When we (MMS) drafted the OCSLA amendments (incorporated into the Energy Policy Act of 2005) that authorized offshore wind operations, we envisioned complementary and synergistic programs. Offshore wind and oil/gas development have many similarities and a common purpose – energy production. There is considerable overlap among the operating companies and contractors.

Unfortunately, politicians are better at dividing than uniting, and a provision in the Schumer-Manchin legislation pits the offshore wind and oil/gas programs against each other. The text (pasted below) from p. 646 of the bill restricts wind leasing when no oil and gas lease sale has been held in the prior year.

I share the concerns about the OCS program evolving into a wind-only program, as has already happened in the Atlantic (more on this at a later date). However, oil and gas sales should be held because they make economic and environmental sense, not because they are a condition for holding wind sales. Oil and gas sales are not punishment and wind sales are not rewards, and holding a single GoM lease sale each year does not balance the offshore program.

(b) LIMITATION ON ISSUANCE OF CERTAIN LEASES OR RIGHTS-OF-WAY.—During the 10-year period beginning on the date of enactment of this Act—

(2) the Secretary may not issue a lease for offshore wind development under section 8(p)(1)(C) of the Outer Continental Shelf Lands Act (43 U.S.C.1337(p)(1)(C)) unless— (A) an offshore lease sale has been held during the 1-year period ending on the date of the issuance of the lease for offshore wind development; and (B) the sum total of acres offered for lease in offshore lease sales during the 1-year period ending on the date of the issuance of the lease for offshore wind development is not less than 60,000,000 acres.

If last fall’s Hurricane Ida dip is excluded, the latest production figure in 2021/2022. New projects should boost production over the next 2 years, but not enough to reach the August 2019 peak of 2.044 million bopd.

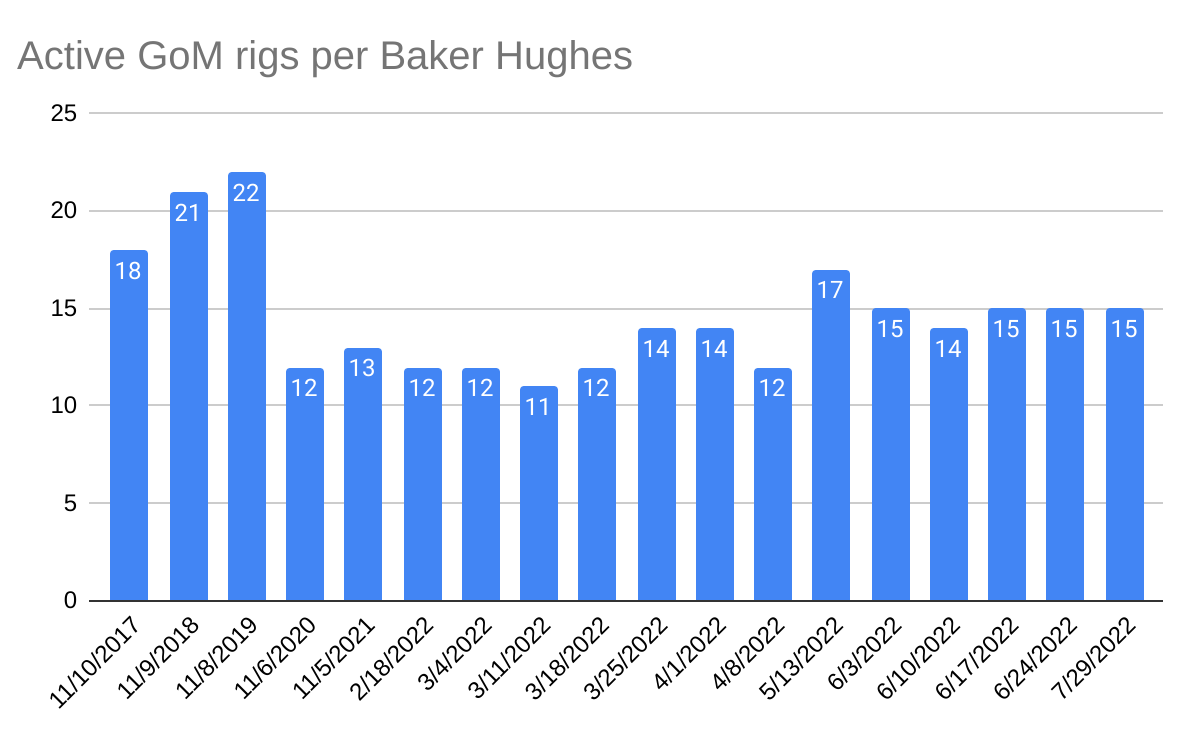

Meanwhile the GoM rig count remains sluggish at 15.

The energy sections begin on page 232 and continue until the end (page 725!). Some highlights from an offshore energy perspective (more important items in bold):

p. 429 – Tax credit eligibility for offshore wind energy components including blades, nacelles, foundations, and towers.

p. 447 – Credits for CCS equipment

p. 460 – For offshore wind facilities, this section specifies the % of the total costs that must be expended in the US for the facility to qualify as being manufactured in the US. That % rises gradually to 55% after 12/31/2027.

p. 518 – Eligibility of CCS for credits

p. 615 – $100 million for offshore wind electricity transmission planning, modelling, and analysis. (Seems like a lot for planning and analysis.)

p. 621 – $10 million for oversight by DOE Inspector General. (Those folks will have their hands full!)

p. 628 – Authorizes wind leasing in the EGOM and South Atlantic areas withdrawn from all leasing at the end of the Trump administration.

p. 631 – Authorizes offshore wind leasing adjacent to US territories. (Should be interesting!)

p. 632 – Codifies increase in offshore royalty rates: range of 16 2/3% – 18 3/4% for 10 years; not less than 16 2/3 % thereafter

p. 640 – The provision requiring that royalty be paid on flared/vented gas could be problematic. The exceptions are not consistent with those currently in the regulations, and would be difficult for BSEE/ONRR to manage. The proposed legislation (exception 1) exempts “gas vented or flared for not longer than 48 hours in an emergency situation that poses a danger to human health, safety, or the environment.” However, current BSEE regulations allow limited (48 hours cumulative) flaring for certain operations (e.g. during the unloading or cleaning of a well, drill-stem testing, production testing, and other well-evaluation testing). This flaring is essential but not normally an emergency situation. Requiring royalty payments for such essential, but not emergency, flaring would be unreasonable and inconsistent with the intent of this provision (minimize unnecessary flaring and venting).

p. 641 – Per our previous post, this section reinstates Lease Sale 257 (GoM) and requires that the scheduled 2022 lease sales 258 (GoM) and 259 (Cook Inlet) be held by 12/31/2022. Lease Sale 261 (GoM) must be held by 9/30/2023. Saddle up!

(b) LEASE SALE 257 REINSTATEMENT.— (1) ACCEPTANCE OF BIDS.—Not later 30 days after the date of enactment of this Act, the Secretary shall, without modification or delay— (A) accept the highest valid bid for each tract or bidding unit of Lease Sale 257 for which a valid bid was received on November 17, 2021; and (B) provide the appropriate lease form to the winning bidder to execute and return.

The platform was supported by an attendant barge that provided living quarters and equipment and materials needed for the drilling operations. This was reportedly the first drilling tender.

BSEE’s borehole file records indicate that 31 wells were drilled on this block beginning in September 1947.

BOEM’s production file shows initial production rates of 7000 to 10,600 bbls of oil per month. The accuracy of these old data is uncertain.

This was reportedly the first time drilling crews worked 12-hour tours for seven days and then rotated to shore for seven days off.

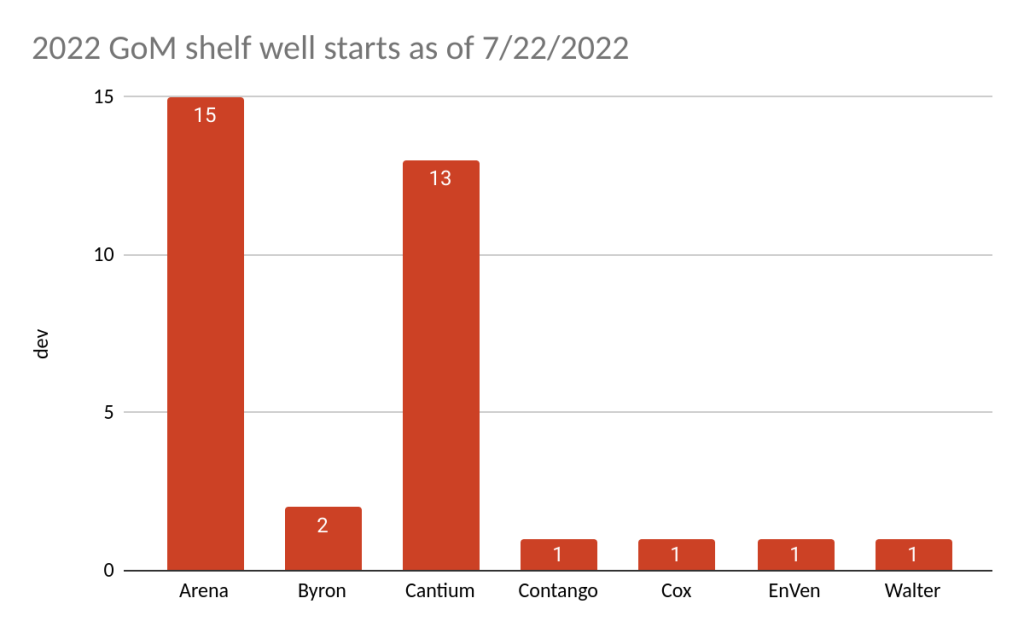

Without much hype, shelf operators continue to find and extract oil and gas from beneath the shallow waters of the GoM. The 1700 shelf platforms that remain provide energy for our economy and important hardbottom substrate for marine life. Keep it going! Only 25 more years until the 100th anniversary! 😀

Foremost energy experts like Daniel Yergin understand that oil and gas will be critical to our economy and security for decades, and that offshore production is an important component of our energy supply chain. Unfortunately, our massive outer continental shelf has, from an oil and gas standpoint, been effectively reduced to the central and western GoM.

Opportunities in the GoM are being seriously constrained by the extended pause in leasing. A lease sale has not been held for 615 days, the longest US offshore leasing gap since the 1950’s.

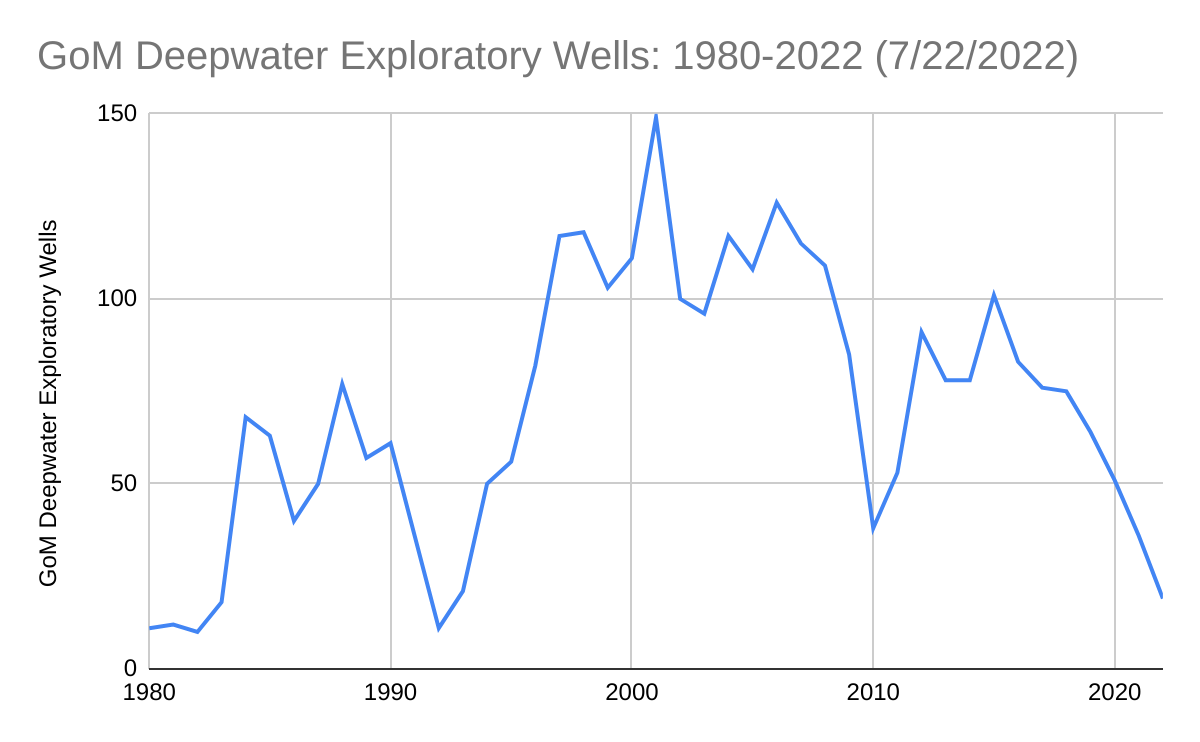

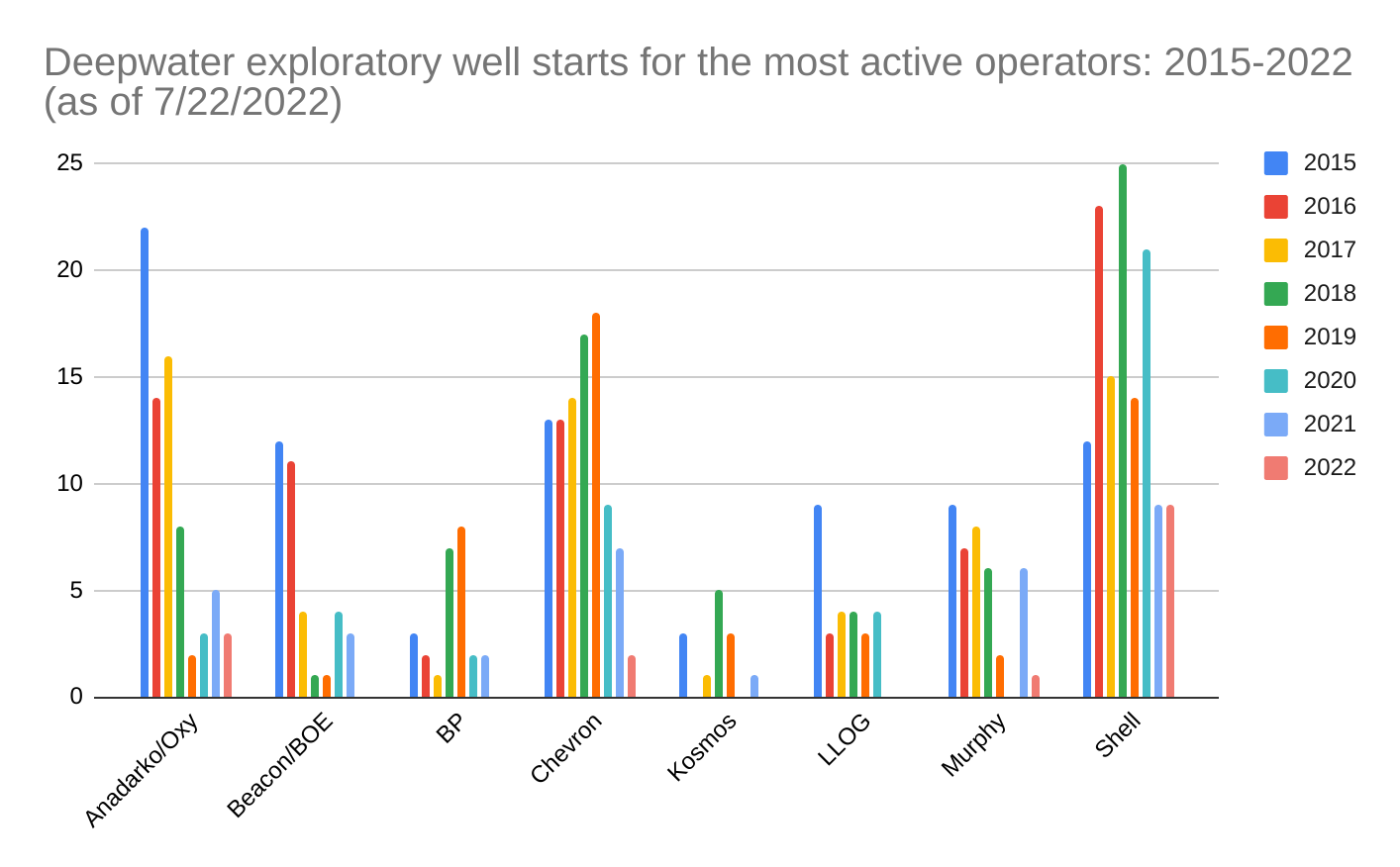

Reserve replacement and sustained production are dependent on exploration. The charts below illustrate the decline in GoM exploratory drilling and the reduced activity by some of the more important operating companies.

Per BSEE data, the number of exploratory well starts averaged only 3/month for the last 18 months (chart 2). This level of activity is the lowest since the early days of deepwater operations (chart 1). There was even more drilling during the post-Macondo moratorium (2010-2011).

ConocoPhillips and Exxon have not drilled a GoM exploratory well since 2016 and 2018 respectively. Activity by other operators has also declined significantly (chart 3). BP has not spudded an exploratory well since Sept. 2021.

…that the SPR legislation authorized the sale of large volumes of oil for the purpose of easing worldwide prices. Per section 151 of the statute, which was passed following the oil embargoes in the 1970’s, the SPR was intended todiminish the vulnerability of the United States to the effects of a severe energy supply interruption.

…that SPR oil could be sold to all entities including Chinese companies that are also buying oil from Russia, the country being boycotted. How absurd is that? (The confirmation of one such transaction is pasted below.)

Good article from our friends at the Petroleum Safety Authority of Norway. When old guys reminisce, people need to listen 😉

“Reagan feared that the world, and especially Europe, would become too dependent on Soviet gas, and saw Troll as an opportunity to create greater independence.”

“Lerøen sees parallels to the current situation, with Russia’s invasion of Ukraine, and the importance Norwegian gas has for the EU, which wants to become independent of Russian gas.”

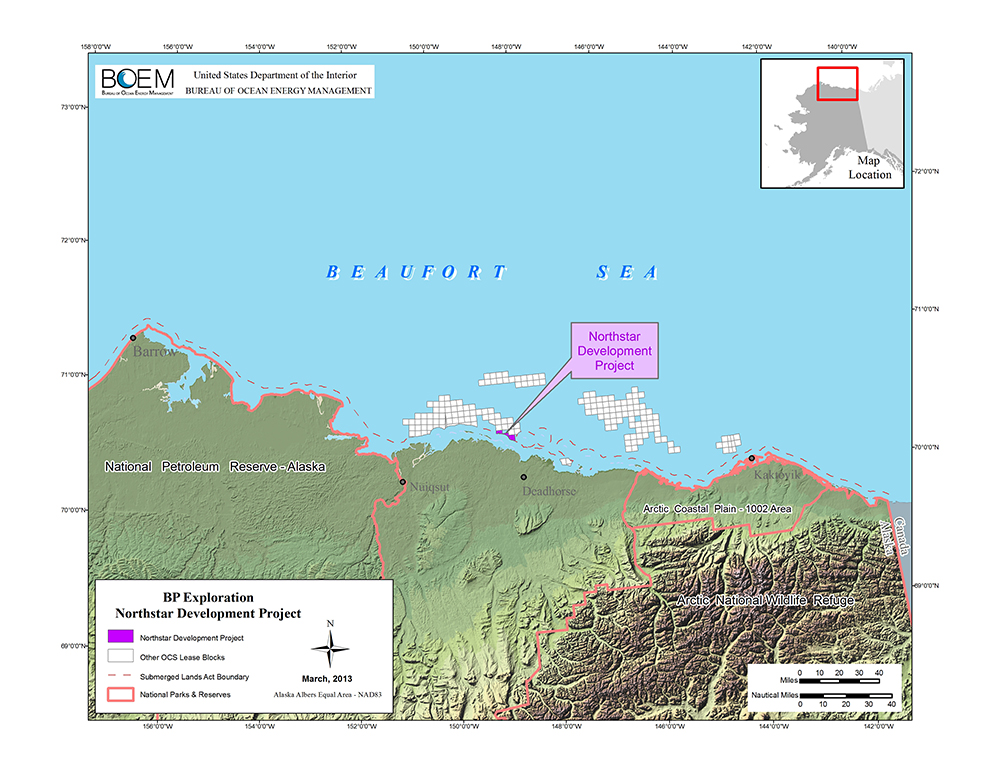

The only current Alaskan OCS production is from Northstar, a joint State-Federal Unit in the Beaufort Sea. The production island is in State waters, but 7 of the wells produce from the Federal sector. The field was originally developed by bp, but Hilcorp is the current operator. To date, BSEE has conducted 5 inspections of the facility in 2022, and no incidents of noncompliance (INCs) were identified.

Per BOEM records, 4 companies operate Pacific (California) OCS facilities that are currently producing. Three of those operators have superior 2022 inspection records. No INCs were issued to either Exxon (11 Santa Ynez Unit inspections) or Freeport-McMoRan (24 Platform Irene inspections). Only 2 warning INCs were issued during 12 inspections of Beta Operating Co. platforms Ellen, Elly, and Eureka in the Beta Unit offshore Long Beach.