In 2025, NRW/Array operations accounted for 486 incidents of non-compliance (INCs), 36.2% of the Gulf of America total. Array and NRW had INC/facility inspection rates of 2.1 and 7.0 respectively, well above the Gulf average of 0.42 and the top performers’ rates of 0.05 to 0.13.

In Array’s defense, their violations declined sharply in the second half of 2025. However, the number of inspections of their facilities declined even more sharply, so the INCs/facility inspection ratio actually increased in the second half.

For the 2025 data in the table below:W=warning, CSI=component shut-in, FSI=facility shut-in. The 3 numbers for Array in each box are full year 2025 data (top), first half 2025 (middle), and second half 2025 (bottom)

operator

W

CSI

FSI

total INCs

Facility Insp.

INCs/isp

Array

352 311 41

93 46 47

6 6 0

451 363 88

218 184 34

2.1 2.0 2.6

NRW

10

24

1

35

5

7.0

Three other companies had more than 10 shelf platforms and INC/facility inspection ratios >1.0: Greyhound Energy (23 platforms), Renaissance (21 platforms) and Sanare Energy (38 platforms).

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac. insp

Greyhound Energy

32

1

0

33

23

1.4

Renaissance Offshore

26

19

3

47

44

1.1

Sanare Energy

60

20

2

82

75

1.1

The table below provides 2025 oil and gas production through Oct (with Gulf of America rank) for the 5 companies mentioned in this post. In determining rankings, subsidiaries and affiliates were counted as a single company (e.g. Chevron, Unocal, and Hess counted as one company).

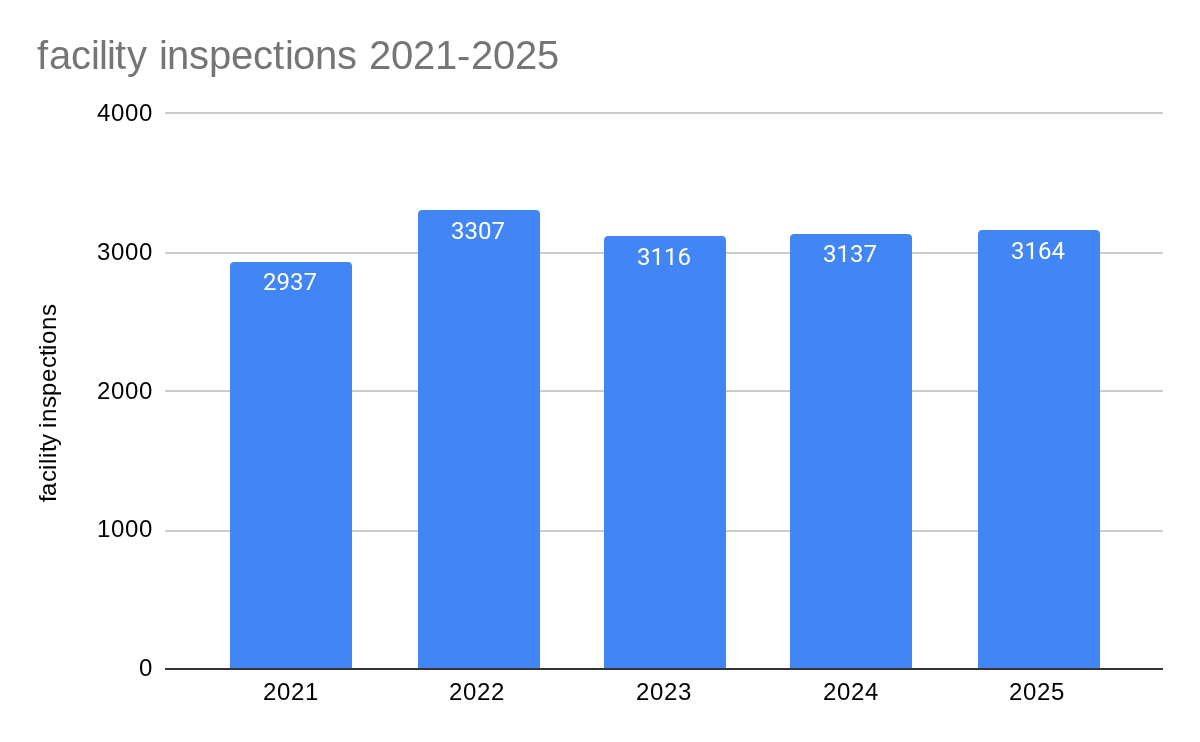

The number of BSEE inspections in 2025 (first chart) remained relatively constant despite the extended government shutdown.

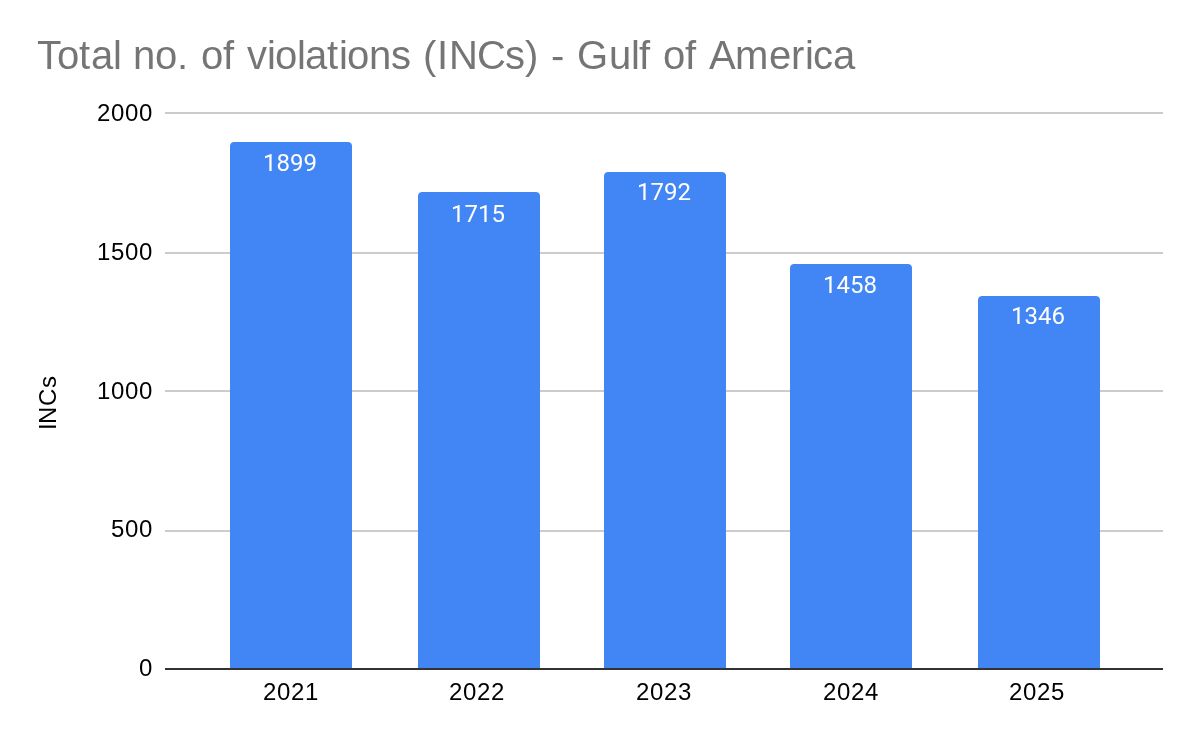

The decline in the number of Incidents of Noncompliance (INCs) in 2025 is encouraging (chart 2).

Given that BSEE’s tables have yet to be updated to include 2024 incidents, let alone 2025, it’s difficult to assess whether there have been similar declines in the number and severity of incidents. We do know that there were no occupational fatalities in 2025. (Note that OCS incident tables were once updated within 30 days at the end of each quarter. The public has a right to timely information on the type of incidents that are occurring, the operating companies, and the resulting casualties, pollution, and property damage.)

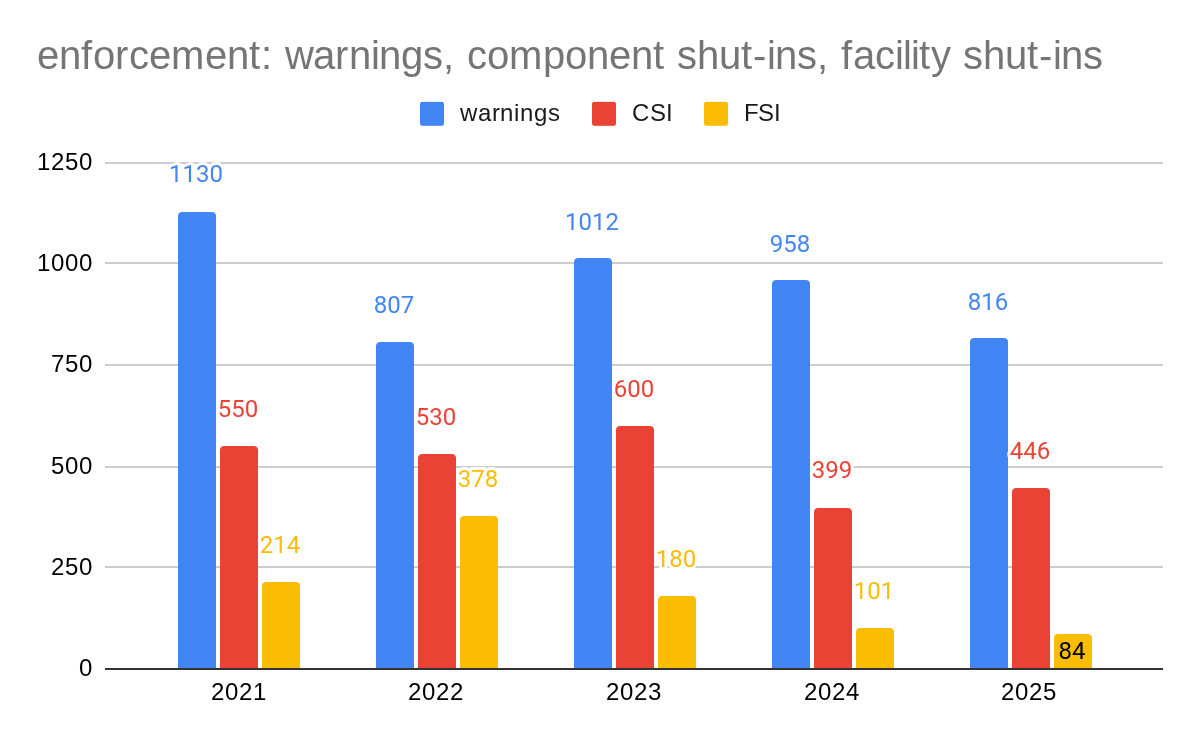

Chart 3 shows the decline in INCs by type – warnings, component shut-ins, and facility shut-ins

As is typically the case, a few companies accounted for a disproportionate number of violations, most notably the Cox legacy operators. More on this in a subsequent post.

The top 6 oil producers all had excellent compliance records, as did a leading shelf operator. More to follow.

Sable Offshore, California’s most notorious operator, fared well during 77 inspections of their three platforms in the Santa Barbara Channel.

The COS has been effective in strengthening corporate Safety and Environmental Management Systems, influencing the industry’s safety culture, and sharing best practices and lessons learned. These are important accomplishments.

The COS has fallen short in gathering the data needed to assess the offshore industry’s safety performance. As is the case with most voluntary reporting programs, data completeness and accuracy issues limit the significance of COS performance reviews.

The COS uses accepted performance indicators and a logical classification scheme.

COS reports that their members accounted for 78% of OCS oil and gas activity in 2024. This is accurate when cross-checked with BSEE hours worked data. However, the % of hours worked is not a good measure of the % of incidents reported in any category.

Only two drilling contractors – Helmerich & Payne and Valaris – are members. Major contractors like Noble, Transocean, and Seadrill are not members. Their incidents will thus not be reported if they are not working for a COS member.

No production contractors are COS members. These companies conduct most of the platform operations on the shelf, where many of the lease operators are not COS members.

Pacific and Alaska Region operators do not participate.

Looking only at fatalities (table below), the most important and easily verified incident category, there are troubling omissions:

COS reports no 2024 fatalities when in fact there was a fatality during an operation for a COS member.

COS reports no 2022 fatalities when there were actually five. A workover incident took the life of one worker, and four died in a helideck crash on an OCS platform. In both cases, the facility operator was a non-member company.

COS records one 2021 fatality, but fails to include a 2021 Fieldwood fatality. There were also6 “non-occupational” fatalities on OCS facilities in 2021, as classified by BSEE. Given the importance of worker health (the H in HSE), such a high number of non-occupational fatalities should be of interest industry-wide.

The COS report includes only two of the six 2020 fatalities, 2 of which were classified by BSEE as non-occupational.

The bottom line is that COS accounted for only 3 of 12 (25%) occupational fatalities during the 2020-24 period. There were at least 20 fatalities if you include the non-occupational incidents.

fatalities per COS

occupational fatalities (from BSEE data)

non-occupational fatalities (from BSEE data)

2024

0

1

?

2023

0

0

?

2022

0

5

?

2021

1

2

6

2020

2

4

2

The offshore industry is only as good as its worst performer, so complete participation is essential. Voluntary reporting is seldom complete reporting, because some companies are more concerned about confidentiality than completeness and information sharing.

For industry reporting programs to be comprehensive and credible:

The entity receiving the reports and managing the data must be independent and not affiliated with an industry advocacy organization.

All operating companies must participate and complete reporting must be required. This can be accomplished contractually. If necessary, the regulator can require participation (either as a separate regulation or as a SEMS element).

Company incident submittals should be audited by the independent entity.

Fees should be solely for the purpose of supporting the independent reporting system.

For SP1 and SP2 incidents (per the COS classification scheme), the names of the responsible companies should be included in the performance reports. The current COS system prioritizes confidentiality over accountabiity and information sharing.

NRW contracted with Array Petroleum to operate the former Cox Assets. Array subsequently sued NRW, asserting that NRW received $78,000,000 in revenue, but disbursed only about $48,000,000 to pay Array’s invoices and those of the subcontractor.

The court filing claimed that NRW failed to pay Array $2.5 million, the subcontractors $10.7 million, and the United States $12 million. A large share of the subcontractor costs were probably for well operations given that 21 Array workover applications were approved in 2024 and 2025. The $12 million due to the Federal government is reportedly for royalty payments. Were any revenues set aside for decommissioning liabilities?

Array’s lawsuit was dismissed by the court on January 3, 2025, after a joint motion to dismiss was filed by the defendants. Information on the reasons for the dismissal is not publicly available.

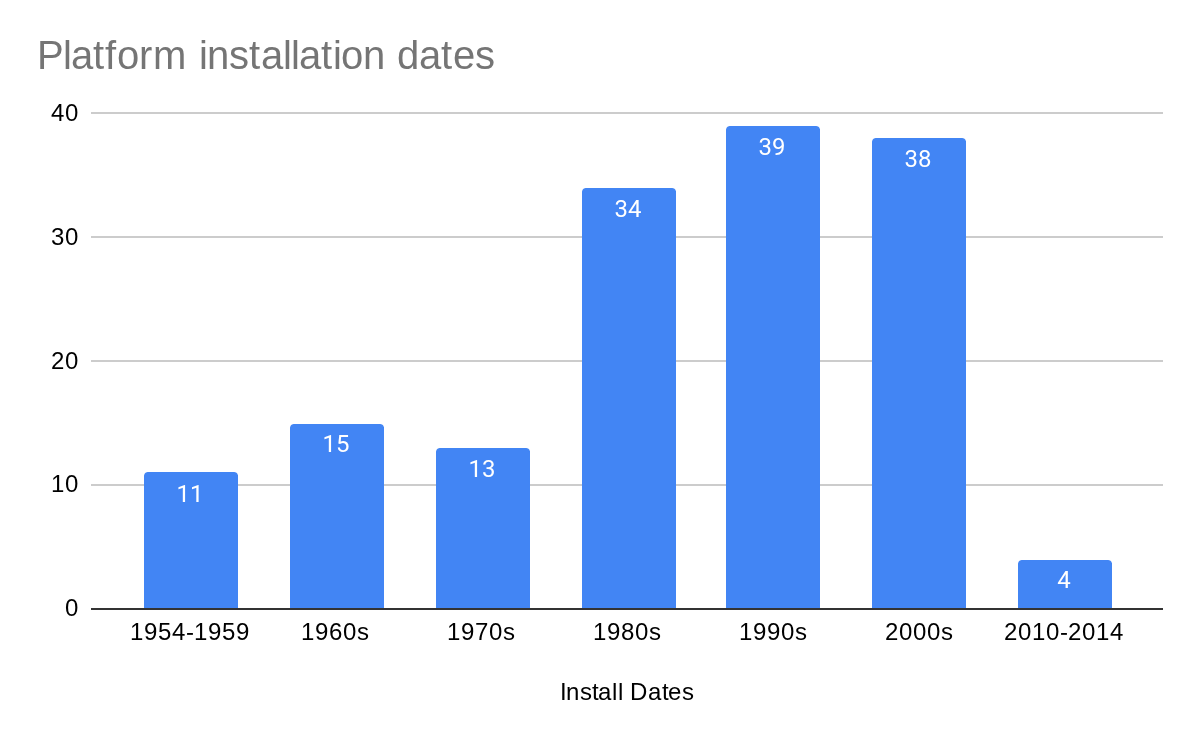

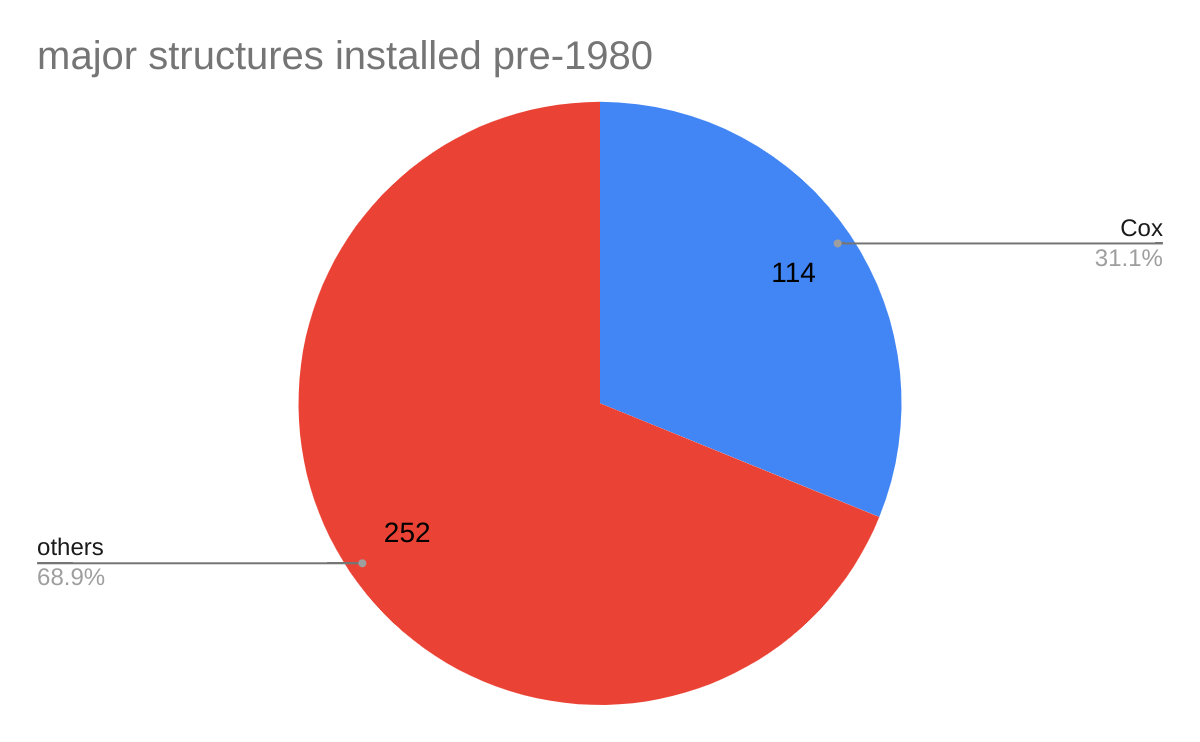

Old platforms: According to BOEM records, Array operates 154 platforms previously owned by Cox. These platforms are in the Ship Shoal, South Marsh Island, and West Delta areas of the Gulf of America. Most are >30 years old and four are more than 70 years old (see chart below). 41 are classified as major structures including 15 of the 26 platforms installed in the 1950s and 1960s. 44 are manned on a 24 hour basis. 79 have helidecks. Massive decommissioning liabilities loom.

Violations: NRW/Array ranks 37th out of 42 companies in GoA oil production (2025 YTD) and 36th out of 42 companies in gas production, but leads the pack in Incidents of Noncompliance (INCs):

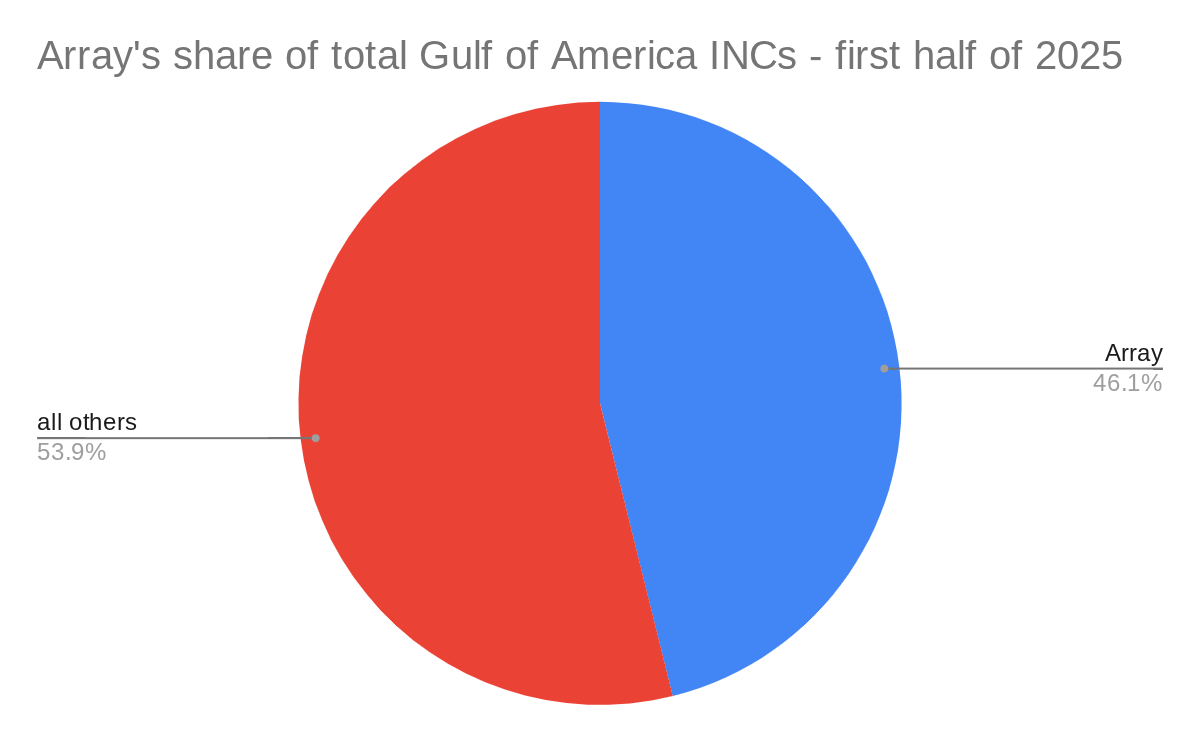

Array accounted for nearly half of all GoA INCs issued in the first half of 2025 (chart below).

Array was issued 9 times more warning INCs (311) than any other operator. Apache was second with 34.

There are many small and mid-sized companies that are responsible operators. Their participation in the OCS program should be encouraged. However, others have demonstrated, by their inattention to financial and safety requirements, that they are not fit to operate OCS facilities.

The growth of Fieldwood, Cox, Signal Hill, and Black Elk was in part facilitated by lax lease assignment and financial assurance policies.

Operating companies should have to demonstrate that they can operate safety and comply with the regulations before they are approved to acquire more properties.

Expect the ultimate public cost of the Cox bankruptcy, in terms of decommissioning liabilities and the need for increased oversight, to be large.

The Federal govt (Justice/Interior) should strongly oppose bankruptcy court asset sales that increase public financial, safety, and environmental risks.

The previously discussed sale of Cox assets in 6 GoM fields to W&T was completed in January for $72 million, $16.5 million less than the proposed price. W&T, an established GoM operator, believes they can increase the pre-bankruptcy production (8300 boepd) through workovers, recompletions, and facility repairs.

The extent to which W&T is assuming decommissioning liability for the Cox assets is unclear to this observer. Decommissioning information from W&T’s SEC filing is pasted at the end of this post.

In February, Cox won court approval to sell “about a dozen oil fields to Natural Resources Worldwide LLC for about $20 million following a bankruptcy court auction.” This sale is more concerning given that the purchaser has no operating history in the GoM, and scant information about the company can be found online. Perhaps they are affiliated with Natural Resources Partners L.P., an energy investment firm which “owns mineral interests and other rights that are leased to companies engaged in the extraction of minerals,” but “does not mine, drill, or produce minerals, has no operations, and conducts business solely in an office environment.”

Per BOEM data, Cox filed requests to assign a number of leases to Natural Resources Worldwide (NRW) in May, but those requests have yet to be approved. Hopefully, BOEM is taking a hard look at these requests and their obligations following the court auction. Decommissioning liabilities should be their number one concern. (Note: NRW was just listed as the operator of the former Cox platform at EI 361, so presumably at least some of those assignments have now been approved.)

According to BOEM’s platform data base, Cox and affiliates Energy XXI and EPL still operate 243 platforms, down from 435 in June 2023. Also per the data base, the Cox companies have not removed any platforms during 2023 or 2024 YTD, so the reduction in platforms is presumably the result of the W&T transaction. Most of the remaining Cox platforms are old – 16 of their 77 major platforms were installed in the 1950s!

Meanwhile, Cox and affiliates continue to be the GoM violations leader by far with 549 incidents of non-compliance (INCs) in 2024 YTD, 45% of the GoM total for all operators. No other company has more than 100 INCs (although Whitney Oil and Gas has a disappointing 93 INCs, including 33 facility shut-ins on only 65 inspections!)

operator

platforms/ major platforms

warning INCs

component shut-in INCs

facility shut-in INCs

Cox

209/69

407

44

4

Energy XXI

19/7

73

1

2

EPL

5/1

16

1

1

Total Cox

233/77

496

46

7

Total GoM

1519/736

831

317

68

INCs are for 2024 as of 9/17/2024. A major platform has at least 6 well completions or more than 2 pieces of production equipment.

The Company may be subject to retained liabilities with respect to certain divested property interests by operation of law. Certain counterparties in past divestiture transactions or third parties in existing leases that have filed for bankruptcy protection or undergone associated reorganizations may not be able to perform required abandonment obligations. Due to operation of law, the Company may be required to assume decommissioning obligations for those interests. The Company may be held jointly and severally liable for the decommissioning of various facilities and related wells. The Company no longer owns these assets, nor are they related to current operations.

During the three months ended March 31, 2024, the Company incurred $2.6 million in costs related to these decommissioning obligations and reassessed the existing decommissioning obligations, recording an additional $5.3 million. As of March 31, 2024, the remaining loss contingency recorded related to the anticipated decommissioning obligations was $20.8 million.

Although it is reasonably possible that the Company could receive state or federal decommissioning orders in the future or be notified of defaulting third parties in existing leases, the Company cannot predict with certainty, if, how or when such orders or notices will be resolved or estimate a possible loss or range of loss that may result from such orders. However, the Company could incur judgments, enter into settlements or revise the Company’s opinion regarding the outcome of certain notices or matters, and such developments could have a material adverse effect on the Company’s results of operations in the period in which the amounts are accrued and the Company’s cash flows in the period in which the amounts are paid. To the extent that the Company does incur costs associated with these properties in future periods, the Company intends to seek contribution from other parties that owned an interest in the facilities.

The bankruptcy court’s priorities should be 1) minimizing safety and environmental risks and 2) protecting the public from the massive decommissioning liabilities.

Per the latest BOEM information, Cox and affiliates Energy XXI and EPL operate 477 platforms, which is 31% of the Gulf of Mexico total! (See the related information posted last June.) BSEE estimates that the decommissioning costs for these platforms will exceed $4.5 billion!

Per BSEE data, Cox and its affiliates were cited for 780 incidents of noncompliance (violations) in 2023. They thus accounted for 43% of all 2023 GoM INCs.

Questions:

How will taxpayers be protected from Cox’s $4.5+ billion decommissioning obligations?

What is the plan for both safely decommissioning facilities and operating those that remain?

Why was Cox allowed to continue expanding GoM operations without demonstrating financial assurance and operational competence?

How was a failing operator (Cox) selected just 8 months ago for a Federally funded (DOE) project to repurpose GoM facilities for carbon sequestration purposes?

The Cox bankruptcy is yet another costly lesson for Federal regulators. Moving forward, decommissioning and lease assignment policies must prioritize safety, environmental protection, and protection of the public’s financial interests.

In a draft rule published on June 29, 2023, BOEM proposes to discontinue using a company’s record of compliance in determining the need for supplemental financial assurance for decommissioning. BOEM’s full explanation for this surprising change is pasted at the end of this post.

Opposing view:

BOEM should be more attentive, not less, to safety performance and compliance data. If they were, taxpayers would have been better protected from the risks associated with the lease acquisitions by Fieldwood, Cox, Black Elk, Signal Hill, and others, and their subsequent bankruptcies.

Safe operations, as reflected in compliance and performance data, are critical to a company’s financial success.

BOEM wrongly infers that Incidents of Noncompliance (INCs) are solely dependent on the number and complexity of facilities. Decades of normalized compliance data have told us that there are marked differences among operators in terms of compliance and safety performance. Companies at the bottom of the performance table don’t usually survive.

Accidents are not mere matters of chance; management and culture matter.

Honor Roll companies, large and small, have superior compliance records, and in 2022 these companies had 50-90% fewer INCs/facility-inspection than the Gulf of Mexico average.

Does BOEM expect noncompliance leaders to be concerned about decommissioning obligations? The record shows that they are not.

Cox’s 2023 bankruptcy was predictable given their past safety performance. In 2022, Cox was a violations leader by any measure, and was responsible for 9 of the 30 safety incidents that were significant enough to require investigation by BSEE.

Fieldwood’s terrible 2021 safety performance has been discussed, and there was ample evidence of performance problems prior to their bankruptcy declaration in 2018. In 2016 and 2017 Fieldwood was, by far, the GoM violations leader with 818 INCs, 401 of which required a facility or component shut-in.

Ironically (or maybe not), the only other company that was even in the same noncompliance ballpark as Fieldwood in 2016 and 2017 was future Cox affiliate Energy XXI GOM. Energy XXI earned 465 INCs (240 shut-ins) during that 2 year period. Did BOEM object to or otherwise comment on the 2018 Cox-Energy XXI merger?

Black Elk Energy was new in 2007 and quickly became a violations leader. Between 2010 and 2012, BSEE cited Black Elk 415 times. 218 of these violations were serious enough to require facility or component shut-ins. On November 16, 2012, explosions at Black Elk’s West Delta 32 platform killed 3 workers, and 2 others suffered severe burns. Criminal charges and a complex bankruptcy followed. BSEE records show 1107 INCs during the company’s short history, 464 of which required facility or component shut-ins.

The rapid growth of Fieldwood, Cox, and Black Elk was in part facilitated by lax lease assignment and financial assurance policies. Operating companies should have to demonstrate that they can operate safety and comply with the regulations before they are approved to acquire more properties.

The Signal Hill sagawas documented nearly 2 years ago, and none of the questions raised in that post have been answered. Violations data and inspector feedback predicted the Signal Hill/POOI failure. Nonetheless, and despite the objections of regional staff, Signal Hill was allowed to tap into its decommissioning account to cover operating expenses. Responsibility for decommissioning Platforms Hogan and Houchin is still uncertain.

Given that BSEE, not BOEM, is responsible for safety and compliance, I sincerely hope that regulatory fragmentationwas not a factor contributing to BOEM’s decision to discontinue the use of compliance data in determining financial assurance needs.

BOEM’s explanation for the proposal to eliminate the record of compliance criterion:

BOEM also proposes to eliminate the existing “record of compliance” criterion found in the current version of § 556.901(d)(1)(v). BOEM has determined that the number of INCs a company receives correlates with the number of OCS properties it owns, not its financial stability, and therefore, BOEM has concluded that it is not an accurate predictor of its financial health. BOEM reviewed BSEE’s Incidents of Non-Compliance (INCs) records and its Increased Oversight List, which represent BSEE’s cumulative records of violations of performance standards on the part of OCS operators and lessees and determined that the number of incidents of non-compliance typically increases with the size and complexity of the operator’s or lessee’s operations, including the ratio of incidents to number of components. Because larger companies (regardless of credit score) tend to have more properties and components and therefore more INCs, BOEM determined that record of compliance criterion does not accurately predict financial default. BOEM’s review of this information confirmed the feedback BOEM received in response to the 2016 NTL, namely that companies with a large number of properties and facilities tended to receive a large number of INCs and had more individual properties on the Increased Oversight List. BOEM specifically requests comments regarding the use of fines and violations as a criterion in the determination of a company’s ability to fulfill decommissioning obligations, and any data or analysis addressing any correlation between the number of violations and the risk of financial default. BOEM also requests comments on whether the elimination of the INC’s criteria would create a disincentive to comply with regulations. BOEM also requests comment on whether or not the cost of decommissioning is likely to increase based on the type, quantity, and magnitude of previous violations.

On a related note, BOEM/BSEE should consider a followup to the John Shultz thesis which found that INCs are a very good predictor of accidents and spills.

As illustrated in the charts below, Cox has the distinction of being the Gulf of Mexico (world?) leader in aging offshore platforms. Per BOEM data, Cox (includes affiliates Energy XXI GOM and EPL) operates more than 1/4 of all GoM platforms. 44% of these platforms were installed prior to 1980, 114 of which are major structures (defined in notes below). 27 of these major structures were installed prior to 1960!

Notes: (1) A major structure contains at least 6 well completions or more than 2 pieces of production equipment. (2) The platform numbers in an earlier post are incomplete in that they include only structures with helidecks.

Along with Cox Operating, six affiliates also filed: MLCJR , M21K, EPL Oil & Gas, Cox Oil Offshore, Energy XXI Gulf Coast, and Energy XXI GOM.

The BOEM platform data base lists only Cox Operating (276 platforms), EPL (10 platforms), and Energy XXI GOM (26 platforms) as current operators of OCS platforms. However, according to the Cox Operating website, the company operates 600 producing wells on 500 structures. Presumably, ~200 of those structures are in State waters.

In 2020, the OPEC price war drove oil prices down, while stay-at-home orders and well shut-ins associated with the COVID-19 global pandemic sharply reduced production.

The debtors’ assets suffered significant damage from five named storms and hurricanes during 2020 and 2021, leading to further reductions in production. Comment: According to BSEE, 7 tropical systems affected GoM operations in 2021, so the number of storms is not in dispute. The extent to which maintenance or preparedness issues contributed to the damage is unknown.

In 2020, a foreign-flagged vessel struck a platform owned by one of the debtors resulting in major damage and substantial losses of production. Comment: Apparently, this is the incident being cited. According to the BSEE report, the operator (Cox) was not at fault. Per BSEE: (1) The navigational lights and foghorn on the platform were maintained and in operational order, (2) the allision was not due to any platform related error, and (3) the platform’s operator and safety system responded in accordance with the regulations.

At this time, the debtors’ production volume is half what it was in 2019. Comment: Comparing the 2019 and 2022 production data, OCS oil and gas production are down by about 30% and 40% respectively. However, the 50% reduction figure seems reasonable given the likelihood of further reductions in State water production and in 2023.