Good article from our friends at the Petroleum Safety Authority of Norway. When old guys reminisce, people need to listen 😉

“Reagan feared that the world, and especially Europe, would become too dependent on Soviet gas, and saw Troll as an opportunity to create greater independence.”

“Lerøen sees parallels to the current situation, with Russia’s invasion of Ukraine, and the importance Norwegian gas has for the EU, which wants to become independent of Russian gas.”

The only current Alaskan OCS production is from Northstar, a joint State-Federal Unit in the Beaufort Sea. The production island is in State waters, but 7 of the wells produce from the Federal sector. The field was originally developed by bp, but Hilcorp is the current operator. To date, BSEE has conducted 5 inspections of the facility in 2022, and no incidents of noncompliance (INCs) were identified.

Per BOEM records, 4 companies operate Pacific (California) OCS facilities that are currently producing. Three of those operators have superior 2022 inspection records. No INCs were issued to either Exxon (11 Santa Ynez Unit inspections) or Freeport-McMoRan (24 Platform Irene inspections). Only 2 warning INCs were issued during 12 inspections of Beta Operating Co. platforms Ellen, Elly, and Eureka in the Beta Unit offshore Long Beach.

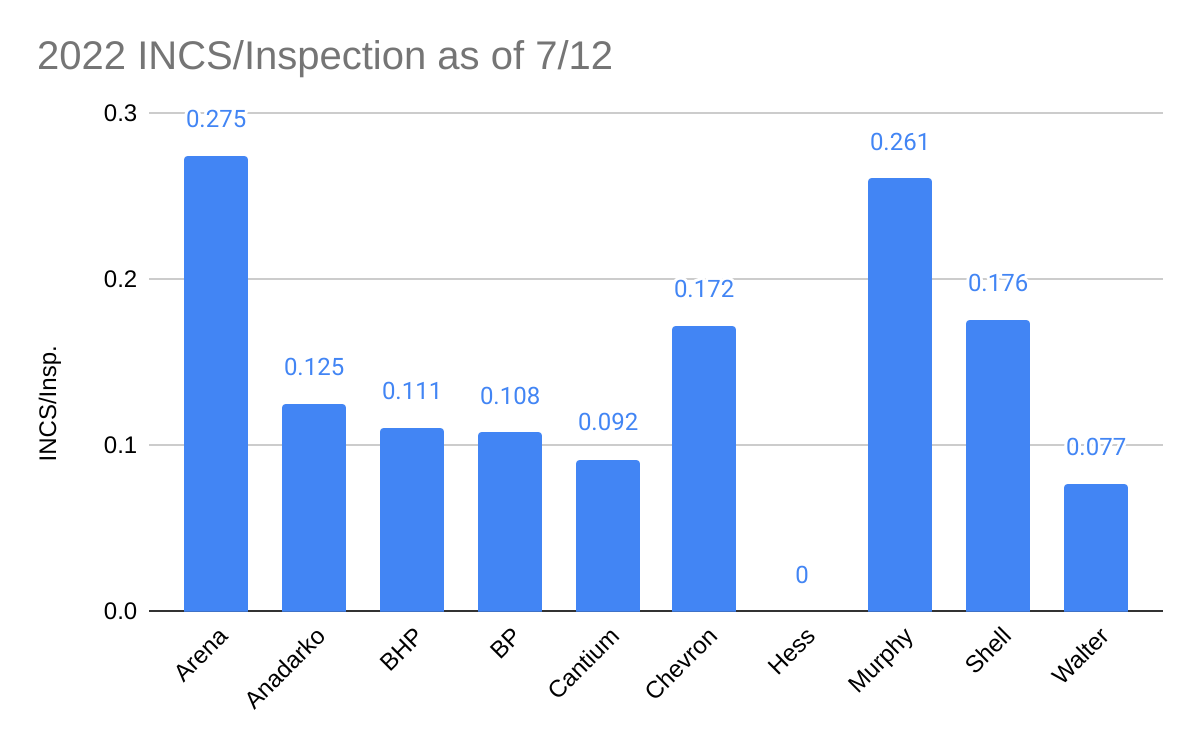

Operating companies (listed alphabetically): Arena, Anadarko (Oxy), BHP, bp, Cantium, Chevron, Hess, Murphy, Shell, and Walter

Criteria:

Must average <0.3 incidents of compliance (INCs) per inspection. (This is less than half the GoM 2022 YTD average of 0.64 INCs/inspection.)

Must operate at least 3 production platforms.

Must have drilled at least one well.

Pacific and Alaska operations will be considered in a separate post.

Comments:

Impressive performance by Hess: 21 inspections and no INCs

Cantium and Walter averaged less than 0.1 INCs/inspection. The INC rates for Anadarko (Oxy), BHP, and BP were only slightly higher.

Among the Honor Roll companies, Shell (highest production, 9 deepwater platforms, and 13 well starts) and Arena (115 shelf platforms and 12 well starts) were the deepwater and shelf activity leaders.They thus had the highest INC exposure.

Although CSI and FSI INCs are typically more significant than W INCs, that is not always the case, so the INCs have not been weighted by type.

As has been previously noted, more inspection data should be readily available online. At a minimum, the specific INC (type) numbers (e.g. P-103, G-110, etc) should be posted so the public can better assess performance. Absent this information, interested parties are left to speculate about the significance of the violations.

While compliance is not synonymous with safety, most experienced observers believe there is a strong correlation. In the 1990’s, John Shultz, a PhD candidate at Carnegie Mellon Univ., studied US offshore facilities and safety data and developed expert and regression models to predict the likelihood of accidents and spills. That was a data rich era in that there were ~4000 US offshore platforms (more than twice the current number) and ~100 well starts/month (>10 times the current rate). In John’s thesis, he found that INCs are a very good predictor of accidents and spills. The offshore world has changed and further study of the correlation between compliance and safety performance is highly recommended.

Chevron may be the only GoM operator to own its helicopter fleet. Data on their safety performance relative to GoM helicopter contractors do not appear to be available online.

Their news release focuses on hurricane preparedness and the benefits of owning their fleet. I’m not sure how significant these advantages are given that other companies can ensure similar availability through their contracts. A comparative analysis would be of interest.

“Other companies that depend on contracted helicopters to evacuate can’t create their own schedule and might have to start departing the platform days in advance,” said Jose Jaramillo, manager of Chevron’s aircraft operations in the Gulf of Mexico. “With our own helicopters on standby, we have more flexibility in determining when to safely shut down the platform, and after the storm passes, we can quickly remobilize, assess our facilities and bring production back online days faster.”

The leading causes, not all inclusive, of the accidents since 1999 are listed below, and secondary causes of these events include 13 related to helideck size or design related issues. • 21 engine related, • 25 loss of control or improper procedures, • 18 helideck obstacle strikes, • 13 controlled flight into terrain, and • 12 other technical failures

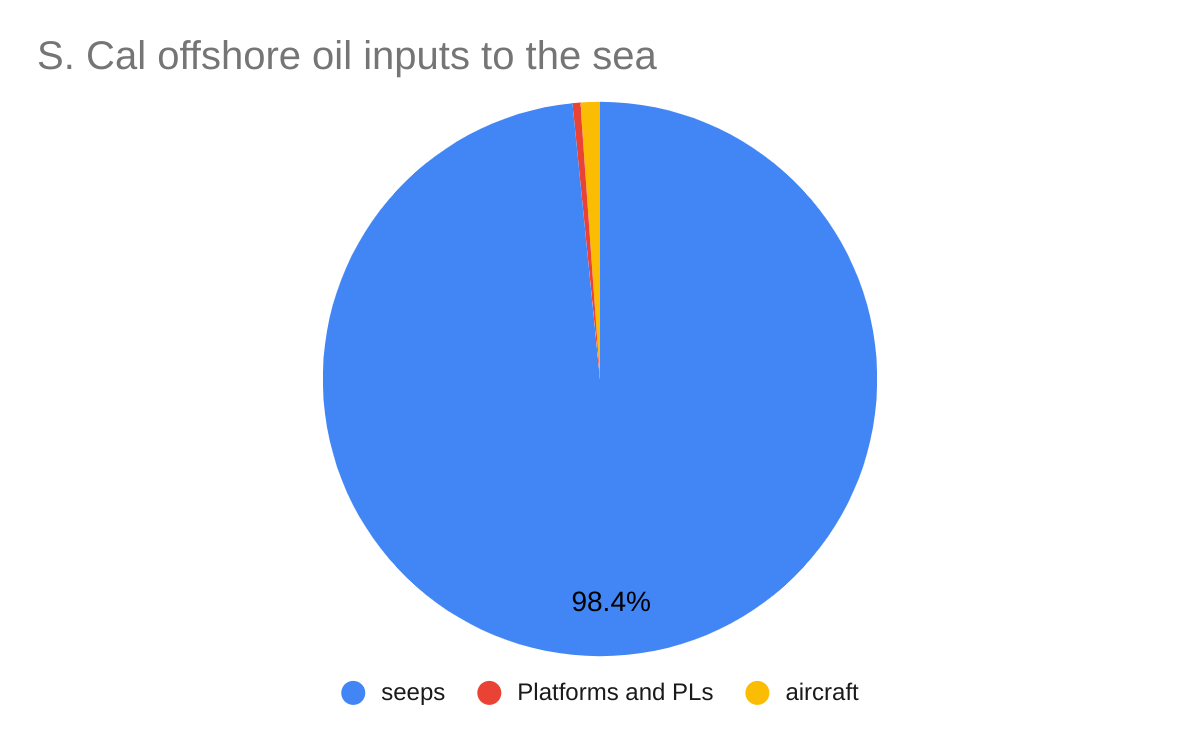

One of our very savvy BOE readers shared data (attached) from Oil in the Sea III, a National Academies report that is the best source of information on oil inputs into US waters. The data for Southern California are presented below in 3 charts. The first chart shows that natural seeps are overwhelmingly the leading offshore source of oil entering SoCal waters, with offshore platforms and pipelines accounting for <0.5% of the oil.

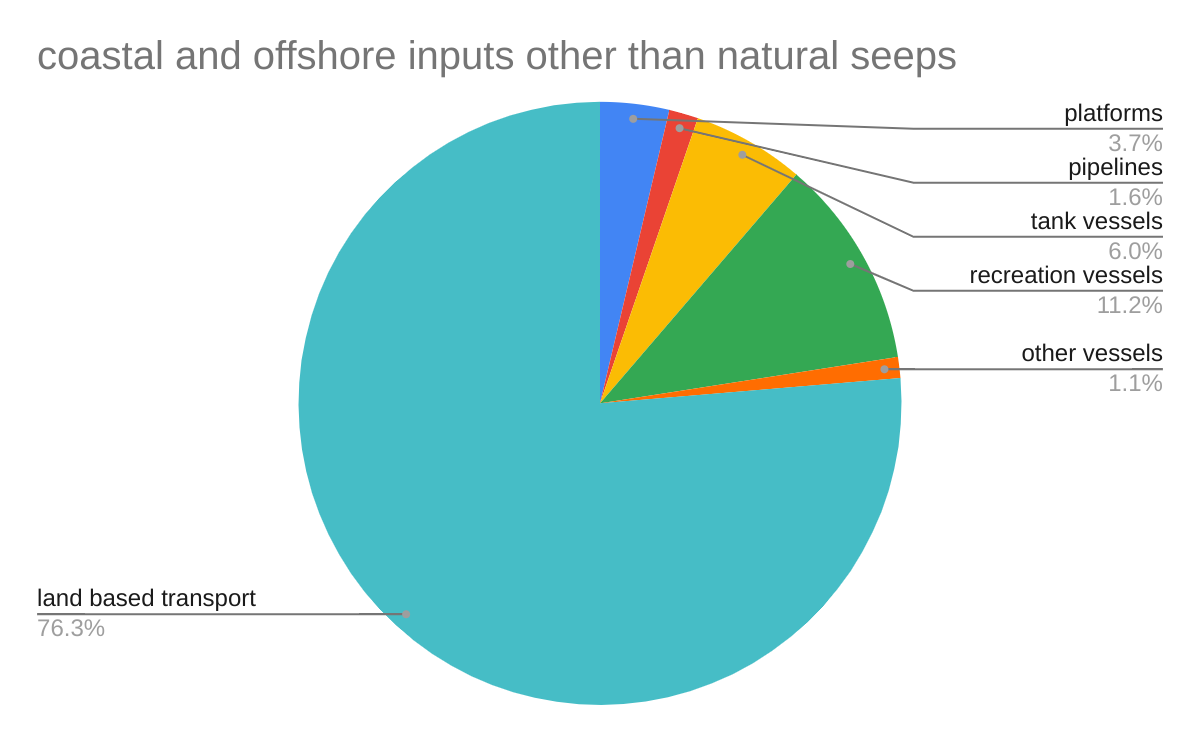

The second and third charts exclude natural seepage and compare the coastal and offshore oil inputs from the other sources. When land based transportation inputs are included (chart 2), platforms and pipelines (combined) account for 5.3% of the oil.

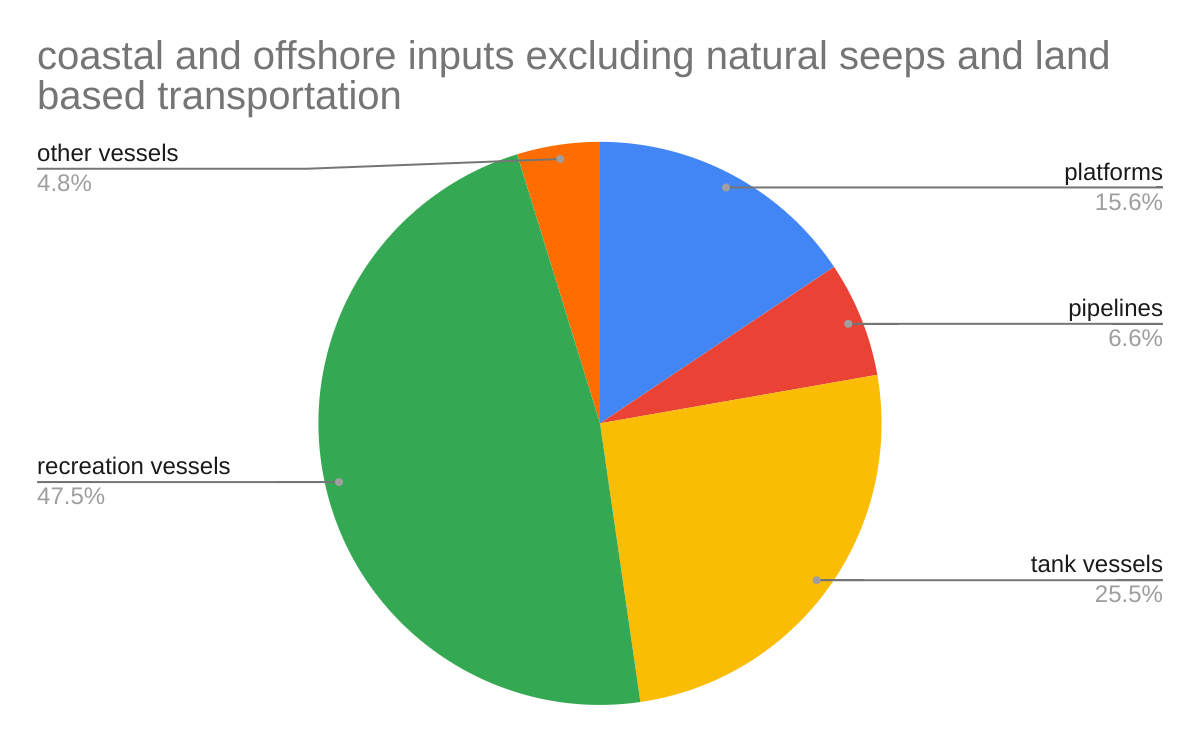

Excluding natural seepage and land based transportation inputs (chart 3), recreation vessels are by far the leading source of oil (47.5%), with platforms and pipelines (combined) accounting for less than half that volume (22.2%).

These data add important perspective, but are not intended to discount platform and pipeline spills. These spills can have significant localized impacts, and every effort must be made to prevent their occurrence.

This blog does not normally cover onshore leasing; pontificating about offshore issues is challenging enough😉. However, Randall Luthi – the former head of the MMS (and thus the US offshore program) – is now dealing with similar issues to those being experienced in the offshore sector.

“The bad news is the sale was 18 months late, was approximately 75% smaller than originally planned, had a huge number of state director deferrals, and offered many less-than-desirable leases,” testified Randall Luthi, who serves as chief energy advisor to Gov. Mark Gordon. “In summary, it was a long-awaited, but paltry sale.”

According to Luthi, the federal government controls approximately 67% of Wyoming’s mineral estate, and nearly 50% of its surface.

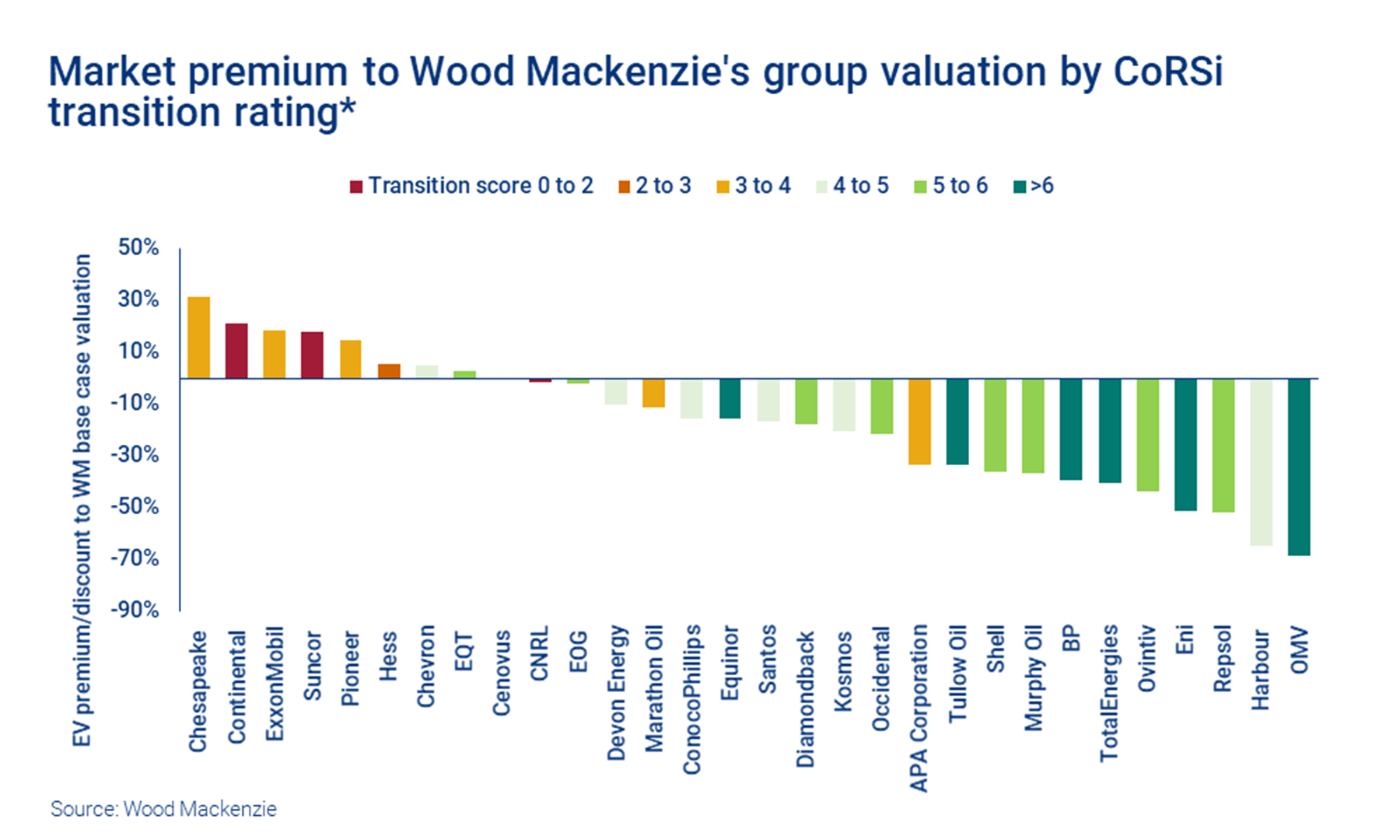

Per Wood Mackenzie, companies with low transition scores (i.e. the purer oil and gas plays) command higher valuations. I’d like to see the scores for other US independents.

“First, investors piled into the pure play oil and gas producers that are most leveraged to oil prices, much as they would in any upcycle. US independents led the sector rise through early June before the oil price and shares fell back over the last month.“

“Euro Majors are also reaping the earnings and cash flow boom. Share price performance has been strong relative to the wider stock market, but most have lagged their US peers. US Majors have long commanded a premium rating to their European counterparts, partly a function of the relatively high rating of the US stock market. The gap though has widened.”

Given the differences in our views on energy policy, particularly with regard to oil and gas, this WP opinion piece is pretty reasonable. The Post acknowledges the continued need for oil and gas, and the importance of domestic production. That said, two statements in the paragraph pasted below warrant immediate comment.

“In reality, neither argument is convincing. The Biden administration’s proposal — which opens the door to up to 11 potential lease sales, 10 in the Gulf of Mexico and one off the coast of Alaska — would have little impact on current energy prices. It would take between five and 10 years to produce oil after a new offshore lease issuance, according to the Interior Department, while more than three-quarters of already-leased offshore federal waters are not in production.”

The purpose of the 5 year leasing plan is to minimize future energy supply and security risks, not to reduce current prices. However, acknowledgement of the importance of offshore production and support for regular lease sales could influence market psychology.

The old and tired arguments about non-producing leases have been frequently addressed on this blog. When you purchase leases, you are not buying oil and gas. You are buying only the opportunity, for a limited period of time, to explore for these commodities. The current percentage of producing leases is actually rather high by historical standards. For more on this topic, see this and this.