Danish Tax Minister Jeppe Bruus boasted that other countries will be inspired by the world’s first tax on livestock emissions.

Not so fast says the University of Nebraska; perhaps the cows deserve a tax credit! 😉

Danish Tax Minister Jeppe Bruus boasted that other countries will be inspired by the world’s first tax on livestock emissions.

Not so fast says the University of Nebraska; perhaps the cows deserve a tax credit! 😉

Posted in climate, energy policy | Tagged cow burps, Denmark, livestock emissions tax, Univ. of Nebraska | Leave a Comment »

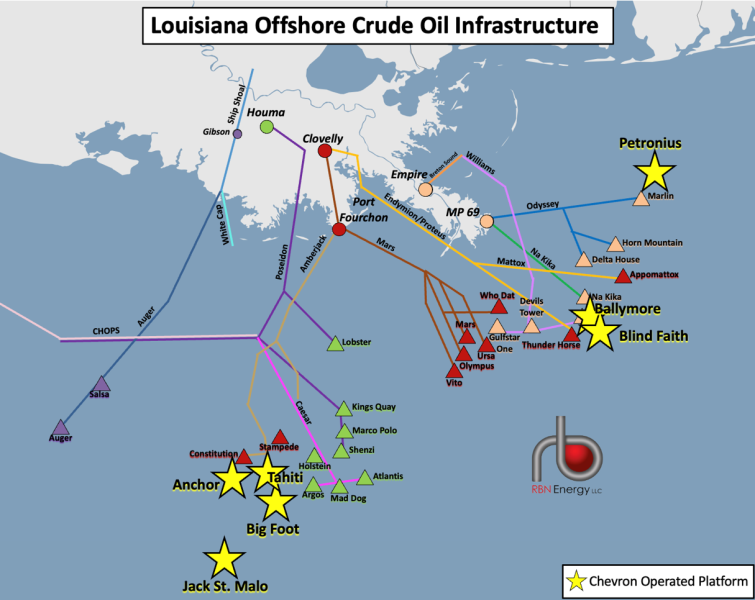

Reuters and others report that zinc from a new Chevron well has contaminated oil production destined for an Exxon refinery via Shell’s Mars Pipeline System. Because contaminated crude may cause maintenance issues and reduces the quality of refined products, Exxon will not accept crude from the Mars system until the zinc issue has been resolved.

The Mars system delivers about 575,000 bopd raising concerns about supplies to Gulf Coast refineries. But fear not, DOE authorized the delivery of up to 1 million barrels of oil from the Strategic Petroleum Reserve to the Exxon’s Baton Rouge refinery.

(Ironically, yesterday’s post pointed to the importance of the SPR and questioned the decision to drastically reduce crude oil purchases. This zinc incident is likely to be minor, and Exxon will repay the SPR in kind. However, more serious regional, domestic, and international events could call for much greater SPR withdrawals.)

The above map shows Chevron platforms that connect with the Mars system at Port Fourchon.

Speculation/commentary:

Posted in Gulf of Mexico, Offshore Energy - General | Tagged Anchor, Chevron, DOE, Exxon, Mars Pipeline System, Shell, Strategic Petroleum Reserve, zinc contamination | Leave a Comment »

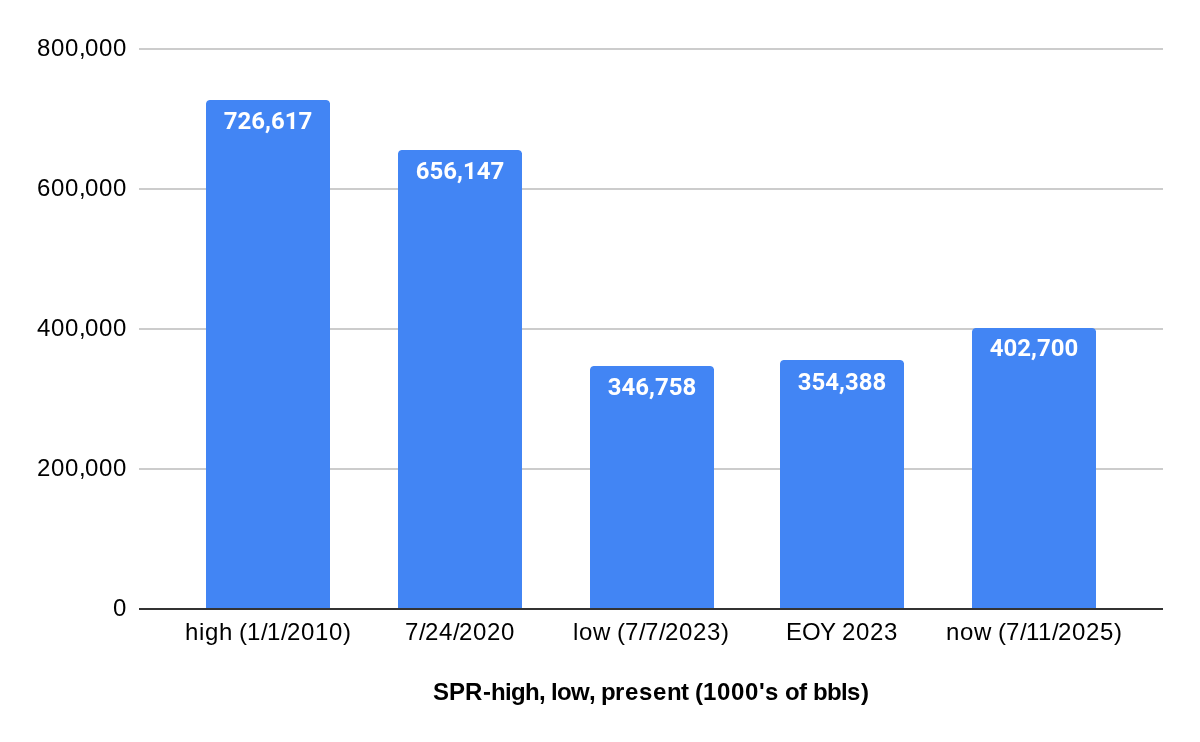

During the 2024 presidential campaign and early in his second term, President Trump repeatedly pledged to “immediately refill” the Strategic Petroleum Reserve (SPR) to its maximum capacity, emphasizing its role in ensuring energy security and stabilizing oil markets during global supply disruptions.

The Big Beautiful Bill (BBB) sends a much different message, providing only $171 million for petroleum acquisition and $218 million for maintenance of SPR facilities through 2029. This is an 87% reduction in the acquisition funding from the House version that proposed $1.3 billion for crude oil purchases.

The Administration has offered no comment on the BBB’s surprise SPR language. Meanwhile, the SPR will likely remain at or near the current level, which is 324 million bbls below the 2010 high and only 56 million bbls above the 2023 low. (See the above chart.)

Posted in energy policy | Tagged Big Beautiful Bill, funding reduction, refill, Strategic Petroleum Reserve | 2 Comments »

Nantucket reached a settlement agreement (attached) with turbine manufacturer GE Vernova (GEV), praising that company while criticizing Vineyard Wind (VW), the lessee and operator:

“The Town of Nantucket commends GE Vernova for its leadership in reaching this agreement. By contrast, the Town has found Vineyard Wind wanting in terms of its leadership, accountability, transparency, and stewardship in the aftermath of the blade failure and determined that it would not accept Vineyard Wind as a signatory to the settlement,” the town stated Friday morning.

Comments:

Posted in accidents, energy policy, Offshore Wind | Tagged GE Vernova, Good Neighbor Agreement, Nantucket, operator responsibility, settlement agreement, turbine blade failure, Vineyard Wind | Leave a Comment »

The main effect of the EPA ruling (attached) appears to be that permit appeals will be submitted to EPA rather than the State of Maryland.

Posted in Offshore Wind | Tagged EPA, Maryland, PSD permit, US Wind | Leave a Comment »

Why has the BSEE investigation report still not been issued?

Construction on the Vineyard Wind project continues yet important questions about quality control, regulatory departures, debris recovery, and environmental impacts remain.

Given the investigation’s significance, not only for Vineyard Wind, but for other offshore wind projects planned or under construction, how is the delay in issuing the report acceptable?

Keep in mind that the lengthy and complex National Commission, BOEMRE, Chief Counsel, and NAE reports on the Macondo blowout were published 6 to to 17 months after the well was shut-in.

Posted in accidents, Offshore Wind | Tagged anniversary, blade failure, BSEE, debris, departures, environmental assessment, investigation report, quality control, Vineyard Wind | Leave a Comment »

Tariffs and their uncertainty “will certainly decrease expected investment activity in the energy sector,” says the new report. More than $50 billion of offshore investment this year has been deferred “with operators looking to wait out current market uncertainty before making significant final investment decisions,” Rystad notes.

Rystad estimates that tariffs will increase costs for offshore oil and gas projects by 8% year-over-year and 12% for onshore. “Most steel and raw material exposed cost categories are feeling the majority of the impact from tariffs and thus will take the biggest hit.”

The Tax Foundation and Wood Mackenzie have offered similar opinions.

Comment: At a glance, the number of 2025 well starts in the GOA appears to be down (more on this at a later date). While there are many factors affecting drilling decisions, lower oil prices and higher costs associated with tariffs are not compatible with a “drill baby drill” philosophy.

Posted in drilling, energy policy, Offshore Energy - General | Tagged drill baby drill, oil and gas drilling, Rystad, tariffs | Leave a Comment »

The full report is attached.

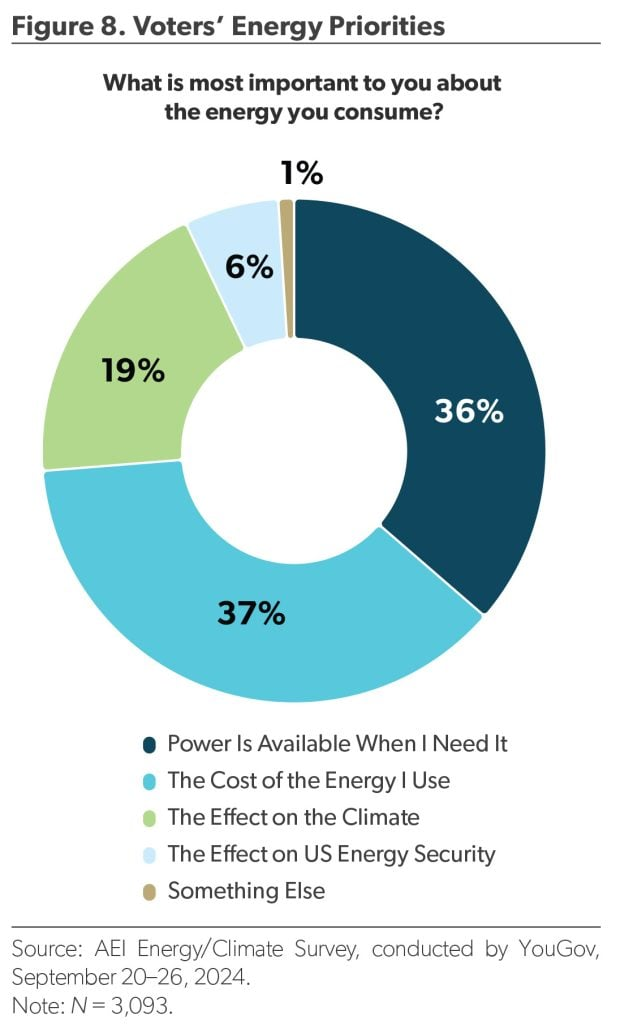

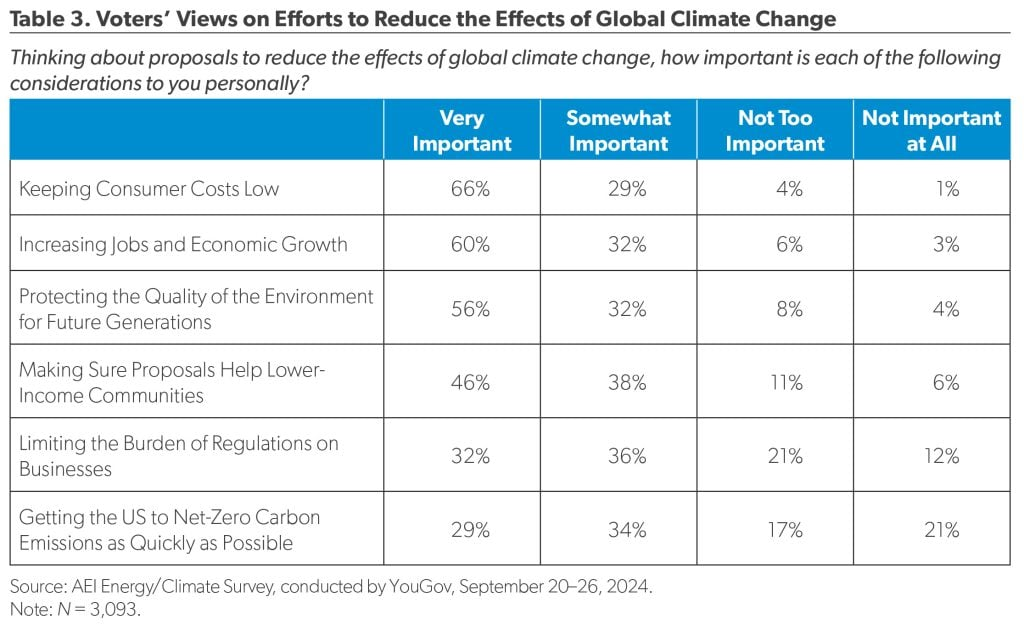

Not at all shocking:

The public is most interested in the cost and reliability of the energy they use and the convenience and comfort of their energy-using products. They are unwilling to sacrifice much at all financially to address climate change or significantly change their consumer behavior.

Posted in climate, energy policy | Tagged AEi, climate, energy cost, energy reliability, voters energy priorities | Leave a Comment »

The proposed rule is attached. Important points:

How can the US issue mining licenses in international waters (controversial)?

“The International Seabed Authority (ISA) regulates deep seabed mining in areas beyond national jurisdiction for countries that are parties to the United Nations Convention on the Law of the Sea (UNCLOS). The United States is a non-party to UNCLOS. Under U.S. law, NOAA may issue licenses and permits to U.S. citizens in areas beyond national jurisdiction under the Deep Seabed Hard Mineral Resources Act (DSHMRA).“

Main objective of the proposed rule (paraphrased):

The deepsea mining industry has gained experience from site specific exploration activities. As a result, later entrants may be able to capitalize on the information gained by previous explorers and lessen the need for further exploration of previously explored areas. In such cases there may be a need for a consolidated licensing process in which permit applicants could meet exploration license requirements to establish priority of right, and permit requirements, simultaneously.

Comment: The proposed rule seems reasonable in that qualified companies that gather the necessary site information would have the right (after NOAA review and approval) to collect the minerals. This would align deepsea mining more closely with offshore oil and gas in that companies acquiring licenses would be able to proceed to production after regulatory approvals.

Posted in deep sea mining, energy policy | Tagged consolidated licensing, deepsea mining, DSHMRA, NOAA, UNCLOS | Leave a Comment »

See the differences in the OCS oil and gas provisions in the House and Senate versions.

We preferred the House version, but the Senate Parliamentarian killed the provisions that reduced the risk of litigation and processing delays.

Whether justified or not, the royalty rate is now capped at 1/6 and a 10-year deepwater lease term is locked in.

The favorable terms and assurance of regular GOA lease sales put the ball squarely in industry’s court. We are looking for a good showing at Sale 262, including some new bidders and the return of some prominent companies.

Posted in energy policy, Offshore Energy - General, Regulation | Tagged Big Beautiful Bill, energy policy, Gulf of America, lease sale 262 | Leave a Comment »