The 2019 annual production record remains intact at 1.897 million bopd, but could be exceeded in 2023 if (1) projected deepwater startups are on schedule, (2) prices remain above $70/bbl, (3) depletion is effectively managed, and (4) the hurricane season is again favorable

The “energy transition” will not affect oil and gas demand for the foreseeable future, more nuclear power plants are not being built, and shale has its limitations. We better not neglect what is left of the OCS oil and gas program.

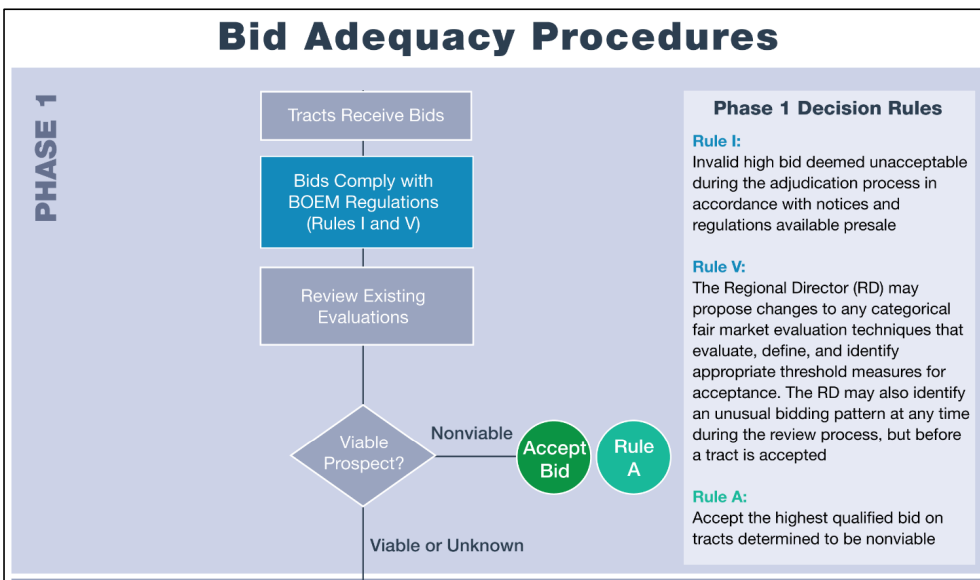

BOEM’s new procedures, which have been published for public comment, seem reasonable. However, it would be helpful to learn more about the testing of the new methodology. (See the quote below). Further, would the rejected Sale 257 bid have been accepted? What was the LBCI for that tract? Would any accepted Sale 257 bids have been rejected? Would the outcome of other sales have been affected?

After a 2-year comprehensive technical review of the delayed valuation methodology, BOEM intends to replace the delayed valuation methodology with a statistical lower bound confidence interval (LBCI) at a 90 percent confidence level as a decision criterion for accepting or rejecting qualified high bids on tracts offered in OCS oil and gas lease sales. Following extensive testing of the alternative approaches using both historical and current lease sale tract data and existing BOEM cash flow simulation models, BOEM determined that the LBCI approach would be the most appropriate substitute for the delayed valuation methodology. The LBCI is a statistical concept that captures the lower bound of a range of values encompassing the true unknown mean of the risked present worth of the resources at the time of the lease sale. The LBCI incorporates the uncertainty of parameters unique to the valuation of each OCS oil and gas lease sale tract. These parameters may include, but are not limited to, subsurface characterization of reservoir properties, cost and timing of the development, and projected revenues. Unlike the delayed valuation methodology, the LBCI approach would not require that BOEM estimate the time delay period between the current OCS oil and gas lease sale and the projected next lease sale. As such, BOEM finds the LBCI to be a better approach going forward.

BOEM published their Sale 257 Decision Matrix on Friday (2/24/2023), and my previous speculation regarding the rejected Sale 257 high bid has proven to be partially incorrect. The rejected high bid was submitted by BP and Talos and was for Green Canyon Block 777. BOEM’s analytics assigned a Mean of the Range-of-Value (MROV) of $4.4 million to that tract, which tied for the highest MROV for any tract receiving a bid. The BP/Talos bid was $1.8 million or just 40% of BOEM’s MROV. BOEM’s tract evaluation is interesting given that the other bid on this wildcat tract (by Chevron, $1.185 million) was considerably lower than the rejected BP/Talos bid.

The Sale 257 bid that I thought might have been rejected was for lease G37261. This lease was never issued per the lease inquiry data base and the final bid recap. BHP’s bid of $3.6 million for that tract (Green Canyon Block 79) was more than 5 times BOEM’s MROV of $576,000, and was accepted per the decision matrix. Why was the lease never issued?

Both Green Canyon 79 and 777 should again be for sale in legislatively mandated Sale 259, which will be held in just a few weeks on March 29, 2023, just 2 days prior to the deadline. It will be interesting to see what the bidding on those tracts looks like.

Meanwhile, Exxon and BOEM are still mum about the 94 Sale 257 oil and gas leases that Exxon acquired for carbon sequestration purposes.Note the large patches of blue just offshore Texas on the map above. These leases were all valued by BOEM at only $144,000 each, which is equivalent to the minimum bid of $25/acre. This valuation reflects the absence of perceived value for oil and gas production purposes. Exxon bid $158,400 for each tract, $27.50/acre or 10% higher than the minimum bid. Given that (1) the Notice of Sale only provided for lease acquisition for oil and gas exploration and production purposes, and (2) it was common knowledge that these tracts were acquired for carbon sequestration, should these bids have been rejected?

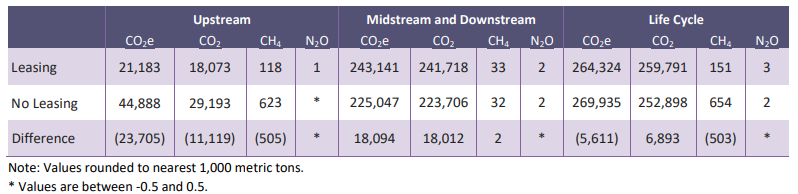

The Nord Stream sabotage likely released more methane than the complete lifecycle of a GoM lease sale (upstream and downstream). Also, the Nord Stream explosions may have released more methane than is emitted by all US offshore producers in an entire year. Here are the numbers:

lifecycle upstream emissions from a typical GoM lease sale (BOEM)

118

lifecycle up- and downstream emissions from a typical GoM sale (BOEM)

151

Finally, remember that offshore oil and gas leasing results in a net reduction in GHG emissions.

The No Leasing scenario results in roughly double the CO2e emissions for upstream activities compared to those of the Leasing scenario, given that, collectively, the substitute energy sources have higher GHG emissions per unit of production (also known as “GHG intensity”) compared to the forgone domestically produced OCS oil and natural gas of the Leasing scenario.

The National Academies of Sciences, Engineering, and Medicine will establish a standing committee to provide ongoing assistance to the Department of the Interior’s Bureau of Ocean Energy Management (BOEM) in its efforts to manage development of the nation’s offshore wind energy resources and their potential effects on fisheries

This seems to be a positive step and the committee members have excellent credentials, but how do you establish such a committee without any representation from the wind industry? Here are the 12 members of the committee.

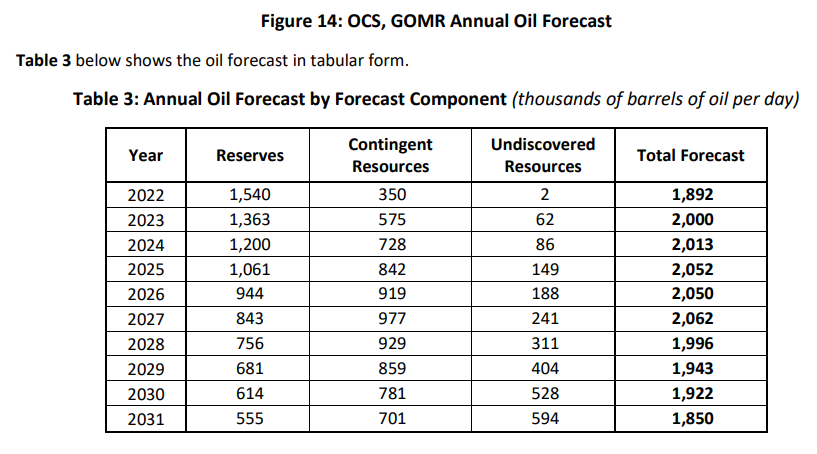

The EIA 2022 figure is spot-on, as it should be given that 10 months of 2022 production data are now in hand. However, BOEM’s 2022 forecast (published in July) missed the mark considerably. (In fairness to BOEM staff, their work was probably completed months before publication pending internal reviews.)

Of greater concern, given the policy implications, is the rosy BOEM forecast for the out-years. Despite historically low levels of leasing and exploratory drilling, BOEM forecasts oil production to exceed 2 million BOPD through 2027 and to remain well above the current (2022) level through 2031 (second table below).

While it’s unlikely that the whale strandings are the result of pre-construction activities for offshore wind development, greater transparency on the part of the developer and regulators would be helpful:

What surveys and other offshore activities are being conducted? Where?

What is the timeframe for these activities?

Any sightings of distressed whales?

Other anomalous observations?

Absent regular activity updates, accusations and protests are likely to continue and intensify.

Liz is an experienced attorney and leader in clean energy, climate change, and environmental law and policy. A member of the Biden-Harris administration since January 20, 2021, Liz has served as Senior Counselor to Secretary Haaland with an emphasis on water policy and climate change resilience. In this role, Liz also served as Chair of the Indian Water Rights Working Group, which manages, negotiates and implements settlements of water rights claims.

Prior to joining the Administration, Liz was Deputy Director of the non-partisan State Energy & Environmental Impact Center at NYU School of Law, which supports state Attorneys General addressing clean energy, climate, and environmental initiatives of regional and national importance. President Biden is the third President under which Liz has served at Interior, having worked for both the Clinton and Obama administrations. Under Secretaries Ken Salazar and Sally Jewell, Liz served as Interior’s Associate Deputy Secretary as well as Principal Deputy Assistant Secretary in the Office of Policy, Management and Budget. She was a key architect of the Obama Administration’s work to create a new offshore wind industry and leasing program.

Congratulations to Ms. Klein on being appointed to lead the Bureau of Ocean Energy Management. In addition to her commendable support for offshore wind energy, I trust that she appreciates the national importance of the OCS oil and gas program and the need for regular lease sales.

Did they write this news release with a straight face? Almost a shutout (could still be if the only bid is rejected). And they need 3 hours to process the results! 😉

That said, good for Hilcorp! They have a vision, and I hope they are successful.

As directed by the Inflation Reduction Act (IRA) of 2022, BOEM held Cook Inlet OCS Oil & Gas Lease Sale 258 on Friday, Dec. 30.

The reading of the bids was conducted via livestream. The lease sale is now concluded. One bid was received on one block. The bid, in the amount of $63,983, was submitted by Hilcorp Alaska LLC.

Final sale results are currently being processed and will be posted to this page by 1 p.m. Alaska Time.

Following today’s sale, there will be a 90-day evaluation process to ensure the public receives fair market value before a lease is awarded, and a Department of Justice review of antitrust considerations. If a lease is awarded it will be posted to BOEM’s website when the review process is completed.

Carbon-Zero US LLC of Dallas (a Cox Oil affiliate) has applied for up to $12 million in U.S. Department of Energy funds to develop a pilot sequestration hub in offshore storage fields about 20 miles from Grand Isle, according to officials from Cox Operating LLC, the Dallas operator that owns some of the storage fields.

Cox Operating LLC will “repurpose facilities and equipment” for the carbon storage project, according to a news release.

Should this company be authorized to repurpose Gulf of Mexico facilities for carbon sequestration?

Per BSEE Incident of Non-Compliance (INC) data for 2022, Cox had more component shut-in INCs (132) than any other company. Cox was second to the Fieldwood companies in the number of warning and facility shut-in INCs, and in the total number of INCs. 48% of the Cox INCs required either a component or facility shut-in.

Cox had an INC/facility-inspection ratio of 0.77, nearly 50% higher than the GoM average of 0.53.

Per the posted BSEE district investigation reports for 2022, Cox was responsible for 9 of the 30 incidents that were significant enough to require investigation. That is more than twice as many as any other company (next highest was 4).

The incidents included 3 serious injuries, 2 fires, a large gas leak, and oil spills of 114, 129, and 660 gallons. Per the posted reports, only one other company had an oil spill of >1 bbl. (Note: Only spills of > 1 bbl are routinely investigated by BSEE. One bbl = 42 gallons.)

While INCs were issued for only 3 of the 9 Cox incidents, a review of the reports suggests that INCs should have been issued for at least 4 of the other incidents.

Cox operates 375 platforms with installation dates as early as 1949. 134 of their platforms are > 50 years old. Only 66 were installed in the last 20 years and only 6 in the last 10 years (most recent December 2014). How will the carbon sequestration plans affect their massive decommissioning obligations?

Many of the Cox platforms were assigned by predecessor lessees. Those predecessors can only be held responsible for the decommissioning of facilities they installed, not for more recent wells or platforms and not for facilities that are repurposed for carbon sequestration.

Also, as noted in the discussion of Exxon’s 94 Sale 257 oil and gas leases, a competitively issued alternate use RUE is required (30 CFR § 585.1007) before sequestration operations may be conducted on an oil and gas lease.