Mike Werth’s response to Jim Kramer’s question about US production leadership is spot-on (see the clip below).

Kudos to Kramer for visiting Chevron’s Anchor platform in the Gulf of Mexico. More business/energy reporters and government officials with energy responsibilities need to (1) learn more about offshore oil and gas exploration and development and (2) visit offshore facilities.

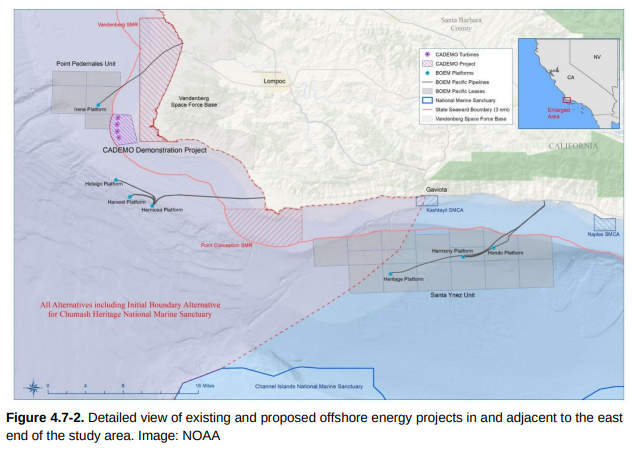

Almost 40 years ago, four large oil and gas platforms were installed in the beautiful offshore area that was part of our Santa Maria District (Pacific Region of the Minerals Management Service). Those platforms are now within the boundaries of the Chumash Heritage National Marine Sanctuary (see map above).

We watched those platforms being installed, inspected the drilling and production operations, and performed a myriad of other duties including the curtailment of offshore operations prior to launches from Vandenberg AFB. Those Vandenberg launches weren’t always perfect as this link clearly demonstrates. Even knowing that, it was still a bit unnerving when missiles were recovered during post-abandonment site clearance trawls.

All four of those Santa Maria District platforms are now on terminated OCS leases. All were installed by companies that are now part of Chevron Corp. (Chevron, Texaco, and Unocal). They are currently maintained by Freeport-McMoRan Oil & Gas, with Chevron retaining financial responsibility for decommissioning.

Platform

Install yr.

installed by

water depth (ft)

Est. removal weight (short tons)

wells drilled

Harvest

1985

Texaco

675

35,150

19

Hermosa

1985

Chevron

603

30,868

13

Hidalgo

1986

Chevron

430

23,384

14

Irene

1985

Unocal

242

8,762

26

BSEE reports that the 46 wells on Harvest, Hermosa, and Hidalgo have been plugged and tested, and that the well conductors have been removed. No information has been posted on the status of the wells at Platform Irene, but presumably they are (or will soon be) plugged in accordance with BSEE regulations.

Will the inclusion of these platforms in the Chumash Marine Sanctuary further complicate the already difficult decommissioning process? Decommissioning specialist John Smith thinks it may:

“In addition to the BOEM and BSEE approval process, Chevron and FMC are going to be dealing with the NOAA permitting regime for Sanctuaries. Those permitting and environmental compliance requirements are extensive. NOAA’s NEPA documentation for West Coast marine sanctuaries will also need to be amended to include the Chumash.”

So the “Mission Impossible” that is California OCS decommissioning now has yet another complex regulatory element.

“Even though most of the SYU facilities are outside the Sanctuary, the proximity of the operations to the Sanctuary is problematic. The Chumash are now going to be a co-manager of the Sanctuary, adding another player in the process. Sable is going to obtain multiple Federal, State and local permits to restart SYU, and law suits are likely at every stage of the process.”

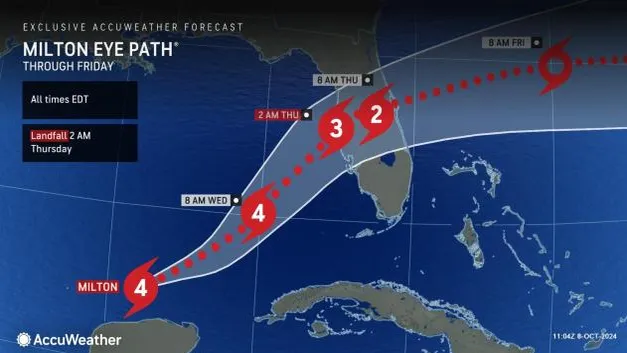

In light of Hurricane Milton’s more southerly and easterly track, Chevron’s Blind Faith floating production unit is the only GoM platform reported to be shut-in at this time. Blind Faith was installed in 2008 in 6480′ of water in the Mississippi Canyon area, and is reportedly producing 65,000 bopd.

Chevron slide: Advances in seismic imaging help characterize deepwater development opportunities

A new JPT article features comments from BOE contributor Lars Herbst on advances in HPHT technology, control systems, sensors and transmitters, and automation that are facilitating the next era of deepwater development.

Well capping technology, which provides a tertiary well control capability, is an essential element of post-Macondo exploration and development. Lars points to the importance of BSEE’s unannounced drill program to verify that capping stacks can be transported and installed in a timely manner. Chevron expresses pride in leading a team that deployed and installed a capping stack in 6,200 feet of water in a drill monitored by BSEE. During that drill, a remotely operated vehicle (ROV) closed 10 valves to shut in a simulated well.

Exxon’s Jayme Meier aptly characterizes the challenge and excitement of deepwater development:

“You are floating on a surface, and you have to be able to pinpoint exactly where you’re going to land subsea hardware, exactly where you’re going to moor an FPSO and hit target boxes that are a few feet by a few feet, and they’re 6,000 ft below you,” she said. “It is the most exciting thing that I’ve ever been involved in. And it involves technology, technical know-how, and an ability to really plan the base plan and the contingency plan.”

Advances in deepwater technology are indeed impressive, but continuous improvement must always be the objective. In that regard, Lars rightfully emphasizes the importance of sustaining research through the industry’s up and down cycles.

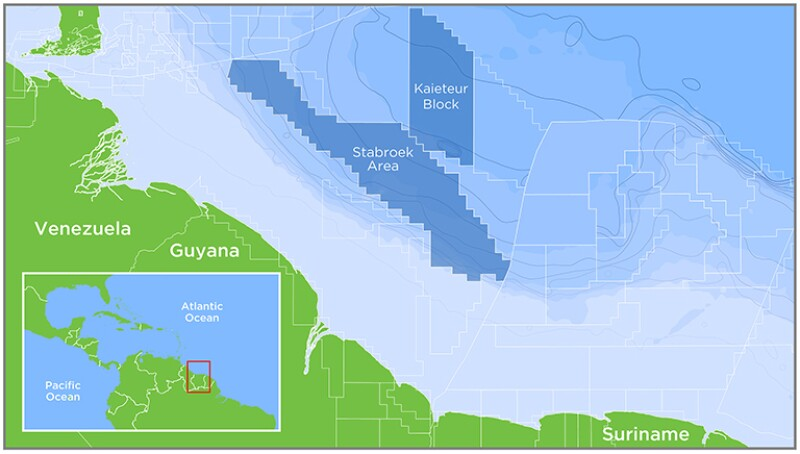

Reuters has published an interesting article on the Exxon/CNOOC vs. Chevron/Hess dispute scheduled for arbitration next year in Paris. According to Reuters (emphasis added):

“Getting the panel to consider the appraised value is central to Exxon’s claim that the deal is an asset acquisition disguised as a merger. Exxon believes the Guyana asset is so valuable that the merger would trigger a change of control and give Exxon and CNOOC a right of first refusal to the asset sale, the people said.“

The Exxon argument implies that Hess’s only major asset is its share of Stabroek, which is hardly the case. Hess’s 30% Stabroek share is without question an important asset with great long-term potential, but Hess is also a major player elsewhere, most notably in the Bakken formation in North Dakota and the Gulf of Mexico. Implying that Hess was a single asset acquisition is thus misleading:

In Q4 of 2023, Hess produced 194,000 boepd in the Bakken formation vs. a Stabroek share of 128,000 bopd.

In 2023, Hess produced 20 million barrels of oil in the GoM and 40 bcf of gas making them the 8th highest oil producer and 7th highest gas producer.

Hess acquired 20 GoM leases in Sale 261, ranking first in total high bids ($88 million) among all participants.

Chevron and Hess GoM assets have significant potential for synergy. The combined company would be the 3rd largest GoM oil producer (behind Shell and bp) and the second largest gas producer (behind only Shell).

This dispute will continue to smolder given the delay in the arbitration hearings until May 2025. As previously mentioned, I believe the Government of Guyana should have intervened. I’m all for companies settling their disputes privately, but this dispute is over Guyanese resources, and the protracted delay could have implications for Guyana.

Four of the five simpler, safer, greener deepwater platforms featured on this blog are now producing. The 5th platform (Whale) is on location and scheduled to begin production later this year.

platform

operator

first production

King’s Quay

Murphy

April 2022

Vito

Shell

Feb 2023

Argos

bp

April 2023

Anchor

Chevron

Aug 2024

Whale

Shell

late 2024

These platforms are in 4000 to 8600′ of water, are expected to reach peak production rates of 100-150,000 boe/day, and have favorable emissions characteristics on a per barrel basis.

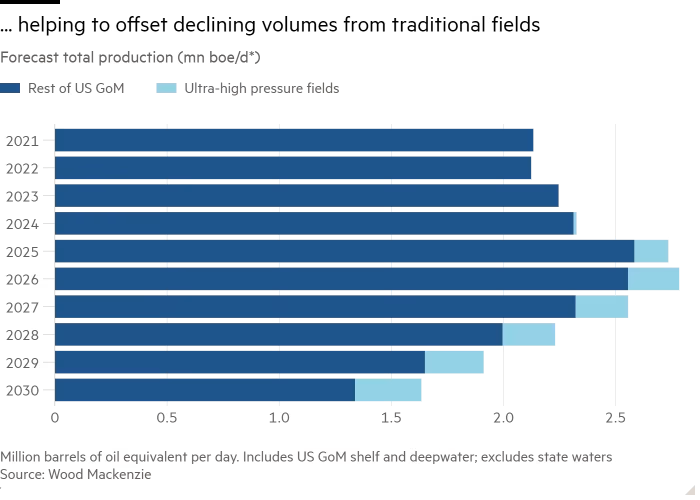

This is all good, but what is next? Will technological advances once again sustain GoM production? The short answer appears to be yes!

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades will facilitate production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded below.)

Chevron’s Anchor is the first deepwater, high-pressure development. Three similar deepwater hub platforms (table below) will begin production over the next 5 years. These host platforms will also facilitate additional production from nearby fields. Each will have production capacities of approximately 100,000 boe/day. Note the long lead times in achieving first production given the technological issues that had to be evaluated and addressed.

platform

operator

discovery date

first production

Kaskida

bp

2006

2029

Sparta

Shell

2012

2028

Shenandoah

Beacon

2009

2025

Wood Mackenzie sees these high pressure projects as the key to sustaining GoM production rates. Their projections for 2024 and 2025 seem optimistic based on 2024 YTD data, which adds to the importance of the projected new production.

Diamond Ocean Blackhawk is drilling MC 40 well for Anadarko

Following up on last year’s deepwater diligence post, 4 recent deepwater exploratory wells (table below) were spudded within 4.5 years of the effective date of their leases.

Particularly noteworthy is Anadarko’s well on newly acquired Mississippi Canyon Block 40, which was spudded only 18 months after the lease was acquired. Everything has to be in place for such an outcome: corporate priority, data gathering and analysis, well plan, permitting, and rig contract/availability.

The well was apparently a high priority not just for Anadarko, but also for Chevron and Murphy. MC 40 was acquired by Chevron (bidding alone) at Sale 257 for $4,409,990, the third highest bid at the sale. Murphy had submitted a losing bid of $3 million, but was assigned a 33% share of the lease by Chevron on 12/15/2023. One month earlier, Anadarko had been assigned a 33% interest and became lease operator.

Interestingly, BOEM’s Mean Range of Value (MROV) estimate for the block was only $576,000, so the three companies are seeing something that BOEM doesn’t. We’ll see how this plays out.

According to rig tracker data the Ocean Blackhawk is still on location at MC 40. Per BSEE permitting data, the well was approved to be bypassed in mid-May.

As we wait for the International Chamber of Commerce (ICC) arbitration panel to rule on the Exxon-CNOOC-Chevron-Hess Stabroek dispute, key excerpts from Chevron’s SEC filing about their merger with Hess are pasted below. The text highlighted in red is particularly interesting.

If the ICC arbitration panel rules that the right-of-first-refusal (ROFR) provision applies, the Chevron filing says that the merger is off and Hess continues as Stabroek’s 30% owner. If that statement is correct, Exxon and CNOOC cannot obtain the Hess share. Their only benefit from the challenge would be to deny their rival Chevron from participating in the block or to receive payment from Chevron for approving the ownership change.

It’s also noteworthy that Exxon initially showed support for the deal (quote below).

p. 32: With respect to the Stabroek ROFR (as defined in the section entitled “The Merger—Stabroek JOA”), if the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close. Some of these conditions are not in Hess’ or Chevron’s control.

Further, subject to any then ongoing arbitration relating to the Stabroek JOA, either Chevron or Hess may terminate the merger agreement if the merger has not been completed by October 22, 2024, (or April 22, 2025 or October 22, 2025, if the applicable end date is extended pursuant to the merger agreement) or by such later date as the parties may mutually agree.

p. 81: The Stabroek JOA contains a right of first refusal (the “Stabroek ROFR”) provision that, if applicable to a change of control transaction and properly exercised, provides the Stabroek Parties with a right to acquire the participating interest in the Stabroek Block held by the Stabroek Party subject to such transaction (at a value that is based on the portion of the value of the change of control transaction that reasonably should be allocated to such participating interest and is increased to reflect a tax gross-up) only after, and conditioned on, the closing of such transaction. Chevron and Hess believe that the Stabroek ROFR does not apply to the merger due to the structure of the merger and the language of the Stabroek ROFR provisions.

p. 82: On October 24, 2023, shortly after the merger was announced, Exxon issued the following statement, indicating its support for the merger: “Hess has been a valued partner in Guyana since 2014 and we look forward to continuing our successful operations in the Stabroek block with Chevron, pending the deal closing.” However, Exxon and CNOOC subsequently informed Chevron and Hess that they believe the Stabroek ROFR applies to the merger. Hess, Chevron, Exxon and CNOOC subsequently engaged in discussions regarding the applicability of the Stabroek ROFR to the merger.

If the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close, and, pursuant to the terms of the Stabroek JOA, the Exxon affiliate and the CNOOC affiliate would cease to have rights under the Stabroek ROFR with respect to the merger. In that event, Hess would remain an independent public company and would continue to own its participating interest in the Stabroek Block. Based on the express terms of the Stabroek JOA, Chevron and Hess do not believe there is any material likelihood that the circumstances described in this paragraph will occur.

p. 118: In addition, with respect to the Stabroek ROFR, if the arbitration does not result in a confirmation that the Stabroek ROFR does not apply to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close.

Chevron continues to operate in Venezuela and is a beneficiary of the easing of US sanctions that facilitated the resumption of oil exports. Is the government of Guyana okay with Stabroek partners helping to support the regime that claims much of their offshore oil?

On the other hand, what about Exxon’s Stabroek partner, state-owned China National Offshore Oil Corp.? CNOOC has a 25% share of the Stabroek block (vs. 45% for Exxon and 30% for Hess) as a result of their takeover of (Canadian) Nexen in 2013. The CNOOC acquisition of Nexen was similar to Chevron’s acquisition of Hess. Was Exxon okay with that change in ownership?

CNOOC hasn’t released any public statements on the Stabroek dispute, but appears to be aligned with Exxon. Presumably, CNOOC also wants a larger share of the Stabroek pie. Is the Government of Guyana okay with an ally of Venezuela increasing their influence and having access to geologic, reservoir, and operational data for the Stabroek block? CNOOC is also partnered with Exxon on the block they acquired at the most recent licensing round.

Given the national security implications, is the Government of Guyana okay with leaving the resolution of this dispute to an ICC tribunal in Paris?