Decommissioning specialist John Smith has summarized the major provisions of BOEM’s decommissioning financial assurance rule for OCS oil and gas operations. He has highlighted his comments in red.

Proved reserves should not be a basis for reducing supplemental assurance. The uncertainty associated with reserve estimates and decommissioning costs can easily negate the assumed buffer in BOEM’s 3 to 1 reserves to decommissioning costs ratio. That approach failed completely at the Carpinteria Field in the Santa Barbara Channel (Platforms Hogan and Houchin). See other points on this issue.

Given that the reverse chronological order process for determining predecessor liability was dropped from consideration last April, there is no defined procedure for issuing decommissioning orders to prior owners. The absence of such a procedure increases the likelihood of confusion, inequity, and challenges, particularly when orders are first issued to companies that owned the leases decades ago, in some cases prior to the establishment of transferor liability in the 1997 MMS “bonding rule.”

BOEM’s concern (below) about investment in US offshore exploration and production is interesting given that their 5 year leasing plan strongly implies otherwise.

BOEM’s goal for its financial assurance program continues to be the protection of the American taxpayers from exposure to financial loss associated with OCS development, while ensuring that the financial assurance program does not detrimentally affect offshore investment or position American offshore exploration and production at a competitive disadvantage

I’m just guessing here, but my sense is that BOEM was pressured to finalize this rule in a timely manner (<10 months is timely for such a complex rule) and was thus reluctant to make any significant changes to the proposal published last summer. A public workshop during the comment period would have been a good idea to facilitate informed discussion on the important issues addressed in this rule. Such workshops were once commonplace for major rules.

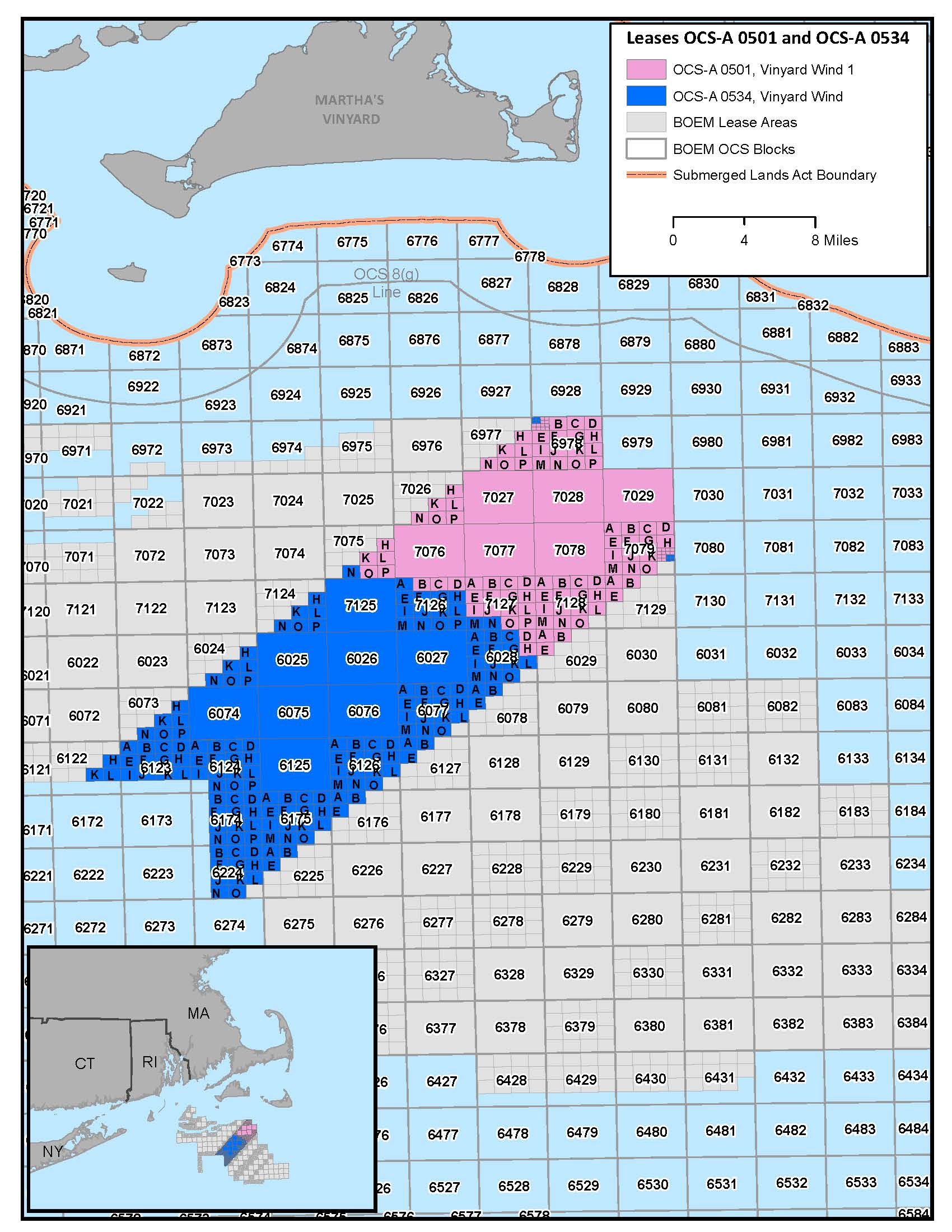

Recent disclosures indicate that BOEM, which very publicly promotes the offshore wind projects that it regulates, has waived a fundamental financial assurance requirement at the request of Vineyard Wind (approval letter attached). Given its broad applicability, this precedential waiver could have the effect of revising a significant provision of the offshore wind decommissioning regulations without public review and comment.

The issue is the “pay as you build” financial assurance requirement at 30 CFR § 585.516, which was waived by BOEM. This requirement, which is intended to project the public from decommissioning liability, is fair and reasonable given that wind developers must only provide financial assurance “in accordance with the number of facilities installed or being installed.” Companies that don’t have sufficient financial strength to comply with this requirement should not be installing and operating offshore wind turbines.

Vineyard Wind was either unable or unwilling to comply with the requirement. They instead requested to defer providing the full amount of the required financial assurance until year 15 of actual operations. The waiver changes “provide assurance when you install” to provide assurance 15 years after installation if everything goes as planned (hoped?).

After their waiver request was denied in 2017, Vineyard Wind resubmitted the request in 2021 seeking a favorable decision from an administration concerned that project cancellation or delay might tarnish the program that they were enthusiastically promoting.

BOEM (as directed from above?) granted the waiver, citing the general departure authority at 30 CFR § 585.103. However, that authority is intended for special situations, not for broadly applicable waivers that have the effect of revising the regulations without the public review required by the Administrative Procedures Act and Executive Orders 12866 and 13563.

There are no criteria in the Vineyard Wind waiver approval that could not apply to other wind developers. Vineyard Wind has simply committed to the same “risk-reduction factors” that apply to all offshore wind projects: damage insurance, the “use of proven turbine technology,” and long-term power purchase agreements. How could BOEM deny the same request from other companies?

It’s noteworthy that the regulations specific to financial assurance at 30 CFR § 585.516 provide no criteria for waiving the assurance requirements; nor do the regulations provide for the 15-year payment plan approved by BOEM. Given the precedential nature of the BOEM action and its enormous financial implications, a revision to the decommissioning regulations that provides criteria for such payment schemes should be promulgating before any similar departures are approved.

In light of the waiver, the public will likely incur substantial costs if Vineyard Wind fails, walks away, doesn’t fully fund their decommissioning account in a timely manner, or seeks new concessions after some or all of the 62 turbines have been installed.

Given the decommissioning obligations, what company would want to step in and assume responsibility for a failing project 10-15 years from now? What happens if Vineyard Wind’s project revenues don’t meet expectations and contributions to their decommissioning account are insufficient or used improperly? More concessions? We’ve seen this dance before.

Whether the project is for oil, gas, or wind energy, protecting the public from decommissioning liabilities should always be prioritized over facilitating development.

The Bureau of Ocean Energy Management (BOEM) is extending the public comment period on our notice of proposed rulemaking (NPRM), “Risk Management and Financial Assurance for Outer Continental Shelf Lease and Grant Obligations,” by 10 days.

The attached comments were submitted to BOEM via Regulations.gov. The comments address specific provisions of the proposed rule and include a recommendation to hold companies fully accountable for their lease transfers, but not for subsequent transfers in which they are not a party.

Do I get a t-shirt for being one of the first 2000 entries? 😀

In a draft rule published on June 29, 2023, BOEM proposes to discontinue using a company’s record of compliance in determining the need for supplemental financial assurance for decommissioning. BOEM’s full explanation for this surprising change is pasted at the end of this post.

Opposing view:

BOEM should be more attentive, not less, to safety performance and compliance data. If they were, taxpayers would have been better protected from the risks associated with the lease acquisitions by Fieldwood, Cox, Black Elk, Signal Hill, and others, and their subsequent bankruptcies.

Safe operations, as reflected in compliance and performance data, are critical to a company’s financial success.

BOEM wrongly infers that Incidents of Noncompliance (INCs) are solely dependent on the number and complexity of facilities. Decades of normalized compliance data have told us that there are marked differences among operators in terms of compliance and safety performance. Companies at the bottom of the performance table don’t usually survive.

Accidents are not mere matters of chance; management and culture matter.

Honor Roll companies, large and small, have superior compliance records, and in 2022 these companies had 50-90% fewer INCs/facility-inspection than the Gulf of Mexico average.

Does BOEM expect noncompliance leaders to be concerned about decommissioning obligations? The record shows that they are not.

Cox’s 2023 bankruptcy was predictable given their past safety performance. In 2022, Cox was a violations leader by any measure, and was responsible for 9 of the 30 safety incidents that were significant enough to require investigation by BSEE.

Fieldwood’s terrible 2021 safety performance has been discussed, and there was ample evidence of performance problems prior to their bankruptcy declaration in 2018. In 2016 and 2017 Fieldwood was, by far, the GoM violations leader with 818 INCs, 401 of which required a facility or component shut-in.

Ironically (or maybe not), the only other company that was even in the same noncompliance ballpark as Fieldwood in 2016 and 2017 was future Cox affiliate Energy XXI GOM. Energy XXI earned 465 INCs (240 shut-ins) during that 2 year period. Did BOEM object to or otherwise comment on the 2018 Cox-Energy XXI merger?

Black Elk Energy was new in 2007 and quickly became a violations leader. Between 2010 and 2012, BSEE cited Black Elk 415 times. 218 of these violations were serious enough to require facility or component shut-ins. On November 16, 2012, explosions at Black Elk’s West Delta 32 platform killed 3 workers, and 2 others suffered severe burns. Criminal charges and a complex bankruptcy followed. BSEE records show 1107 INCs during the company’s short history, 464 of which required facility or component shut-ins.

The rapid growth of Fieldwood, Cox, and Black Elk was in part facilitated by lax lease assignment and financial assurance policies. Operating companies should have to demonstrate that they can operate safety and comply with the regulations before they are approved to acquire more properties.

The Signal Hill sagawas documented nearly 2 years ago, and none of the questions raised in that post have been answered. Violations data and inspector feedback predicted the Signal Hill/POOI failure. Nonetheless, and despite the objections of regional staff, Signal Hill was allowed to tap into its decommissioning account to cover operating expenses. Responsibility for decommissioning Platforms Hogan and Houchin is still uncertain.

Given that BSEE, not BOEM, is responsible for safety and compliance, I sincerely hope that regulatory fragmentationwas not a factor contributing to BOEM’s decision to discontinue the use of compliance data in determining financial assurance needs.

BOEM’s explanation for the proposal to eliminate the record of compliance criterion:

BOEM also proposes to eliminate the existing “record of compliance” criterion found in the current version of § 556.901(d)(1)(v). BOEM has determined that the number of INCs a company receives correlates with the number of OCS properties it owns, not its financial stability, and therefore, BOEM has concluded that it is not an accurate predictor of its financial health. BOEM reviewed BSEE’s Incidents of Non-Compliance (INCs) records and its Increased Oversight List, which represent BSEE’s cumulative records of violations of performance standards on the part of OCS operators and lessees and determined that the number of incidents of non-compliance typically increases with the size and complexity of the operator’s or lessee’s operations, including the ratio of incidents to number of components. Because larger companies (regardless of credit score) tend to have more properties and components and therefore more INCs, BOEM determined that record of compliance criterion does not accurately predict financial default. BOEM’s review of this information confirmed the feedback BOEM received in response to the 2016 NTL, namely that companies with a large number of properties and facilities tended to receive a large number of INCs and had more individual properties on the Increased Oversight List. BOEM specifically requests comments regarding the use of fines and violations as a criterion in the determination of a company’s ability to fulfill decommissioning obligations, and any data or analysis addressing any correlation between the number of violations and the risk of financial default. BOEM also requests comments on whether the elimination of the INC’s criteria would create a disincentive to comply with regulations. BOEM also requests comment on whether or not the cost of decommissioning is likely to increase based on the type, quantity, and magnitude of previous violations.

On a related note, BOEM/BSEE should consider a followup to the John Shultz thesis which found that INCs are a very good predictor of accidents and spills.

BOEM has rather surprisingly proposed to eliminate consideration of a company’s compliance record in determining the need for supplemental financial assurance.An opposing view will be posted tomorrow.

If a lease has proved reserves with a value of at least three times that of the estimated decommissioning cost, no supplemental financial assurance would be required. Comparing two imprecise and variable estimates is neither a simple nor reliable method for determining the need for supplemental financial assurance. BOEM should look at the history of the Carpenteria field (Santa Barbara Channel) and the reserve estimates that were provided to discount decommissioning risks. More on this at a later date.

Transferor liability applies only to those obligations existing at the time of transfer; new facilities, or additions to existing facilities, that were not in existence at the time of any lease transfer are not obligations of a predecessor company and are considered obligations of the party that built such new facilities and its co- and successor lessees. This is a good policy, but is difficult to implement. Some of the complexities may need to be addressed.More later.

The “reverse chronological order” provision was withdrawn in April, so there is no defined process for issuing decommissioning orders to predecessor lessees. Is it good policy to first issue such orders to companies who may have owned leases decades ago, in some cases prior to the establishment of transferor liability in the 1997 MMS “bonding rule?”

The proposed rule would clarify that BOEM will not approve the transfer of a lease interest until the transferee complies with all applicable regulations and orders, including the financial assurance requirements. BOEM needs to be firmly enforce this policy. See tomorrow’s post.

The proposed rule would not allow BOEM to rely upon the financial strength of predecessor lessees when determining whether, or how much, supplemental financial assurance should be provided. This is a good provision.

BOEM proposes to use the P70 probabilistic value to set the amount of any required supplemental financial assurance. These estimates do not seem sufficiently conservative to protect other parties and the public in the event of default. This is particularly true after storm damage which can increase plugging costs more than tenfold.

The probabilistic cost estimates were updated in 2020 and are based on data submitted subsequent to 2016 and 2017 NTLs. How often will these estimates be updated?

The final rule should specify that funds may not be withdrawn from decommissioning accounts for operational purposes, and that BOEM approval is required for such withdrawals.