The plaintiffs assert “insufficient and arbitrary environmental analyses, in violation of the National Environmental Policy Act (NEPA) and the Administrative Procedure Act (APA).” The court filing is attached.

All of this will have to be resolved in the next 3 weeks, as the congressionally mandated sale, scheduled for 27 September, (presumably) cannot be postponed.

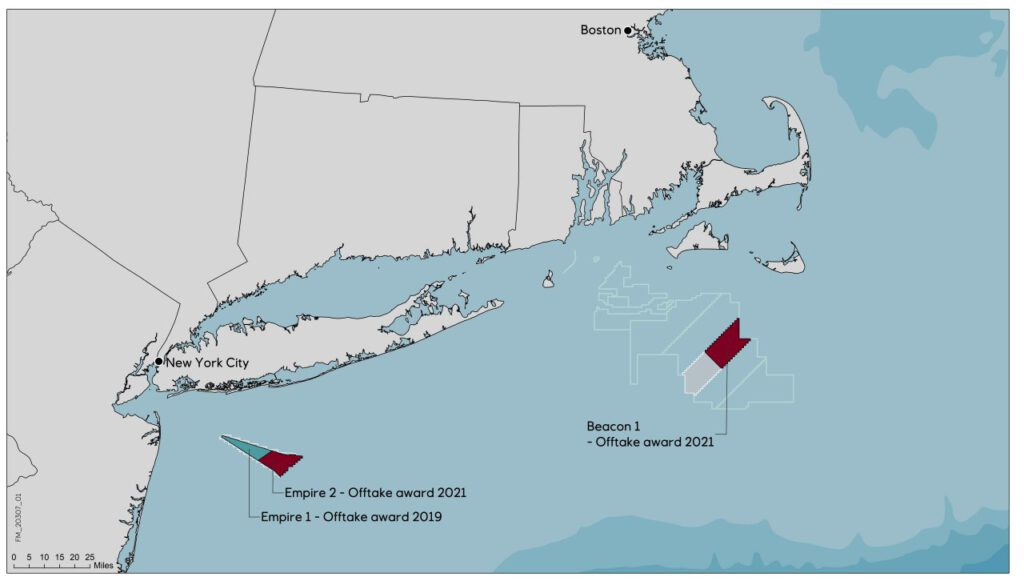

According to the New York State Energy Research and Development Authority, this would result in an average 54% price hike across their portfolio. The strike prices would rise from $118.38 to $159.64/MWh for Empire Wind 1, from $107.50 to $177.84/MWh for Empire Wind 2, and from $118.00 to $190.82/MWh for Beacon Wind.

This Court should grant Plaintiffs—the State of Louisiana, the American Petroleum Institute (“API”), and Chevron U.S.A. Inc. (“Chevron”)—a preliminary injunction and prevent those unlawful provisions from permanently disrupting the result of the fast-approaching lease sale (which Congress has directed must occur by September 30, and which cannot be delayed without causing Plaintiffs even more serious injury).

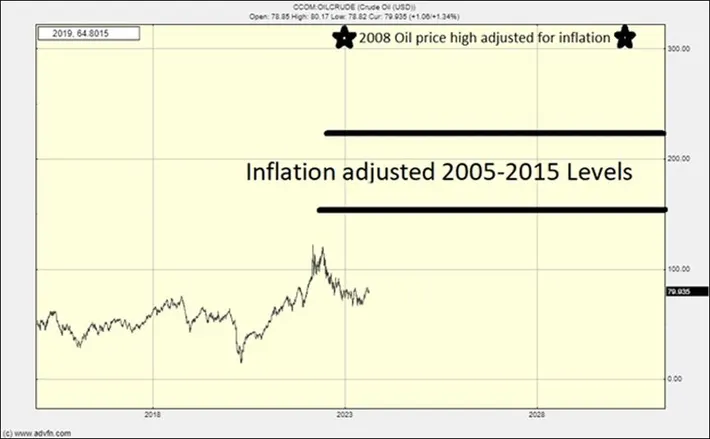

The title grabs your attention, but the justification isn’t terribly compelling. The author simply adjusts the brief 2008 price spike ($200/barrel) for inflation to justify his forecast.

Per the author:

The thing about commodities like oil is that while they can be acutely volatile because of supply and demand and political events, long term their price is a function of the technology needed to create them and the state of inflation in the denominating economy.

Unsurprisingly, Orsted management assumes no responsibility for the company’s poor performance, blaming supply chain problems, high interest rates and “a lack of new tax credits.” Outsiders might suggest that there were other factors such as irrational exuberance in the acquisition of wind leases at inflated prices, and unrealistic expectations regarding a complementary power source that is dependent on government mandates and subsidies.

“The situation in U.S. offshore wind is severe,” Chief Executive Mads Nipper told reporters on a conference call.

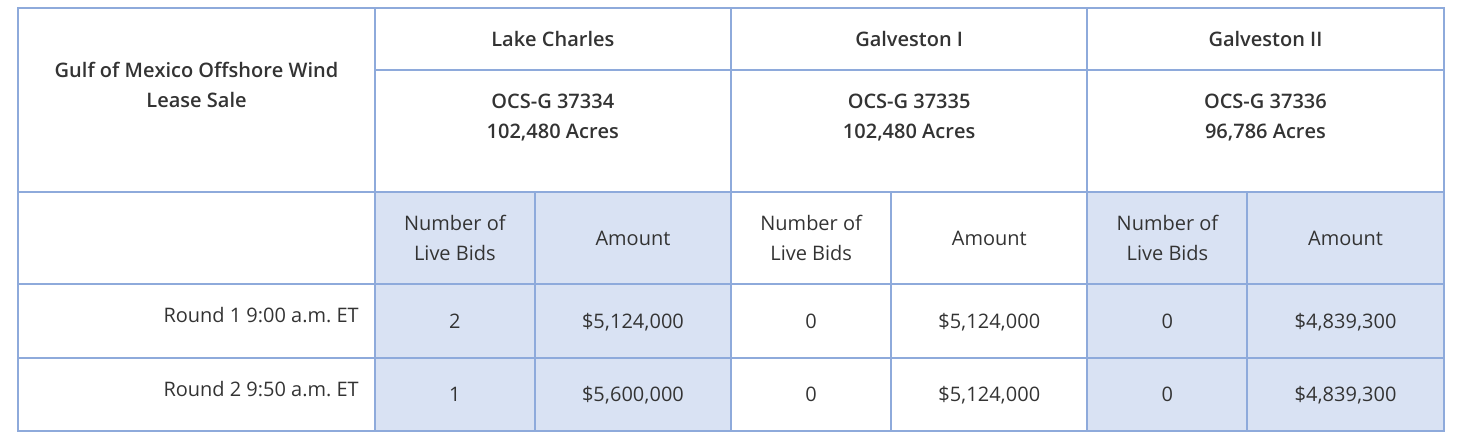

Only 1 of the 3 tracts was sold, and the amount bid was a modest $5.6 million. Given the extensive lease sale planning and promotion, this would seem to be a rather embarrassing outcome.

RWE Offshore US Gulf LLC won the Lake Charles tract. Neither of the 2 Galveston tracts received bids. RWE’s headquarters are located in Essen, Germany.

As a followup to the post on the sale of the Quissett estate, previously owned by the National Academies and used for conferences and meetings, the purchasers are William F Scannell and his wife Elizabeth A Scannell. Bill Scannell is President of Global Sales & Customer Operations at Dell Technologies.

The property was on the market for 2 years, and the purchase price was only about half of what NASEM was asking. NASEM must have really wanted to unload this great property which served the marine science community well for nearly 50 years