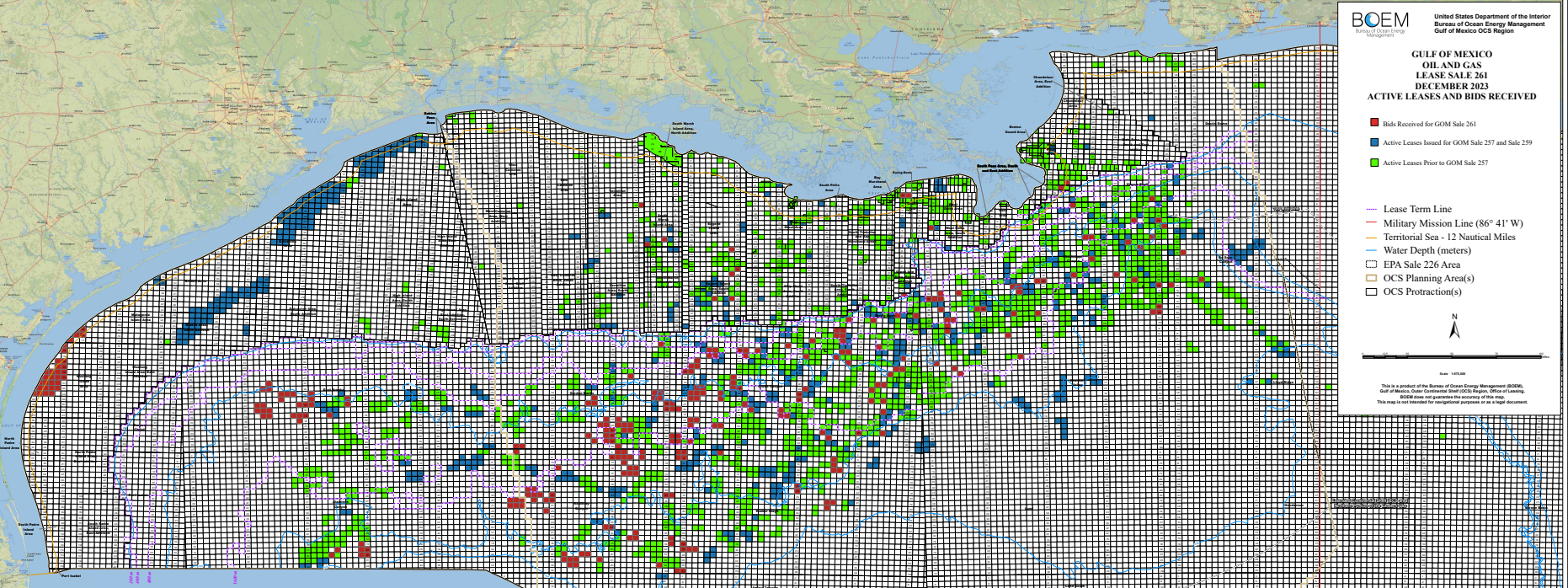

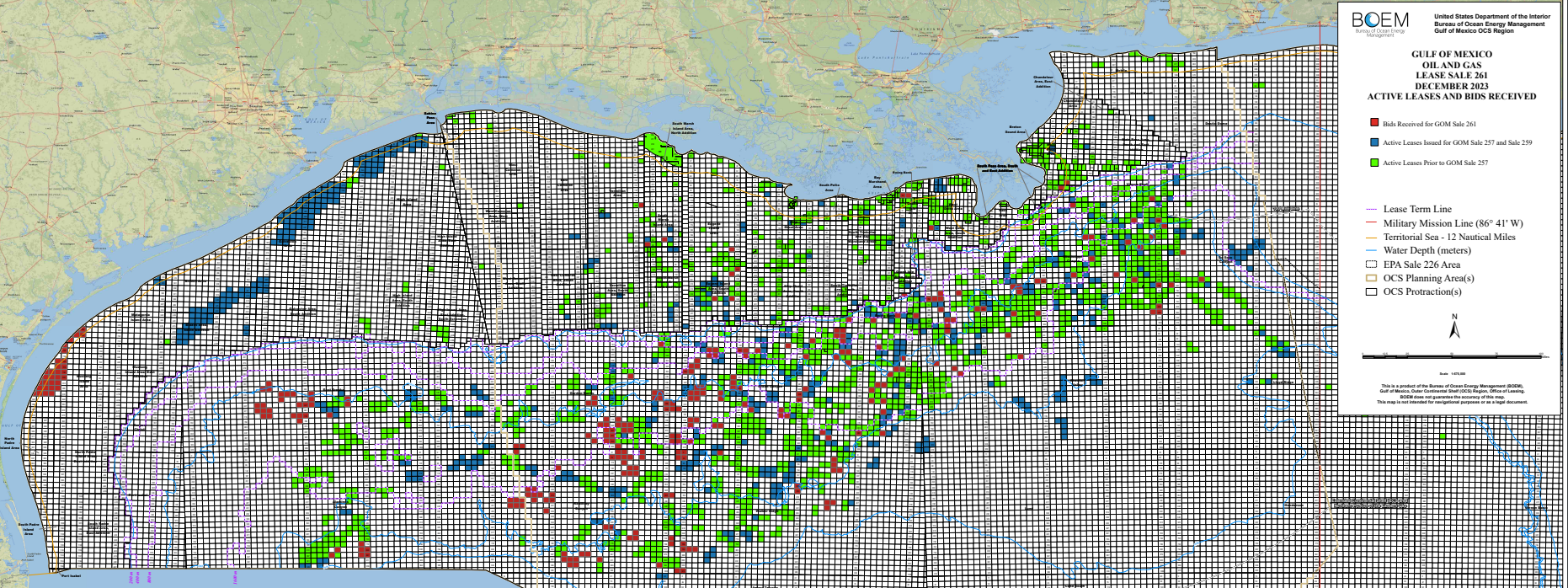

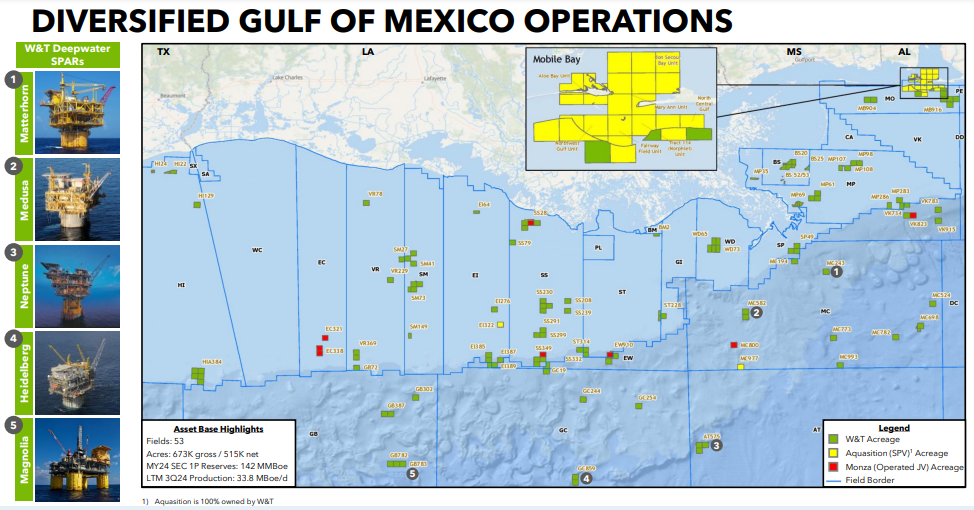

W&T (lease and facility map above) claims that insurers have colluded to damage the company by jointly demanding additional collateral and premiums.

Comments on excerpts from the W&T press release follow:

“At the heart of the dispute are rules from the federal Bureau of Ocean Energy Management – BOEM – which require energy producers in the Outer Continental Shelf to provide a bond to pay for well, platform, pipeline and facilities cleanup if the operating company fails to do so.”

Comment: Despite disagreeing with aspects of the BOEM financial assurance rule, this blog has defended the rule against unfair criticism. Better solutions are achievable, but that will require industry leaders from all factions to come to the table with a commitment to reach a balanced agreement that protects the public interest.

“These insurance companies and their unreasonable demands for increased collateral pose an existential threat to independent operators like W&T.”

Comment: If insuring offshore decommissioning is so risk-free and lucrative, why aren’t other companies entering the market?

“Several states, including Texas, are challenging the BOEM rule and in one case they specifically cite W&T as an example of how the rule could be misused to irreparably harm energy producers.“

Comment: As previously posted, the concerned States should propose alternative solutions that would promote production while also protecting taxpayer interests. Arguing that decommissioning financial risks are not a problem is neither accurate nor a solution.

“In over 70 years of producer operations in the Gulf of Mexico, the federal government has never been forced to pay for any abandonment cleanup operations associated with well, platform facility, or pipeline operations.”

Comment: Shamefully, from the standpoints of both the offshore industry and the Federal government, that statement is no longer true. The taxpayer has now funded decommissioning operations in the Matagorda Island Area offshore Texas (BSEE photo below) and more significant decommissioning liabilities loom.

Other thoughts:

- To what extent, if any, has W&T’s acquisition of certain Cox assets contributed to their increased insurance costs?

- My comments and John Smith’s comments on the BOEM’s draft financial assurance rule, which was essentially unchanged when published in final form, are relevant to this discussion.

- Also noteworthy in this discussion are BOEM’s lax financial assurance requirements for wind facility decommissioning. Has BOEM’s promotion of offshore wind influenced their financial assurance decisions, increasing the risks to taxpayers in the process?