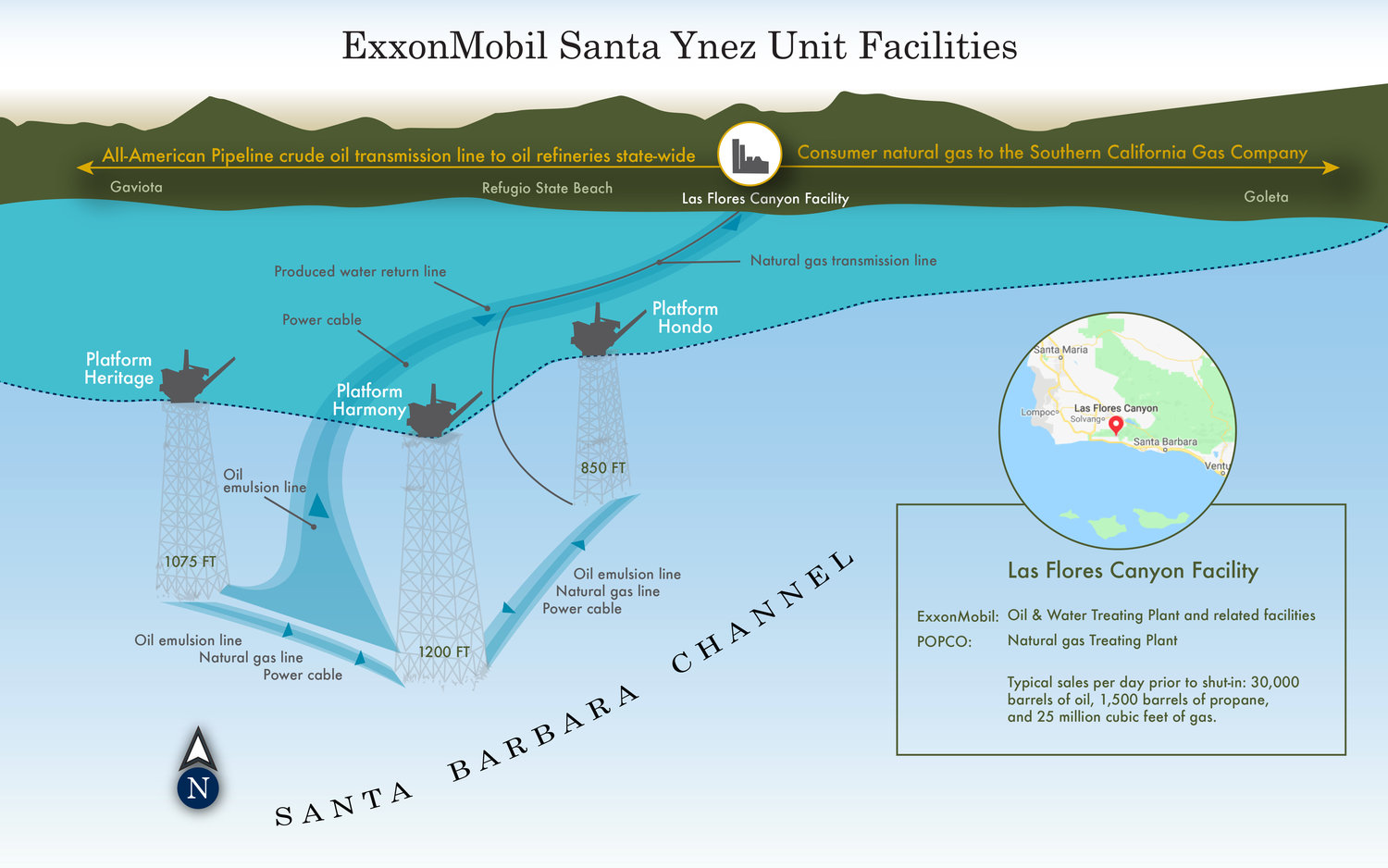

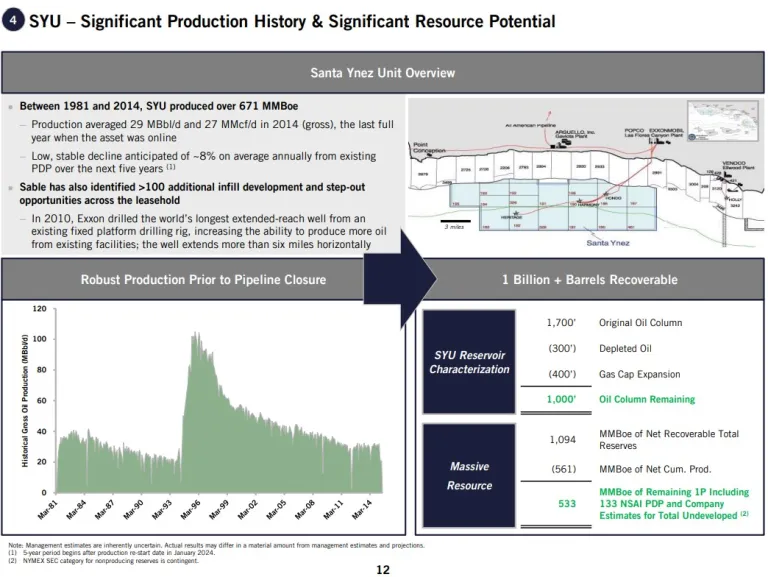

When Exxon was unable to get approval for an onshore oil processing facility, the company installed this offshore storage and treatment (OS&T) vessel and single anchor leg mooring (SALM) 3.5 miles from shore, just seaward of the State-Federal boundary. The OS&T, a converted tanker, operated from 1981 to 1994. By 1994, the onshore gas processing facility in Las Flores Canyon had been expanded to process Santa Ynez crude, eliminating the need for the OS&T. While the OS&T had a very good performance record, the highly visible vessel was less than endearing to most Santa Barbara County residents, and there was no apparent sadness when the OS&T and SALM were decommissioned in 1995.

With this deal, Exxon is essentially lending Flame, Sable’s management team and PIPE investors the money to buy the facilities from itself. If they are able to get them back online, great, Exxon gets its $623 million loan paid back with 10% interest. If not, it presumably repossesses the facilities and their associated headaches.